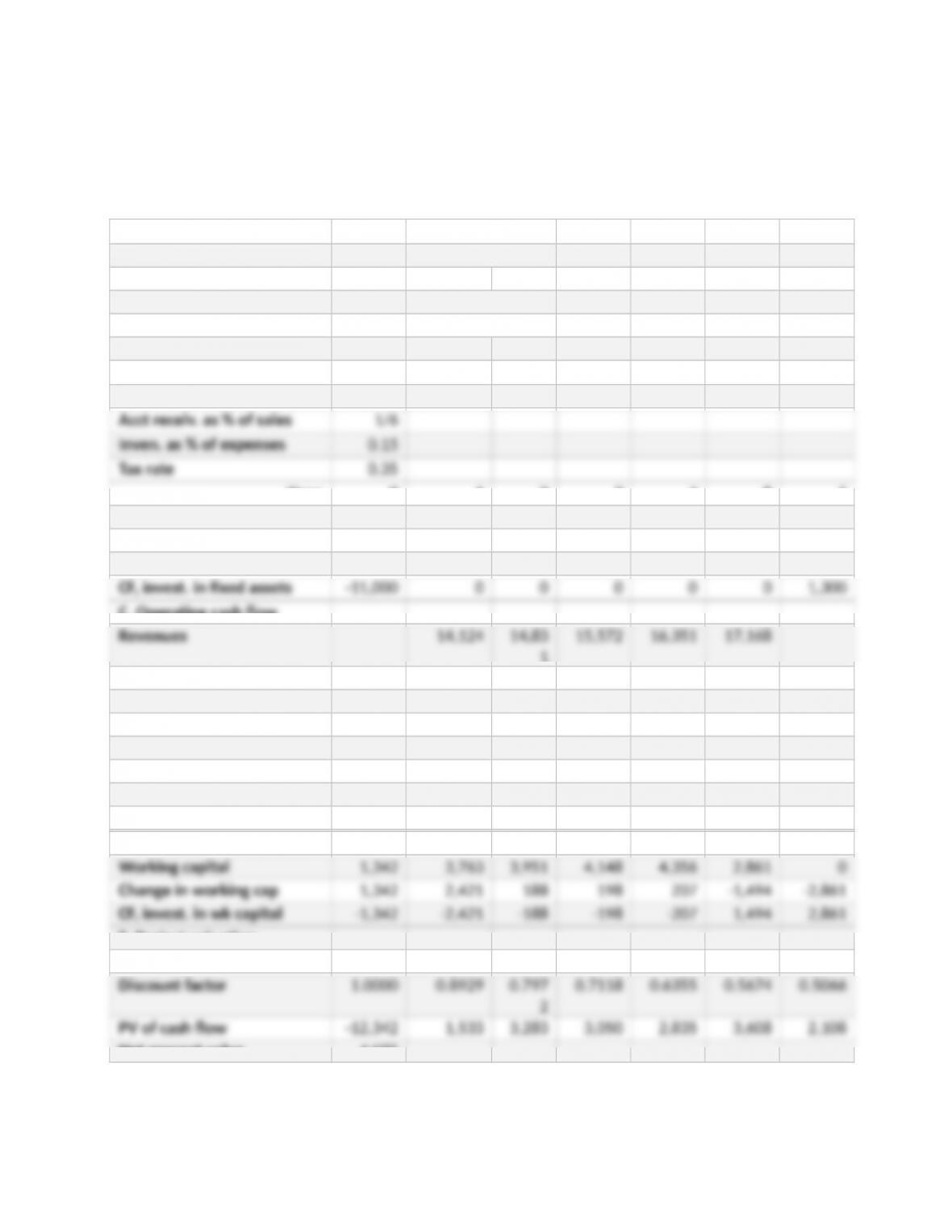

a. Use goal seek to isolate profit after tax as the dependent variable relating to initial

revenue. The level of initial revenue in the base case was $15,000,000, which

produced accounting profits of $11,458,000 across the five project years. Adjusting

the spreadsheet to the scenario presented here, initial revenue can fall to $14,124,000

before accounting profits fall below $11,458,000:

A. Inputs

Initial investment 11,000

Salvage value 2,000

Initial revenue 14,124

Initial fixed expenses 4,000

Expenses % of Revenue 0.35

Inflation rate 0.05

Discount rate 0.12

Year: 0 1 2 3 4 5 6

B. Capital investment

Investment in fixed assets 11,000

Sales of fixed assets 1,300

C. Operating cash flow

1

Variable expenses 4,944 5,191 5,450 5,723 6,009

Fixed expenses 4,000 4,200 4,410 4,631 4,862

Depreciation 2,200 2,200 2,200 2,200 2,200

Pretax profit 2,981 3,240 3,512 3,798 4,097

Tax 1,043 1,134 1,229 1,329 1,434

Profit a3er tax 1,938 2,106 2,283 2,468 2,663

Operating cash flow 4,138 4,306 4,483 4,668 4,863

D. Changes in working capital

E. Project valuation

Total project cash flow -12,342 1,716 4,118 4,285 4,461 6,358 4,161

Net present value 4,075

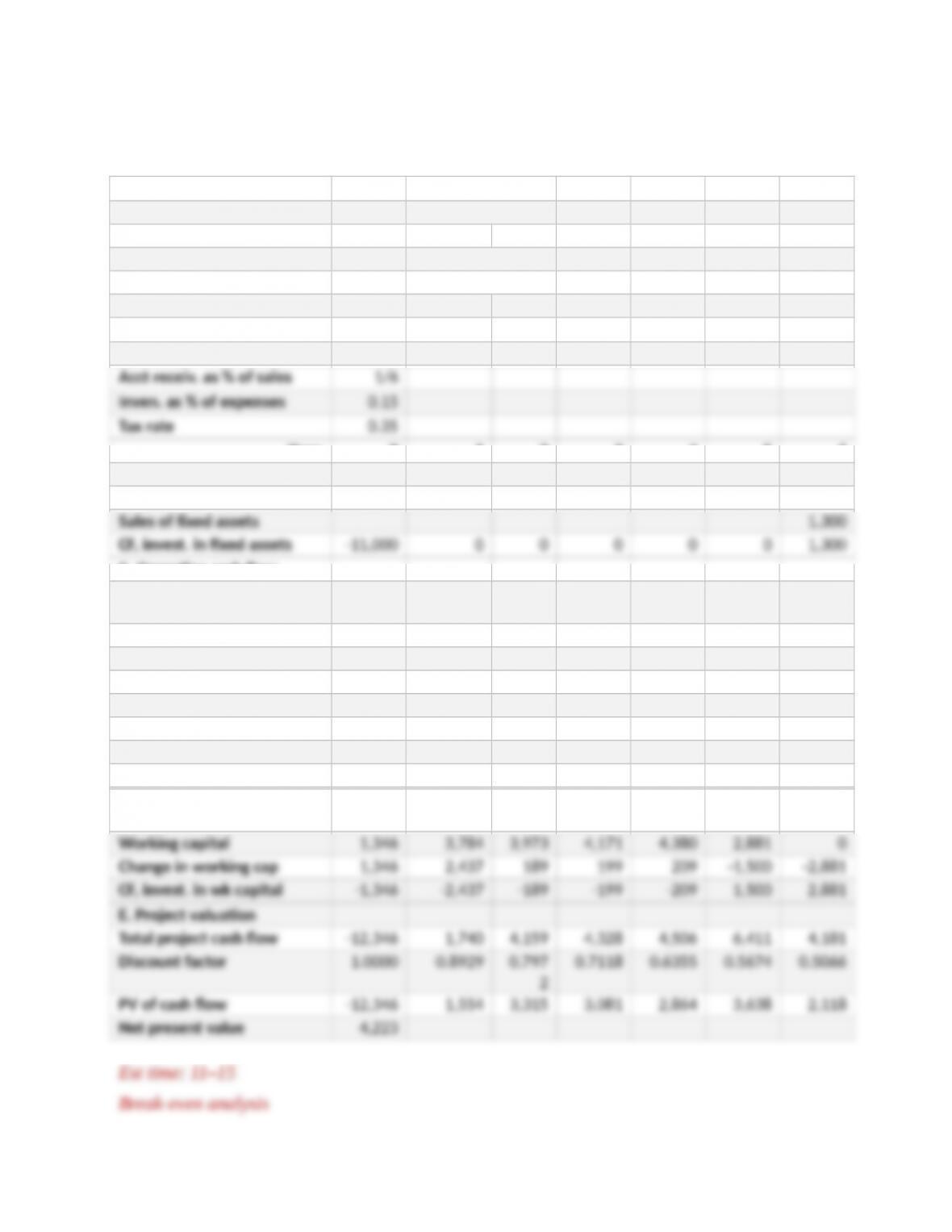

b. Use goal seek to isolate net present value as the dependent variable relating to initial

revenue. The level of initial revenue in the base case was $15,000,000, which

10-‘

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

produced net present value of $4,223,000. Adjusting the spreadsheet to the scenario

presented here, initial revenue can fall to $14,219,000 before net present value falls

below $4,223,000:

A. Inputs

Initial investment 11,000

Salvage value 2,000

Initial revenue 14,219

Initial fixed expenses 4,000

Expenses % of Revenue 0.35

Inflation rate 0.05

Discount rate 0.12

Year: 0 1 2 3 4 5 6

B. Capital investment

Investment in fixed assets 11,000

C. Operating cash flow

Revenues 14,219 14,93

0

15,676 16,460 17,283

Variable expenses 4,977 5,225 5,487 5,761 6,049

Fixed expenses 4,000 4,200 4,410 4,631 4,862

Depreciation 2,200 2,200 2,200 2,200 2,200

Pretax profit 3,042 3,304 3,580 3,869 4,172

Tax 1,065 1,157 1,253 1,354 1,460

Profit a3er tax 1,978 2,148 2,327 2,515 2,712

Operating cash flow 4,178 4,348 4,527 4,715 4,912

D. Changes in working

capital

10-‘

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

1. NPV will be negative. We’ve shown in the previous problem that the accounting

2. Percentage change in profits = percentage change in sales DOL.

3. DOL =

fixed costs (including depreciation)

1profits

+

a. Profit = revenues – variable costs – fixed costs – depreciation

4. DOL =

fixed costs (including depreciation)

1profits

+

10-‘

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

5. a. Pretax profits currently equal:

Revenue – variable costs – fixed costs – depreciation

b. DOL =

4

500$

500,1$

1

ofitspr

on)depreciati (including costs fixed

1

6.

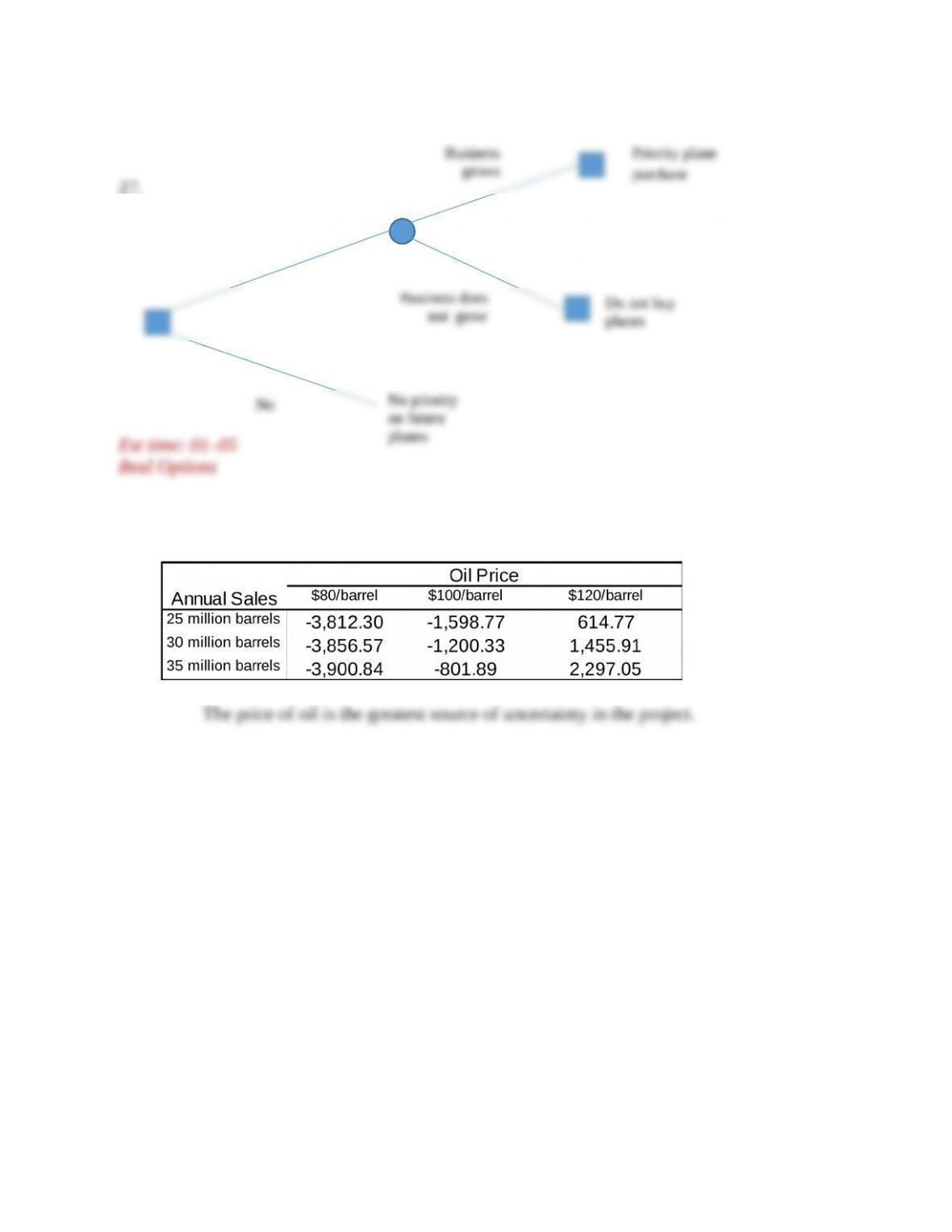

a The option to delay expansion is a Timing Option because the decision to expand is not

7. We compare expected NPV with and without testing. If the field is large, then:

10-‘

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

24. a. Average annual expenses = (10,000 $32) + $40,000 = $360,000

Average annual revenue = 10,000 (.5 × $24) + 10,000 (.5 × $48) = $360,000

Average cash flow = revenue – expenses = $360,000 – $360,000 = $0

b. If you can shut down the mine 50% of the time, CF in the low-price years will be zero. In

the remaining years:

10-‘

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

Real options

25.

a. Expected NPV = [0.5 ($140 – $100)] + [0.5 ($50 – $100)] = –$5 million

b. Now the worst-case value of the installed project is $95 million rather than $50 million.

c.

Invest

$100 million

26. Options provide the ability to cut losses or to extend gains. You benefit from good

outcomes but can limit damage from bad outcomes. The ability to change your actions

10-‘

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

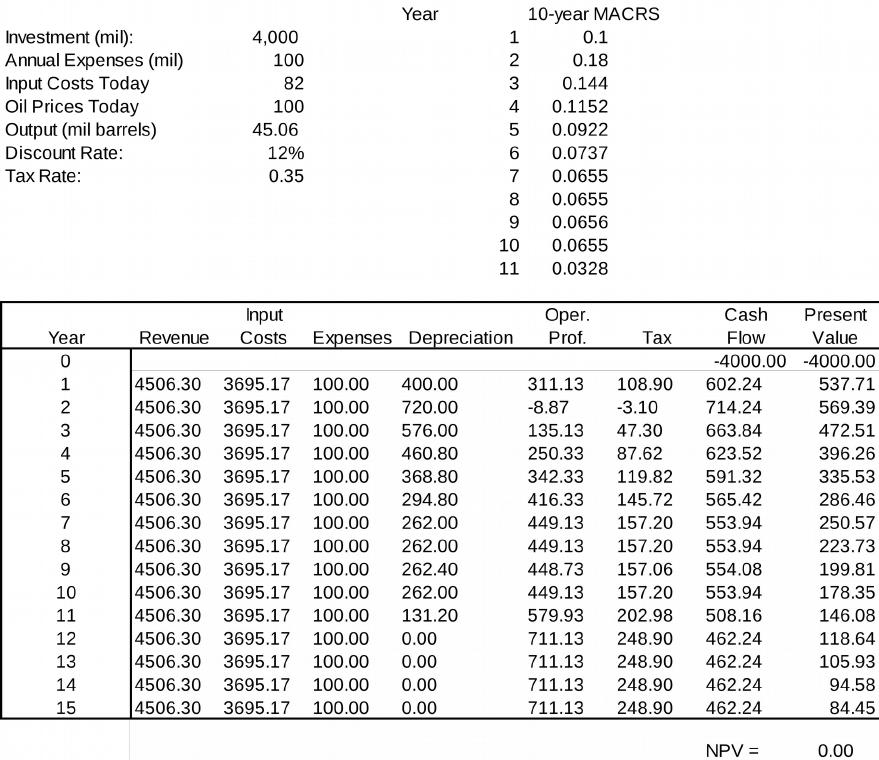

28. a.

b. Given a $100 per barrel price, the annual level of sales necessary for an NPV break-even

is 45.00 million barrels. The value was found using Excel’s Goal Seek, shown below:

10-‘

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

Decision to

buy option

10-‘

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

c.

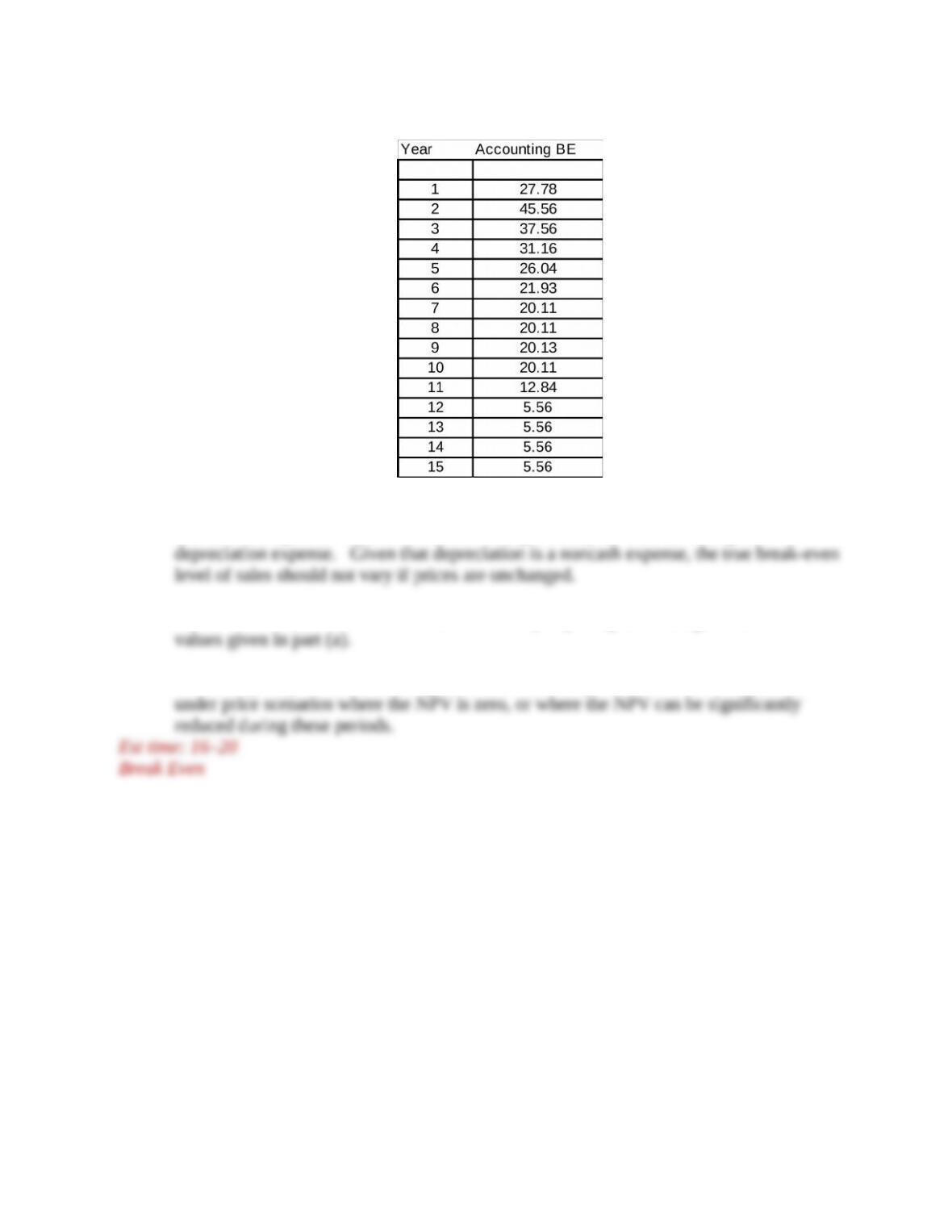

The accounting break-even level of sales changes each year with the changes in

d. The NPV of –$1,200.33 million is found as an equally weighted average for all NPV

e. The facility may be worth building if the firm has the option to shut down the facilities

10-‘

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.