Problem 8-24 (continued)

4. The formula for the internal rate of return is:

Investment required

Factor of the internal=

rate of return Annual net cash inflow

$94,500

= = 4.500

$21,000

Looking in Exhibit 8B-2, and reading along the 12-period line, a factor of

42 Managerial Accounting for Managers, 4th Edition

Problem 8-25 (30 minutes)

1. The present value of each alternative’s cash flows is computed as

follows:

Purchase Alternative:

Now

1

2

3

Purchase of cars ……….

$(170,000)

Annual servicing costs ..

$(3,000)

$(3,000)

$(3,000)

Repairs……………………

(1,500)

(4,000)

(6,000)

Resale value of cars …..

________

______

______

85,000

Total cash flows (a) …..

$(170,000)

$(4,500)

$(7,000)

$76,000

Discount factor (b) …….

1.000

0.847

0.718

0.609

Present value (a)×(b) ..

$(170,000)

$(3,812)

$(5,026)

$46,284

Present value ……………

$(132,554)

Lease Alternative:

Now

1

2

3

Security deposit …………….

$(10,000)

Annual lease payments .….

$(55,000)

$(55,000)

$(55,000)

Refund of deposit ………….

_______

_______

_______

10,000

Total cash flows (a) ……….

$(10,000)

$(55,000)

$(55,000)

$(45,000)

Discount factor (b) ……..….

1.000

0.847

0.718

0.609

Present value (a)×(b) …….

$(10,000)

$(46,585)

$(39,490)

$(27,405)

Net present value ………….

$(123,480)

2. The company should lease the cars because this alternative has the

lowest present value of total costs.

Problem 8-26 (30 minutes)

1. The annual incremental net operating income can be determined as

follows:

Ticket revenue (50,000 × $3.60) …………….

$180,000

Selling and administrative expenses:

Salaries …………………………………………..

$85,000

Insurance ………………………………………..

4,200

Utilities ……………………………………………

13,000

Depreciation* …………………………………..

27,500

Maintenance …………………………………….

9,800

Total selling and administrative expenses ….

139,500

Net operating income …………………………..

$ 40,500

*$330,000 ÷ 12 years = $27,500 per year.

2. The simple rate of return is:

Annual incremental net operating income

Simple rate=

of return Initial investment (net of salvage from old equipment)

$40,500 $40,500

= = = 15%

$330,000 – $60,000 $270,000

Yes, the water slide would be constructed. Its return is greater than the

3. The payback period is:

Investment required (net of salvage from old equipment)

Payback =

period Annual net cash inflow

$330,000 – $60,000 $270,000

= = = 3.97 years (rounded)

$68,000* $68,000*

*Net operating income + Depreciation = Annual net cash flow

$40,500 + $27,500 = $68,000.

Yes, the water slide would be constructed. The payback period is within

the 5 year payback required by Mr. Sharkey.

Problem 8-27 (30 minutes)

1. Average weekly use of the auto wash and the vacuum will be:

$1,350

Auto wash: = 675 uses

$2.00

Vacuum: 675 × 60% = 405 uses

The expected annual net cash flow from operations would be:

Auto wash cash receipts ($1,350 × 52) ………..

$70,200

Vacuum cash receipts (405 × $1.00 × 52) ……

21,060

Total cash receipts ………………………………..

91,260

Less cash disbursements:

Water (675 × $0.20 × 52) ………………………

$ 7,020

Electricity (405 × $0.10 × 52) …………………

2,106

Rent ($1,700 × 12) ……………………………….

20,400

Cleaning ($450 × 12) …………………………….

5,400

Insurance ($75 × 12) …………………………….

900

Maintenance ($500 × 12) ……………………….

6,000

Total cash disbursements ………………………….

41,826

Annual net cash flow from operations ………….

$49,434

Solutions Manual, Chapter 8 45

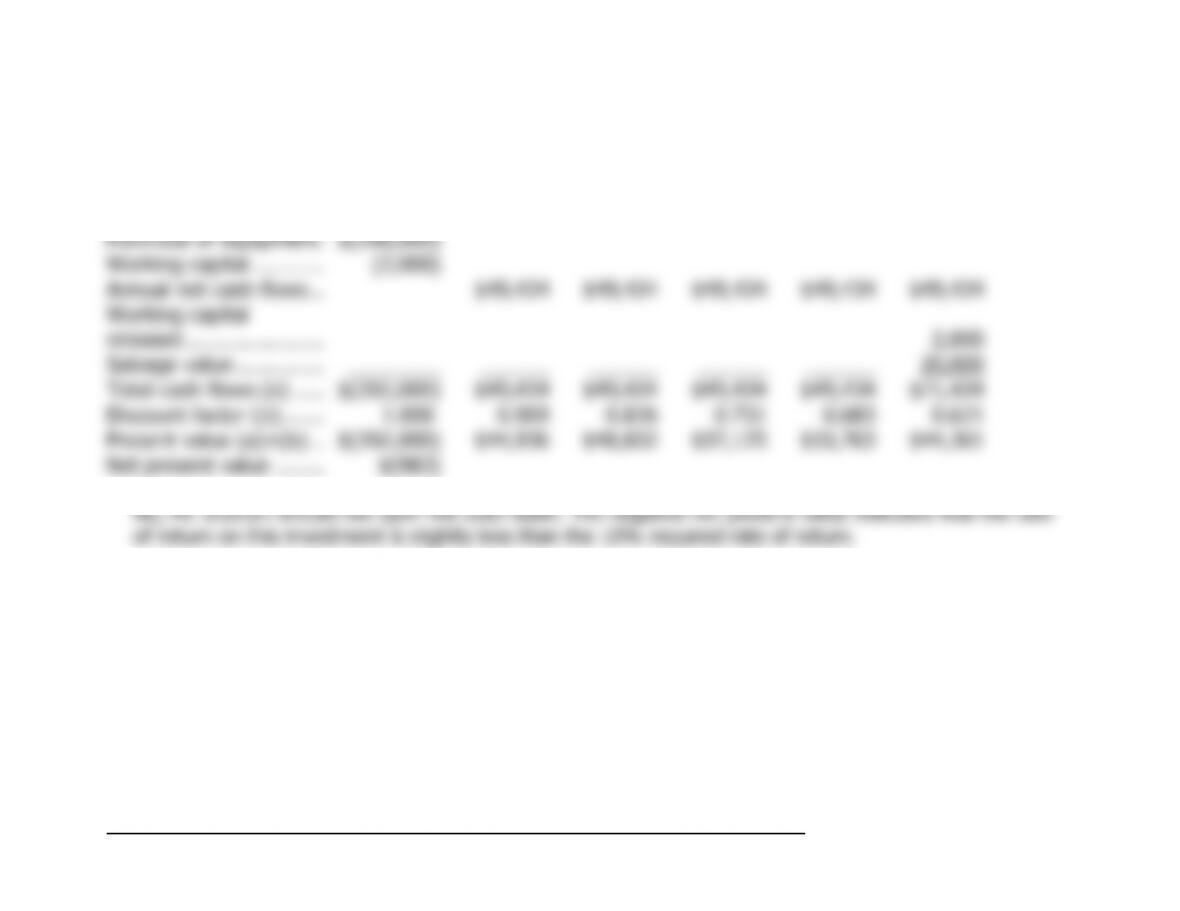

Problem 8-27 (continued)

2. The net present value is computed as follows:

Now

1

2

3

4

5

Purchase of equipment .

$(200,000)

Working capital …………

(2,000)

Annual net cash flows ..

$49,434

$49,434

$49,434

$49,434

$49,434

Working capital

released ………………….

2,000

Salvage value …………..

________

______

______

______

______

20,000

Total cash flows (a) …..

$(202,000)

$49,434

$49,434

$49,434

$49,434

$71,434

Discount factor (b) …….

1.000

0.909

0.826

0.751

0.683

0.621

Present value (a)×(b) ..

$(202,000)

$44,936

$40,832

$37,125

$33,763

$44,361

Net present value ……..

$(983)

46 Managerial Accounting for Managers, 4th Edition

Problem 8-28 (20 minutes)

Keep the old truck:

Now

1

2

3

4

5

Overhaul needed now ..

$(7,000)

Annual operating costs .

(10,000)

(10,000)

(10,000)

(10,000)

(10,000)

Salvage value (old) ……

______

_______

_______

_______

_______

1,000

Total cash flows (a) …..

$(7,000)

$(10,000)

$(10,000)

$(10,000)

$(10,000)

$(9,000)

Discount factor (b) …….

1.000

0.862

0.743

0.641

0.552

0.476

Present value (a)×(b) ..

$(7,000)

$(8,620)

$(7,430)

$(6,410)

$(5,520)

$(4,284)

Present value ……………

$(39,264)

Purchase the new truck:

Now

1

2

3

4

5

Purchase new truck ……

$(30,000)

Salvage value (old) ……

9,000

Annual operating costs .

(6,500)

(6,500)

(6,500)

(6,500)

(6,500)

Salvage value (new) ….

_______

______

______

______

______

4,000

Total cash flows (a) …..

$(21,000)

$(6,500)

$(6,500)

$(6,500)

$(6,500)

$(2,500)

Discount factor (b) …….

1.000

0.862

0.743

0.641

0.552

0.476

Present value (a)×(b) ..

$(21,000)

$(5,603)

$(4,830)

$(4,167)

$(3,588)

$(1,190)

Present value ……………

$(40,378)

that alternative.

Solutions Manual, Chapter 8 47

Problem 8-29 (45 minutes)

1. A net present value computation for each investment follows:

Common stock:

Now

1

2

3

Purchase of the stock …

$(95,000)

Sales of the stock ……..

________

______

______

160,000

Total cash flows (a) …..

$(95,000)

$0

$0

$160,000

Discount factor (b) …….

1.000

0.862

0.743

0.641

Present value (a)×(b) ..

$(95,000)

$0

$0

$102,560

Net present value ……..

$7,560

Preferred stock:

Now

1

2

3

Purchase of the stock …

$(30,000)

Annual cash dividend …

$1,800

$1,800

$1,800

Sales of the stock ……..

________

______

______

27,000

Total cash flows (a) …..

$(30,000)

$1,800

$1,800

$28,800

Discount factor (b) …….

1.000

0.862

0.743

0.641

Present value (a)×(b) ..

$(30,000)

$1,552

$1,337

$18,461

Net present value ……..

$(8,650)

Bonds:

Now

1

2

3

Purchase of the bonds..

$(50,000)

Annual interest income .

$6,000

$6,000

$6,000

Sales of the bonds …….

________

______

______

52,700

Total cash flows (a) …..

$(50,000)

$6,000

$6,000

$58,700

Discount factor (b) …….

1.000

0.862

0.743

0.641

Present value (a)×(b) ..

$(50,000)

$5,172

$4,458

$37,627

Net present value ……..

$(2,743)

preferred stock or the bonds.

48 Managerial Accounting for Managers, 4th Edition

Problem 8-29 (continued)

2. Considering all three investments together, Linda did not earn a 16%

rate of return. The computation is:

Net

Present

Value

Common stock …………………….

$ 7,560

Preferred stock …………………….

(8,650)

Bonds …………………………..……

(2,743)

Overall net present value ……….

$(3,833)

The defect in the broker’s computation is that it does not consider the

time value of money and therefore has overstated the rate of return

earned.

3.

Investment required

Factor of the internal =

rate of return Annual net cash inflow

Substituting the $239,700 investment and the factor for 14% for 12

periods into this formula, we get:

=

$239,700 5.660

Annual cash inflow

Therefore, the required annual net cash inflow is: $239,700 ÷ 5.660 =

$42,350.

Solutions Manual, Chapter 8 49

Problem 8-30 (60 minutes)

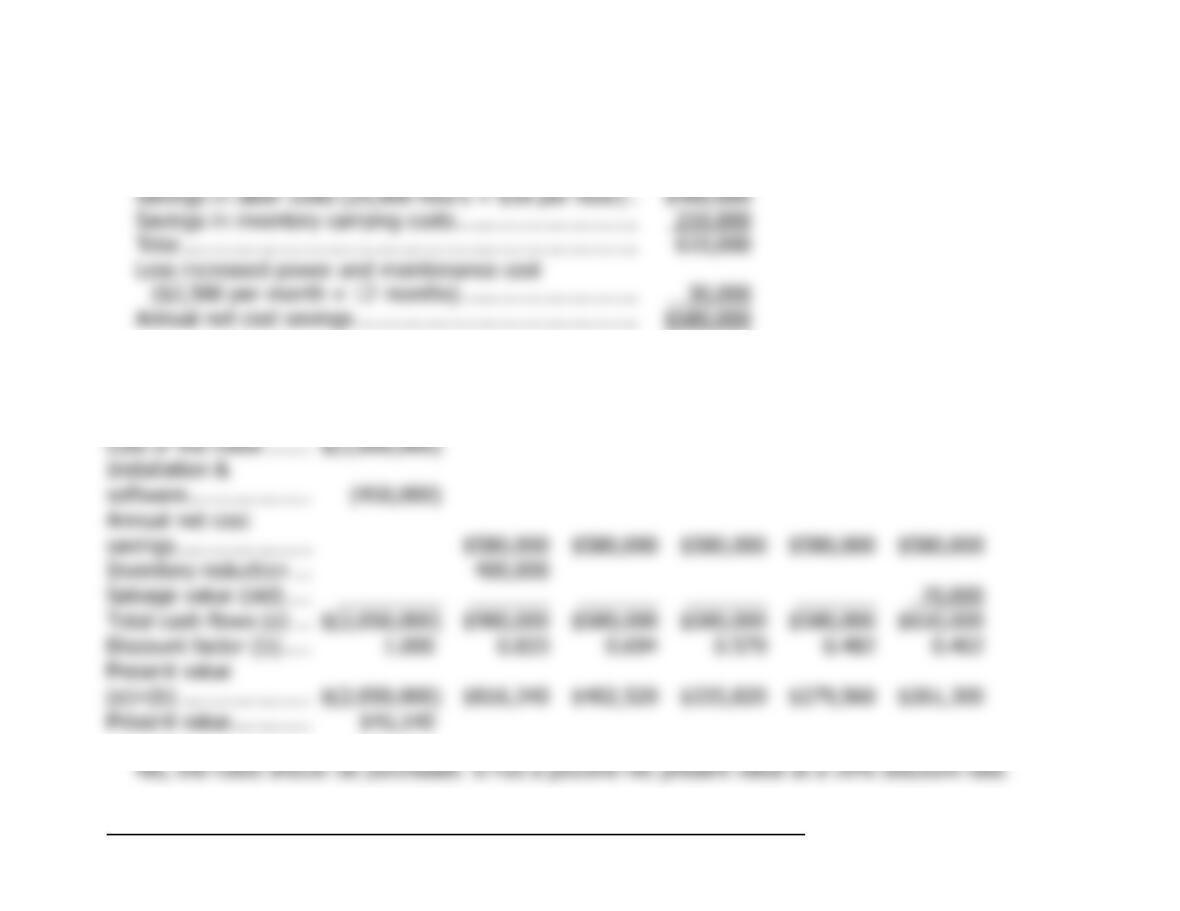

1. Computation of the annual net cost savings:

Savings in labor costs (25,000 hours × $16 per hour) .

$400,000

Savings in inventory carrying costs ………………………..

210,000

Total ……………………………………………………………….

610,000

Less increased power and maintenance cost

($2,500 per month × 12 months) ……………………….

30,000

Annual net cost savings ………………………………………

$580,000

2. The net present value is computed as follows:

Now

1

2

3

4

5

Cost of the robot …….

$(1,600,000)

Installation &

software ………………..

(450,000)

Annual net cost

savings………………….

$580,000

$580,000

$580,000

$580,000

$580,000

Inventory reduction …

400,000

Salvage value (old) ….

_________

_______

_______

_______

_______

70,000

Total cash flows (a) …

$(2,050,000)

$980,000

$580,000

$580,000

$580,000

$650,000

Discount factor (b) …..

1.000

0.833

0.694

0.579

0.482

0.402

Present value

(a)×(b) …………………

$(2,050,000)

$816,340

$402,520

$335,820

$279,560

$261,300

Present value ………….

$45,540

50 Managerial Accounting for Managers, 4th Edition

Problem 8-30 (continued)

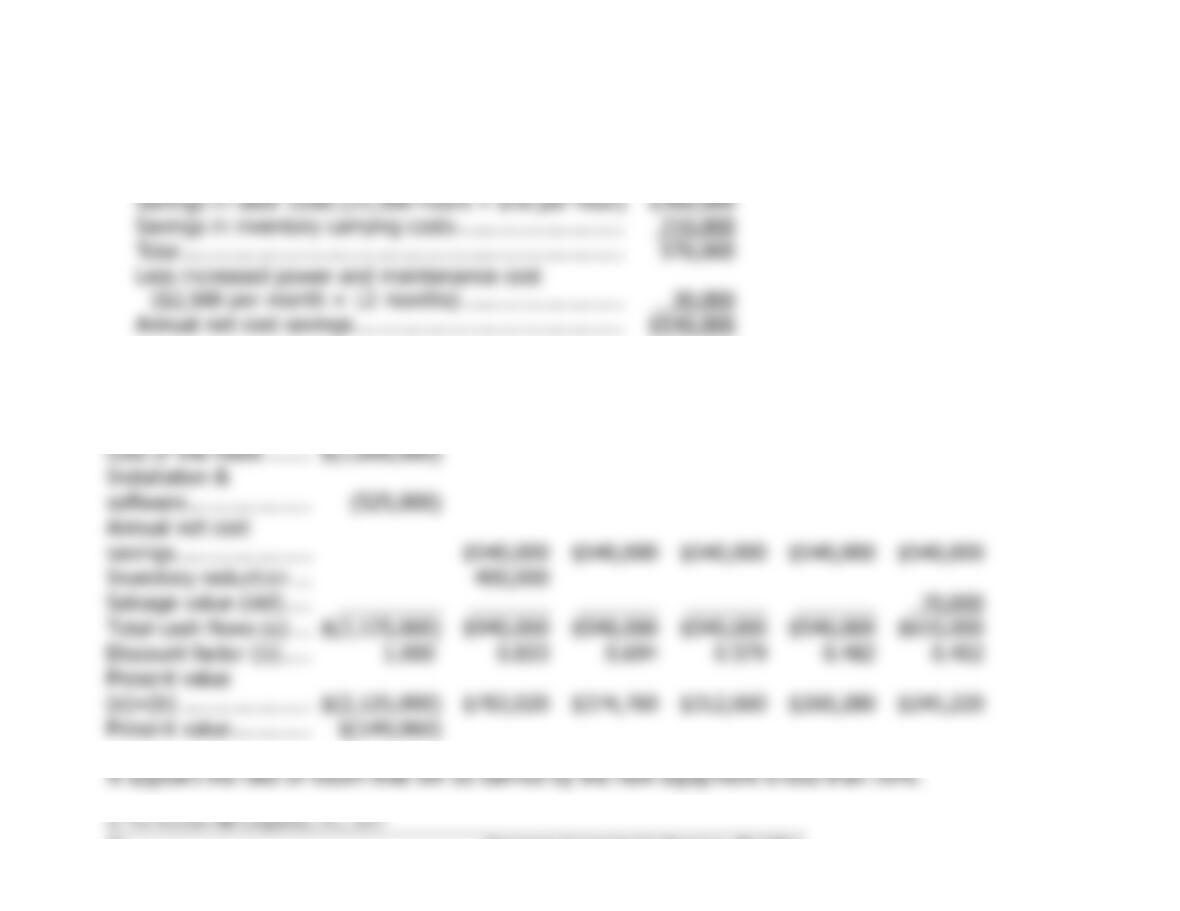

3. Recomputation of the annual net cost savings:

Savings in labor costs (22,500 hours × $16 per hour)

$360,000

Savings in inventory carrying costs ………………………

210,000

Total ……………………………………………………………..

570,000

Less increased power and maintenance cost

($2,500 per month × 12 months) ……………………..

30,000

Annual net cost savings …………………………………….

$540,000

The revised present value computations are follows:

Now

1

2

3

4

5

Cost of the robot ……...

$(1,600,000)

Installation &

software ………………….

(525,000)

Annual net cost

savings…………………...

$540,000

$540,000

$540,000

$540,000

$540,000

Inventory reduction …..

400,000

Salvage value (old) …...

_________

_______

_______

_______

_______

70,000

Total cash flows (a) …..

$(2,125,000)

$940,000

$540,000

$540,000

$540,000

$610,000

Discount factor (b) …….

1.000

0.833

0.694

0.579

0.482

0.402

Present value

(a)×(b) …………………..

$(2,125,000)

$783,020

$374,760

$312,660

$260,280

$245,220

Present value …………...

$(149,060)