Solutions to Chapter 10

Project Analysis

1. Scenario analysis – Project NPV is recalculated by changing several inputs to new but

consistent values.

Real option – Opportunity to modify a project at a future date.

Sensitivity analysis – Analysis of how project NPV changes if different assumptions are

2.

False – Approval of the capital budget allows manager to go ahead with any project

included in the budget.

3.

True – Sensitivity analysis can be used to identify the variables most crucial to a project’s

success.

4.

The extra 2 million burgers increase total costs by $1.0 million.

10-6

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

5.

10-6

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

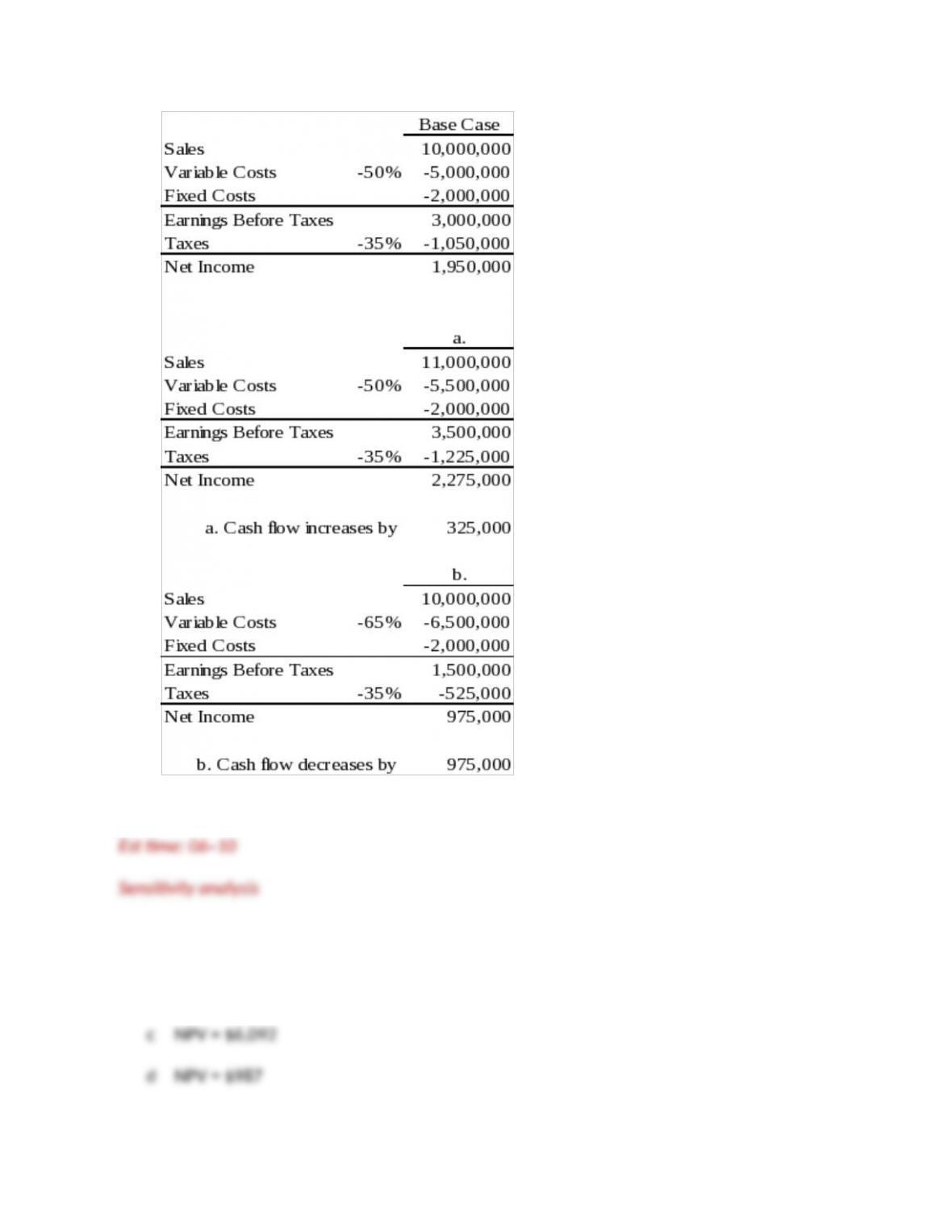

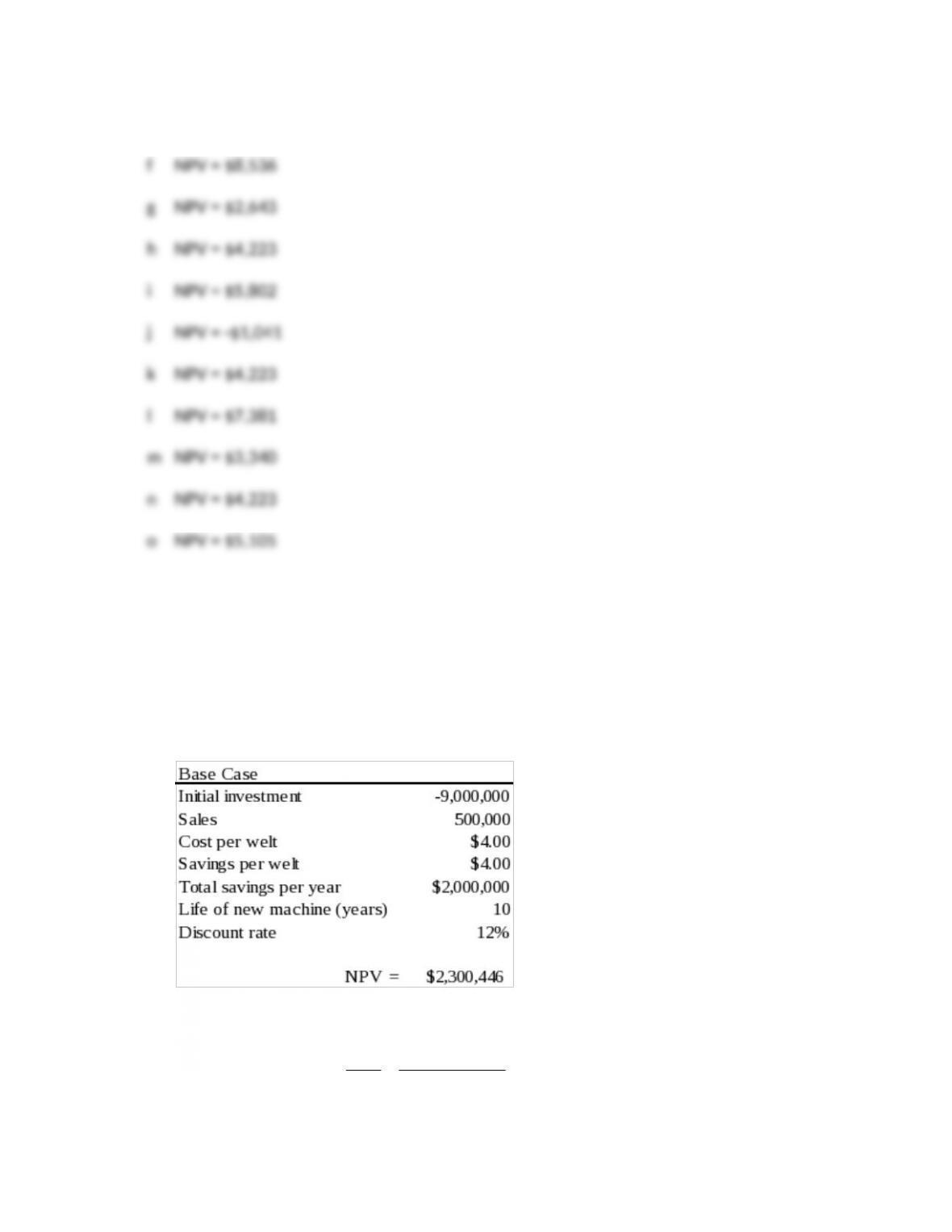

6. Use the student spreadsheet provided for Blooper’s to calculate NPVs (in thousands):

a NPV = $484

b NPV = $4,223

10-6

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

e NPV = $4,223

Est time: 06–10

Sensitivity analysis

7.

a.

357,40$000,000,9

)12.1(0.12

1

0.12

1

$1,600,000NPV 10

10-6

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

8. Revenue = price quantity = $2 6 million = $12 million

Expense = variable cost + fixed cost = ($1 6 million) + $2 million = $8 million

10-6

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

10-6

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

9.

Most Likely Best Case Worst Case

Price

$50

$55

$45

Variable cost $30 $27 $33

Fixed cost $300,000 $270,000 $330,000

Sales 30,000 units 33,000 units 27,000 units

Cash flow = [(1 – T) (revenue – cash expenses)] + (T depreciation)

10. At the break-even level of sales (60,000 units) profit would be zero:

11.

a. Each dollar of sales generates $0.60 of pretax profit. depreciation expense is $100,000

per year, and fixed costs are $200,000. Therefore:

b. Let Q = the number of diamonds sold.

10-6

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

12%, 10-year annuity factor =

65022.5

(1.12)0.12

1

0.12

1

10

12.

a. The accounting break-even point would be unaffected since taxes paid are zero when

b. The NPV break-even point would increase since the after-tax cash flow corresponding to any

13.

a Cash 9ow = net income + depreciation

b. If cash 9ow = 0 for the entire life of the project, then the present value of cash 9ows =

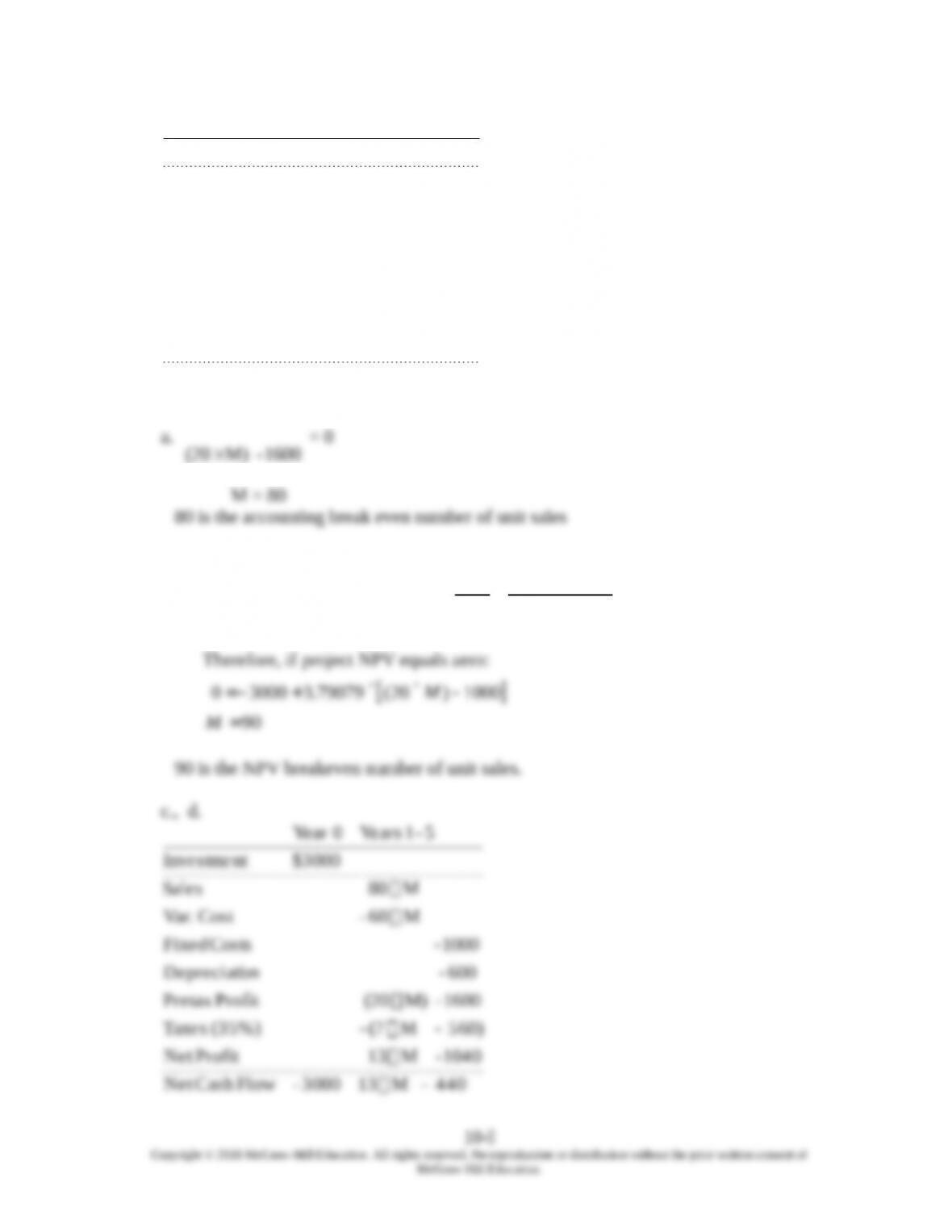

14. a., b.

10-6

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

1000 – M) (20 3000-FlowCash Net

1600 – M) (20 ProfitNet

0(0%) Taxes

1600 – M) (20 ProfitPretax

600- onDepreciati

1000- Costs Fixed

M 60-Cost Var.

M 80 Sales

$3000Investment

5-1 Years0Year

a.

1600 – M) (20

= 0

M = 80

80 is the accounting break even number of unit sales

b. The 10%, 5-year annuity factor is:

79079.3

(1.10)0.10

1

0.10

1

5

d. The 10%, 5-year annuity factor is:

79079.3

(1.10)0.10

1

0.10

1

5

15.

a accounting break-even level of sales increases. MACRS results in higher depreciation

b. NPV break-even level of sales decreases. The accelerated depreciation increases the

c. MACRS makes the project more aBrac5ve. The PV of the tax shield is higher, so the

16.

10-6

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

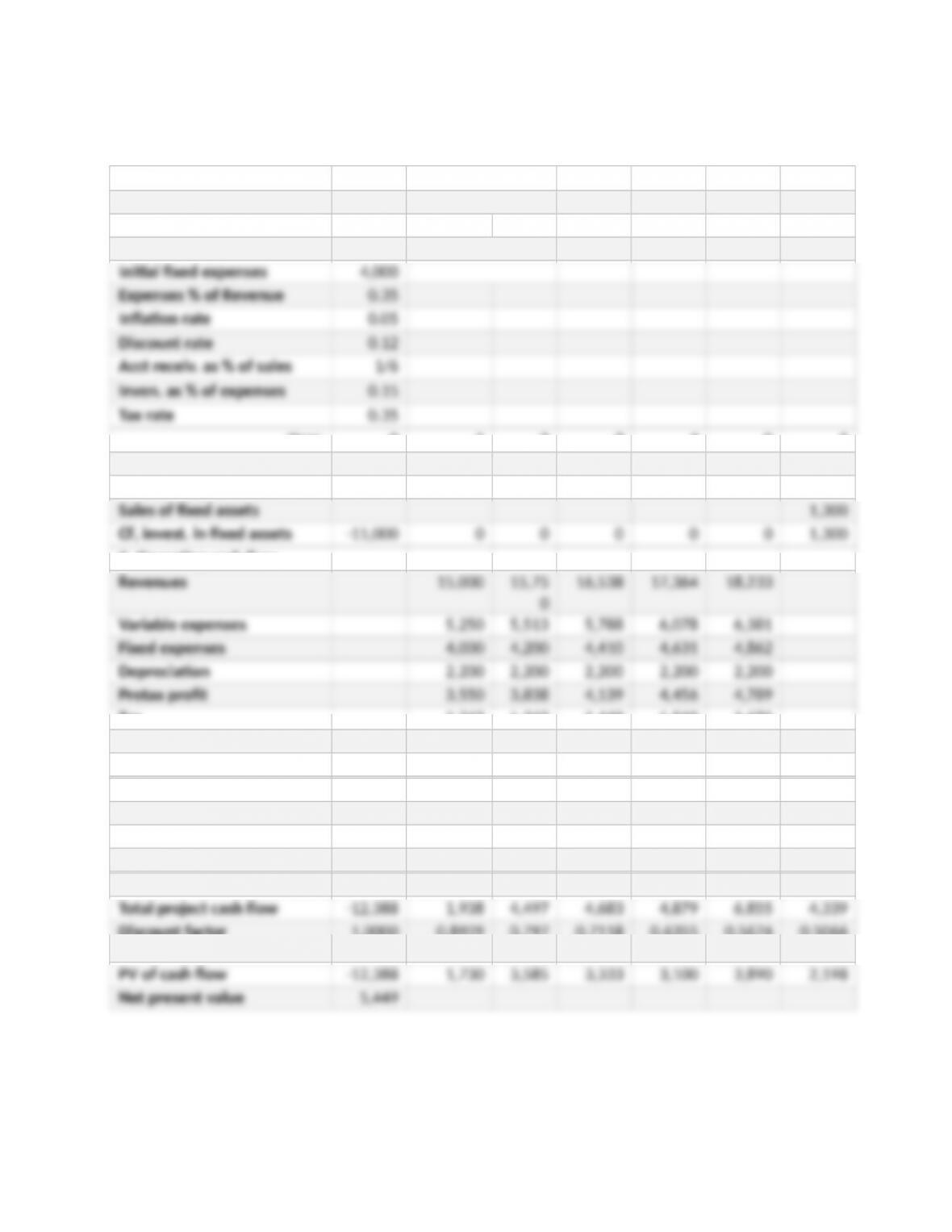

a. The analysis under the new scenario is as follows:

A. Inputs

Initial investment 11,000

Salvage value 2,000

Initial revenue 15,000

Year: 0 1 2 3 4 5 6

B. Capital investment

Investment in fixed assets 11,000

C. Operating cash ow

Tax 1,243 1,343 1,449 1,560 1,676

Profit a3er tax 2,308 2,494 2,691 2,897 3,113

Operating cash ow 4,508 4,694 4,891 5,097 5,313

D. Changes in working capital

Working capital 1,388 3,957 4,155 4,362 4,581 3,039 0

Change in working cap 1,388 2,569 198 208 218 -1,542 -3,039

CF, invest. in wk capital -1,388 -2,569 -198 -208 -218 1,542 3,039

E. Project valuation

Discount factor 1.0000 0.8929 0.797

2

0.7118 0.6355 0.5674 0.5066

10-6

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.