Solutions to Chapter 12

Risk, Return, and Capital Budgeting

1. The risks of deaths of individual policyholders are largely independent and are therefore

diversifiable. The insurance company is satisfied to charge a premium that reflects

actuarial probabilities of death, without an additional risk premium. In contrast, flood

2. The actual returns for the Snake Oil fund exhibit considerable variation around the

regression line. This indicates that the fund is subject to diversifiable risk: It is not well

3. Beta tells us how sensitive the stock return is to changes in market performance. The

market return was 5% less than your prior expectation. Therefore, the stock would be

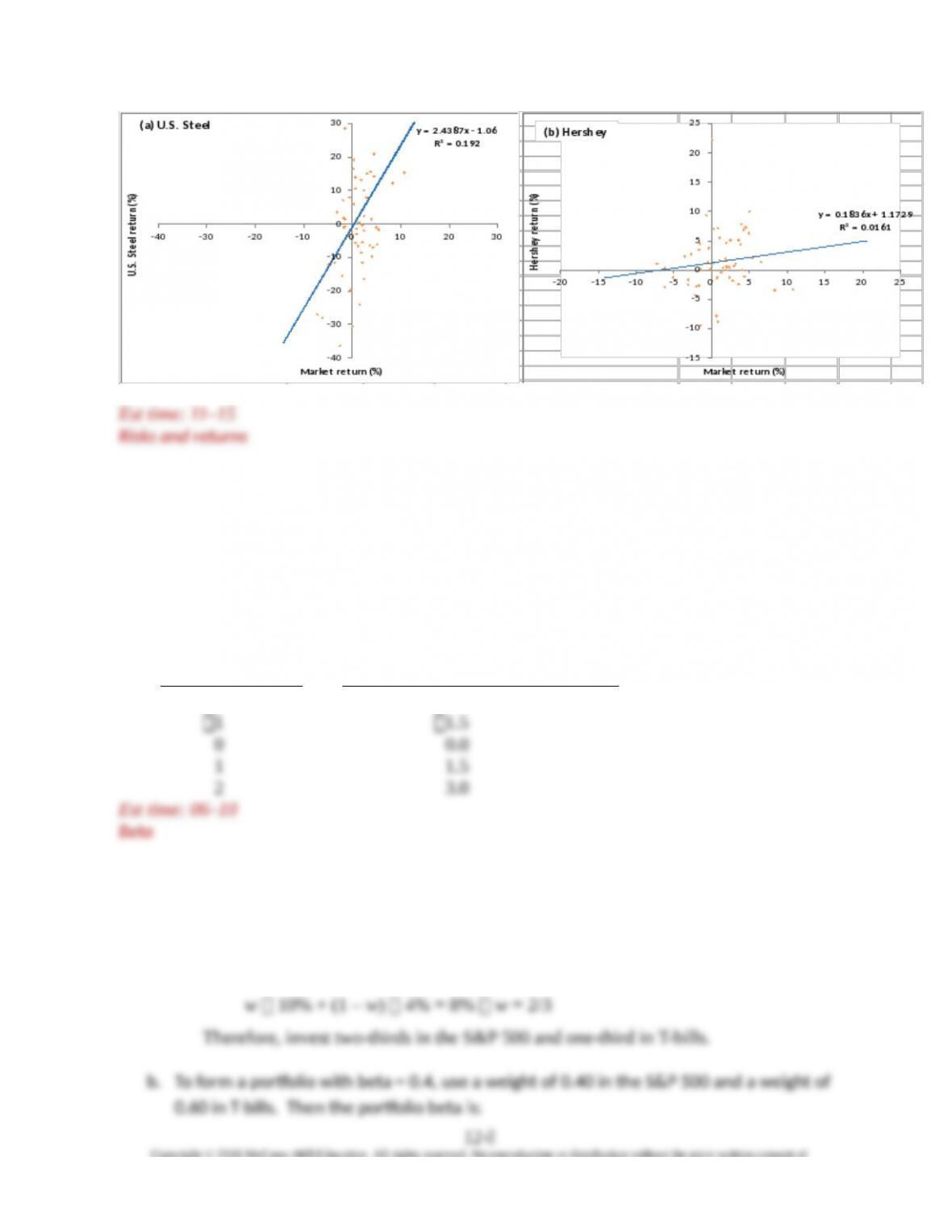

4. a. A diversified investor will find the lowest-beta stock safest. This is Walmart,

b. Pfizer has the lowest total volatility; the standard deviation of its returns is15.3%.

12-<

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

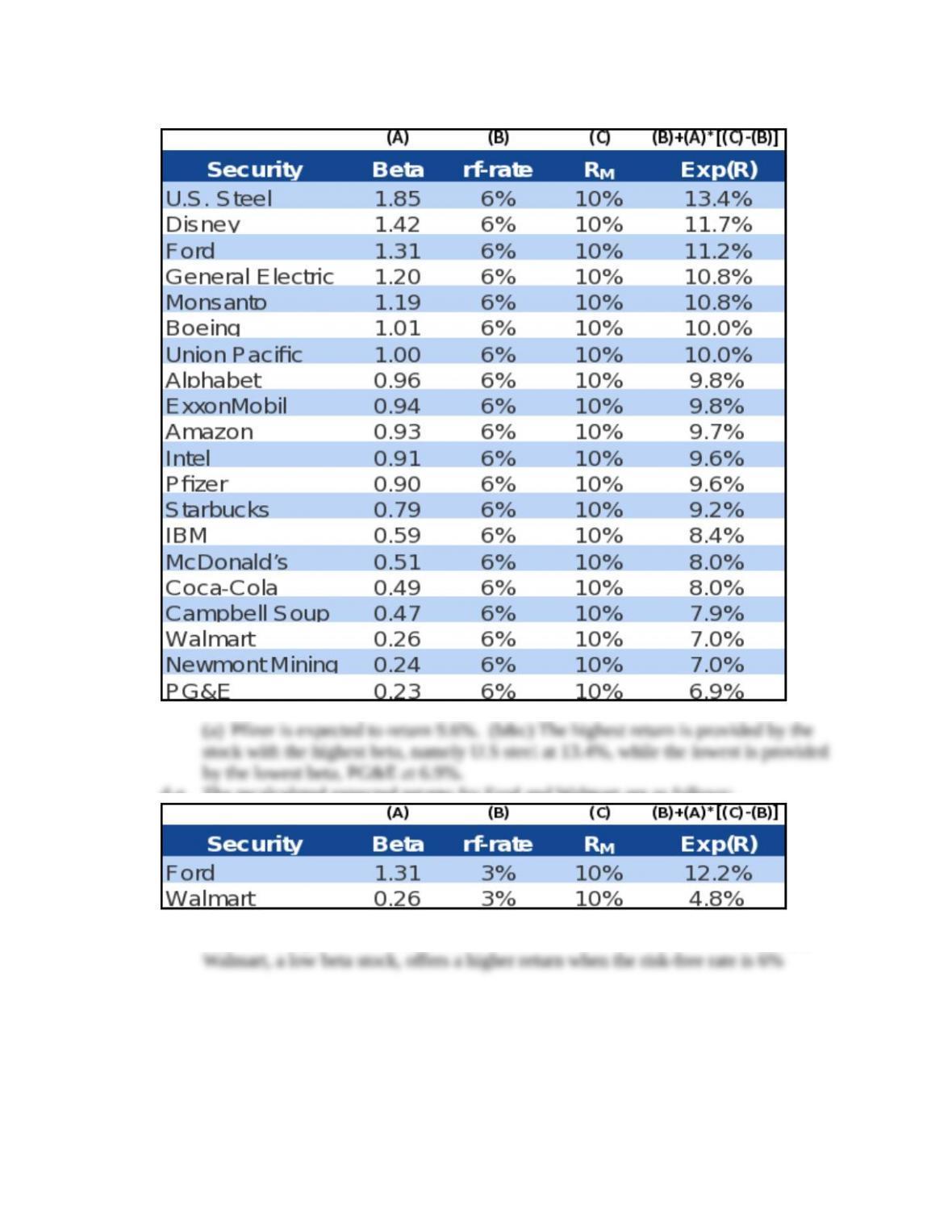

e. Using the CAPM, we compute the expected rate of return on each stock from the

equation r = rf + (rm – rf).

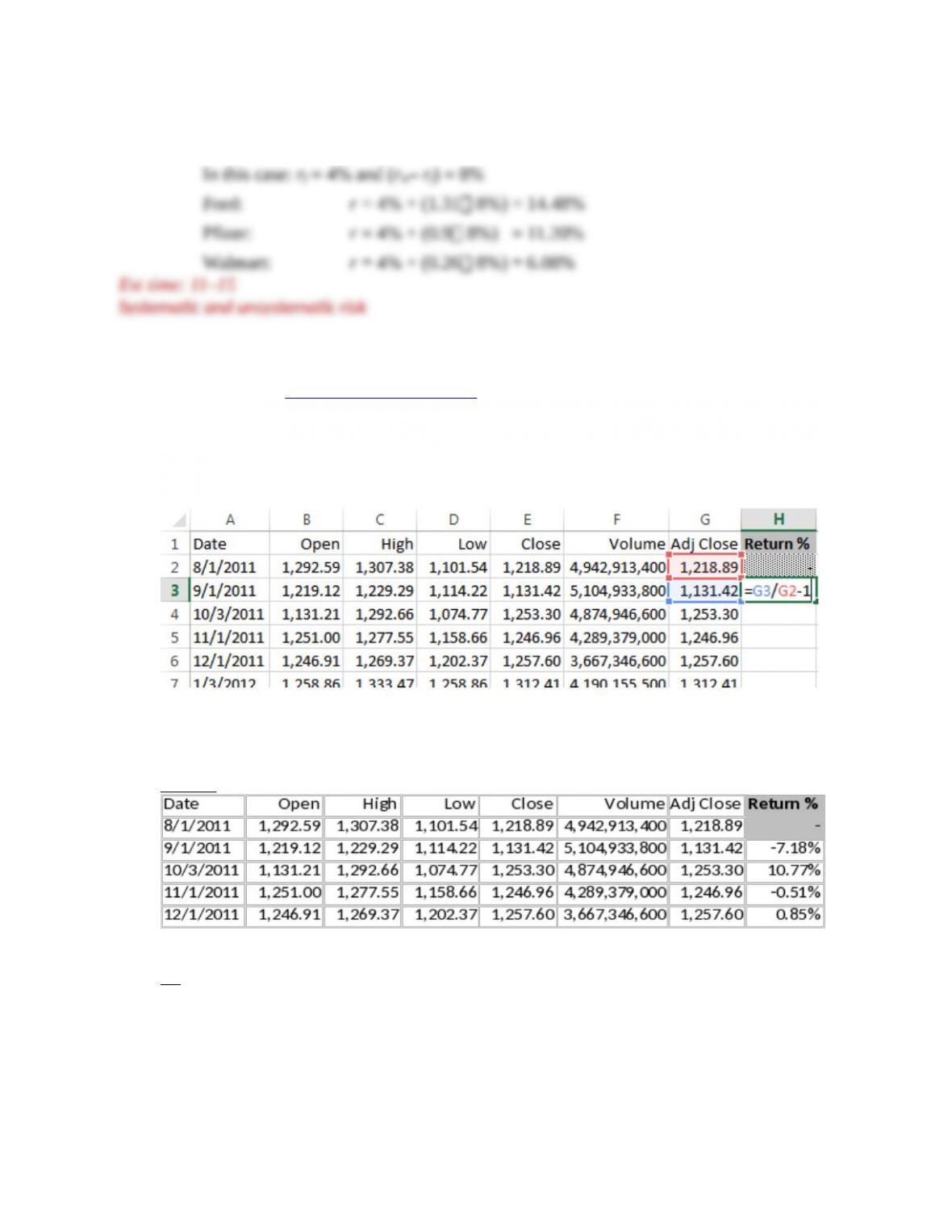

5. a. Navigating to http://finance.yahoo.com/. Look up each security and GSPC (S&P 500

index) and select the “Historical Data” menu. Set the criteria to a date range of 8/1/2011

through 8/1/2016 and a frequency of monthly. Click “apply,” then download as a CSV file.

Once saved as an excel file, first sort the data from oldest to newest date (column A) then

navigate to the next available column (should be column H) and enter a formula to

calculate the monthly returns:

You will have 60 data points, but note that there will be 61 rows of data since the first row

(row 2) is only used to calculate the first rate of return. The following displays a sample of

the three datasets:

GSPC:

X:

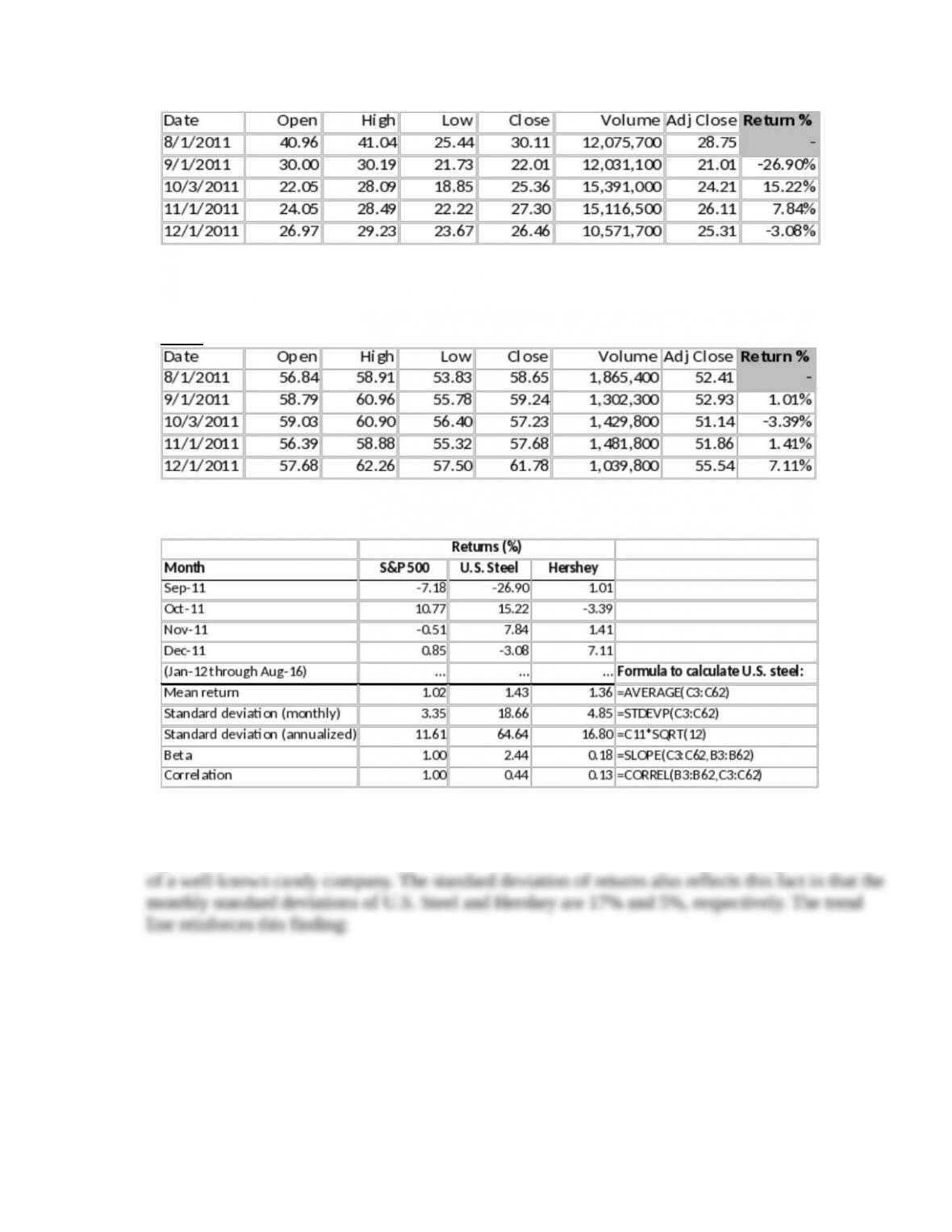

12-<

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

HSY:

Once the 60 data points are prepared for each variable, copy and past the returns into a

single spreadsheet and apply the SLOPE formula twice for each stock against the market:

b. The return on Hershey’s stock is relatively less volatile than that of U.S. Steel. The resulting

higher beta for U.S. Steel makes sense, as the business risk for a steel company is higher than that

12-<

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

6. The following table shows the average return on Tumblehome for various values of the

market return. It is clear from the table that when the market return increases by 1%,

Tumblehome’s return increases, on average, by 1.5%. Therefore, = 1.5. If you prepare

a plot of the return on Tumblehome as a function of the market return, you will find that

the slope of the line through the points is 1.5.

Market Return (%) Average Return on Tumblehome (%)

23.0

7.

a. Call the weight in the S&P 500 w and the weight in T-bills (1 – w). Then w must satisfy

the equation:

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

8. A security with a negative beta would be expected to produce a return less than the risk-

9. Investors would buy shares of firms with high levels of diversifiable risk and earn

10. a. The expected cash flows from the firm are in the form of a perpetuity. The discount

rate is:

rf + (rm – rf) = 4% + 0.4 (11% – 4%) = 6.8%

82.058,147$

068.0

000,10$flow cash

0

r

P

b. If the true beta is actually 0.6, the discount rate should be:

rf + (rm – rf) = 4% + [0.6 (11% – 4%)] = 8.2%

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

11. Required return = rf + (rm – rf) = 6% + [1.25 (13% – 6%)] = 14.75%

Expected return = 16%

12. a. Alphabet has a beta of 0.96 and McDonald’s has a beta of 0.51, therefore:

Porfolio beta=.4 ×0.96+.6 ×0.51=0.69

b. The portfolio holding just Alphabet and McDonald’s securities will be under

,,,

d-e. The recalculated expected returns for Ford and Walmart are as follows:

(d) Ford, a high beta stock, offers a lower return when the risk-free rate is 6%. (e)

12-<

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.