Solutions Manual, Chapter 9 31

Problem 9-18 (continued)

2.

Minden Company

Budgeted Income Statement

For the Month of May

Sales ……………………………………………….

$220,000

Cost of goods sold:

Beginning inventory ………………………….

$ 30,000

Add purchases …………………………………

120,000

Goods available for sale ……………………..

150,000

Ending inventory ………………………………

40,000

Cost of goods sold ………………………………

110,000

Gross margin ……………………………………..

110,000

Selling and administrative expenses

($72,000 + $2,000) ………………………….

74,000

Net operating income ………………………….

36,000

Interest expense ………………………………..

100

Net income …………………………..…………..

$ 35,900

3.

Minden Company

Budgeted Balance Sheet

May 31

Assets

Cash ……………………………………………………………….

$ 22,900

Accounts receivable (40% × $160,000) ………………….

64,000

Inventory …………………………………………………………

40,000

Buildings and equipment, net of depreciation

($207,000 + $6,500 – $2,000) …………………………...

211,500

Total assets ………………………………………………………

$338,400

Liabilities and Stockholders’ Equity

Accounts payable (50% × 120,000) ……………………….

$ 60,000

Note payable …………………………………………………….

20,000

Capital stock …………………………………………………….

180,000

Retained earnings ($42,500 + $35,900) ………………….

78,400

Total liabilities and stockholders’ equity …………………..

$338,400

32 Managerial Accounting for Managers, 4th Edition

Problem 9-19 (30 minutes)

1.

December cash sales …………………………….

$ 83,000

Collections on account:

October sales: $400,000 × 18% ……………

72,000

November sales: $525,000 × 60% …………

315,000

December sales: $600,000 × 20% …………

120,000

Total cash collections ………………………….

$590,000

2.

Payments to suppliers:

November purchases (accounts payable) …

$161,000

December purchases: $280,000 × 30% ….

84,000

Total cash payments …………………………..

$245,000

3.

Ashton Company

Cash Budget

For the Month of December

Beginning cash balance ……………………………..

$ 40,000

Add collections from customers ……………………

590,000

Total cash available ……………………………………

630,000

Less cash disbursements:

Payments to suppliers for inventory ……………

$245,000

Selling and administrative expenses* ………….

380,000

New web server ……………………………………..

76,000

Dividends paid ……………………………………….

9,000

Total cash disbursements …………………………...

710,000

Excess (deficiency) of cash available over

disbursements ……………………………………….

(80,000)

Financing:

Borrowings ……………………………………………

100,000

Repayments …………………………..……………..

0

Interest ………………………………………………..

0

Total financing …………………………..……………..

100,000

Ending cash balance ………………………………….

$ 20,000

Solutions Manual, Chapter 9 33

Problem 9-20 (30 minutes)

1. The budget at Springfield is an imposed “top-down” budget that fails to

consider both the need for realistic data and the human interaction

gathering and manipulation of data. This suggests there will be little

enthusiasm for implementing the budget.

The initial meeting between the Vice President of Finance, Executive

2. Springfield should consider adopting a “bottom-up” budget process. This

means that the people responsible for performance under the budget

operates. Although time consuming, the approach should produce a

more acceptable, honest, and workable goal-control mechanism.

discretionary and nondiscretionary. Flexible budgeting techniques could

34 Managerial Accounting for Managers, 4th Edition

Problem 9-20 (continued)

3. The functional areas should not necessarily be expected to cut costs

when sales volume falls below budget. The time frame of the budget

a. control is exercised over the costs within their function.

sales, i.e., slack was present.

serious effect on the department.

(Adapted unofficial CMA Solution)

Solutions Manual, Chapter 9 35

Problem 9-21 (45 minutes)

1. Schedule of expected cash collections:

Month

April

May

June

Quarter

From accounts receivable .

$120,000

$ 16,000

$136,000

From April sales:

30% × $300,000 ……….

90,000

90,000

60% × $300,000 ……….

180,000

180,000

8% × $300,000 …………

$ 24,000

24,000

From May sales:

30% × $400,000 ……….

120,000

120,000

60% × $400,000 ……….

240,000

240,000

From June sales:

30% × $250,000 ……….

75,000

75,000

Total cash collections …….

$210,000

$316,000

$339,000

$865,000

36 Managerial Accounting for Managers, 4th Edition

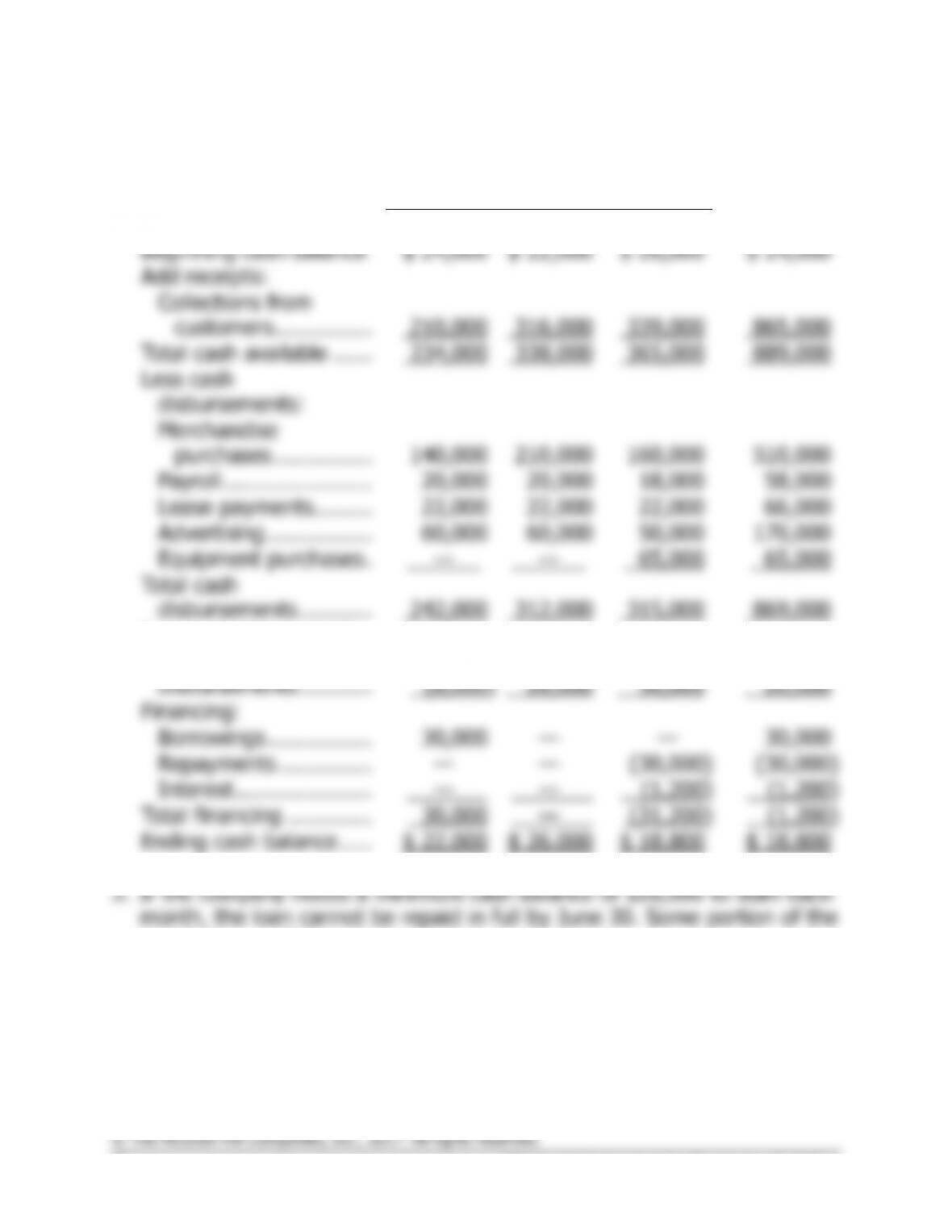

Problem 9-21 (continued)

2. Cash budget:

Month

April

May

June

Quarter

Beginning cash balance

$ 24,000

$ 22,000

$ 26,000

$ 24,000

Add receipts:

Collections from

customers ……………

210,000

316,000

339,000

865,000

Total cash available ……

234,000

338,000

365,000

889,000

Less cash

disbursements:

Merchandise

purchases ……………

140,000

210,000

160,000

510,000

Payroll …………………..

20,000

20,000

18,000

58,000

Lease payments ………

22,000

22,000

22,000

66,000

Advertising …………….

60,000

60,000

50,000

170,000

Equipment purchases .

—

—

65,000

65,000

Total cash

disbursements ………..

242,000

312,000

315,000

869,000

Excess (deficiency) of

cash available over

disbursements ………..

(8,000)

26,000

50,000

20,000

Financing:

Borrowings …………….

30,000

—

—

30,000

Repayments …………..

—

—

(30,000)

(30,000)

Interest …………………

—

—

(1,200)

(1,200)

Total financing ………….

30,000

—

(31,200)

(1,200)

Ending cash balance …..

$ 22,000

$ 26,000

$ 18,800

$ 18,800

loan balance will have to be carried over to July.

Solutions Manual, Chapter 9 37

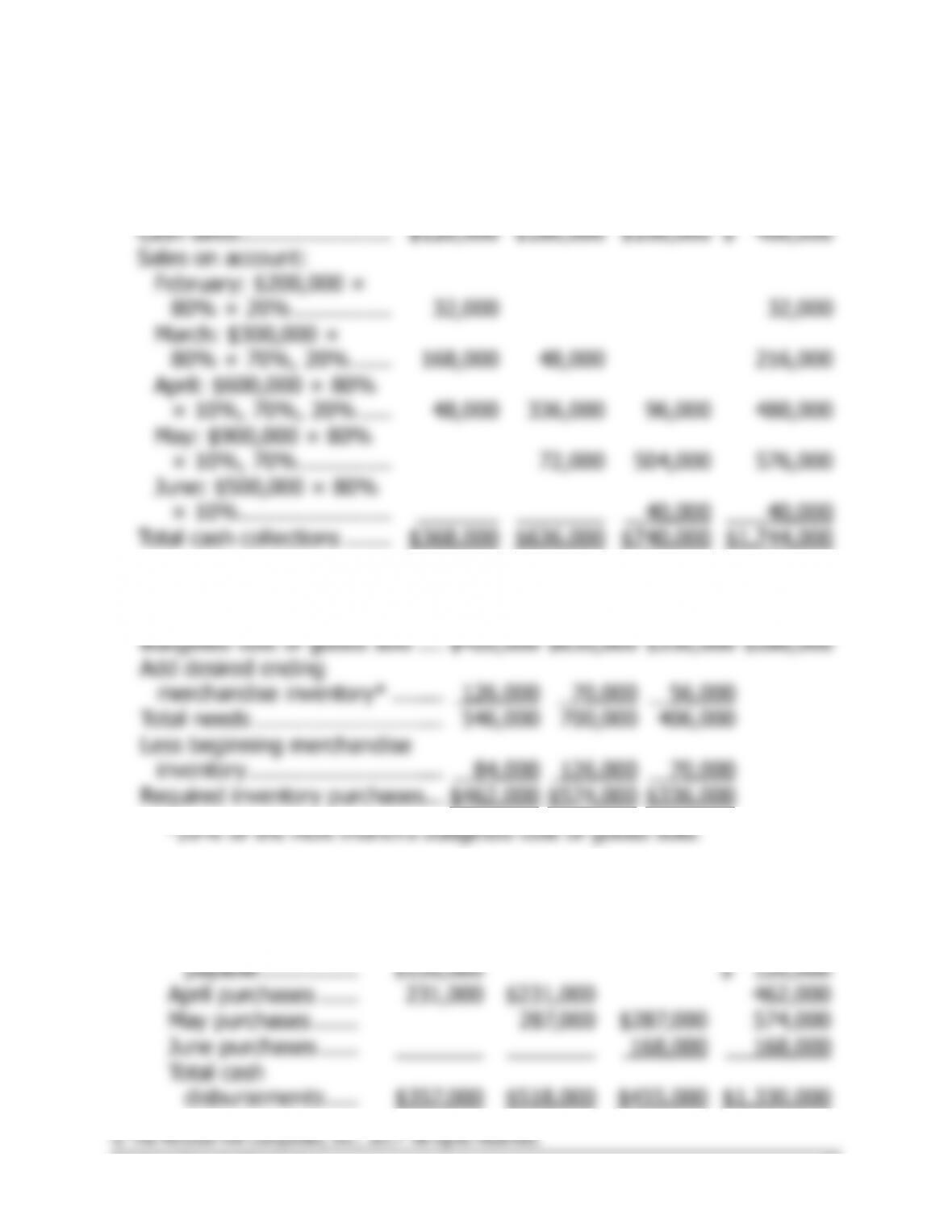

Problem 9-22 (60 minutes)

1. Collections on sales:

April

May

June

Quarter

Cash sales …………………..

$120,000

$180,000

$100,000

$ 400,000

Sales on account:

February: $200,000 ×

80% × 20% ……………

32,000

32,000

March: $300,000 ×

80% × 70%, 20% ……

168,000

48,000

216,000

April: $600,000 × 80%

× 10%, 70%, 20% …..

48,000

336,000

96,000

480,000

May: $900,000 × 80%

× 10%, 70% …………..

72,000

504,000

576,000

June: $500,000 × 80%

× 10% …………………..

40,000

40,000

Total cash collections …….

$368,000

$636,000

$740,000

$1,744,000

2. a. Merchandise purchases budget:

April

May

June

July

Budgeted cost of goods sold ….

$420,000

$630,000

$350,000

$280,000

Add desired ending

merchandise inventory* ……..

126,000

70,000

56,000

Total needs ………………………..

546,000

700,000

406,000

Less beginning merchandise

inventory …………………………

84,000

126,000

70,000

Required inventory purchases…

$462,000

$574,000

$336,000

b. Schedule of expected cash disbursements for merchandise purchases:

April

May

June

Quarter

Beginning accounts

payable ……………

$126,000

$ 126,000

April purchases ……

231,000

$231,000

462,000

May purchases …….

287,000

$287,000

574,000

June purchases ……

168,000

168,000

Total cash

disbursements …..

$357,000

$518,000

$455,000

$1,330,000

38 Managerial Accounting for Managers, 4th Edition

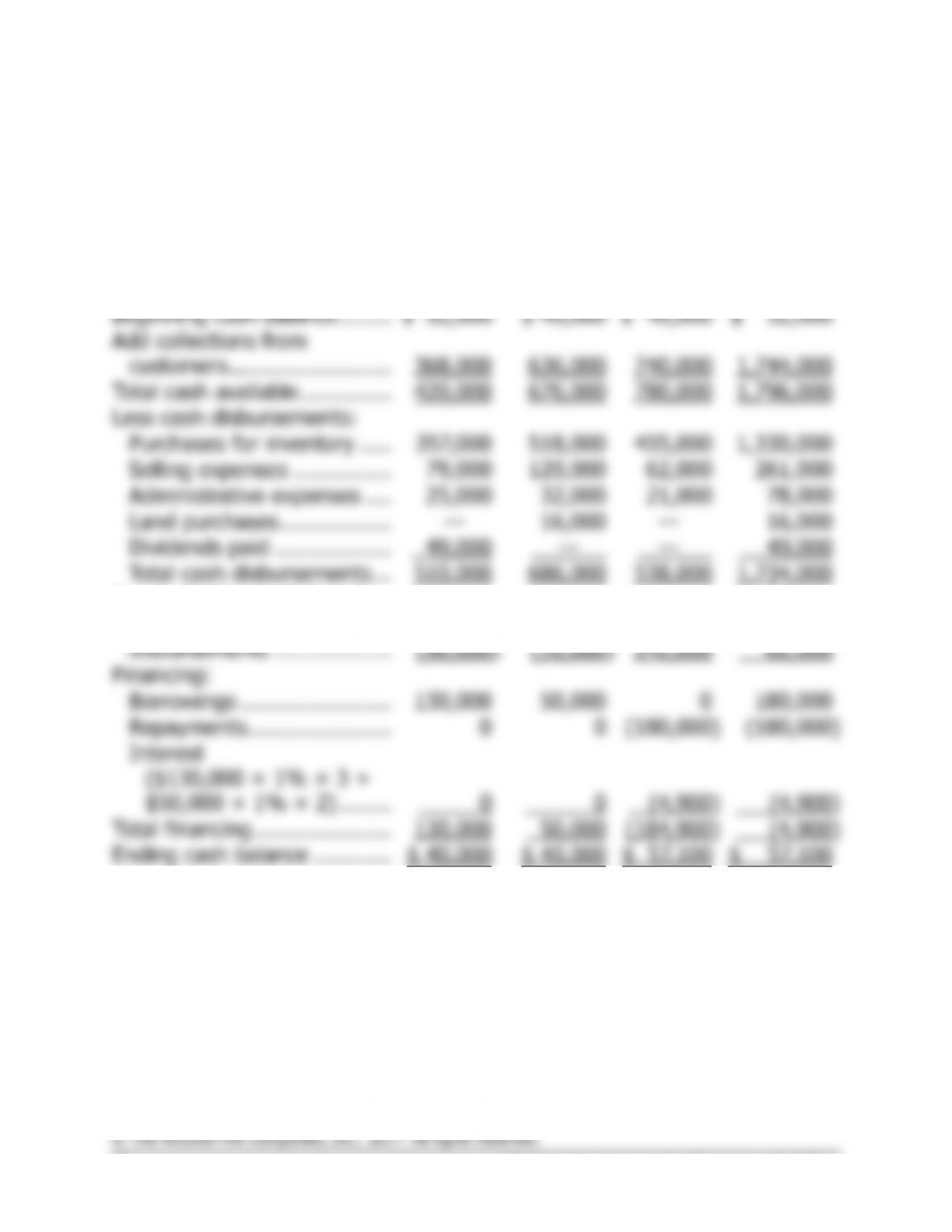

Problem 9-22 (continued)

3.

Garden Sales, Inc.

Cash Budget

For the Quarter Ended June 30

April

May

June

Quarter

Beginning cash balance ……..

$ 52,000

$ 40,000

$ 40,000

$ 52,000

Add collections from

customers …………………….

368,000

636,000

740,000

1,744,000

Total cash available …………..

420,000

676,000

780,000

1,796,000

Less cash disbursements:

Purchases for inventory …..

357,000

518,000

455,000

1,330,000

Selling expenses ……………

79,000

120,000

62,000

261,000

Administrative expenses ….

25,000

32,000

21,000

78,000

Land purchases ……………..

—

16,000

—

16,000

Dividends paid ………………

49,000

—

—

49,000

Total cash disbursements …

510,000

686,000

538,000

1,734,000

Excess (deficiency) of cash

available over

disbursements ………………

(90,000)

(10,000)

242,000

62,000

Financing:

Borrowings …………………..

130,000

50,000

0

180,000

Repayments ………………….

0

0

(180,000)

(180,000)

Interest

($130,000 × 1% × 3 +

$50,000 × 1% × 2) ……..

0

0

(4,900)

(4,900)

Total financing …………………

130,000

50,000

(184,900)

(4,900)

Ending cash balance …………

$ 40,000

$ 40,000

$ 57,100

$ 57,100

Solutions Manual, Chapter 9 39

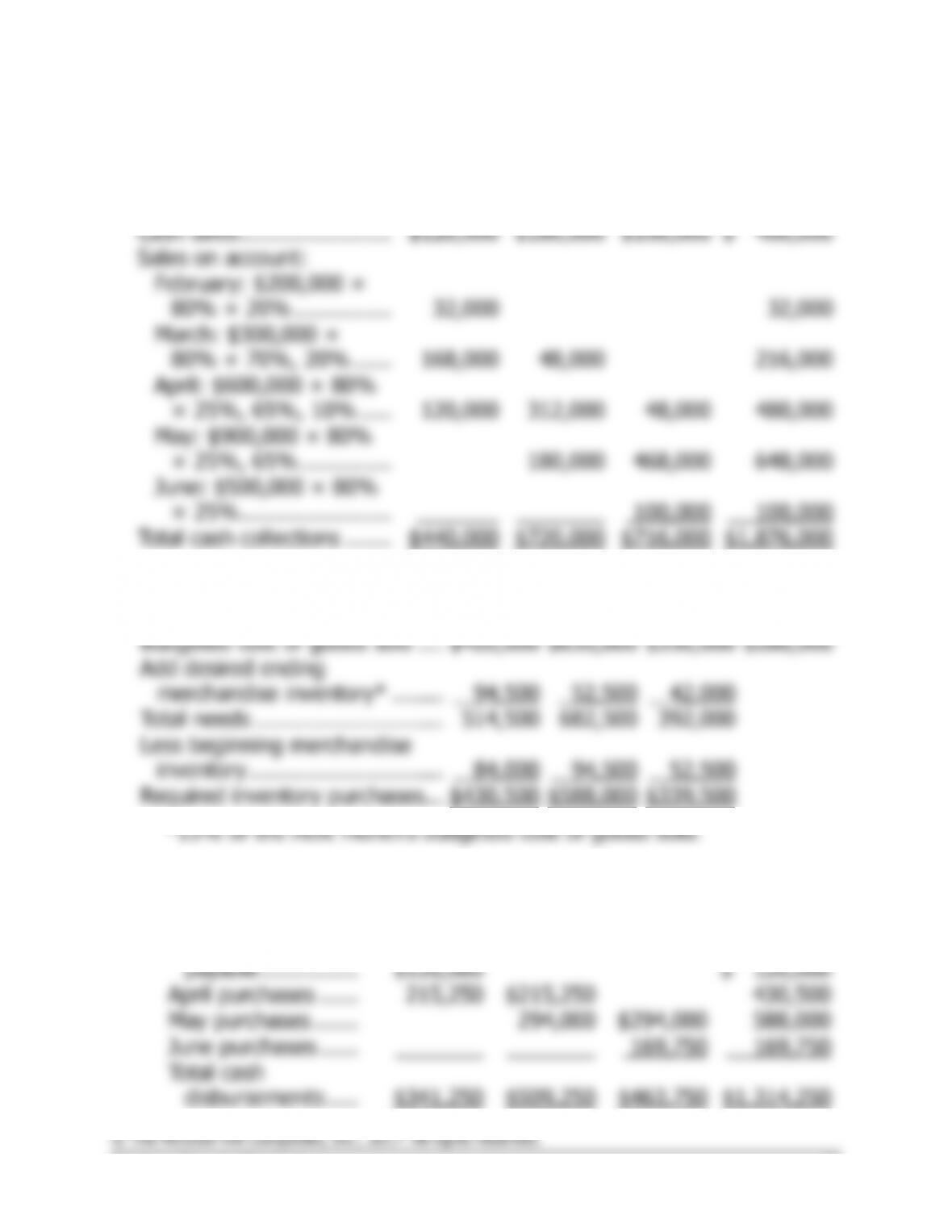

Problem 9-23 (60 minutes)

1. Collections on sales:

April

May

June

Quarter

Cash sales …………………..

$120,000

$180,000

$100,000

$ 400,000

Sales on account:

February: $200,000 ×

80% × 20% ……………

32,000

32,000

March: $300,000 ×

80% × 70%, 20% ……

168,000

48,000

216,000

April: $600,000 × 80%

× 25%, 65%, 10% …..

120,000

312,000

48,000

480,000

May: $900,000 × 80%

× 25%, 65% …………..

180,000

468,000

648,000

June: $500,000 × 80%

× 25% …………………..

100,000

100,000

Total cash collections …….

$440,000

$720,000

$716,000

$1,876,000

2. a. Merchandise purchases budget:

April

May

June

July

Budgeted cost of goods sold ….

$420,000

$630,000

$350,000

$280,000

Add desired ending

merchandise inventory* ……..

94,500

52,500

42,000

Total needs ………………………..

514,500

682,500

392,000

Less beginning merchandise

inventory …………………………

84,000

94,500

52,500

Required inventory purchases…

$430,500

$588,000

$339,500

b. Schedule of expected cash disbursements for merchandise purchases:

April

May

June

Quarter

Beginning accounts

payable ……………

$126,000

$ 126,000

April purchases ……

215,250

$215,250

430,500

May purchases …….

294,000

$294,000

588,000

June purchases ……

169,750

169,750

Total cash

disbursements …..

$341,250

$509,250

$463,750

$1,314,250

40 Managerial Accounting for Managers, 4th Edition

Problem 9-23 (continued)

3.

Garden Sales, Inc.

Cash Budget

For the Quarter Ended June 30

April

May

June

Quarter

Beginning cash balance ……..

$ 52,000

$ 40,750

$ 83,500

$ 52,000

Add collections from

customers …………………….

440,000

720,000

716,000

1,876,000

Total cash available …………..

492,000

760,750

799,500

1,928,000

Less cash disbursements:

Purchases for inventory …..

341,250

509,250

463,750

1,314,250

Selling expenses ……………

79,000

120,000

62,000

261,000

Administrative expenses ….

25,000

32,000

21,000

78,000

Land purchases ……………..

—

16,000

—

16,000

Dividends paid ………………

49,000

—

—

49,000

Total cash disbursements …

494,250

677,250

546,750

1,718,250

Excess (deficiency) of cash

available over

disbursements ………………

(2,250)

83,500

252,750

209,750

Financing:

Borrowings …………………..

43,000

0

0

43,000

Repayments ………………….

0

0

(43,000)

(43,000)

Interest

($43,000 × 1% × 3) …….

0

0

(1,290)

(1,290)

Total financing …………………

43,000

0

(44,290)

(1,290)

Ending cash balance …………

$ 40,750

$ 83,500

$ 208,460

$ 208,460

4. Collecting accounts receivable sooner and reducing inventory levels