Chapter 15

Stock Options

Concept Questions

1. Assuming American-style exercise rights, a call option confers the right, without the obligation, to

buy an asset at a given price on or before a given date. An American-style put option confers the

right, without the obligation, to sell an asset at a given price on or before a given date. European-

2. a. The buyer of a call option pays money for the right to buy….

3. In general, the breakeven stock price for a call purchase is the exercise price plus the premium paid.

4. If you buy a put option on a stock that you already own, you guarantee that you can sell the stock for

6. The intrinsic value of a put option at expiration is max{0, K – S}. By definition, the intrinsic value

7. The call is selling for less than its intrinsic value; an arbitrage opportunity exists. Buy the call for

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

11. The March call and the October put are mispriced. The call is mispriced because it is selling for less

than its intrinsic value. The arbitrage is to buy the call for $3.50, exercise it and pay $55 for a share

of stock, and sell the stock for $59 for a riskless profit of $0.50. The October put is mispriced

12. The covered put would represent writing put options on the stock. This strategy is analogous to a

The protective call would represent the purchase of call options as a form of insurance for the short

13. The call is worth more. To see this, we can rearrange the put-call parity condition as follows:

C – P = S – K/(1+r)T

If the options are at the money, S = K, then the right-hand side of this expression is equal to the stock

14. Looking at the previous answer, if the call and put have the same price (i.e., C – P = 0), it must be

Solutions to Questions and Problems

NOTE: All end of chapter problems were solved using a spreadsheet. Many problems require multiple

steps. Due to space and readability constraints, when these intermediate steps are included in this

solutions manual, rounding may appear to have occurred. However, the final answer for each problem is

found without rounding during any step in the problem.

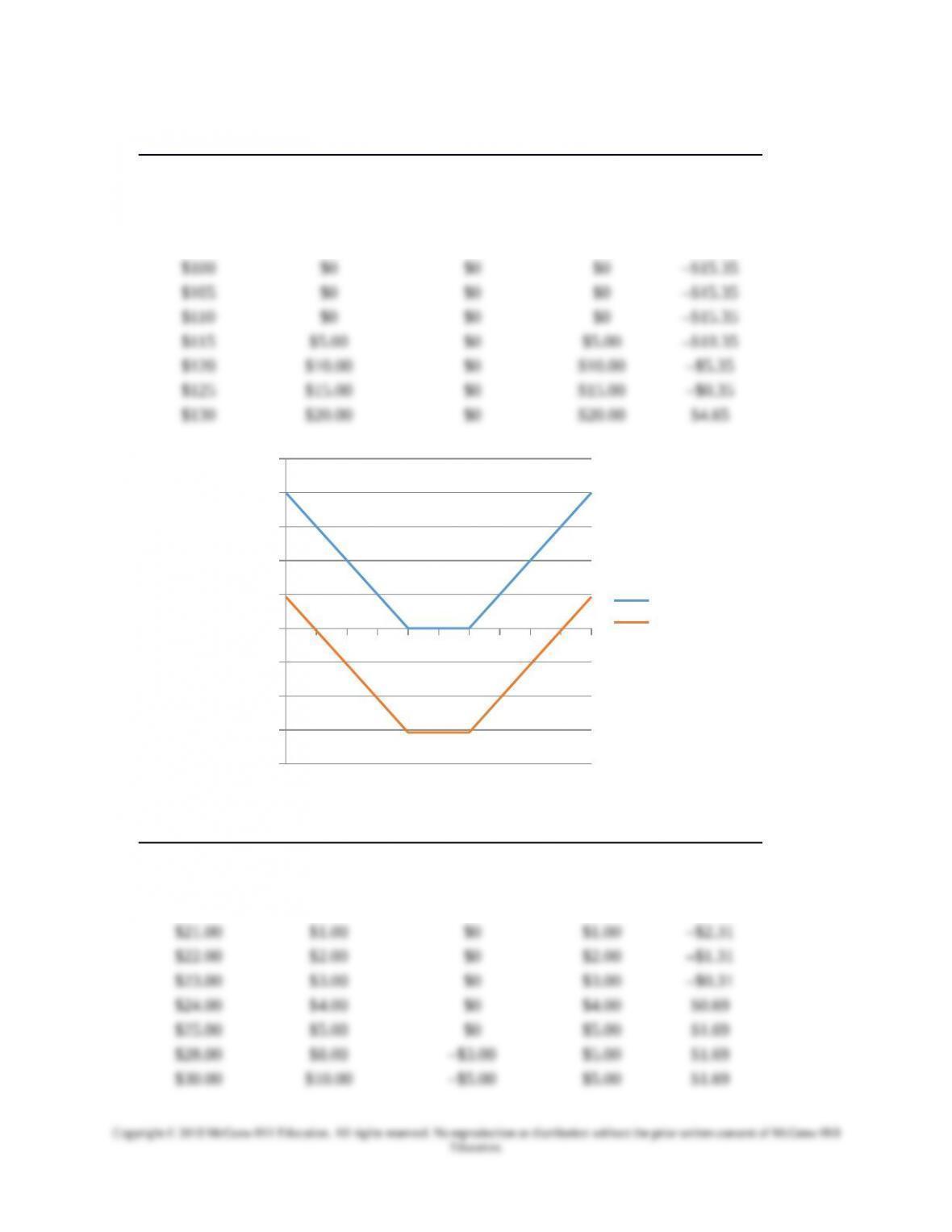

Core Questions

1. Your options are worth $64 – 60 = $4 each, or $400 per contract. With eight contracts, the total value

2. Your options are worth $45 – 39 = $6 each, or $600 per contract. With five contracts, the total value

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

3. The stock costs $50 per share, so if you invest $97,500, you’ll get 1,950 shares. The option premium

is $1.95, so an option contract costs $195. If you invest $97,500, you’ll get $97,500 / $195 = 500

If the stock is selling for $50, your profit is $0 on the stock, so your percentage return is 0%. Your

7. Stock price = $90:

Initial revenue = 30(100)($10.10) = $30,300

8. P = C – S + K / (1 + r)T

9. S = C – P + K / (1 + r)T

10. C = S + P – K / (1 + r)T

Intermediate Questions

11. Div = $1.45 / (1 + .04)2/12 = $1.44

12. Div = $2.10 / (1 + .06)3/12 = $2.07

S = C – P + Div + K / (1 + r)T

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

13. Div = $1.40 / (1 + .05)2/12 = $1.39

14. You get to keep the premium in all cases. For 10 contracts and a $2.75 premium, that’s $2,750. If the

15. You get to keep the premium in all cases. For 15 contracts and a $2.40 premium, that’s $3,600. If the

16. The contract costs $1,400. At maturity, an in-the-money SPX option is worth 100 times the

17.

Stock price Short profit

Short put

payoff

Short

put profit Net profit

$50.00 $10.00 –$10.00 –$8.20 $1.80

18.

Stock price Short profit Call payoff Call profit Net profit

$60 $10 $0 –$3.40 $6.60

$65 $5 $0 –$3.40 $1.60

19.

Stock price Short profit

Short

Put payoff

Protective

Call payoff Total payoff

$70 $10 –$10 $0 $0

20. Stock price Put payoff Call payoff Total payoff

$70 –$10 $0 –$10

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

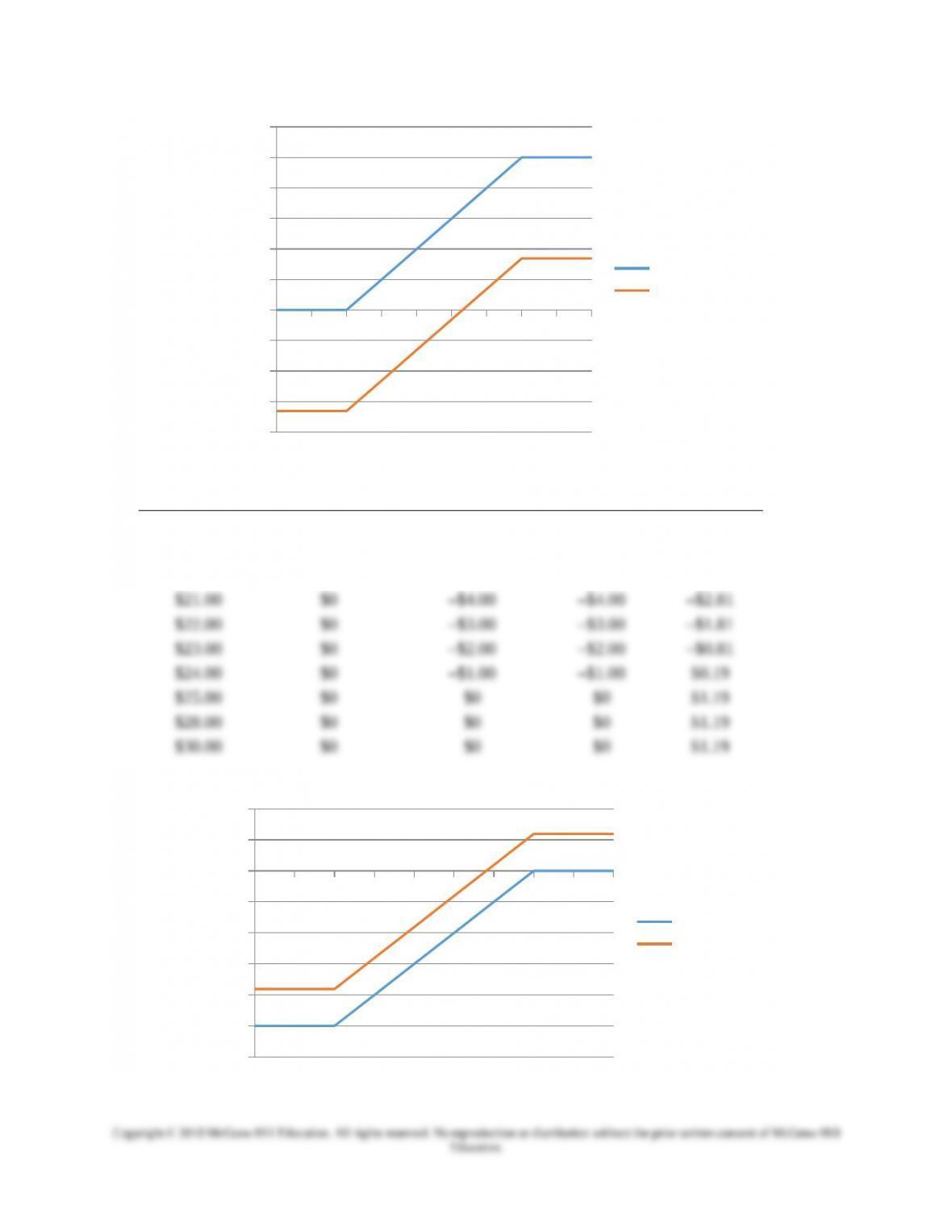

21. Cost of strategy = $4.20 + 2.80 = $7.00

Stock price Call payoff Put payoff Total payoff Total profit

$65 $0 $10 $10 $3.00

22.

Index level

Long call

payoff

Short call

payoff Total payoff

2050 0 0 0

23.

Index level

Long put

payoff

Short put

payoff Total payoff

2000 100 –125 –25

24.

Index level

Long call

payoff

Short put

payoff Total payoff

2000 0 –100 –100

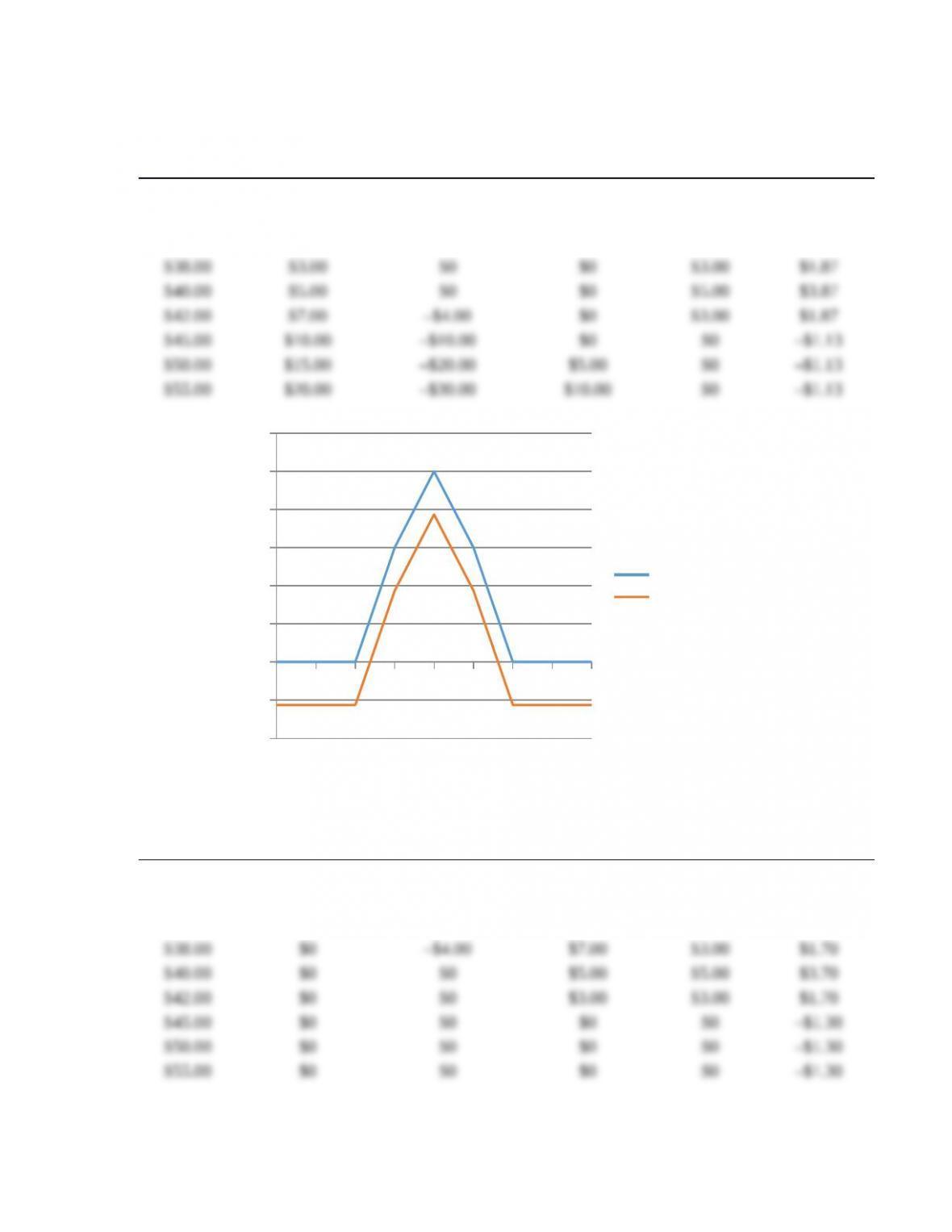

25.

Index level

Long call

payoff (1300)

Long call

payoff (1500)

Short call (2)

payoff (1400) Total payoff

1900 0 0 0 0

1950 0 0 0 0

2050 50 0 0 50

2100 100 0 0 100

2150 150 0 –100 50

$80.00

$85.00

$90.00

$95.00

$100.00

$105.00

$110.00

$115.00

$120.00

$125.00

$130.00

$(20.00)

$(15.00)

$(10.00)

$(5.00)

$–

$5.00

$10.00

$15.00

$20.00

$25.00

Total payof

Total profit

27. Total cost = $4.55 – 1.24 = $3.31

Stock price Long call payoff Short call payoff Total payoff Total profit

$15.00 $0 $0 $0 –$3.31

$17.00 $0 $0 $0 –$3.31

$20.00 $0 $0 $0 –$3.31

$21.00 $1.00 $0 $1.00 –$2.31

$22.00 $2.00 $0 $2.00 –$1.31

$23.00 $3.00 $0 $3.00 –$0.31

$24.00 $4.00 $0 $4.00 $0.69

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

$15.00

$17.00

$20.00

$21.00

$22.00

$23.00

$24.00

$25.00

$28.00

$30.00

$(4.00)

$(3.00)

$(2.00)

$(1.00)

$–

$1.00

$2.00

$3.00

$4.00

$5.00

$6.00

Total payof

Total profit

28. Total cost = $0.45 – 1.64 = -$1.19

Stock price Long put payoff Short put payoff Total payoff Total profit

$15.00 $5.00 –$10.00 –$5.00 –$3.81

$17.00 $3.00 –$8.00 –$5.00 –$3.81

$20.00 $0 –$5.00 –$5.00 –$3.81

$15.00

$17.00

$20.00

$21.00

$22.00

$23.00

$24.00

$25.00

$28.00

$30.00

$(6.00)

$(5.00)

$(4.00)

$(3.00)

$(2.00)

$(1.00)

$–

$1.00

$2.00

Total payof

Total profit

$25.00

$30.00

$35.00

$38.00

$40.00

$42.00

$45.00

$50.00

$55.00

$(2.00)

$(1.00)

$–

$1.00

$2.00

$3.00

$4.00

$5.00

$6.00

Total payof

Total profit

30. Total cost = –$0.90 + 2($2.35) – $5.10 = –$1.30

Stock price Long put payoff

Short put payoff

(2x) Long put payoff Total payoff Total profit

$25.00 $10.00 –$30.00 $20.00 $0 –$1.30

$30.00 $5.00 –$20.00 $15.00 $0 –$1.30

$35.00 $0 –$10.00 $10.00 $0 –$1.30

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

$25.00

$30.00

$35.00

$38.00

$40.00

$42.00

$45.00

$50.00

$55.00

$(2.00)

$(1.00)

$–

$1.00

$2.00

$3.00

$4.00

$5.00

$6.00

Total payof

Total profit

CFA Exam Review by Kaplan Schweser

1. b

Put-call parity states: S + Vp = Vc + Xe-rt

2. a

3. b

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.