Solutions Manual, Chapter 6 21

Exercise 6-13 (30 minutes)

1. Activity rates are computed as follows:

Activity Cost Pool

(a)

Estimated

Overhead

Cost

(b)

Expected

Activity

(a) ÷ (b)

Activity

Rate

Machine setups ……

$72,000

400

setups

$180

per setup

Special processing ..

$200,000

5,000

MHs

$40

per MH

2. Overhead is assigned to the two products as follows:

Hubs:

Activity Cost Pool

(a)

Activity Rate

(b)

Activity

(a) × (b)

ABC Cost

Machine setups …………………

$180

per setup

100

setups

$ 18,000

Special processing ……………..

$40

per MH

5,000

MHs

200,000

Total ……………………………….

$218,000

Sprockets:

Activity Cost Pool

(a)

Activity Rate

(b)

Activity

(a) × (b)

ABC Cost

Machine setups …………………

$180

per setup

300

setups

$54,000

Special processing ……………..

$40

per MH

0

MHs

0

Total ……………………………….

$54,000

22 Managerial Accounting for Managers, 4th Edition

Exercise 6-13 (continued)

Hubs

Sprockets

Direct materials ……………………………..

$32.00

$18.00

Direct labor:

$15 per DLH × 0.80 DLHs per unit…..

12.00

$15 per DLH × 0.40 DLHs per unit…..

6.00

Overhead:

$218,000 ÷ 10,000 units ……………….

21.80

$54,000 ÷ 40,000 units ………………..

1.35

Unit cost ………………………………………

$65.80

$25.35

Solutions Manual, Chapter 6 23

Exercise 6-14 (30 minutes)

1. The first step is to determine the activity rates:

Activity Cost Pools

(a)

Total Cost

(b)

Total Activity

(a) ÷ (b)

Activity Rate

Serving parties …….

$33,000

6,000

parties

$5.50

per party

Serving diners ……..

$138,000

15,000

diners

$9.20

per diner

Serving drinks ……..

$24,000

10,000

drinks

$2.40

per drink

a. Party of 4 persons who order a total of 3 drinks:

Activity Cost Pool

(a)

Activity Rate

(b)

Activity

(a) × (b)

ABC Cost

Serving parties …….

$5.50

per party

1

party

$ 5.50

Serving diners ……..

$9.20

per diner

4

diners

36.80

Serving drinks ……..

$2.40

per drink

3

drinks

7.20

Total …………………

$49.50

Activity Cost Pool

(a)

Activity Rate

(b)

Activity

(a) × (b)

ABC Cost

Serving parties …….

$5.50

per party

1

party

$ 5.50

Serving diners ……..

$9.20

per diner

2

diners

18.40

Serving drinks ……..

$2.40

per drink

0

drinks

0

Total …………………

$23.90

c. Party of 1 person who orders 2 drinks:

Activity Cost Pool

(a)

Activity Rate

(b)

Activity

(a) × (b)

ABC Cost

Serving parties …….

$5.50

per party

1

party

$ 5.50

Serving diners ……..

$9.20

per diner

1

diner

9.20

Serving drinks ……..

$2.40

per drink

2

drinks

4.80

Total …………………

$19.50

24 Managerial Accounting for Managers, 4th Edition

Exercise 6-14 (continued)

2. The average cost per diner for each party can be computed by dividing

the total cost of the party by the number of diners in the party as

follows:

3. The average cost per diner differs from party to party under the activity-

based costing system for two reasons. First, the cost of serving a party

($5.50) does not depend on the number of diners in the party.

Therefore, the average cost per diner of this activity decreases as the

costs of serving drinks are assigned to the party.

The average cost per diner differs from the overall average cost of $16

per diner for several reasons. First, the average cost of $16 per diner

includes organization-sustaining costs that are excluded from the

We should note that the activity-based costing system itself does not

various meals on the menu. It may or may not be worth the effort to

build a more detailed activity-based costing system that would take such

nuances into account.

Solutions Manual, Chapter 6 25

Exercise 6-15 (30 minutes)

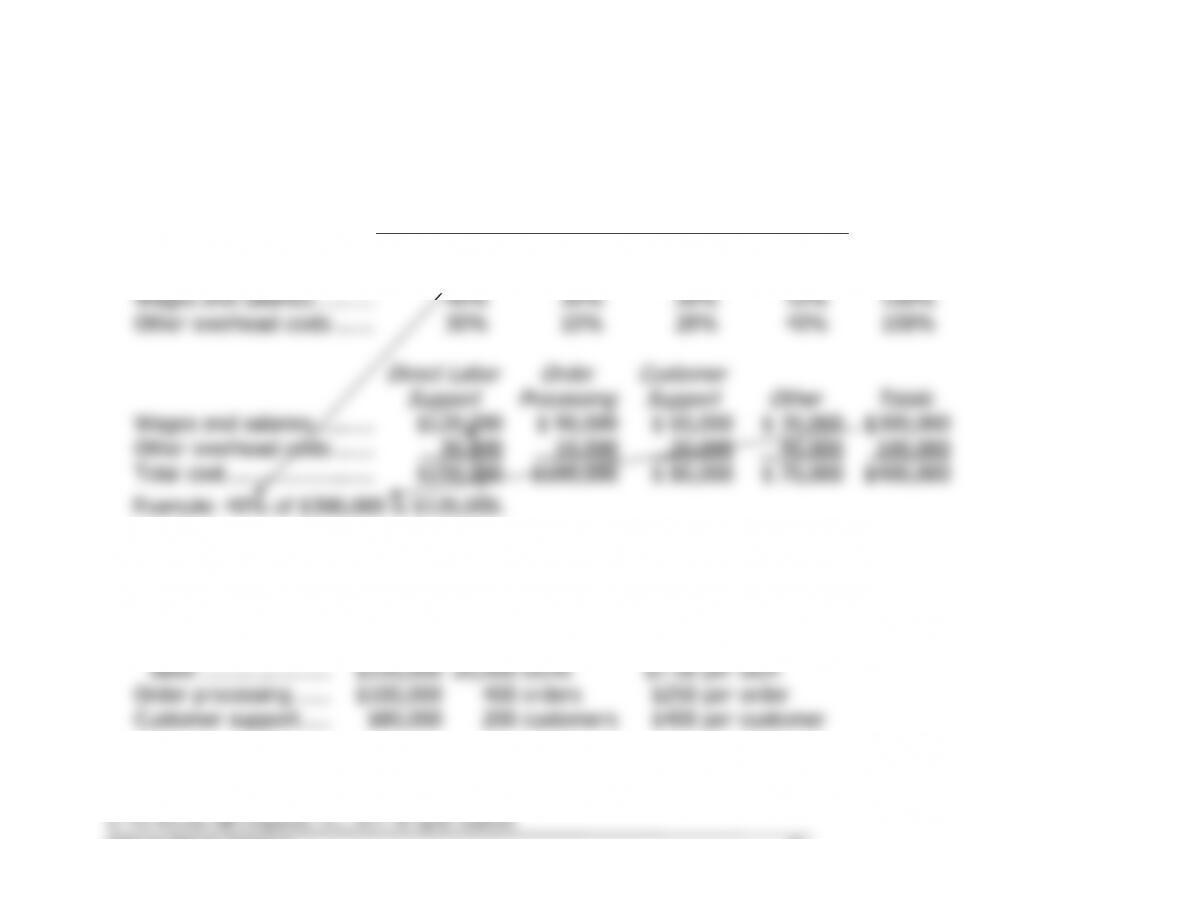

1. First-stage allocations of overhead costs to the activity cost pools:

Distribution of Resource Consumption

Across Activity Cost Pools

Supporting

Direct Labor

Order

Processing

Customer

Support

Other

Totals

Wages and salaries ……….

40%

30%

20%

10%

100%

Other overhead costs ……

30%

10%

20%

40%

100%

Direct Labor

Support

Order

Processing

Customer

Support

Other

Totals

Wages and salaries ……….

$120,000

$ 90,000

$ 60,000

$ 30,000

$300,000

Other overhead costs ……

30,000

10,000

20,000

40,000

100,000

Total cost ……………………

$150,000

$100,000

$ 80,000

$ 70,000

$400,000

Example: 40% of $300,000 is $120,000.

2. Computation of activity rates:

Activity Cost Pools

(a)

Total Cost

(b)

Total Activity

(a) ÷ (b)

Activity Rate

Supporting direct

labor …………………

$150,000

20,000

DLHs

$7.50

per DLH

Order processing ……

$100,000

400

orders

$250

per order

Customer support …..

$80,000

200

customers

$400

per customer

26 Managerial Accounting for Managers, 4th Edition

Exercise 6-15 (continued)

3. Computation of the overhead costs for the Shenzhen Enterprises order:

Activity Cost Pool

(a)

Activity Rate

(b)

Activity

(a) × (b)

ABC Cost

Supporting direct

labor ……………..

$7.50

per DLH

20

DLHs*

$150

Order processing ..

$250

per order

1

order

250

Customer support

$400

per customer

1

customer

400

Total ………………..

$800

*2 DLHs per unit × 10 units = 20 DLHs.

4. The customer margin for Shenzhen Enterprises is computed as follows:

Customer Margin—ABC Analysis

Sales (10 units × $300 per unit) …………………

$3,000

Costs:

Direct materials ($180 per unit × 10 units) …

$1,800

Direct labor ($50 per unit × 10 units) ………..

500

Support direct labor overhead (see part 3

above) ……………………………………………..

150

Order processing overhead (see part 3

above) ……………………………………………..

250

Customer support overhead (see part 3

above) ……………………………………………..

400

3,100

Customer margin …………………………………….

$ (100)

Problem 6-16 (45 minutes)

1. Under the traditional direct labor-dollar based costing system,

manufacturing overhead is applied to products using the predetermined

overhead rate computed as follows:

Estimated total manufacturing overhead cost

Predetermined =

overhead rate Estimated total direct labor dollars

$608,000

= = $2.00 per DL$

$304,000

The product margins using the traditional approach would be computed

as follows:

B300

T500

Total

Sales ……………………………..

$1,400,000

$700,000

$2,100,000

Direct materials ………………..

436,300

251,700

688,000

Direct labor ……………………..

200,000

104,000

304,000

Manufacturing overhead

applied @ $2.00 per direct

labor-dollar……………………

400,000

208,000

608,000

Total manufacturing cost ……

1,036,300

563,700

1,600,000

Product margin ………………..

$ 363,700

$136,300

$ 500,000

28 Managerial Accounting for Managers, 4th Edition

Problem 6-16 (continued)

2. The first step is to determine the activity rates:

Activity Cost Pools

(a)

Total

Cost

(b)

Total Activity

(a) ÷ (b)

Activity Rate

Machining …………..

$213,500

152,500

MHR

$1.40

per MHR

Setups ……………….

$157,500

375

setup hrs.

$420

per setup hr.

Product sustaining ..

$120,000

2

products

$60,000

per product

assigned to products.

Under the activity-based costing system, the product margins would be

computed as follows:

B300

T500

Total

Sales ……………………………..

$1,400,000

$700,000

$2,100,000

Direct materials ………………..

436,300

251,700

688,000

Direct labor ……………………..

200,000

104,000

304,000

Advertising expense ………….

50,000

100,000

150,000

Machining ……………………….

126,000

87,500

213,500

Setups …………………………...

31,500

126,000

157,500

Product sustaining …………….

60,000

60,000

120,000

Total cost ……………………….

903,800

729,200

1,633,000

Product margin ………………..

$ 496,200

$(29,200)

$ 467,000

Solutions Manual, Chapter 6 29

Problem 6-16 (continued)

3. The quantitative comparison is as follows:

B300

T500

Total

Traditional Cost System

(a)

Amount

(a) ÷ (c)

%

(b)

Amount

(b) ÷ (c)

%

(c)

Amount

Direct materials

$436,300

63.4%

$251,700

36.6%

$ 688,000

Direct labor

200,000

65.8%

104,000

34.2%

304,000

Manufacturing overhead

400,000

65.8%

208,000

34.2%

608,000

Total cost assigned to products

$1,036,300

$563,700

$1,600,000

Selling and administrative

550,000

Total cost

$2,150,000

Activity-Based Costing System

Direct costs:

Direct materials

$436,300

63.4%

$251,700

36.6%

$ 688,000

Direct labor

200,000

65.8%

104,000

34.2%

304,000

Advertising expense

50,000

33.3%

100,000

66.7%

150,000

Indirect costs:

Machining

126,000

59.0%

87,500

41.0%

213,500

Setups

31,500

20.0%

126,000

80.0%

157,500

Product sustaining

60,000

50.0%

60,000

50.0%

120,000

Total cost assigned to products

$903,800

$729,200

1,633,000

Costs not assigned to products:

Selling and administrative

400,000

Other

117,000

Total cost

$2,150,000

30 Managerial Accounting for Managers, 4th Edition

Problem 6-16 (continued)

represent organization-sustaining costs. Second, the traditional system

Machining costs to the B300 product line and 41.0% to the T500

advertising to the T500 product line.