Solutions for Chapter 17

Payout Policy

1. a. May 7: Declaration date

b. The stock price will fall on the ex-dividend date, June 7. The price falls on this day

c. The annual dividend is $0.075 4 = $0.30.

d. The percentage payout rate was $0.30/$1.90 = 0.1579 = 15.79%.

2. a. True

b. True. The effective rate can be less than the stated rate because the realization of gains

c. True. Research shows changes in dividends are more relevant than the actual amount.

d. False. The repurchase program announcement may signal that managers have no good

e. False. Stock dividends increase the number of shares, but cause dilution of value to

17-1

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

3. a. 1,000 1.25 = 1,250 shares

b. Price per share will fall to $100/1.25 = $80.

c. A 5-for-4 split will have precisely the same effect on price per share, shares held, and

4.

a. True.

b. False. The most common method is via open-market repurchase.

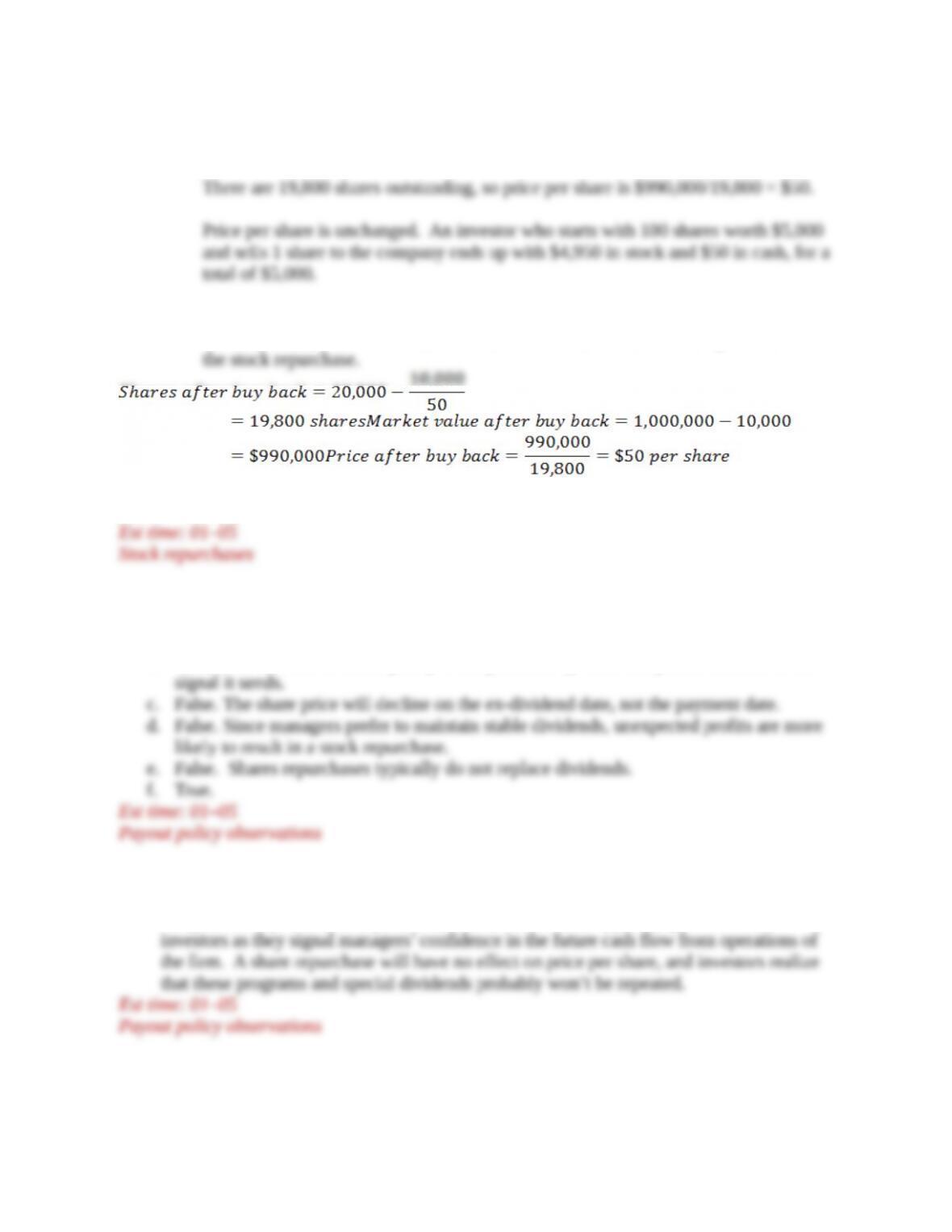

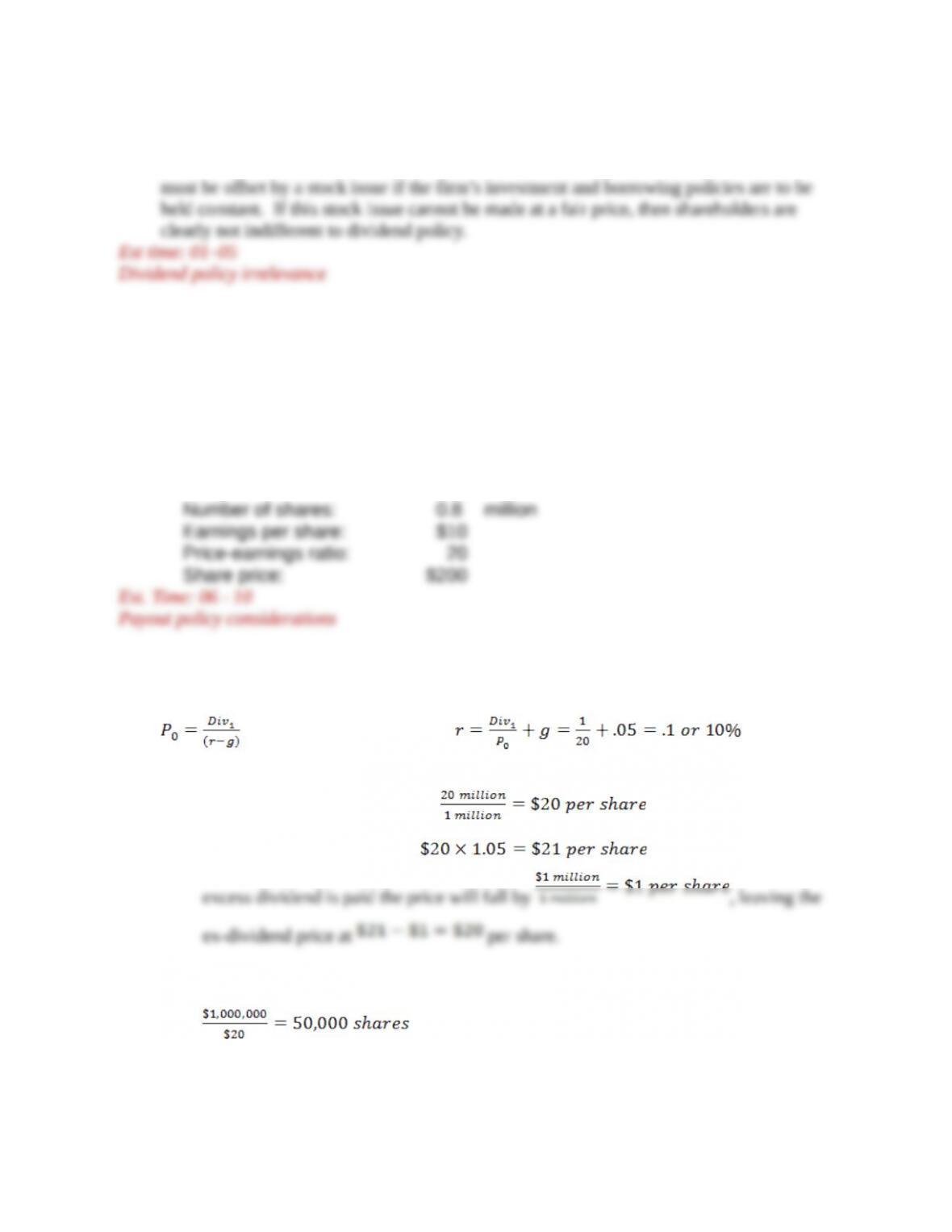

5. a. P = $1,000,000/20,000 = $50

b. The price tomorrow will be $0.50 per share lower, or $49.50.

6.

17-2

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

a. After the repurchase, the market value of equity falls to $990,000, and the number of

shares outstanding falls by $10,000/$50 = 200 shares.

b. If the firm pays a dividend, the investor would have 100 shares worth $49.50 each

and $50 cash, for a total of $5,000. This is identical to the investor’s position after

7.

a. False. 55% of all companies pay neither a cash dividend nor a stock repurchase.

b. False. The residual dividend policy is not practiced by most companies because of the

8. The announcement of an increase in Growler Corporation’s regular dividend would have

the greatest impact on stock price. Dividend increases are typically good news for

17-3

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

9. Dividend increases are typically good news for investors as they signal managers’

confidence in the future cash flow from operations of the firm. A dividend cut conveys a

10. Facebook is known as a growth company. As such, the company reinvests its earnings

instead of paying a dividend. This implies the company is producing positive NPVs. This

11.

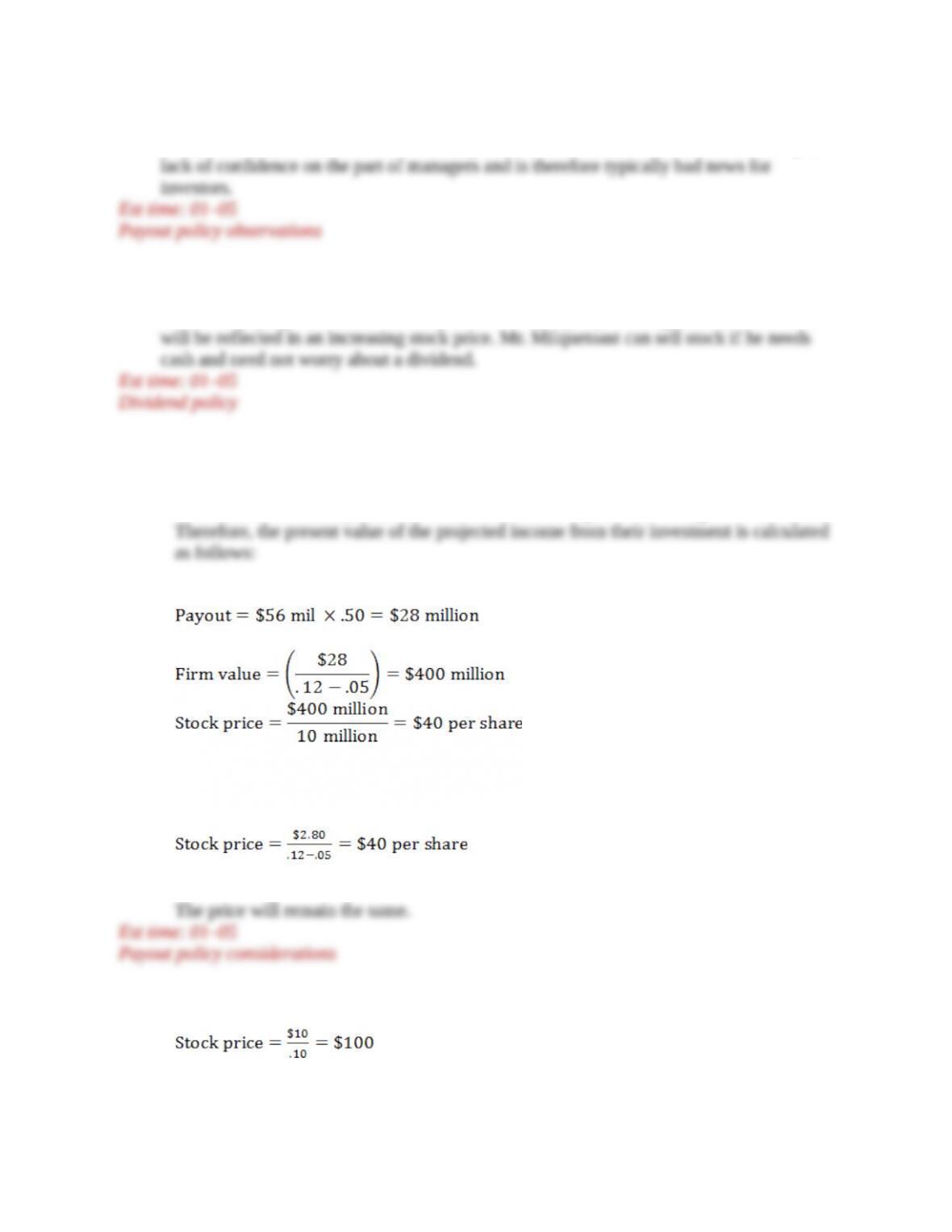

a. Under the current repurchase plan, stockholders will sell half of their shares this year for

$28 million. In future years, their total income from repurchases will grow at a 5% rate.

b. Dividends per share this year will be $2.80, and they are projected grow at a rate of 5%.

Therefore,

12.

a.

17-4

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

b.

c.

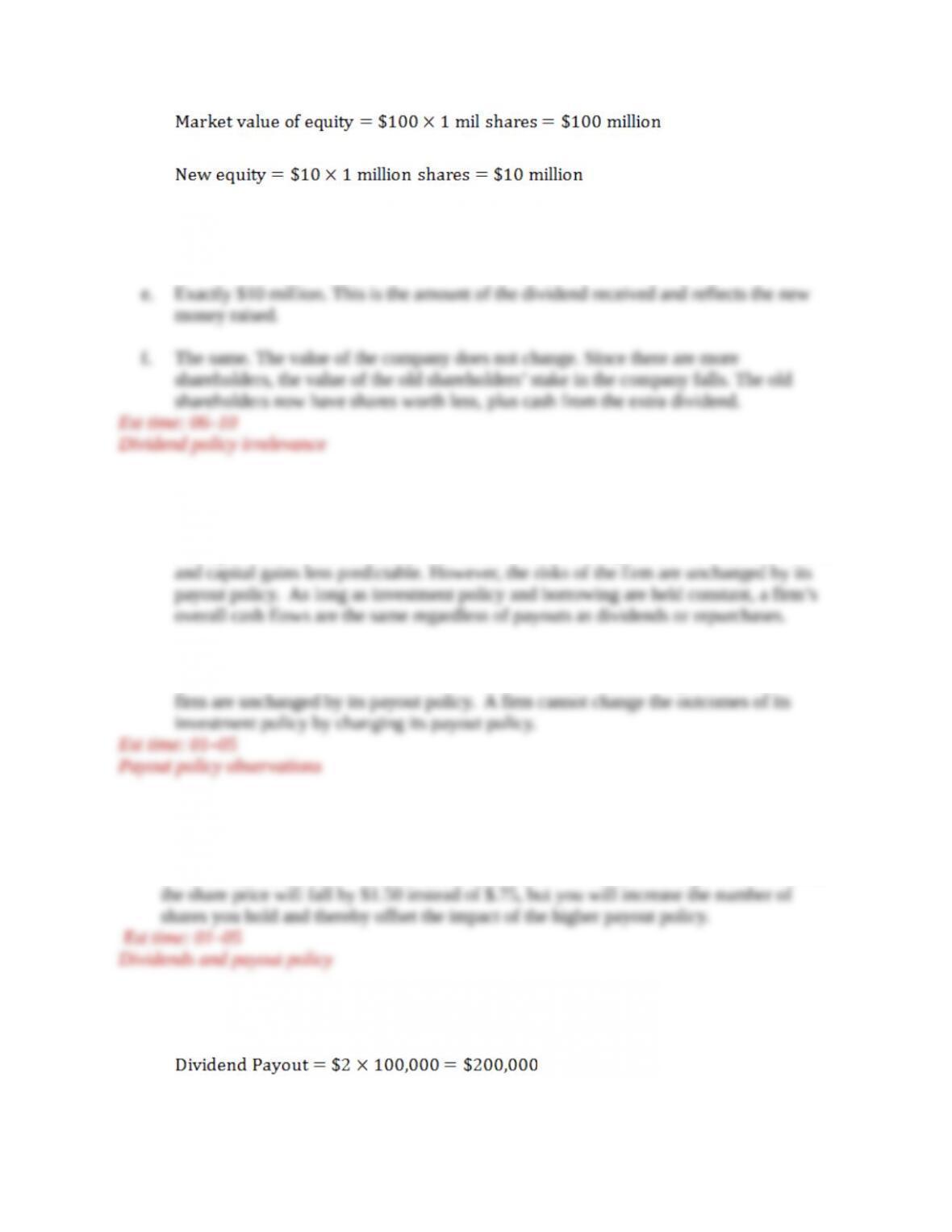

d. The present value of the new shares will need to be $10 million, since that is the amount

of the investment.

13.

a. The risk in the firm is determined by the variability in cash flows, not payout policy.

Managers can stabilize dividends and cannot control stock prices, so dividends are stable

b. The causation in this statement is reversed: Safer companies pay more generous

dividends because their forecast cash flows are more predictable. Again, the risks of the

14. Your dividend income will increase from $1,500 to $3,000. If you view the dividend as

excessive, you can invest the extra $1,500 in the firm. When the stock goes ex-dividend,

15.

a.

17-5

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

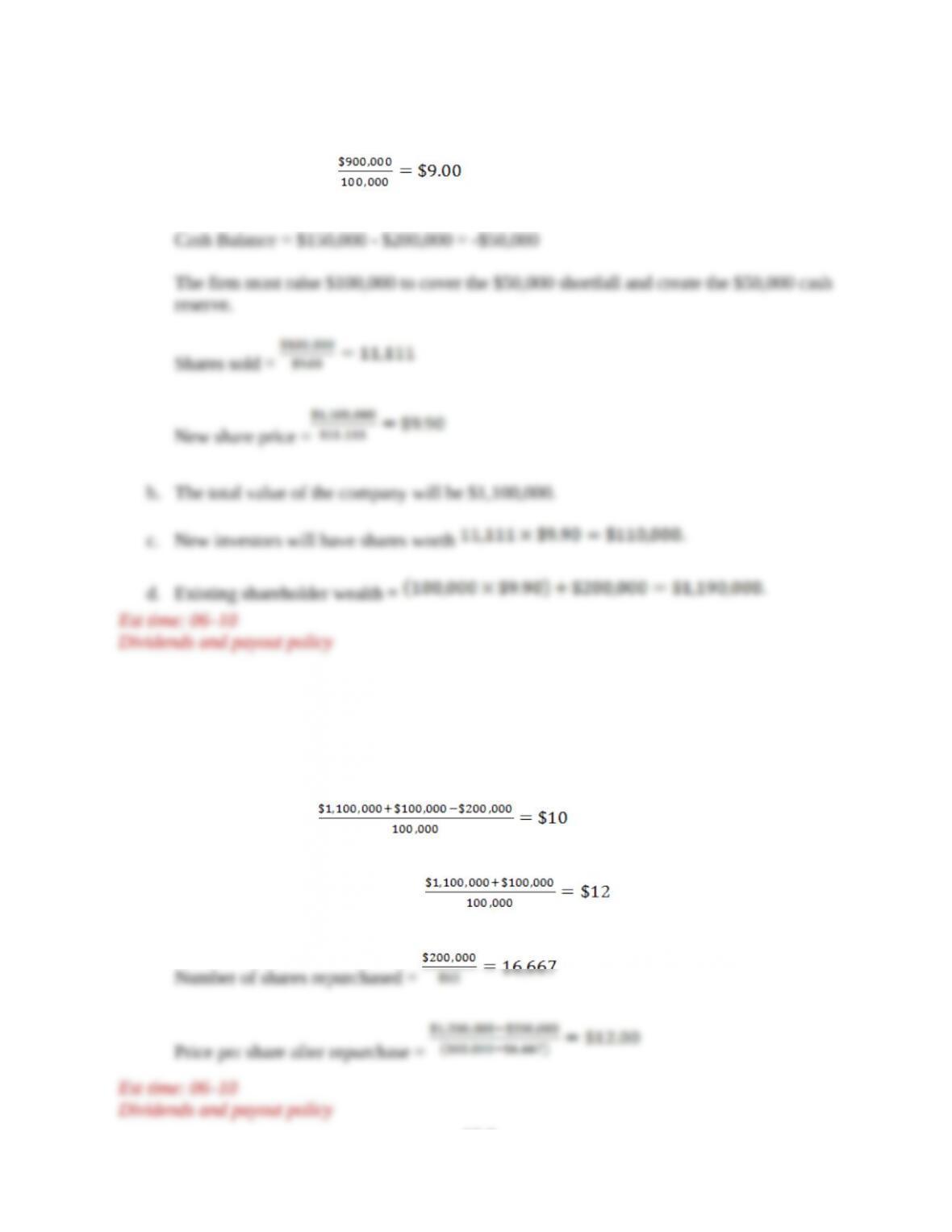

The value of the equity drops to $900,000 = $1,100,00 – $200,000

The price per share =

16.

a. Price per share =

b. Price per share after windfall =

17-6

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

17.

a.

b. The firm value after announcement does not change. It remains constant at $500,000.

18.

At a price of $8.00, the firm will need to sell 12,500 shares.

The new price per share =

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

If shares are issued at $8 per share, then the new shareholders are getting a bargain, i.e.,

the new shareholders win and the old shareholders lose. Any increase in cash dividend

19. One problem with this analysis is that it assumes the company’s net profit remains

constant even though the asset base of the company shrinks by 20%. That is, in order to

raise the cash necessary to repurchase the shares, the company must sell assets. If the

assets sold are representative of the company as a whole, we would expect net profit to

decrease by 20% so that earnings per share and the P/E ratio remain the same. After the

repurchase, the company will look like this next year:

Net profit: $8 million

20. It is useful to first calculate the required return on the equity to facilitate valuations of the

company’s stock. We can find the required return by solving for “r” in the growing

perpetuity formula:

rearranged to solve for “r”,

a. The price of Little Oil today is: .

In one year, the price will be , however once the

b. To raise the additional $1 million to fund the dividend, the firm will need to issue:

17-8

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

c. With the additional issue, shares outstanding will be 1,050,0000 after year 1.

d. The new schedule of dividends is $2.0 in year 1, $1.0 in year 2, $1.05 in year 3, and

so on at 5% growth. Using the discount dividend model:

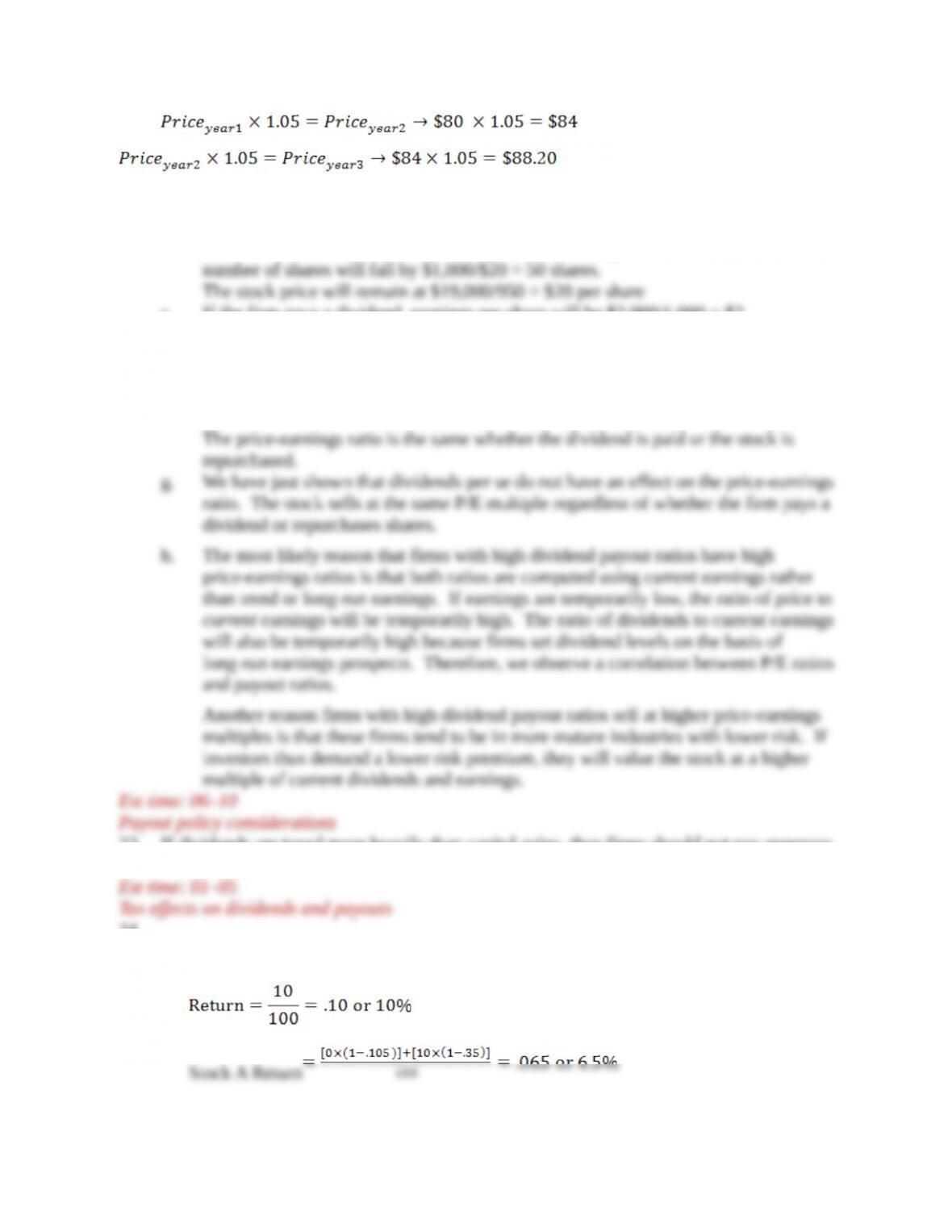

21. a. There will be no immediate effect on the stock price. Absent tax effects or signaling,

b. The firm will purchase at a price of $84 per share and they have $4 to fund the

c. In the case of a dividend repurchase, the stock price will remain at $80 immediately

following the ex-dividend date each year.

17-9

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

22.

a.If the firm pays a dividend, the stock price will fall to $19 per share.

b. If the firm repurchases stock, the market value of equity will fall to $19,000 and the

c. If the firm pays a dividend, earnings per share will be $2,000/1,000 = $2.

a. If the firm repurchases stock, then EPS = $2,000/950 = $2.105.

e. If the dividend is paid, the price-earnings ratio will be $19/$2 = 9.50.

f. If the stock is repurchased, the price-earnings ratio will be $20/$2.105 = 9.50.

23. If dividends are taxed more heavily than capital gains, then firms should not pay generous

cash dividends.

24.

a.

i. A pension plan pays no taxes and earns the same on all investments.

ii. Corporation

17-10

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

iii. Individual

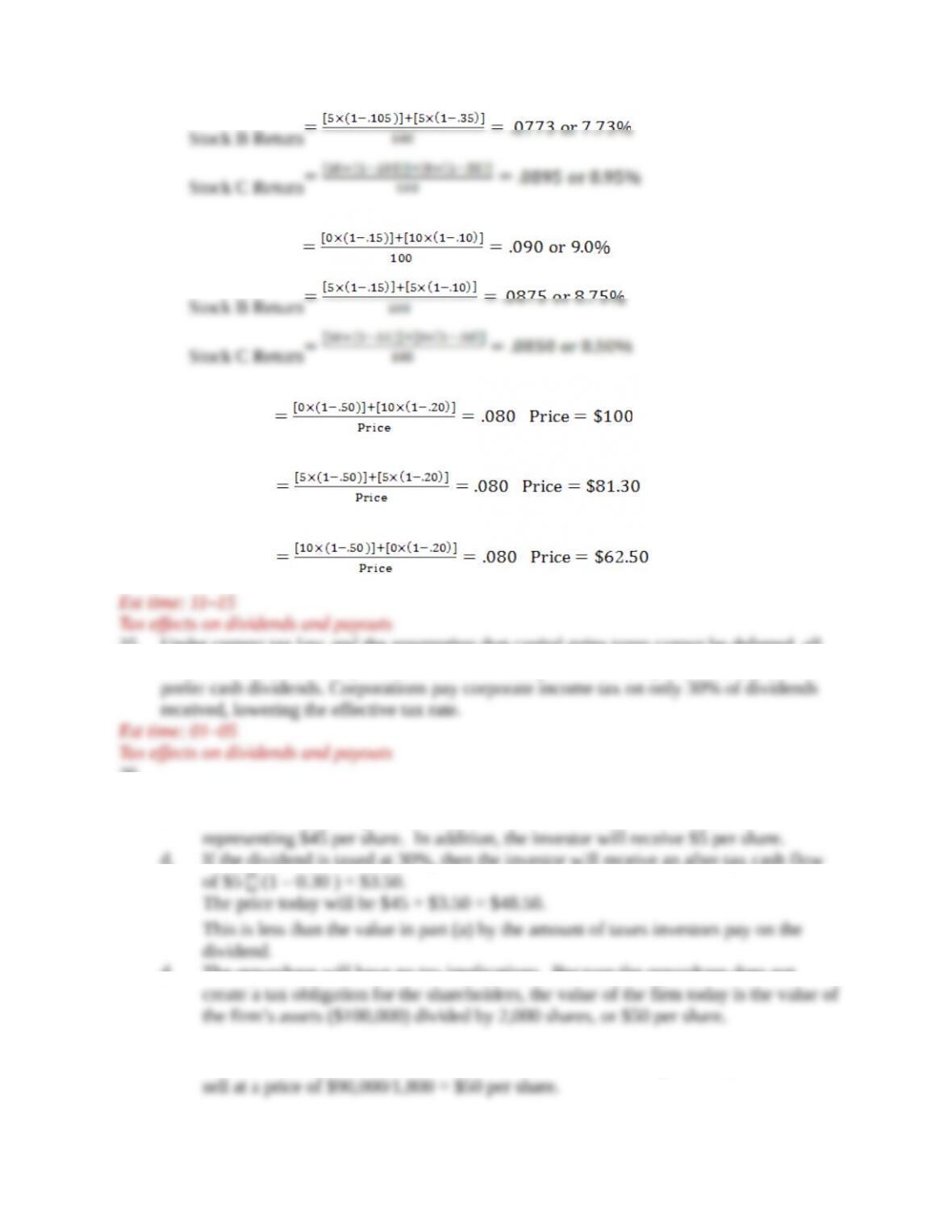

Stock A Return

b.

Stock A Return

Stock B Return

Stock C Return

25. Under current tax law, and the assumption that capital gains taxes cannot be deferred, all

investors should have no preference, with the exception of the corporation. Corporations

26.

b. Price = $100,000 / 2,000 = $50 per share

c. After the dividend is paid, total market value of the firm will be $90,000,

d. If the dividend is taxed at 30%, then the investor will receive an after-tax cash flow

d. The repurchase will have no tax implications. Because the repurchase does not

e. The firm will repurchase 200 shares for $10,000. After the repurchase, the stock will

17-11

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

f. It depends on the tax rate. Whichever payout is taxed lower will be preferred.

27.

a. Price = PV (after-tax dividend plus final share price)

45.19$

10.1

20$)]30.01(2[$

b. Before-tax rate of return

Dividend capital gain $2 ($20 $19.45) 0.1311 13.11%

price $19.45

+ + –

= = = =

c. Price = PV (after-tax dividend plus final share price) =

09.20$

10.1

20$)]30.01(3[$

d. Before-tax rate of return

%48.141448.0

09.20$

)09.20$20($3$

price

gain capital dividend

The before-tax return is higher because the larger dividend creates a greater tax

burden. The before-tax return must increase in order to provide the same after-tax

return of 10%.

e. Larger.

Est time: 06–10

Tax effects on dividends and payouts

28. Prowler should reduce its equity through a special dividend or share repurchase. First, as a

capital gain, the tax effect to shareholders is lower. Capital gains have a tax advantage for

investors, as the investor pays no tax until he or she actually sells shares. The longer he or

17-12

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

29. Younger firms are in a growth stage. As such, they are in need of capital to grow. All

things being equal, growth companies can produce a return in excess of the investors’

30. The survey indicates a reluctance to decrease dividends. As companies mature, they

transition from growth companies to stable cash flow firms. These firms begin to pay

31. Younger firms are more likely to use repurchases. Since managers are reluctant to

decrease dividends, and younger firms are more likely in a growth stage, funds available

17-13

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.