Chapter 11

Diversification and Risky Asset Allocation

Concept Questions

1. Based on market history, the average annual standard deviation of return for a single, randomly

2. If the returns on two stocks are highly correlated, they have a strong tendency to move up and down

6. The common answer might be that over time volatility cancels out; however, this is incorrect and is

7. An investment with high volatility could actually reduce the risk of the overall portfolio if its

8. The importance of the minimum variance portfolio is that it determines the lower bound of the

10. If two assets have zero correlation and the same standard deviation, then evaluating the general

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

Solutions to Questions and Problems

NOTE: All end of chapter problems were solved using a spreadsheet. Many problems require multiple

steps. Due to space and readability constraints, when these intermediate steps are included in this

solutions manual, rounding may appear to have occurred. However, the final answer for each problem is

found without rounding during any step in the problem.

Core Questions

1. .25(–.08) + .5(.13) + .25(.23) = 10.25%

4.

Calculating Expected Returns

Roll Ross

(1)

State of

Economy

(2)

Probability of

State of

Economy

(3)

Return if

State

Occurs

(4)

Product

(2) × (3)

(5)

Return if

State

Occurs

(6)

Product

(2) × (5)

Bust .40 –10% –.0400 21% .0840

5.

(1)

State

of Economy

(2)

Probability of

State of

Economy

(3)

Return Deviation

from Expected

Return

(4)

Squared

Return

Deviation

(5)

Product

(2) × (4)

Roll

Bust .40 –.2280 .0520 .0208

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

6.

Expected Portfolio Return

(1)

State of

Economy

(2)

Probability of

State of

Economy

(3)

Portfolio Return if State Occurs

(4)

Product

(2) × (3)

7.

Calculating Portfolio Variance

(1)

State of

Economy

(2)

Probability of

State of Economy

(3)

Portfolio Return

if State Occurs

(4)

Squared Deviation from

Expected Return

(5)

Product

(2) × (4)

8. E[RA] = .3(.04) + .4(.09) + .3(.12) = 8.40%

9. a. boom: E[Rp] = .25(.18) + .50(.48) + .25(.33) = .3675

good: E[Rp] = .25(.11) + .50(.18) + .25(.15) = .1550

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

10. Notice that we have historical information here, so we calculate the sample average and sample

standard deviation (using n – 1) just like we did in Chapter 1. Notice also that the portfolio has less

risk than either asset.

Annual Returns on Stocks A and B

Year Stock A Stock B Portfolio AB

2012 11% 21% 17.00%

Intermediate Questions

11. Boom: .35(15%) + .45(18%) + .20(20%) = 17.35%

σP

2

12. E(RP) = .50(.14) + .50(.10) = 12.00%

σP

2

13.

σP

2

= .502(.422)+ .502(.312) + 2(.50)(.50)(.42)(.31)(1.0) = .13323; σP = 36.50%

σP

2

σP

2

As the correlation becomes smaller, the standard deviation of the portfolio decreases. In the extreme,

14. w3 Doors =

.312 – . 42 ×.31 ×.10

. 422+. 312 – 2 ×.42 ×.31 ×.10

= .33709; wDown = (1 – .33709) = .66291

σP

2

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

15.

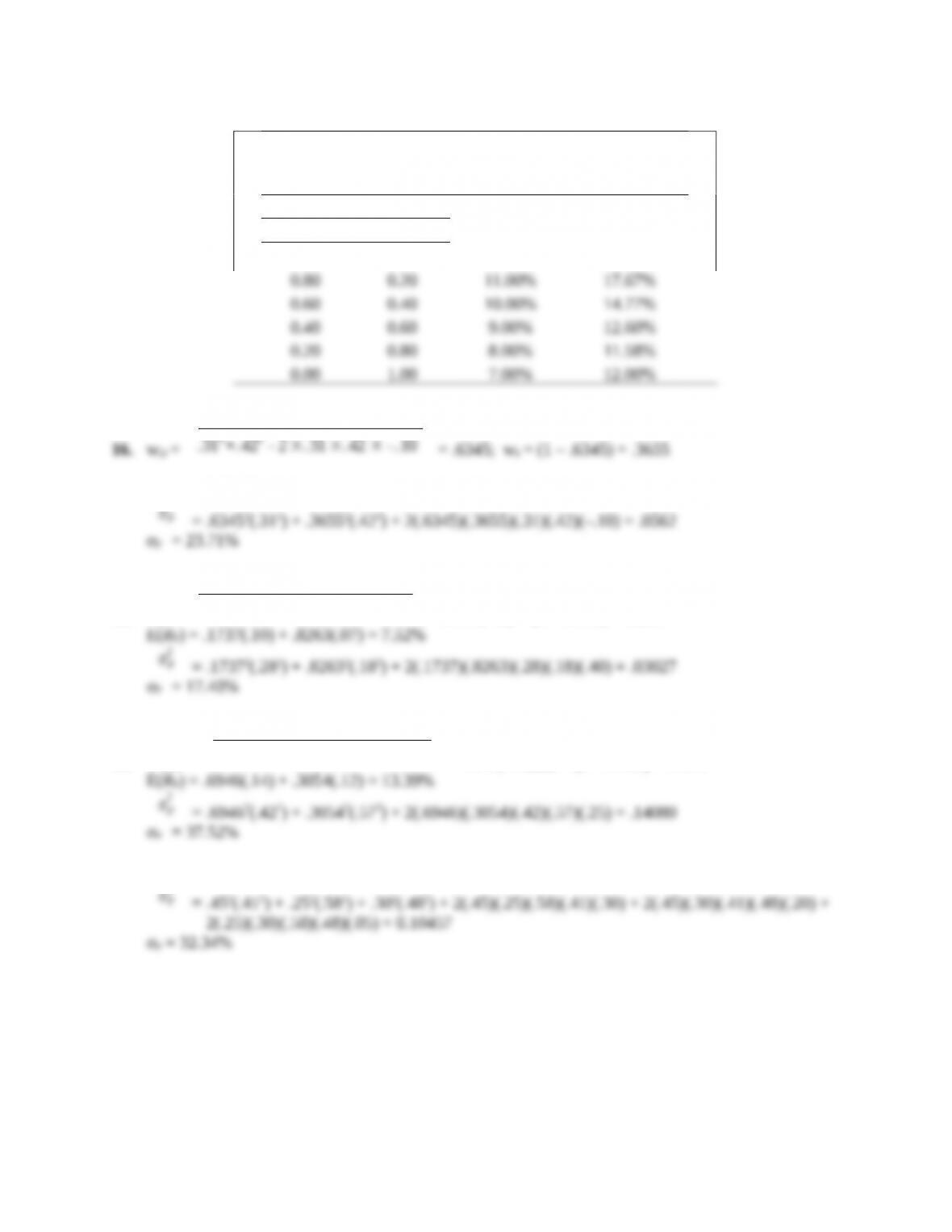

Risk and Return with Stocks and Bonds

Portfolio Weights Expected Standard

Stocks Bonds Return Deviation

1.00 0.00 12.00% 21.00%

16. wD =

. 422 – .31 ×. 42 × – . 10

.312+. 422 – 2 ×.31 ×. 42 × –. 10

= .6345; wI = (1 – .6345) = .3655

17. E(RP) = .6345(.13) + .3655(.16) = 14.10%

σP

2

18. wK =

.182 – . 28 ×. 18 ×. 40

.282+. 182 – 2 ×. 28 ×. 18 ×. 40

= .1737; wL = (1 – .1737) = .8263

σP

2

19. wBruin =

.572 – . 42 ×. 57 ×. 25

. 422+. 572 – 2 ×.57 ×. 42×. 25

= .6946; wWildcat = (1 – .6946) = .3054

σP

2

= .69462(.422) + .30542(.572) + 2(.6946)(.3054)(.42)(.57)(.25) = .14080

σP = 37.52%

20. E(R) = .45(12%) + .25(16%) + .30(13%) = 13.30%

σP

2

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

21. wJ =

.192 – . 54 ×. 19 ×. 50

.542+. 192 – 2 ×.54 ×.19 ×.50

= –.0675; wS = (1 – (–.0675)) = 1.0675

σP

2

Even though it is possible to mathematically calculate the standard deviation and expected return of

a portfolio with a negative weight, an explicit assumption is that no asset can have a negative weight.

The reason this portfolio has a negative weight in one asset is the relatively high correlation between

is:

σmin

σmax

> . In this case,

.19

.54

= .3519 < .50 so there is no minimum variance portfolio with a

variance lower than the lowest variance asset assuming non-negative asset weights.

22. Look at

σP

2

:

σP

2

σP

2

σP

2

25. Let stand for the correlation, then:

σP

2

=

xA

2×σA

2+ xB

2×σB

2+ 2 × x A× xB×σA×σB×ρ

= x2 × σA2 + (1 – x)2 × σB2 + 2 × x × (1 – x) × σA × σB ×

Take the derivative with respect to x and set equal to zero:

Solve for x to get the expression in the text.

CFA Exam Review by Kaplan Schweser

1. b

Simply increasing return may not be appropriate if the risk level increases more than the return.

2. a

3. b

4. c

5. c

Since the beta of Beta Naught is zero, its correlation with any of the other funds is zero. Thus, the

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.