Chapter 12

Return, Risk, and the Security Market Line

Concept Questions

1. Some of the risk in holding any asset is unique to the asset in question. By investing in a variety of

assets, this unique portion of the total risk can be almost completely eliminated at little cost. On the

2. If the market expected the growth rate in the coming year to be 2 percent, then there would be no

change in security prices if this expectation had been fully anticipated and priced. However, if the

3. a. systematic

b. unsystematic

4. a. An unexpected, systematic event occurred; market prices in general will most likely

decline.

b. No unexpected event occurred; company price will most likely stay constant.

6. Earnings contain information about recent sales and costs. This information is useful for projecting

7. Yes. It is possible, in theory, for a risky asset to have a beta of zero. Such an asset’s return is simply

uncorrelated with the overall market. Based on the CAPM, this asset’s expected return would be

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

8. The rule is always “buy low, sell high.” In this case, we buy the undervalued asset and sell (short) the

overvalued one. It does not matter whether the two securities are misvalued with regard to some

9. If every asset has the same reward-to-risk ratio, the implication is that every asset provides the same

risk premium for each unit of risk. In other words, the only way to increase your return (reward) is to

accept more risk. Investors will only take more risk if the reward is higher, and a constant reward-to-

10. a. Systematic risk refers to fluctuations in asset prices caused by macroeconomic factors that are

common to all risky assets; hence systematic risk is often referred to as market risk. Examples of

b. Trudy should explain to the client that picking only the top five best ideas would most likely result

in the client holding a much more risky portfolio. The total risk of the portfolio, or portfolio

variance, is the combination of systematic risk and firm-specific risk. i.) The systematic component

depends on the sensitivity of the individual assets to market movements as measured by beta.

Solutions to Questions and Problems

NOTE: All end of chapter problems were solved using a spreadsheet. Many problems require multiple

steps. Due to space and readability constraints, when these intermediate steps are included in this

solutions manual, rounding may appear to have occurred. However, the final answer for each problem is

found without rounding during any step in the problem.

Core Questions

1. E(Ri) = .132 = .035 + .075i ; i = 1.29

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

3. E(Ri) = .12 = Rf + (.10 – Rf)(1.40); Rf = .05

6. Portfolio value = 400($60) + 500($85) + 900($25) = $89,000

7. P = 1.0 = 1/3(0) + 1/3(1.20) + 1/3(X) ; X = 1.80

9. E(Ri) = .055 + (.12 – .055)(1.2) = .1330

10. a. E(RP) = (.09 + .04) / 2 = .0650

b. P = 0.5 = xS(0.9) + (1 – xS)(0) ; xS = .5 / .9 = .5556 ; xrf = 1 – .5556 = .4444

Intermediate Questions

11. P = xW(1.1) + (1 – xW)(0) = 1.1xW

xWE[rp]pxWE[rp]p

0% 4.00% .00 100% 12.00% 1.10

12. E[Rii] = .05 + .07i

.13 > E[RY] = .05 + .07(1.05) = .1235; Y plots above the SML and is undervalued.

13. [.13 – Rf]/1.05 = [.09 – Rf] / 0.70 ; Rf = .01

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

14. (E(RA) – Rf)/ A = (E(RB) – Rf)/ B

15. Here we have the expected return and beta for two assets. We can express the returns of the two

(.123 – Rf) / 1.05 = (.118 – Rf) / .90

Now using CAPM to find the expected return on the market with both stocks, we find:

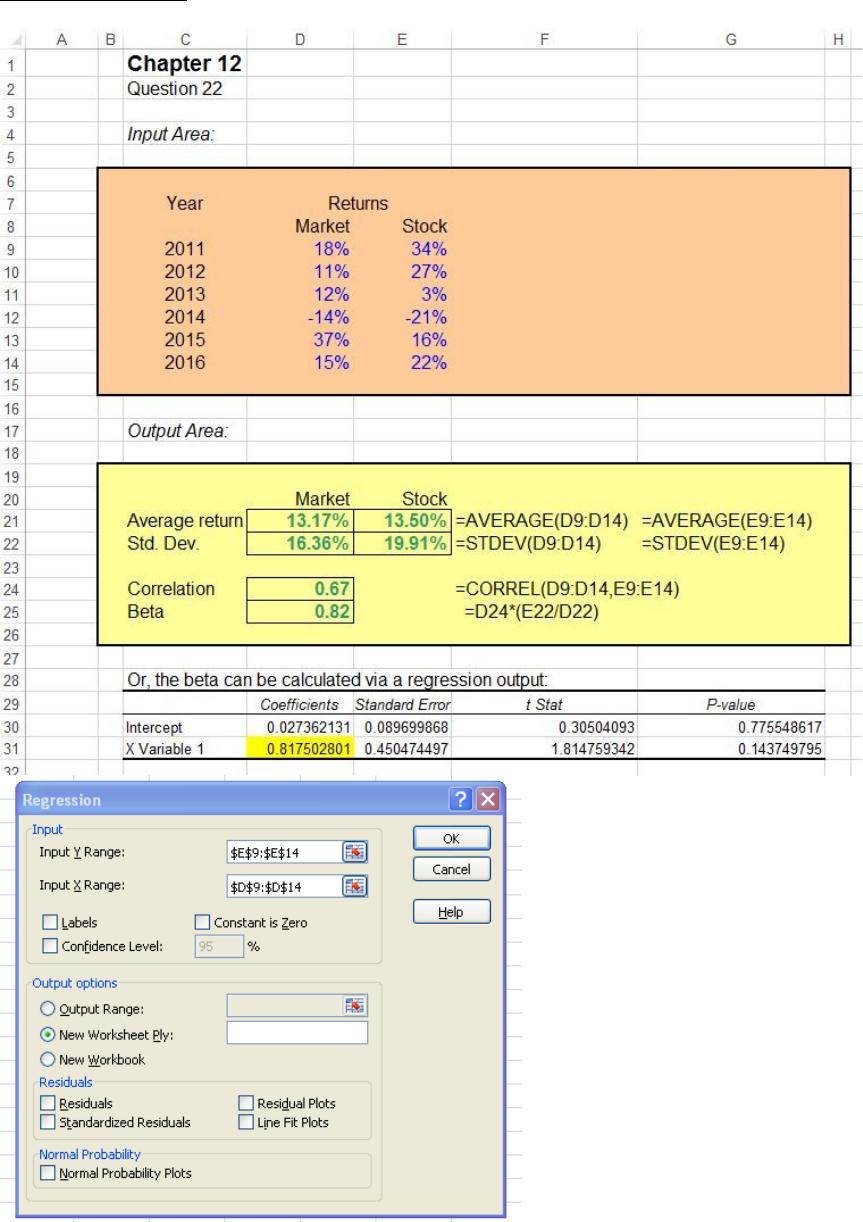

17. The relevant calculations can be summarized as follows:

Returns Return deviations Squared deviations

Product

of

deviations

Year Security Market Security Market Security Market

2012 8% 5% -5% -2% .00250 .00032 .00090

2013 -18% -14% -31% –21% .09610 .04326 .06448

Average returns: Variances: Standard deviations:

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

18. E[Rp] = .13 = wX(.31) + wY(.20) + (1 – wX – wY)(.07)

19. E[RI] = .30(.05) + .40(.19) + .30(.13) = .1300 ; .1300 = .05 + .08I , I = 1.00

σI

2

σII

2

Although stock II has more total risk than I, it has much less systematic risk, since its beta is much

20. E(R) = .05 + 1.15[.13 – .05] = 14.20%

Unexpected

Returns

Systematic

Portion

Unsystematic

Portion

Year R – E(R) RM – E(RM) × [RM – E(RM)] R – E(R) – × [RM – E(RM)]

2012 –4.20% –1.00% -1.15% –3.05%

21. Furhman Labs: E(R) = 4.0% + 1.2(11.5% – 4.0%) = 13.00% Undervalued

*Supporting calculations

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

Spreadsheet Problem

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

CFA Exam Review by Kaplan Schweser

1. a

2. c

3. a

Montana’s required return = 7% + 7%(1.5) = 17.5%. Since this required return is higher than the

4. b

Since the security market line runs from the risk-free rate through the market return, holding the

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.