Chapter 7

Stock Price Behavior and Market Efficiency

Concept Questions

2. Unlike gambling, the stock market is a positive sum game; everybody can win. Also, speculators

3. The efficient markets paradigm only says, within the bounds of increasingly strong assumptions about

However, that does not mean that a few particular investors cannot outperform the market over a

4. a. If the market is not weak-form efficient, then this information could be acted on and a profit

b. Under 2, if the market is not semistrong-form efficient, then this information could be used to buy

c. Under 3, if the market is not strong-form efficient, then this information could be used as a

profitable trading strategy, by noting the buying activity of the insiders as a signal that the stock is

d. Despite the fact that this information is obviously less open to the public and a clearer signal of

imminent price gains than is the scenario in part (c), the conclusions remain the same. If the

5. Taken at face value, this fact suggests that markets have become more efficient. The increasing ease

with which information is available over the internet lends strength to this conclusion. On the other

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

6. It is likely the market has a better estimate of the stock price, assuming it is semistrong-form efficient.

However, semistrong-form efficiency only states that you cannot easily profit from publicly available

7. Beating the market during any year is entirely possible. If you are able to consistently beat the market,

8. a. False. Market efficiency implies that prices reflect all available information, but it does not

b. True. Market efficiency exists when prices reflect all available information. To be efficient in

the weak form, the market must incorporate all historical data into prices. Under the semi-

c. False. Market efficiency implies that market participants are rational. Rational people will

e. True. Competition among investors results in the rapid transmission of new market information.

10. Ignoring trading costs, on average, such investors merely earn what the market offers; the trades all

b. Only scenario (ii) indicates market efficiency. In that case, the price of the stock rises

12. False. The stock price would have adjusted before the founder’s death only if investors had perfect

forecasting ability. The 12.5 percent increase in the stock price after the founder’s death indicates that

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

13. The announcement should not deter investors from buying UPC’s stock. If the market is semi-strong

form efficient, the stock price will have already reflected the present value of the payments that UPC

14. The market is generally considered to be efficient up to the semi-strong form. Therefore, no

systematic profit can be made by trading on publicly-available information. Although illegal, the lead

15. Under the semi-strong form of market efficiency, the stock price should stay the same. The

16. Because the number of subscribers has increased dramatically, the time it takes for information in the

newsletter to be reflected in prices has shortened. With shorter adjustment periods, it becomes

17. You should not agree with your broker. The performance ratings of the small manufacturing firms

b. Possibly. If the rumors were publicly disseminated, the prices would have already adjusted for

20. The statement is false because every investor has a different risk preference. Although the expected

21. At the time of the announcement, the price of the stock should immediately decrease to reflect the

negative information.

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

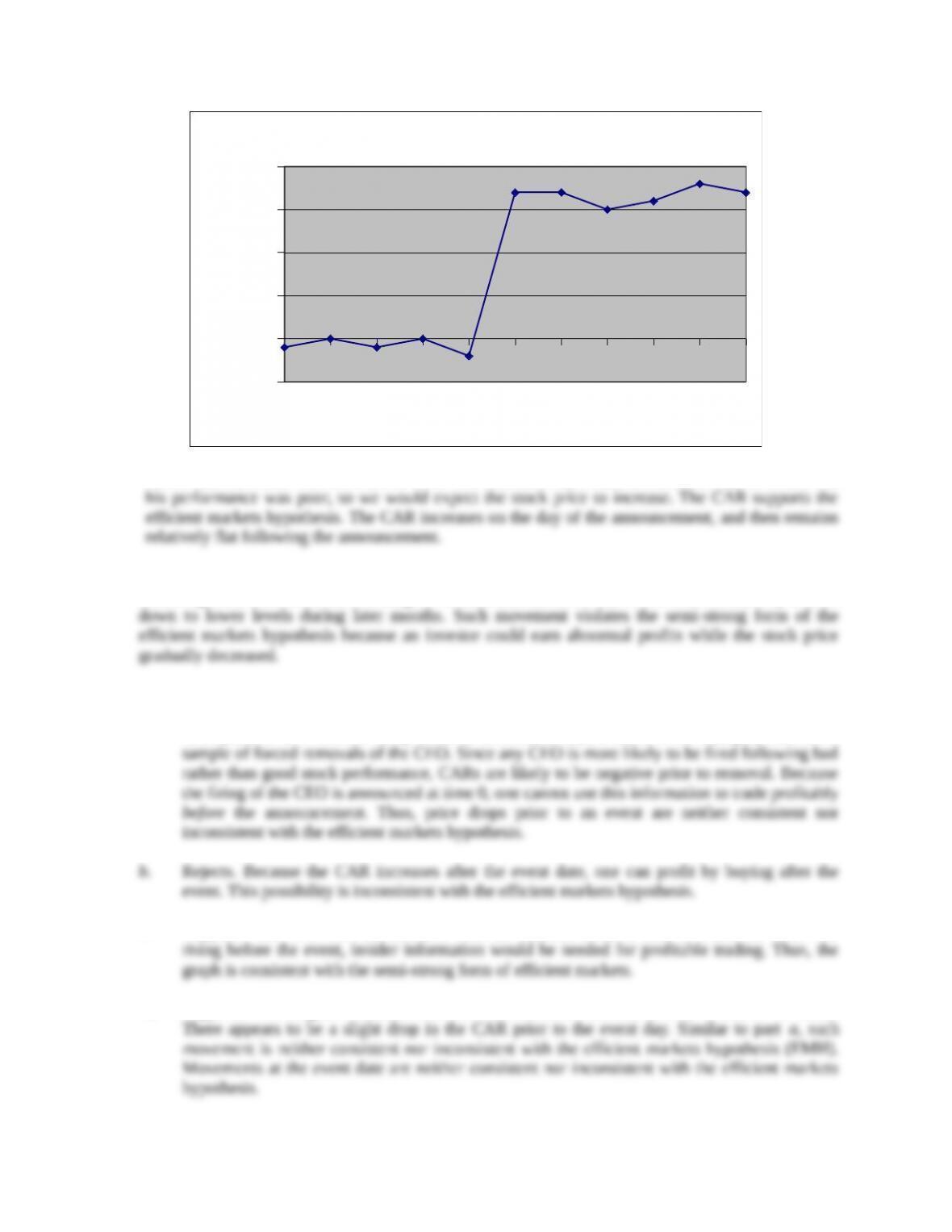

22. In an efficient market, the cumulative abnormal return (CAR) for Prospectors would rise substantially

at the announcement of a new discovery. The CAR falls slightly on any day when no discovery is

on the other days, leaving CARs that are horizontal over time.

Solutions to Questions and Problems

NOTE: All end of chapter problems were solved using a spreadsheet. Many problems require multiple

Core Questions

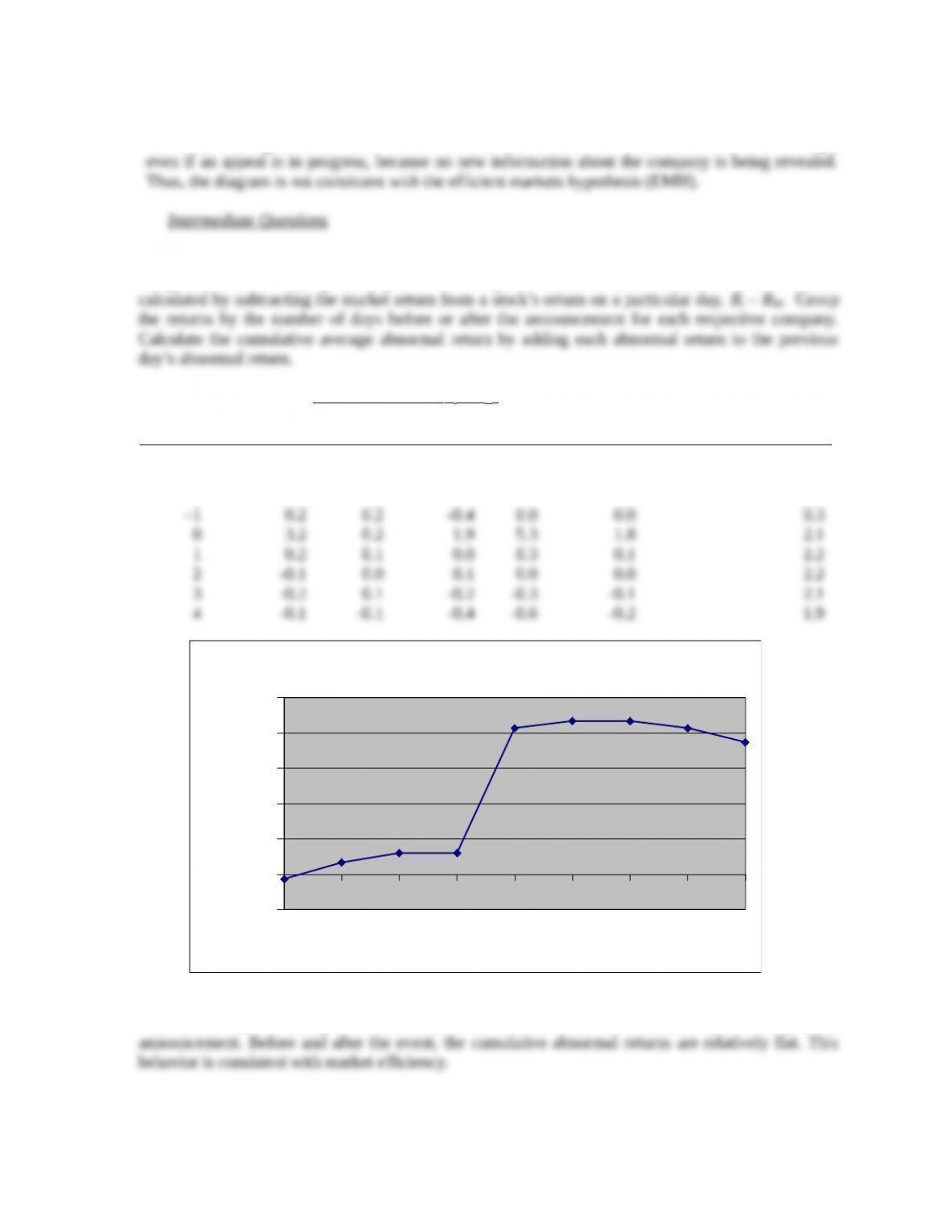

1. To find the cumulative abnormal returns, we chart the abnormal returns for the days preceding and

Daily Cumulative

Days from Abnormal Abnormal

Announcement Return Return

-5 -0.1 -0.1

-4 0.1 0.0

-3 -0.1 -0.1

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

–5 –4 –3 –2 –1 0 1 2 3 4 5

–0.5

0.0

0.5

1.0

1.5

2.0

Cumulative Abnormal Returns

Days from announcement

CAR

Given that the battle with the current CEO was acrimonious, it must be assumed that investors felt

2. The diagram does not support the efficient markets hypothesis. The CAR should remain relatively flat

following the announcements. The diagram reveals that the CAR rose in the first month, only to drift

3. a. Supports. The CAR remained constant after the event at time 0. This result is consistent with

market efficiency, because prices adjust immediately to reflect the new information. Drops in

CAR prior to an event can easily occur in an efficient capital market. For example, consider a

c. Supports. The CAR does not fluctuate after the announcement at time 0. While the CAR was

d. Supports. The diagram indicates that the information announced at time 0 was of no value.

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

4. Once the verdict is reached, the diagram shows that the CAR continues to decline after the court

decision, allowing investors to earn abnormal returns. The CAR should remain constant on average,

5. To find the cumulative abnormal returns, we chart the abnormal returns for each of the three

companies for the days preceding and following the announcement. The abnormal return is

Abnormal returns ( Ri – R M)

Days from

announcement Ross W’field Jordan Sum

Average

abnormal return

Cumulative

average residual

–4 -0.2 -0.2 0.2 -0.2 -0.1 -0.1

–3 0.2 -0.1 0.6 0.7 0.2 0.2

–2 0.2 -0.2 0.4 0.4 0.1 0.3

–4 –3 –2 –1 0 1 2 3 4

–0.5

0.0

0.5

1.0

1.5

2.0

2.5

Cumulative Abnormal Returns

Days from announcement

CAR

The market reacts favorably to the announcements. Moreover, the market reacts only on the day of the

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.