Solutions Manual, Chapter 6 41

Problem 6-20 (continued)

5. Gallatin Carpet Cleaning appears to be losing money on the Flying N

Ranch job. However, caution is advised. Some of the costs may not be

simple report in part (4) above.

Nevertheless, there is a point at which travel costs eat up all of the

6. The company should consider charging a fee for travel to outlying

customers based on the distance traveled and a flat fee per job. At

present, close-in customers are in essence subsidizing service to

outlying customers and large-volume customers are subsidizing service

may choose to clean their carpets more frequently if the price were

more attractive.)

42 Managerial Accounting for Managers, 4th Edition

Appendix 6A

ABC Action Analysis

Exercise 6A-1 (20 minutes)

Sales (100 clubs × $50 per club) ……………………..

$5,000.00

Green costs:

Direct materials (100 clubs × $29.50 per club) ….

$2,950.00

2,950.00

Green margin ………………………………………………

2,050.00

Yellow costs:

Direct labor (100 clubs × 0.3 hour per club ×

$20.50 per hour) ………………………………………

615.00

Indirect labor ……………………………………………..

95.90

Marketing expenses …………………………………….

540.70

1,251.60

Yellow margin ………………………………………………

798.40

Red costs:

Factory equipment depreciation ……………………..

103.70

Factory administration ………………………………….

259.00

Selling and administrative wages and salaries ……

429.00

Selling and administrative depreciation …………….

30.00

821.70

Red margin …………………………………………………

$ (23.30)

Sales (100 clubs × $50 per club) ……………………..

$5,000.00

Costs:

Direct materials ………………………………………….

$2,950.00

Direct labor ……………………………………………….

615.00

Supporting direct labor ……………………………….

285.40

Batch processing ……………………………………….

55.10

Order processing ……………………………………….

114.80

Customer service ……………………………………….

1,003.00

5,023.30

Customer margin ………………………………………….

$ (23.30)

Solutions Manual, Appendix 6A 43

Exercise 6A-2 (30 minutes)

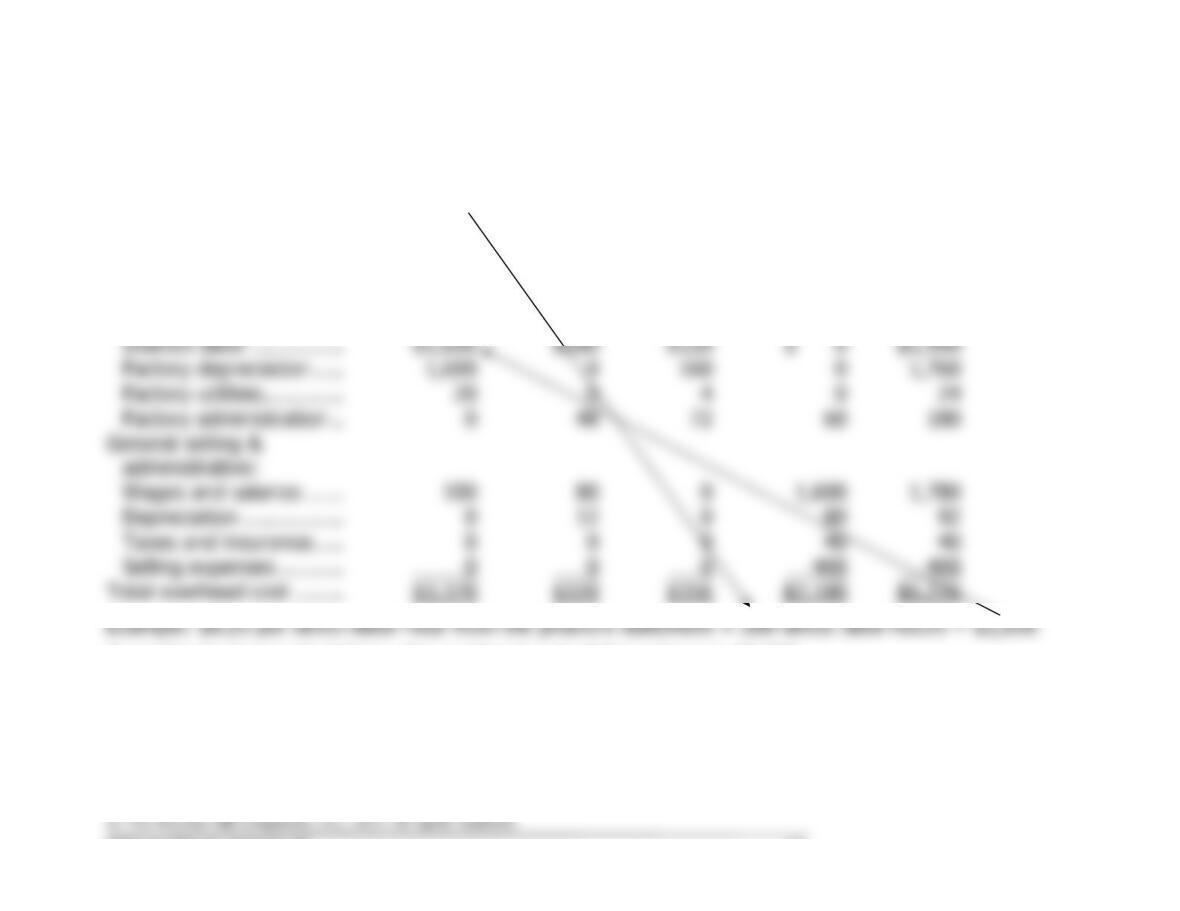

1.

Order Size

Customer

Orders

Product

Testing

Selling

Total

Activity level ……………….

200

1

4

2

direct labor-

hours

customer

order

product

testing

hours

sales calls

Manufacturing overhead:

Indirect labor ……………

$1,650

$180

$120

$ 0

$1,950

Factory depreciation …..

1,600

0

160

0

1,760

Factory utilities ………….

20

0

4

0

24

Factory administration ..

0

48

72

60

180

General selling &

administrative:

Wages and salaries ……

100

80

0

1,600

1,780

Depreciation …………….

0

12

0

80

92

Taxes and insurance …..

0

0

0

40

40

Selling expenses ………..

0

0

0

400

400

Total overhead cost ……..

$3,370

$320

$356

$2,180

$6,226

According to these calculations, the overhead cost of the order was $6,226.

44 Managerial Accounting for Managers, 4th Edition

Exercise 6A-2 (continued)

2. The table prepared in part (1) above allows two different perspectives

on the overhead cost of the order. The column totals that appear in the

last row of the table tell us the cost of the order in terms of the

activities it required. The row totals that appear in the last column of the

table tell us how much the order cost in terms of the overhead accounts

in the underlying accounting system. Another way of saying this is that

the column totals tell us what the costs were incurred

for

. The row

totals tell us what the costs were incurred

on

. For example, you may

spend money

on

a chocolate bar in order to satisfy your craving

for

chocolate. Both perspectives are important. To control costs, it is

necessary to know both what the costs were incurred for and what

actual costs would have to be adjusted (i.e., what the costs were

incurred on).

The two different perspectives can be explicitly shown as follows:

What the overhead costs were incurred

on

:

Manufacturing overhead:

Indirect labor …………………………..

$1,950

Factory depreciation ………………….

1,760

Factory utilities …………………………

24

Factory administration ……………….

180

General selling & administrative:

Wages and salaries ……………………

1,780

Depreciation …………………………….

92

Taxes and insurance ………………….

40

Selling expenses ……………………….

400

Total overhead cost ……………………..

$6,226

What the overhead costs were incurred

for

:

Order size ………………………………….

$3,370

Customer orders …………………………

320

Product testing …………………………..

356

Selling ………………………………………

2,180

Total overhead cost ……………………..

$6,226

Solutions Manual, Appendix 6A 45

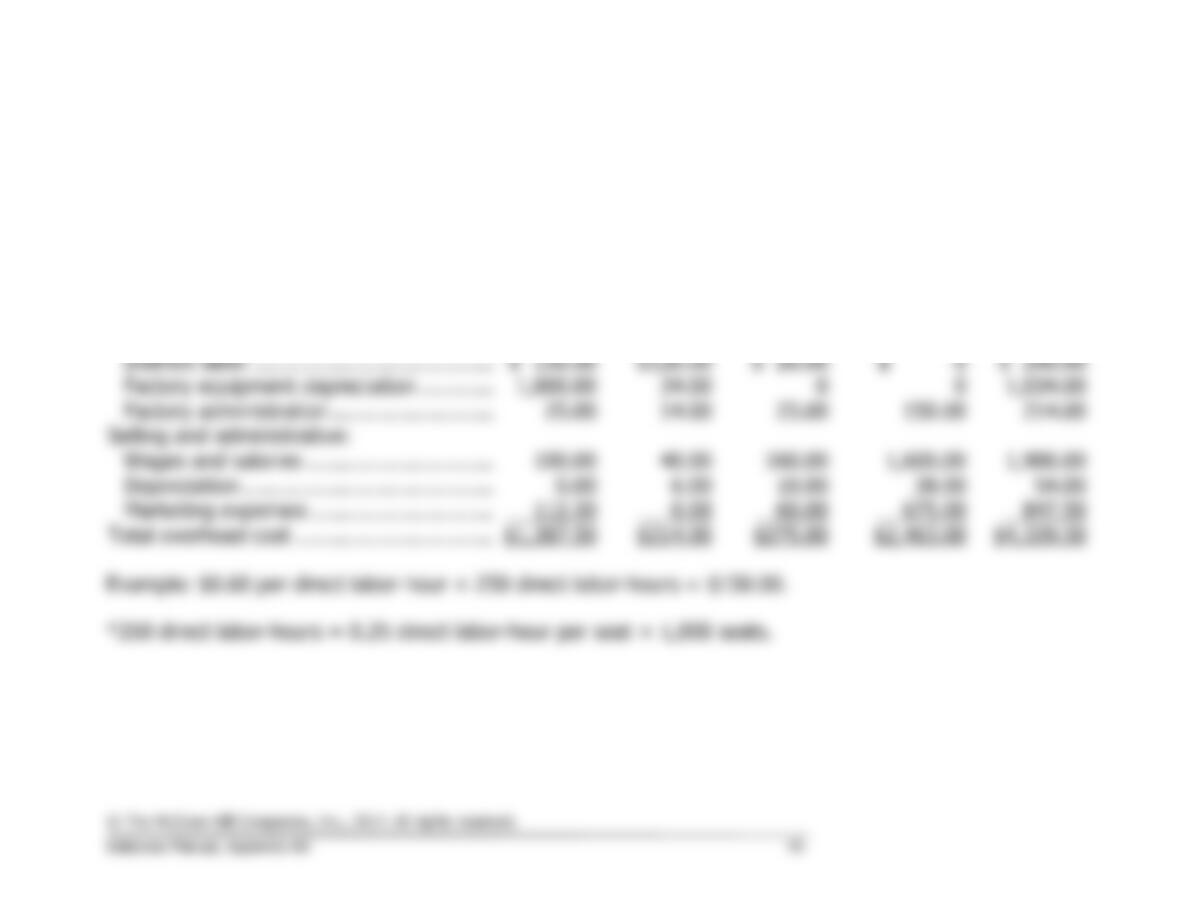

Exercise 6A-3 (30 minutes)

Supporting

Direct

Labor

Batch

Processing

Order

Processing

Customer

Service

Total

Total activity for the order …………………..

250

2

1

1

Direct labor-

hours*

Batches

Order

Customer

Manufacturing overhead:

Indirect labor …………………………………

$ 150.00

$120.00

$ 20.00

$ 0

$ 290.00

Factory equipment depreciation …………

1,000.00

34.00

0

0

1,034.00

Factory administration ……………………..

25.00

14.00

25.00

150.00

214.00

Selling and administrative:

Wages and salaries …………………………

100.00

40.00

160.00

1,600.00

1,900.00

Depreciation ………………………………….

0.00

6.00

10.00

38.00

54.00

Marketing expenses ………………………..

112.50

0.00

60.00

675.00

847.50

Total overhead cost …………………………..

$1,387.50

$214.00

$275.00

$2,463.00

$4,339.50

Example: $0.60 per direct labor-hour × 250 direct labor-hours = $150.00.

*250 direct labor-hours = 0.25 direct labor-hour per seat × 1,000 seats.

46 Managerial Accounting for Managers, 4th Edition

Exercise 6A-3 (continued)

adjustment codes:

Sales (1,000 units × $20 per unit) ………………….

$20,000.00

Green costs:

Direct materials (1,000 units × $8.50 per unit) .

$8,500.00

8,500.00

Green margin …………………………………………….

11,500.00

Yellow costs:

Direct labor (1,000 units × $6.00 per unit) …….

6,000.00

Indirect labor …………………………………………..

290.00

Marketing expenses …………………………………..

847.50

7,137.50

Yellow margin …………………………………………….

4,362.50

Red costs:

Factory equipment depreciation …………………..

1,034.00

Factory administration ……………………………….

214.00

Selling and administrative wages and salaries …

1,900.00

Selling and administrative depreciation ………….

54.00

3,202.00

Red margin ……………………………………………….

$ 1,160.50

Solutions Manual, Appendix 6A 47

Exercise 6A-4 (60 minutes)

1. First-stage allocations of overhead costs to the activity cost pools:

Distribution of Resource Consumption

Across Activity Cost Pools

Direct Labor

Support

Order

Processing

Customer

Support

Other

Totals

Wages and salaries …….

40%

30%

20%

10%

100%

Other overhead costs …

30%

10%

20%

40%

100%

Direct Labor

Support

Order

Processing

Customer

Support

Other

Totals

Wages and salaries …….

$120,000

$ 90,000

$60,000

$30,000

$300,000

Other overhead costs …

30,000

10,000

20,000

40,000

100,000

Total cost …………………

$150,000

$100,000

$80,000

$70,000

$400,000

Example: 40% of $300,000 is $120,000.