Chapter 16

Option Valuation

Concept Questions

1. The six factors are the stock price, the strike price, the time to expiration, the risk-free interest rate,

2. Increasing the time to expiration increases the value of an option. The reason is that the option gives

the holder the right to buy or sell. The longer the holder has that right, the more time there is for the

3. An increase in volatility acts to increase both put and call values because greater volatility increases

4. An increase in dividend yield reduces call values and increases put values. The reason is that, all else

the same, dividend payments decrease stock prices. To give an extreme example, consider a

5. Interest rate increases are good for calls and bad for puts. The reason is that if a call is exercised in

6. The time value of both a call option and a put option is the difference between the price of the option

7. An option’s delta tells us the (approximate) dollar change in the option’s value that will result from a

8. Vesting refers to the date at which an option can be exercised. For example, if the option has a 4 year

9. There are two possible benefits. First, awarding employee stock options may better align the

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

10. The fact that employee stock options are not tradeable decreases its value relative to a tradeable

Solutions to Questions and Problems

NOTE: All end of chapter problems were solved using a spreadsheet. Many problems require multiple

steps. Due to space and readability constraints, when these intermediate steps are included in this

solutions manual, rounding may appear to have occurred. However, the final answer for each problem is

found without rounding during any step in the problem.

Core Questions

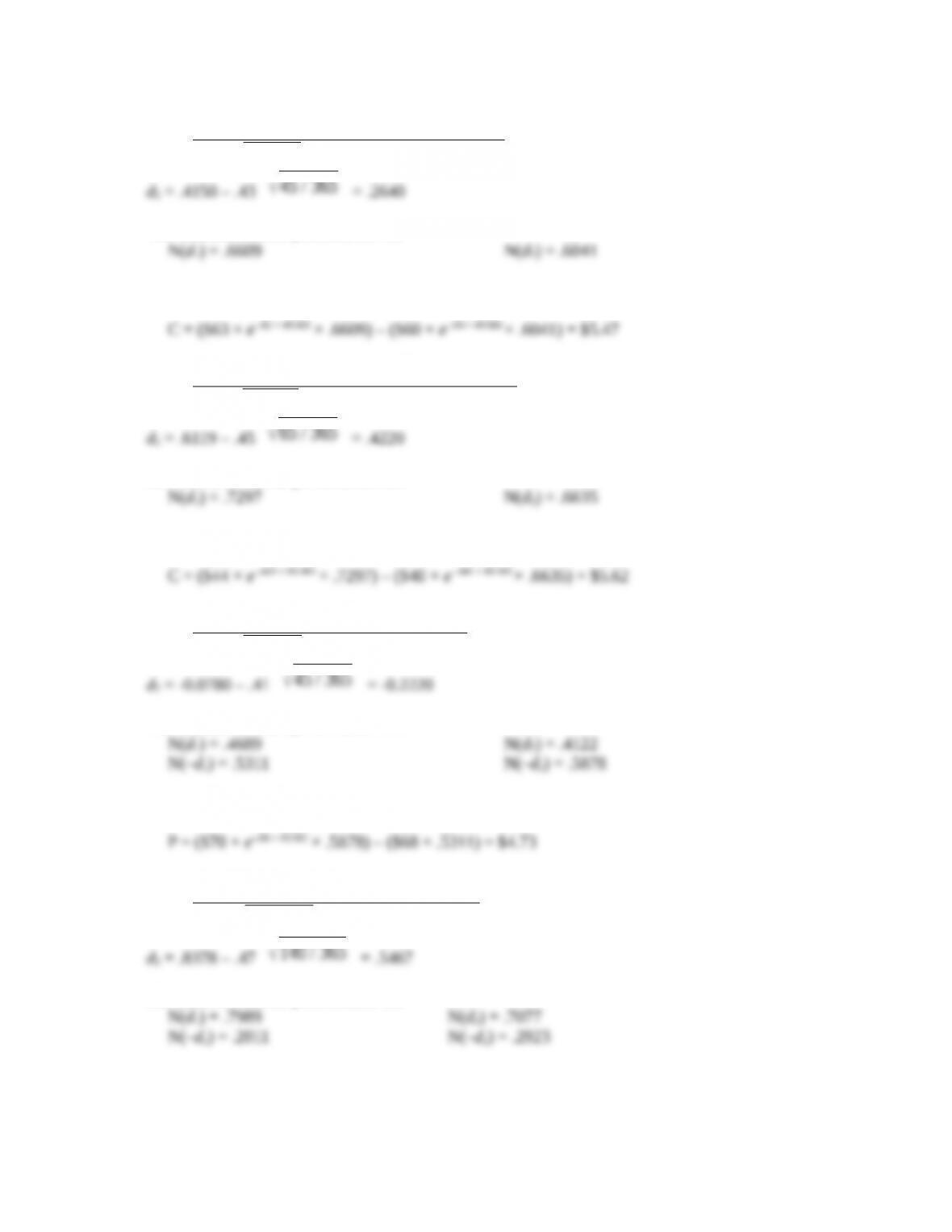

1. d1 =

ln(84/80 )+(.04 +. 422/ 2)× 135 / 365

. 42 ×

√

135 / 365

= .3766

d2 = .3766 – .42

√

135 / 365

= .1212

The standard normal probabilities are:

Calculating the price of the call option yields:

2. d1 =

ln(81 / 90)+(.03 +. 502/ 2)× 60 / 365

.50 ×

√

60 / 365

= –.3940

60 / 365

The standard normal probabilities are:

Calculating the price of the call option yields:

3. d1 =

ln(73 / 75 )+(. 05 +. 372/ 2)× 100 / 365

.37 ×

√

100 / 365

= .0280

100 / 365

The standard normal probabilities are:

Calculating the price of the call option yields:

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

4. d1 =

ln(63 / 60 )+(.04 – . 02 +. 432/ 2)× 45 / 365

. 43 ×

√

45 / 365

= .4150

45 / 365

The standard normal probabilities are:

Calculating the price of the call option yields:

5. d1 =

ln(44 / 40 )+(. 041 – .025 +. 452/ 2)× 65 / 365

. 45 ×

√

65 / 365

= .6119

65 / 365

The standard normal probabilities are:

Calculating the price of the call option yields:

6. d1 =

ln(68 / 70 )+(.06 +. 412/ 2 )× 45 / 365

. 41 ×

√

45 / 365

= -0.0780

45 / 365

The standard normal probabilities are:

Calculating the price of the put option yields:

7. d1 =

ln(42 / 35 )+(. 05+. 472/ 2)× 140 / 365

. 47 ×

√

140 / 365

= .8378

140 / 365

The standard normal probabilities are:

Calculating the price of the put option yields:

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

8. d1 =

ln(67 / 80 )+(.03 +. 302/ 2 )× 60 / 365

.30 ×

√

60 / 365

= –1.3566

60 / 365

The standard normal probabilities are:

Calculating the price of the put option yields:

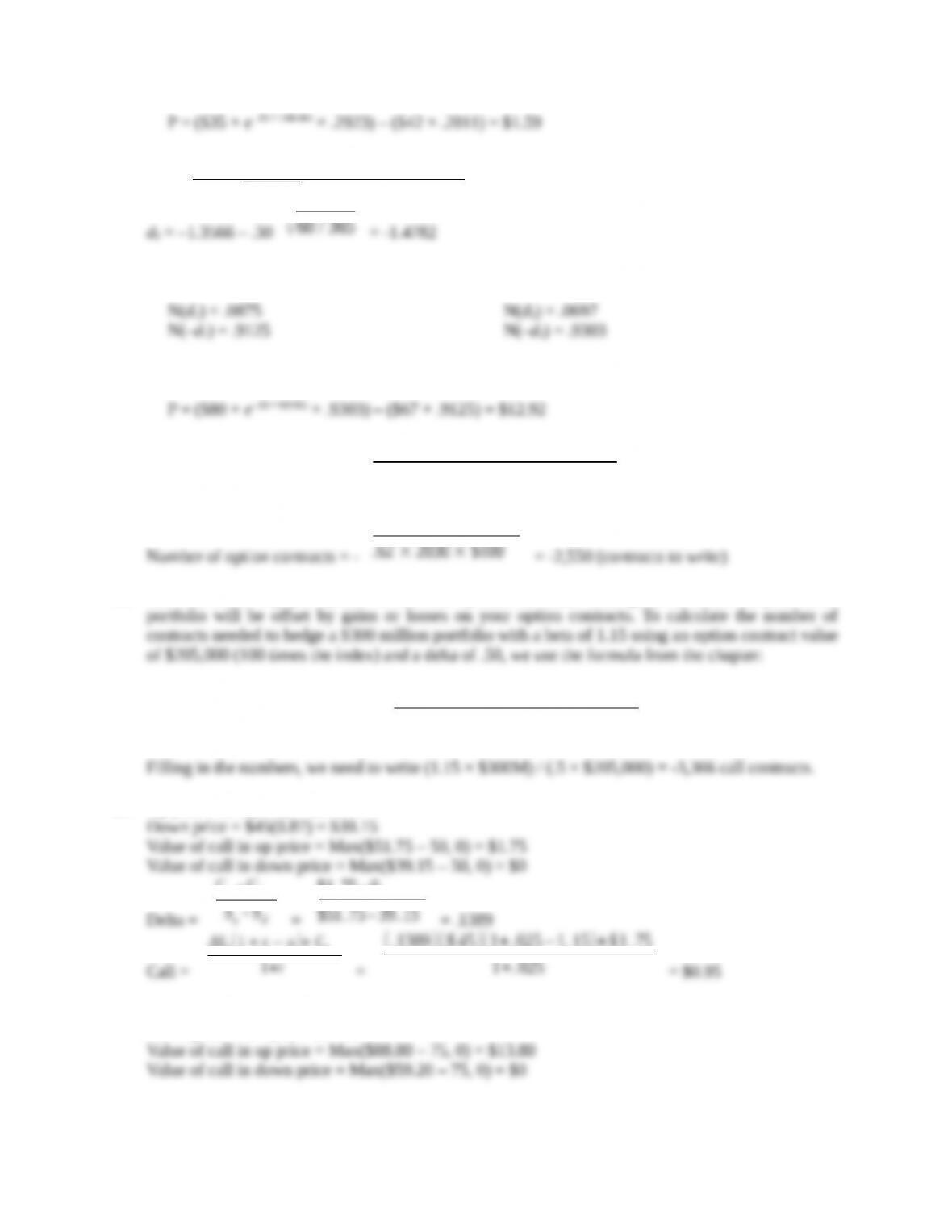

9. Number of option contracts = –

Portfolio beta × Portfolio value

Option delta × Option contract value

Number of option contracts = –

1 . 07 × $300,000,000

.62 × 2030 × $100

= -2,550 (contracts to write)

10. You can either buy put options or sell call options. In either case, gains or losses on your stock

Number of option contracts = –

Portfolio beta × Portfolio value

Option delta × Option contract value

11. Up price = $45(1.15) = $51.75

Delta =

Cu – Cd

Su – Sd

=

$1. 75 – 0

$51. 75 – 39. 15

= .1389

Call =

ΔSu(1 + r − u )+ Cu

1+r

=

(.1389 )($45 )(1+. 025−1. 15)+$1 .75

1+. 025

= $0.95

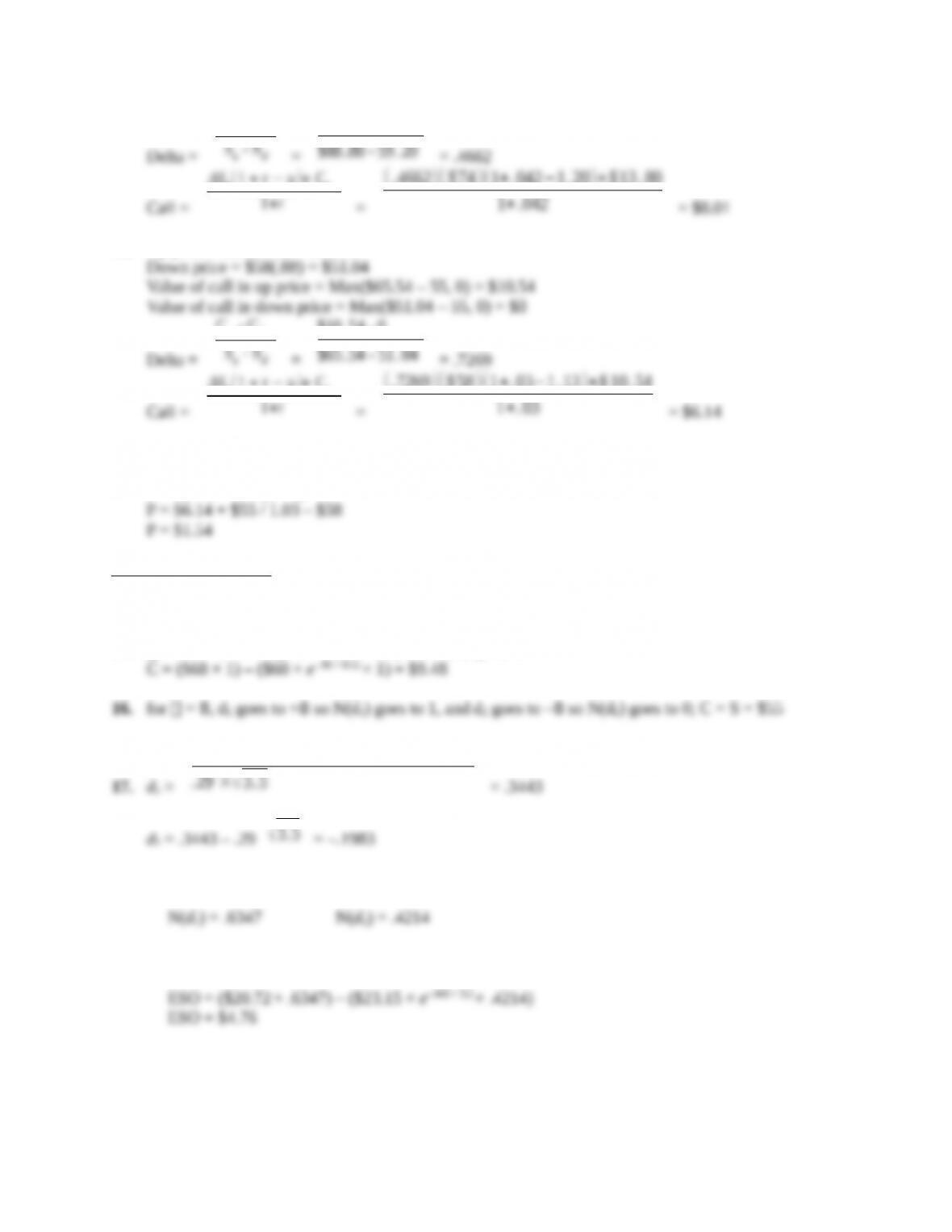

12. Up price = $74(1.2) = $88.80

Down price = $74(.8) = $59.20

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

Delta =

Cu – Cd

Su – Sd

=

$13 .80 – 0

$88 .80 – 59 .20

= .4662

Call =

ΔSu(1 + r − u )+ Cu

1+r

=

(. 4662)( $74 )(1+. 042−1. 20)+$13 . 80

1+.042

= $8.01

13. Up price = $58(1.13) = $65.54

Delta =

Cu – Cd

Su – Sd

=

$10 .54 – 0

$65 .54 – 51 . 04

= .7269

Call =

ΔSu(1 + r − u )+ Cu

1+r

=

(.7269 )($58 )(1+. 03−1 .13 )+$10. 54

1+. 03

= $6.14

Using put-call parity:

P + S0 = C + K / (1 + r)

Intermediate Questions

14. K = 0, so C = S = $70

15. = 0, so d1 and d2 go to +8, so N(d1) and N(d2) go to 1.

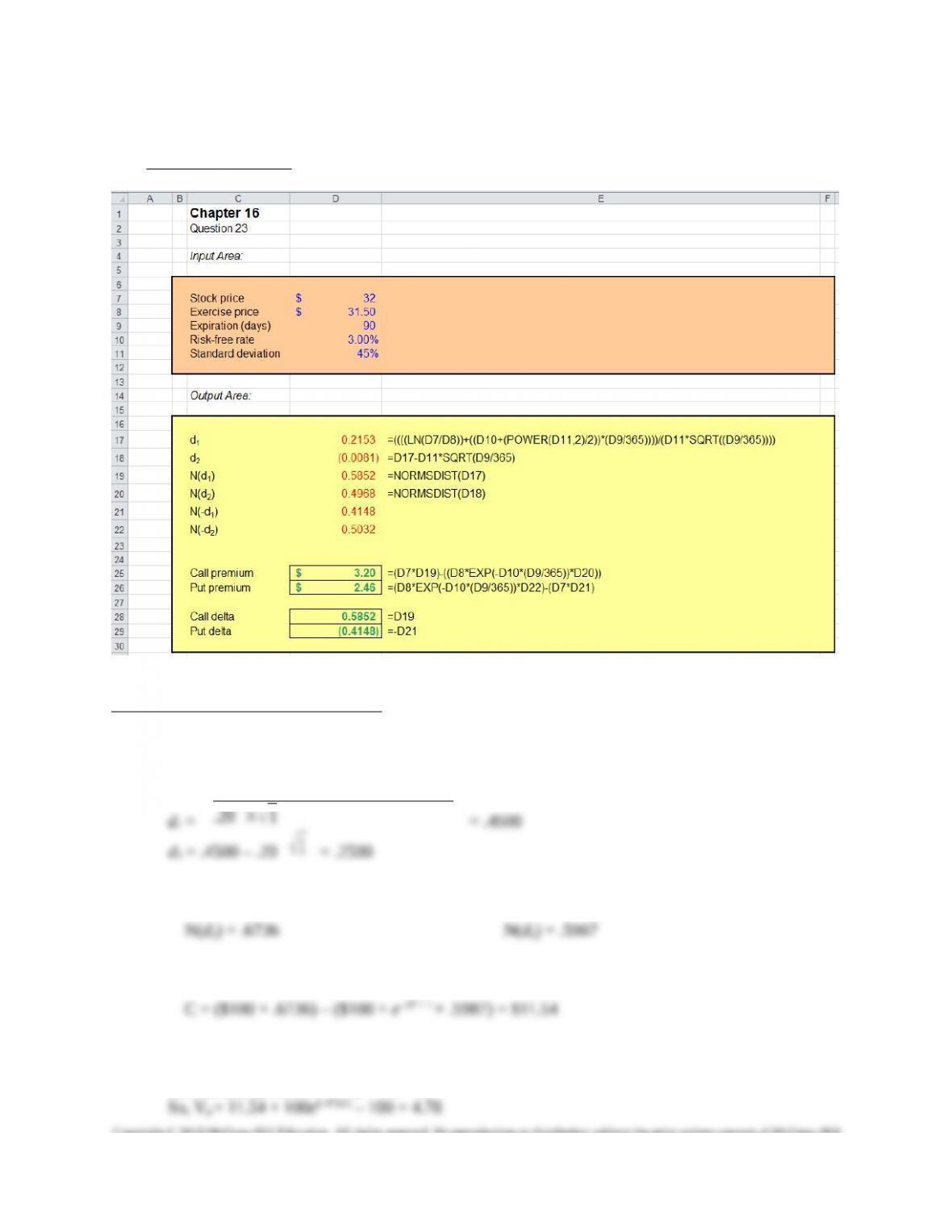

17. d1 =

ln(20 . 72/23 .15 )+(. 043 +. 292/2)× 3. 5

.29 ×

√

3. 5

= .3443

d2 = .3443 – .29

√

3. 5

= –.1983

These standard normal probabilities are given:

Calculating the price of the employee stock options yields:

18. This is a hedging problem in which you wish to hedge one option position with another. Your

employee stock option (ESO) position represents 10,000 shares, and you need to know how many

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

Using values from the previous answer, the ESO delta is

ESO (Call) Delta = N(d1) = .6347

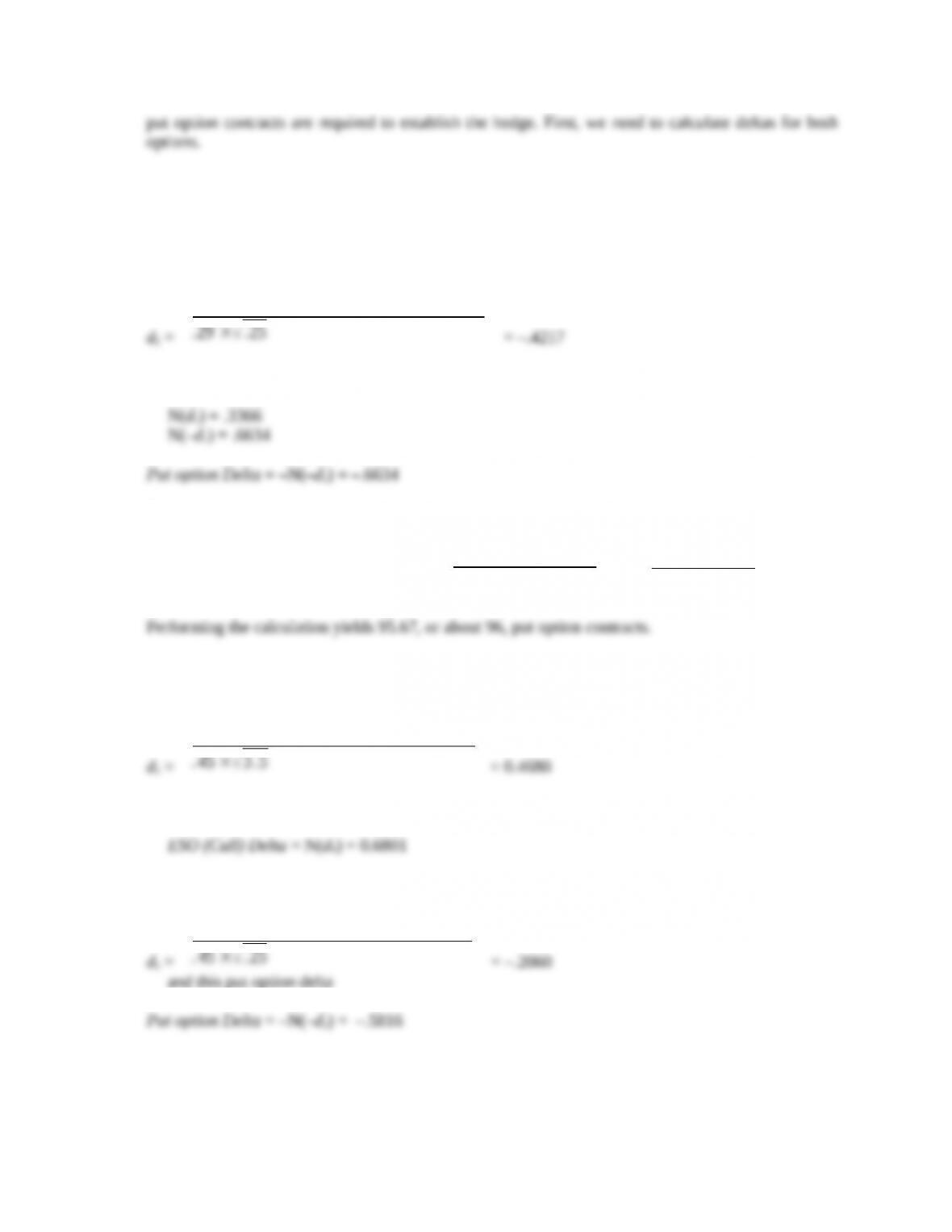

For the put option, we get this value for d1

d1 =

ln(20 . 72 / 22 .50 )+(. 043 +.292/ 2)×. 25

.29 ×

√

.25

= –.4217

These standard normal probabilities are given:

The number of put option contracts is then calculated as

Number of option contracts = –

ESO delta ×10,000

Put option delta × 100

= –

.6347 × 10,000

−.6634 × 100

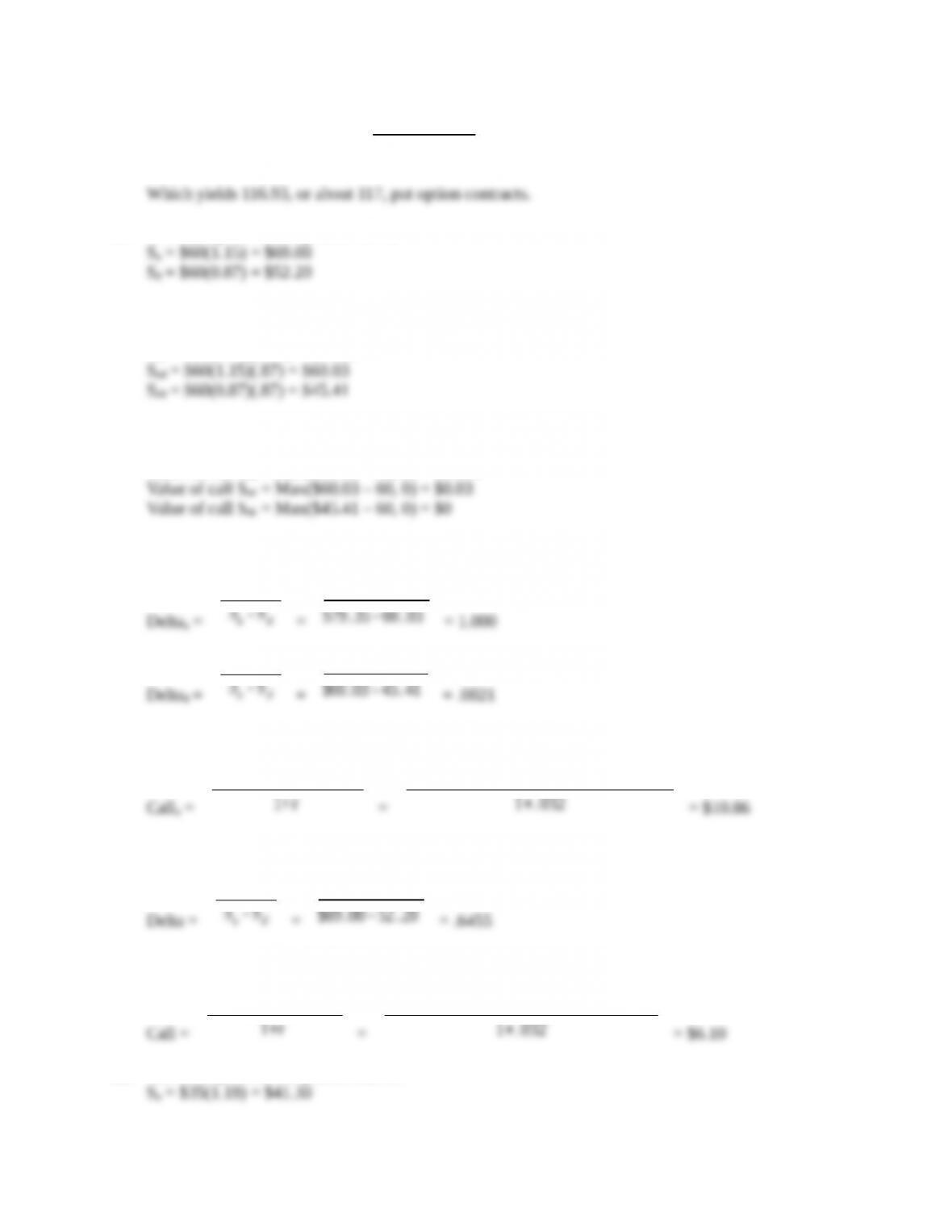

Performing the calculation yields 95.67, or about 96, put option contracts.

19. After the volatility shift, we need to recalculate deltas for both options. The new value of d1 for

the ESO is:

d1 =

ln(20 . 72/23.15 )+(. 043 +. 452/2)× 3 .5

. 45 ×

√

3 .5

= 0.4680

In turn, the new ESO delta is

For the put option, we obtain this value for d1

d1 =

ln(20 . 72/22.50 )+(. 043 +. 452/2)×. 25

. 45 ×

√

. 25

= –.2060

and this put option delta

The new number of contracts required is:

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

Number of option contracts = –

.6801×10 ,000

−. 5816×100

Which yields 116.93, or about 117, put option contracts.

20. The stock price in one period will be:

In two periods, the stock price will be:

Suu = $60(1.15)(1.15) = $79.35

The call value for each node is:

Value of call Suu = Max($79.35 – 60, 0) = $19.35

The delta of the up and down moves will be:

Deltau =

Cu – Cd

Su – Sd

=

$19 .35 – 0 . 03

$79 .35 – 60 .03

= 1.000

Deltad =

Cu – Cd

Su – Sd

=

$0 .03 – 0

$60 .03 – 45 . 41

= .0021

So the call value after an up move will be:

Callu =

ΔSu(1 + r − u )+ Cuu

1+r

=

(1. 00 )($69 )(1+. 032−1. 15 )+$19 . 35

1+. 032

= $10.86

The value of a call with a first down move is $0 since it will always be worthless. The delta today is:

Delta =

Cu – Cd

Su – Sd

=

$10 .86 – 0. 02

$69 .00 – 52 .20

= .6455

So, the value of call today is:

Call =

ΔS(1 + r − u )+ Cu

1+r

=

(.6455 )($60)(1+. 032−1 .15 )+$10. 86

1+.032

= $6.10

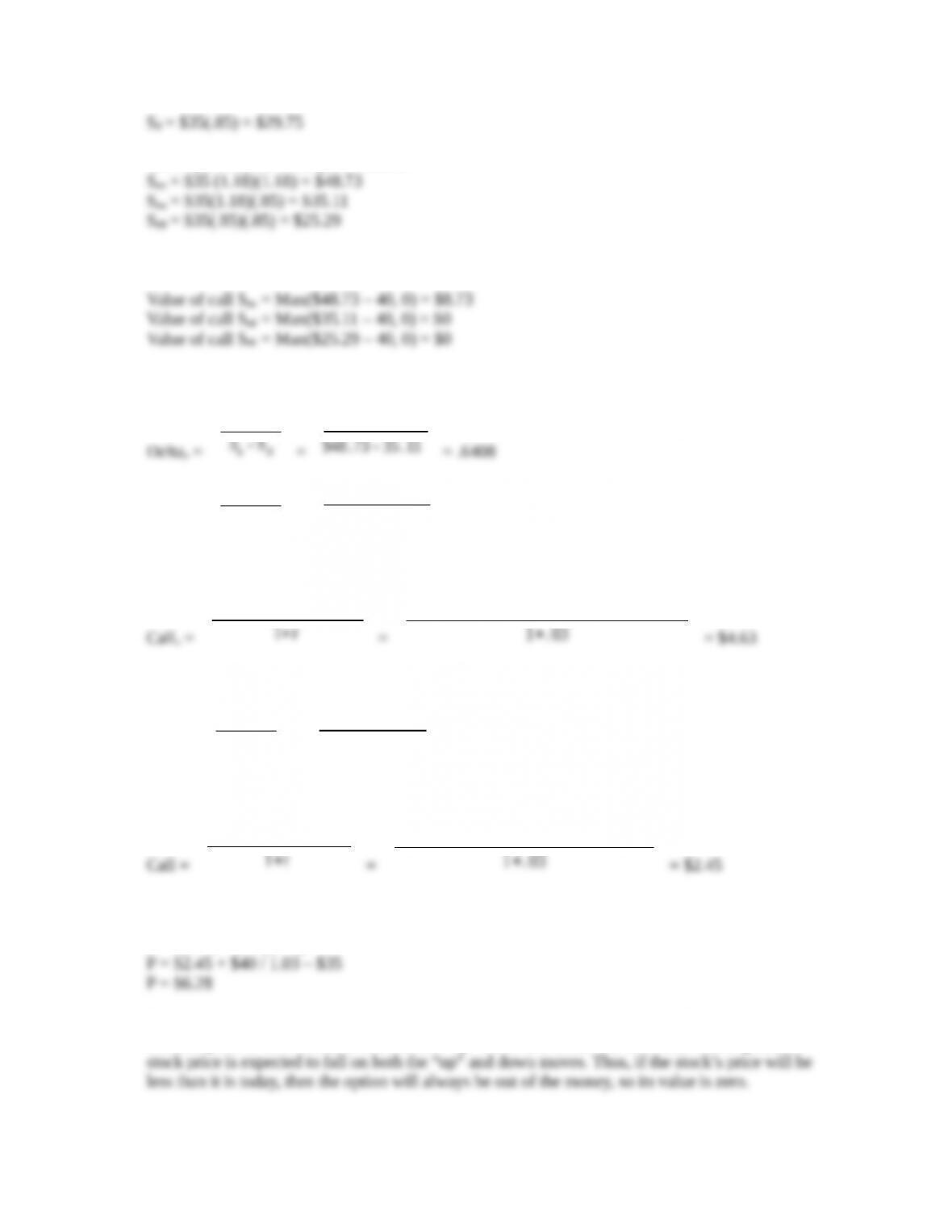

21. The stock price in one period will be:

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

In two periods, the stock price will be:

The call value for each node is:

The delta of the up and down moves will be:

Deltau =

Cu – Cd

Su – Sd

=

$8 .73 – 0

$48 .73 – 35 .11

= .6408

Deltad =

Cu – Cd

Su – Sd

=

$0 – 0

$35 .11 – 25 .29

= 0

So the call value after an up move will be:

Callu =

ΔSu(1 + r − u )+ Cuu

1+r

=

(.6408 )($41 .30 )(1+.03−1 .18 )+$8. 73

1+. 03

= $4.63

The value of a call with a first down move is $0 since it will always be worthless. The delta today is:

Delta =

Cu – Cd

Su – Sd

=

$4 . 63 – 0

$41. 30-29 . 75

= .4005

So, the value of call today is:

Call =

ΔS(1 + r − u )+ Cu

1+r

=

(. 4005)( $35 )(1+. 03−1. 18)+$4 .63

1+. 03

= $2.45

Using put-call parity:

P + S0 = C + K / (1 + r)

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

Spreadsheet Answers

CFA Exam Review by Kaplan Schweser

1. c

ln(100 / 100)+(. 07 +. 202/ 2)× 1

.20 ×

1

The standard normal probabilities are:

Calculating the price of the call option yields:

2. a

Put-call parity states: S + Vp = Vc + Xe-rt

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

3. b

4. b

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.