1.

a.

%20.11%14

27

19

)35.01(%7

27

8

WACC

b. If the firm has no debt, the market value of the firm would decrease by the present value of

the tax shield: 0.35 $800 = $280.

2.

a. PV tax shield = 0.35 debt = 0.35 $40 = $14

b.

%55.12%15

160

120

)35.01(%8

160

40

WACC

c. Annual tax shield = 0.35 interest expense = 0.35 (0.08 $40) = $1.12

PV tax shield = $1.12 annuity factor (8%, 5 years)

47.4$

(1.08)0.08

1

0.08

1

$1.12

5

The total value of the firm falls by $14 – $4.47 = $9.53.

The total value of the firm = $160.00 – $9.53 = $150.47.

Est time: 06–10

Capital structure weights

3. Suppose the firm’s tax bracket is 35% while shareholders’ tax bracket is 27%. The firm

has EBIT per share of $5. Compare two situations, one in which the interest on the

16-<

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

In the case that the firm has not borrowed but the investor has, the investor’s total after-tax

income (on a per-share basis) is computed as follows:

EBIT $5.00

Taxes 1.75

Net income earned per share 3.25

Less interest per share paid

Now consider the case that the firm has borrowed and pays interest of $1 per share but the

investor has not borrowed:

EBIT $5.00

Interest paid 1.00

Total after-tax income going to the investor is $0.08 per share higher when the firm, rather

4. If there is a tax advantage to firm borrowing, there must be a symmetric disadvantage

to firm lending. If the firm lends, it pays taxes on its interest income. If its tax bracket

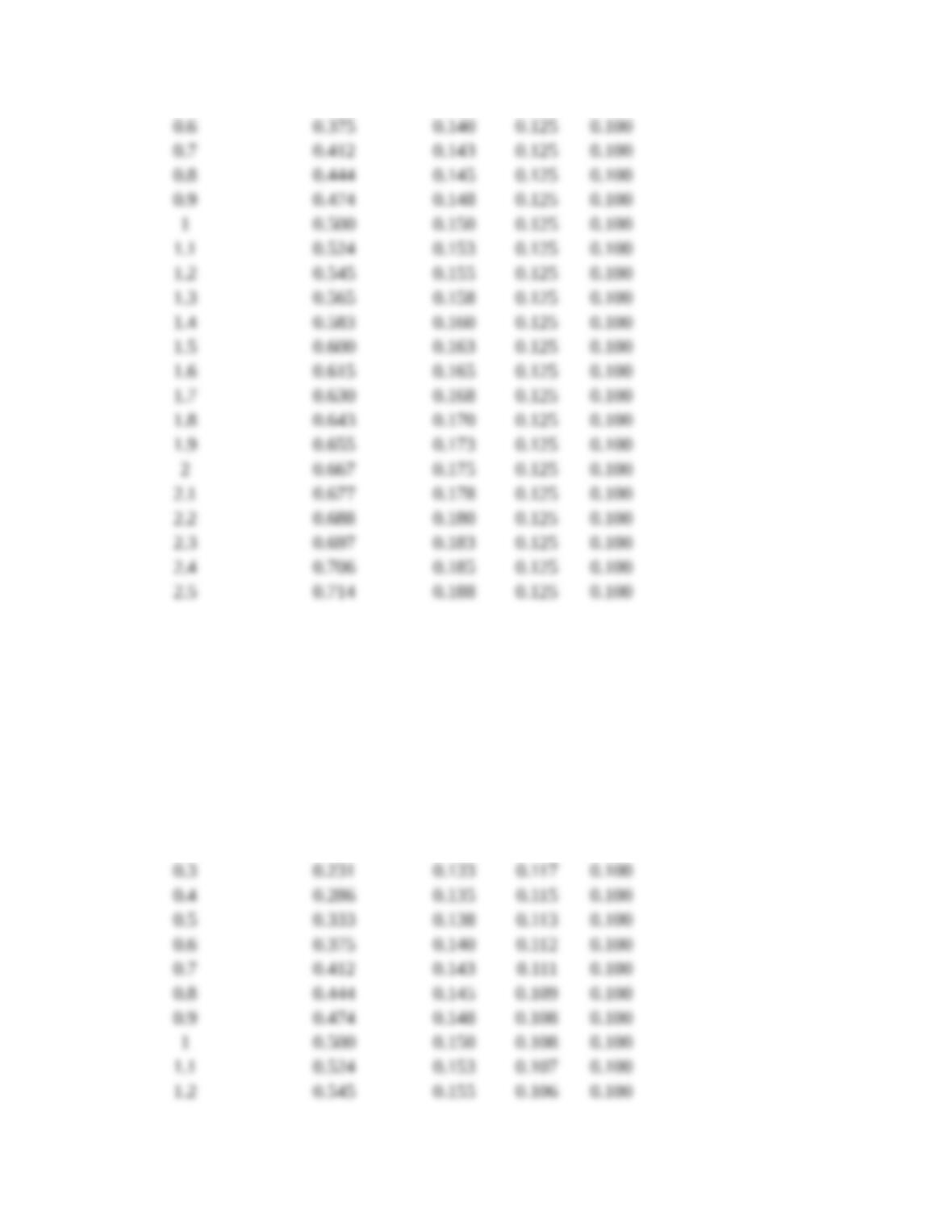

5. a. In the absence of taxes, WACC and rdebt do not change. The requity increases with

increased leverage.

Debt-Equity

Ratio D/(D + E)requity WACC rdebt

0 0.000 0.125 0.125 0.100

0.1 0.091 0.128 0.125 0.100

16-<

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

b. When the corporate tax rate is 35%, the WACC cost declines with increases in leverage.

The optimal capital structure seems to be 100% debt financing.

Debt-Equity

Ratio D/(D + E)requity WACC rdebt

0 0.000 0.125 0.125 0.100

0.1 0.091 0.128 0.122 0.100

0.2 0.167 0.130 0.119 0.100

16-<

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

c. What is not considered in the optimal capital structure seemingly implied by part (b) is

6.

a True. If the probability of default is high, managers and stockholders will be tempted to

a. True. If the probability of default is high, stockholders may refuse to contribute equity

b. False. When a company borrows, the expected costs of bankruptcy come out of the

7. Firms operating close to bankruptcy face two general types of problems. First, other

firms they do business with will try to protect themselves, in the process impeding the

16-<

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

8.

a. If SOS runs into financial difficulties, the additional funds contributed by the

equityholders to finance the new project will end up being available to pay the

b. If the new project is sufficiently risky, it may increase the expected payoff to equityholders.

To see this, imagine the following extreme case:

9. The computer software company would experience higher costs of financial distress if

its business became shaky. Its assets—largely the skills of its trained employees—are

intangible. In contrast, the shipping company could sell off some of its assets if

10.

a. Stockholders gain and bondholders lose. Bond value decreases because the value of

b. If we assume the cash is left in Treasury bills, then bondholders gain. The bondholders

c. The bondholders lose and the stockholders gain. The firm adds assets worth $10 and

16-<

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

d. The original stockholders lose and bondholders gain. There are now more assets

backing the bondholders’ claim. Since the bonds are worth more, the market value of all

11. a.

500,162$

10.0

)35.01(000,25$)1(EBIT

r

T

V

c

b. The value of the firm increases by the present value of the interest tax shield:

c. The expected cost of bankruptcy is 0.30 $200,000 = $60,000.

d. Since the present value of the expected bankruptcy cost is greater than the present value

12. The pecking- order theory states that firms prefer to raise funds through internal finance

and, if external finance is required, that they prefer debt to equity issues. This

preference—or pecking- order—results from the fact that investors may interpret

13. Alpha Corp is more profitable and is therefore able to rely to a greater extent on

16-<

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

Est time: 01–05

Pecking-order theory

14. Suppose the firm has assets in place that can generate cash flows with present value of

$100 million but the market believes the assets are actually worth $110 million. If there

are 1 million shares outstanding, the shares will sell for $110. The managers (but not

Now look at the market value balance sheet of the firm after the market reassesses the value

of the firm (therefore using the true value of the original assets) and assuming there is no debt

outstanding:

Assets Liabilities & Shareholders’ Equity

Original assets $100 million

New assets $11 million Shareholders’ equity $111 million

There are now 1.1 million shares outstanding, so the price per share is:

15. Because debtholders share in the success of the firm only to a minimal extent (i.e., to

the extent that bankruptcy risk falls), an issue of debt is not usually taken as a signal

that a firm’s management has concluded that the market is overvaluing the firm. Thus

16.

16-<

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

a True. Financial slack means having cash in the bank or ready access to the debt

c. False. Financial slack is most valuable to firms with few investment

17. Managers will try to increase debt levels to the point where the value of additional interest

tax shields is exactly offset by the additional costs of financial distress. This is known as the

18. Sealed Air started with considerable financial slack. Unlike most firms, it was a net

lender. The value of such slack is that it could enable the firm to take advantage of any

investment opportunities that might arise without the need to raise funds in the

securities market. However, top management realized that there could be too much

16-<

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.