Solutions to Chapter 16

Debt Policy

1. a. True.

b. False. As financial leverage increases, the expected rate of return on equity rises by

c. False. The sensitivity of equity returns to business risk, and therefore the cost of

2. b. By issuing debt, the company has created financial leverage for the investor. This

creates more volatility in returns. By raising money and investing in the debt, the

3. Number of shares = 75,000

Price per share = $10

State of the Economy

Slump Normal Boom

Operating income

$75,000

$125,000

$175,000

Interest $25,000 $25,000 $25,000

16-5

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

4. a. Share price = $10

With no leverage, there are 100,000 shares outstanding:

b. With leverage, there are 75,000 shares outstanding:

5.

a. Rosencrantz can recreate the returns to Stock A by buying Stock B with all of his capital

2

b. Guildenstern can recreate the returns to Stock B by buying Stock A with

7

9=¿

9=¿

2

b. Moderate borrowing does not significantly affect the probability of financial distress,

c. If the opportunity were the firm’s only asset, this would be a good deal. Stockholders

d. This is not an important reason for conservative debt levels. As long as MM’s

proposition holds, the company’s overall cost of capital is unchanged despite increasing

7.

a. The price of the stock should remain at $10 per share—all else equal.

160,000,000

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

a. Market value of the firm is $100 10,000 = $1,000,000.

b. Low-debt plan:

EBIT $110,000

c. With the high-debt plan, equity falls by $400,000, so:

9. Expected return on assets is:

10.

16-5

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

a

rassets =.05×.5+.10 ×.5=.075∨7.5

d. The percentage of equity is now 25% and the value of equity is $250,000

11. Currently, with no outstanding debt, equity = 1.0.

Therefore: assets = 1.0

a. (equity 0.5) + (debt 0.5) = assets = 1

b. requity = rassets = 10%

c. requity = rassets + [D/E (rassets – rdebt)] = 10% + [1 (10% – 5%)] = 15%

d. 5%

e. rassets = (0.5 requity) + (0.5 rdebt) = (0.5 15%) + (0.5 5%) = 10%

16-5

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

f. Suppose total equity before the refinancing was $1,000. Then expected earnings were

15.

a.

rE=rf +β ×

(

rM−rf

)

=10 +1.5 ×

(

8

)

=22

rA=

E

+

D

=

(

0.5×22

)

+

(

0.5×12

)

=17

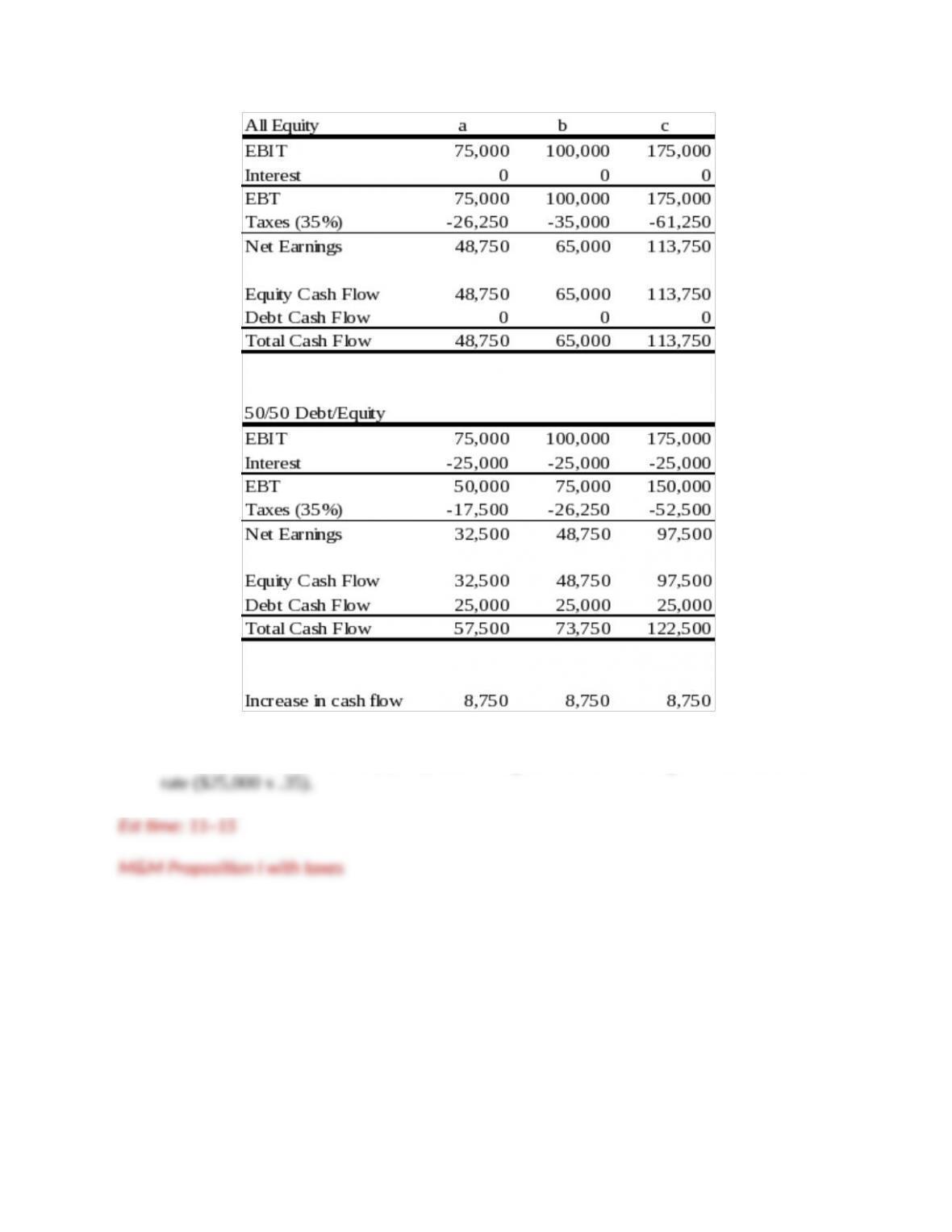

The increase in cash flow is $8,750, which is equal to the interest expense times the tax

17.

a.

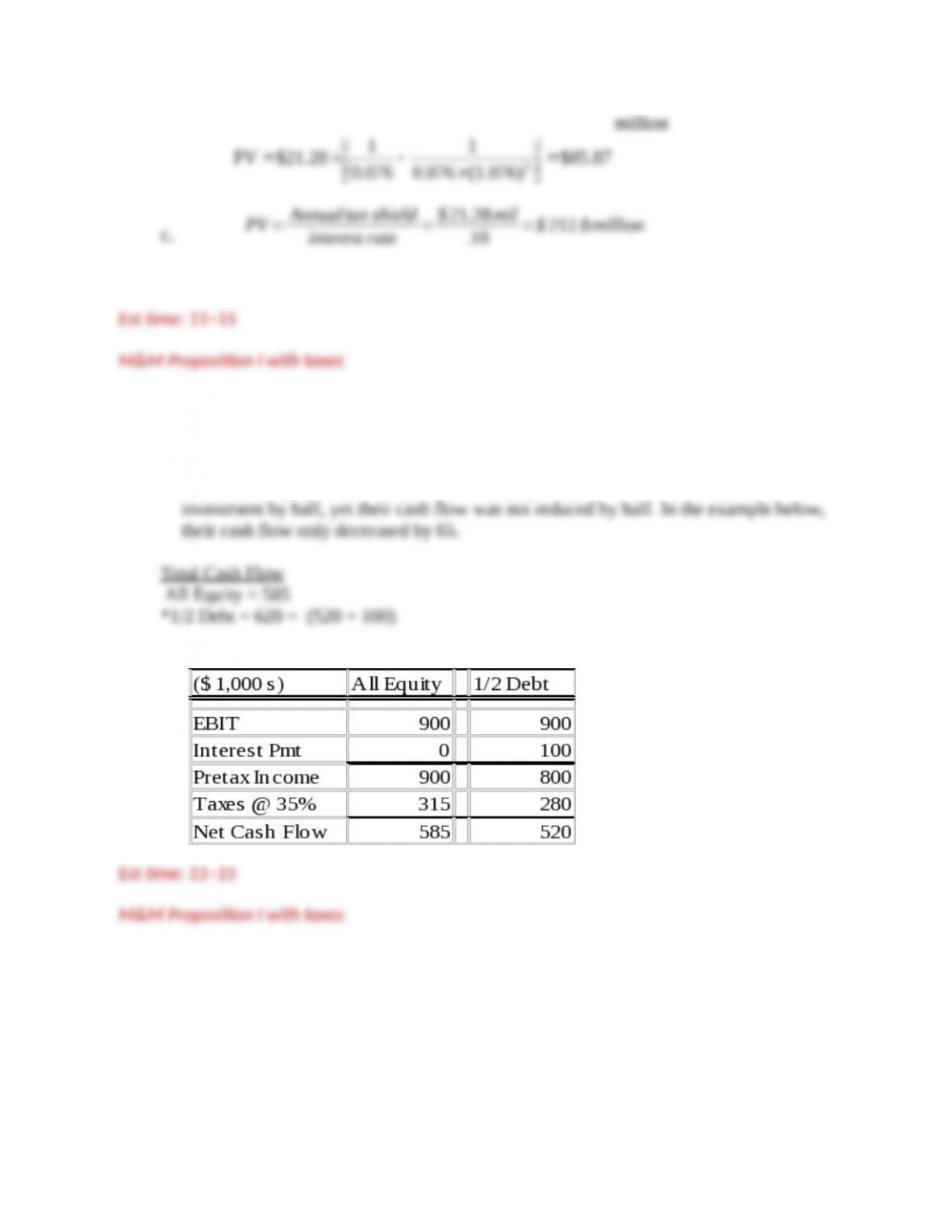

PV tax shield=$800 mil× .35=$280 million

b.

Annual tax shield=$800 mil ×.076 ×.35=$21.28 million

16-5

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

18. The interest tax shield represents a tax savings based upon the tax deductibility of

interest. If an all equity company replaces half its equity with debt, the total cash flow

to debt and equity holders increases. The equity holders benefit since they reduced their

19.

a.

1206.15.7.)35.01(08.3. WACC

or 12.06%

16-5

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

b.

1290.15.7.08.3. WACC

or 12.90%

Est time: 01–05

Weighted average cost of capital

16-5

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.