Solutions Manual, Chapter 8 31

Problem 8-19 (continued)

3. The formula for the payback period is:

Investment required

Payback period = Annual net cash inflow

$270,000

= = 4.5 years

$60,000*

*Net operating income + Depreciation = Annual net cash inflow

$43,200 + $16,800 = $60,000

According to the payback computation, the franchise would not be

32 Managerial Accounting for Managers, 4th Edition

Problem 8-20 (30 minutes)

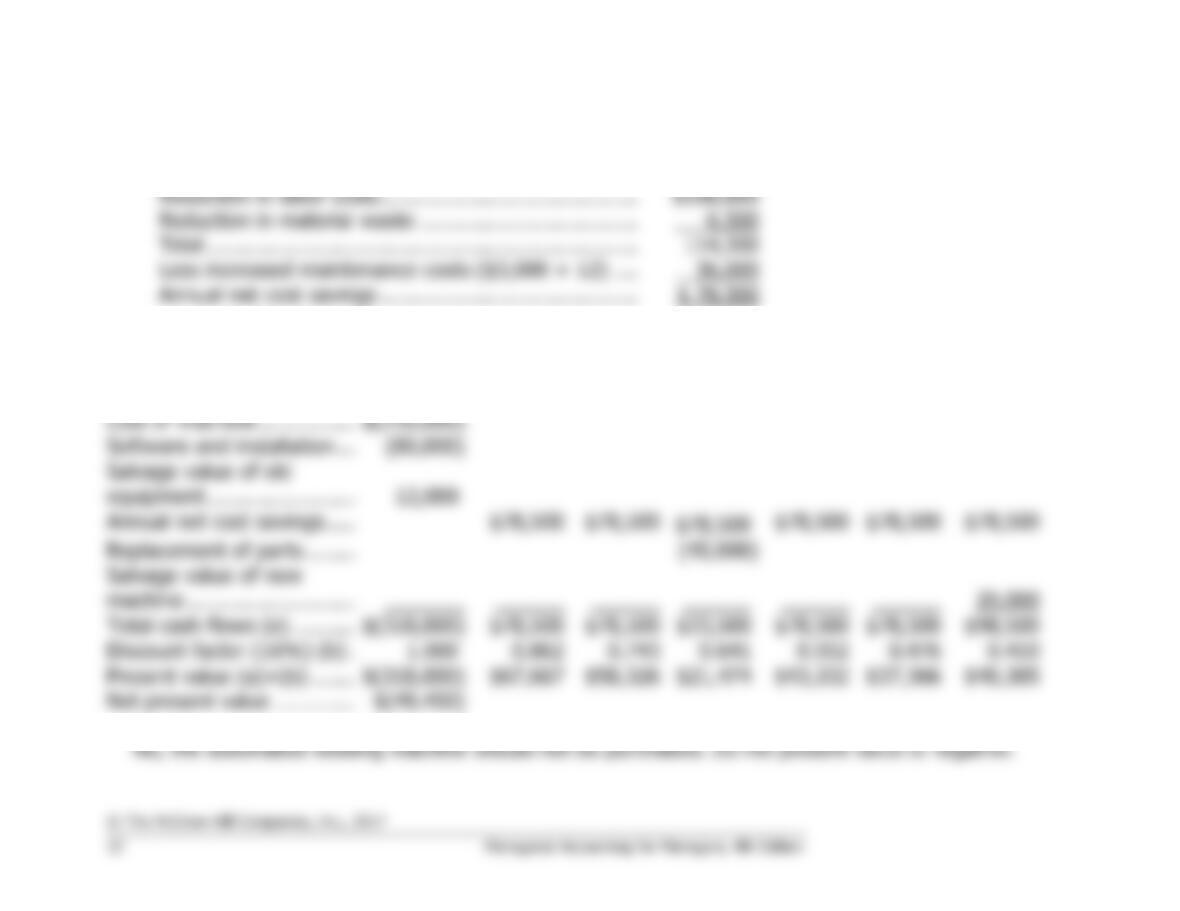

1. The annual net cost savings would be:

Reduction in labor costs …………………………………..

$108,000

Reduction in material waste ……………………………..

6,500

Total ……………………………………………………………

114,500

Less increased maintenance costs ($3,000 × 12) ….

36,000

Annual net cost savings …………………………………..

$ 78,500

2. Using this cost savings figure, and other data from the text, the net present value analysis would be:

Now

1

2

3

4

5

6

Cost of machine …………….

$(250,000)

Software and installation …

(80,000)

Salvage value of old

equipment ……………………

12,000

Annual net cost savings …..

$78,500

$78,500

$78,500

$78,500

$78,500

$78,500

Replacement of parts ……..

(45,000)

Salvage value of new

machine ………………………

_______

______

______

______

______

______

20,000

Total cash flows (a) ……….

$(318,000)

$78,500

$78,500

$33,500

$78,500

$78,500

$98,500

Discount factor (16%) (b) .

1.000

0.862

0.743

0.641

0.552

0.476

0.410

Present value (a)×(b) …….

$(318,000)

$67,667

$58,326

$21,474

$43,332

$37,366

$40,385

Net present value ………….

$(49,450)

Problem 8-20 (continued)

34 Managerial Accounting for Managers, 4th Edition

Problem 8-21 (30 minutes)

1. The formula for the project profitability index is:

Net present value of the project

Project profitability index = Investment required by the project

The indexes for the projects under consideration would be:

Project 1:

$66,140 ÷ $270,000 = 0.24

Project 2:

$72,970 ÷ $450,000 = 0.16

Project 3:

$73,400 ÷ $360,000 = 0.20

Project 4:

$87,270 ÷ $480,000 = 0.18

2. a., b., and c.

Net Present

Value

Project

Profitability

Index

Internal Rate

of Return

First preference ……..

4

1

2

Second preference ….

3

3

1

Third preference …….

2

4

4

Fourth preference …..

1

2

3

Solutions Manual, Chapter 8 35

Problem 8-21 (continued)

3. Which ranking is best will depend on Revco Products’ opportunities for

reinvesting funds as they are released from the project. The internal

The project profitability index approach assumes that funds released

from a project are reinvested in other projects at a rate of return equal

The net present value is inferior to the project profitability index as a

ranking device because it looks only at the total amount of net present

36 Managerial Accounting for Managers, 4th Edition

Problem 8-22 (20 minutes)

1. The annual net cash inflows would be:

Reduction in annual operating costs:

Operating costs, present hand method …..

$30,000

Operating costs, new machine ……………..

7,000

Annual savings in operating costs …………

23,000

Increased annual contribution margin:

6,000 boxes × $1.50 per box ……………….

9,000

Total annual net cash inflows …………………

$32,000

2. The net present value is computed as follows:

Now

1

2

3

4

5

Purchase of machine ……..

$(120,000)

Annual net cash inflows ….

$32,000

$32,000

$32,000

$32,000

$32,000

Replacement parts ………..

(9,000)

Salvage value of machine .

________

______

______

_______

______

7,500

Total cash flows (a) ………

$(120,000)

$32,000

$32,000

$23,000

$32,000

$39,500

Discount factor (20%) (b)

1.000

0.833

0.694

0.579

0.482

0.402

Present value (a)×(b) ……

$(120,000)

$26,656

$22,208

$13,317

$15,424

$15,879

Net present value …………

(26,516)

Solutions Manual, Chapter 8 37

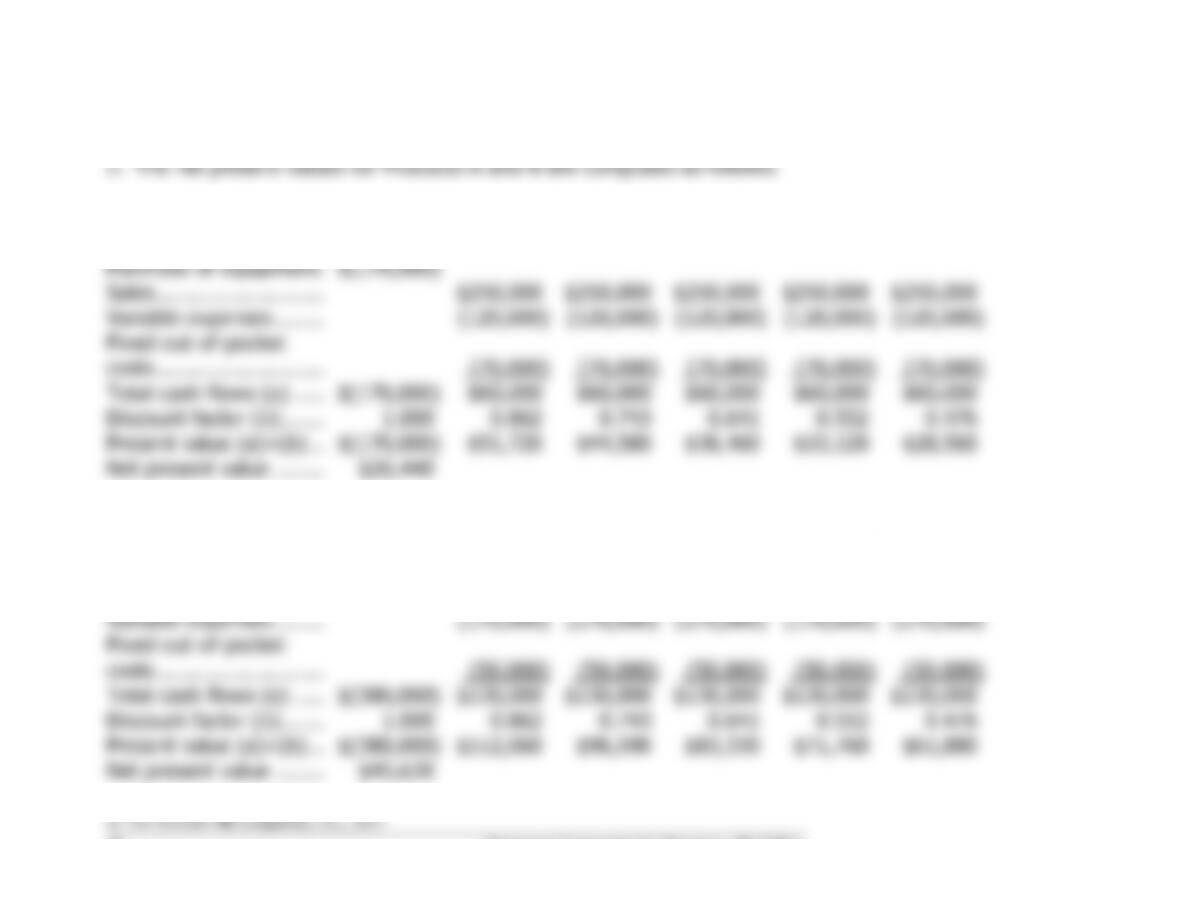

Problem 8-23 (45 minutes)

follows:

Product A

Product B

Sales revenues ……………………………….

$250,000

$350,000

Variable expenses …………………………..

(120,000)

(170,000)

Fixed out-of-pocket operating costs ……

(70,000)

(50,000)

Annual net cash inflows ……………………

$ 60,000

$130,000

follows:

Product A

Product B

Investment required (a) ……………………

$170,000

$380,000

Annual net cash inflow (b) ………………..

$60,000

$130,000

Payback period (a) ÷ (b) ………………….

2.83 years

2.92 years

38 Managerial Accounting for Managers, 4th Edition

Problem 8-23 (continued)

Product A:

Now

1

2

3

4

5

Purchase of equipment ..….

$(170,000)

Sales ……………………….….

$250,000

$250,000

$250,000

$250,000

$250,000

Variable expenses ………….

(120,000)

(120,000)

(120,000)

(120,000)

(120,000)

Fixed out-of-pocket

costs ……………………….….

(70,000)

(70,000)

(70,000)

(70,000)

(70,000)

Total cash flows (a) ……….

$(170,000)

$60,000

$60,000

$60,000

$60,000

$60,000

Discount factor (b) ……..….

1.000

0.862

0.743

0.641

0.552

0.476

Present value (a)×(b) …….

$(170,000)

$51,720

$44,580

$38,460

$33,120

$28,560

Net present value ………….

$26,440

Product B:

Now

1

2

3

4

5

Purchase of equipment ..….

$(380,000)

Sales ……………………….….

$350,000

$350,000

$350,000

$350,000

$350,000

Variable expenses ………….

(170,000)

(170,000)

(170,000)

(170,000)

(170,000)

Fixed out-of-pocket

costs ……………………….….

(50,000)

(50,000)

(50,000)

(50,000)

(50,000)

Total cash flows (a) ……….

$(380,000)

$130,000

$130,000

$130,000

$130,000

$130,000

Discount factor (b) ……..….

1.000

0.862

0.743

0.641

0.552

0.476

Present value (a)×(b) …….

$(380,000)

$112,060

$96,590

$83,330

$71,760

$61,880

Net present value ………….

$45,620

Solutions Manual, Chapter 8 39

Problem 8-23 (continued)

3. The internal rate of return for each product is calculated as follows:

Product A

Product B

Investment required (a) …………………………..

$170,000

$380,000

Annual net cash inflow (b) ………………………..

$60,000

$130,000

Factor of the internal rate of return (a) ÷ (b) ..

2.833

2.923

Looking in Exhibit 8B-2 and scanning along the 5-period line, a factor of

4. The project profitability index for each product is computed as follows:

Product A

Product B

Net present value (a) ………………………………

$26,440

$45,620

Investment required (b) …………………………..

$170,000

$380,000

Project profitability index (a) ÷ (b) ……………..

0.16

0.12

5. The simple rate of return for each product is computed as follows:

Product A

Product B

Annual net cash inflow …………………………….

$60,000

$130,000

Depreciation expense ………………………………

34,000

76,000

Annual incremental net operating income …….

$26,000

$54,000

Product A

Product B

Annual incremental net operating income (a)..

$26,000

$54,000

Initial investment (b) ……………………………….

$170,000

$380,000

Simple rate of return (a) ÷ (b) …………………..

15.3%

14.2%

6. The net present value calculations suggest that Product B is preferable

to Product A. However, the project profitability index reveals that

Problem 8-24 (45 minutes)

1.

Present cost of transient workers ……………………..

$40,000

Less out–of-pocket costs to operate the cherry picker:

Cost of an operator and assistant …………………..

$14,000

Insurance ………………………………………………….

200

Fuel …………………………………………………………

1,800

Maintenance contract …………………………………..

3,000

19,000

Annual savings in cash operating costs ………………

$21,000

2. The first step is to determine the annual incremental net operating

income:

Annual savings in cash operating costs ………….

$21,000

Less annual depreciation ($90,000 ÷ 12 years) .

7,500

Annual incremental net operating income ………

$13,500

Annual incremental net operating income

Simple rate of return = Initial investment

$13,500

= = 14.3% (rounded)

$94,500

3. The formula for the payback period is:

Investment required

Payback period = Annual net cash inflow

$94,500

= = 4.5 years

$21,000*

*

In this case, the cash inflow is measured by the annual savings

in cash operating costs.