Solutions Manual, Appendix 5A 69

Exercise 5A-3 (20 minutes)

1 a. Under super-variable costing, the unit product cost for both years

includes direct materials of $12.

1 b.

Year 1

Year 2

Sales …………………………………………………

$2,000,000

$3,000,000

Variable cost of goods sold (@ $12 per unit)

480,000

720,000

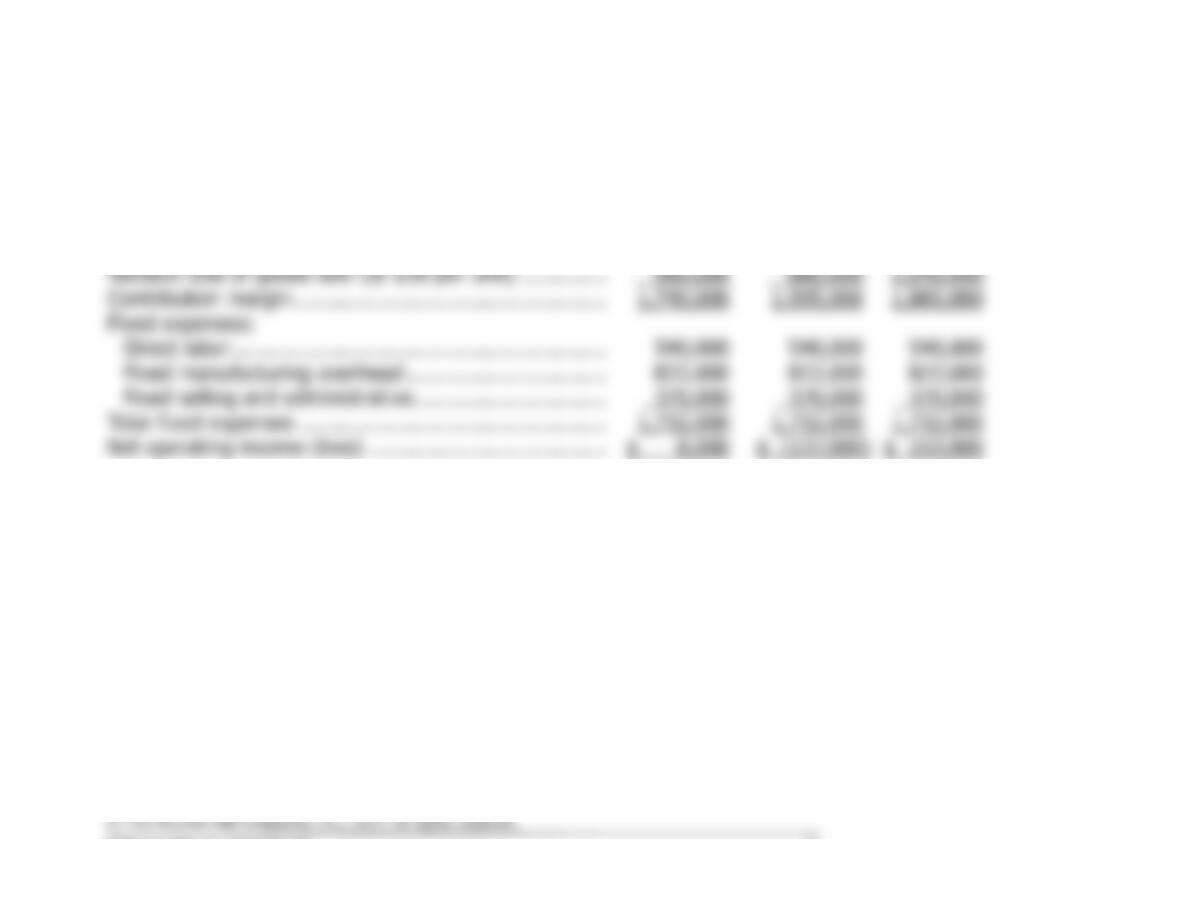

Contribution margin ………………………………

1,520,000

2,280,000

Fixed expenses:

Direct labor ………………………………………

500,000

500,000

Fixed manufacturing overhead ………………

450,000

450,000

Fixed selling and administrative …………….

180,000

180,000

Total fixed expenses ……………………………..

1,130,000

1,130,000

Net operating income …………………………...

$ 390,000

$1,150,000

2 a. The unit product costs under variable costing:

Year 1

Year 2

Direct materials ………………………………

$12

$12

Direct labor ……………………………………

*10

*10

Variable costing unit product cost ……….

$22

$22

* $500,000 ÷ 50,000 units = $10 per unit.

70 Managerial Accounting for Managers, 4th Edition

Exercise 5A-3 (continued)

2 b. The variable costing income statements would be:

Year 1

Year 2

Sales …………………………………………………

$2,000,000

$3,000,000

Variable cost of goods sold (@ $22 per unit)

880,000

1,320,000

Contribution margin ………………………………

1,120,000

1,680,000

Fixed expenses:

Fixed manufacturing overhead ………………

450,000

450,000

Fixed selling and administrative …………….

180,000

180,000

Total fixed expenses ……………………………..

630,000

630,000

Net operating income …………………………...

$ 490,000

$1,050,000

3. The net operating incomes are reconciled as follows:

Year 1

Year 2

Units in beginning inventory ……………………

0

10,000

+ Units produced …………………………………

50,000

50,000

− Units sold ………………………………………..

40,000

60,000

= Units in ending inventory …………………….

10,000

0

Year 1

Year 2

Direct labor cost in ending inventory

(10,000 units × $10 per unit) ……………….

$100,000

$ 0

− Direct labor cost in beginning inventory

(10,000 units × $10 per unit) ……………….

100,000

= Direct labor cost deferred in (released

from) inventory………………………………….

$100,000

$(100,000)

Year 1

Year 2

Super-variable costing net operating income

$390,000

$1,150,000

Add: Direct labor deferred in inventory

under variable costing …………………………

100,000

Deduct: Direct labor released from

inventory under variable costing ……………

(100,000)

Variable costing net operating income ………

$490,000

$1,050,000

Solutions Manual, Appendix 5A 71

Problem 5A-4 (30 minutes)

1 a. and b. The unit product cost for all three years under super-variable costing would include direct

materials of $16 per unit. The super-variable costing income statements appear below:

Year 1

Year 2

Year 3

Sales ………………………………………………………………

$2,700,000

$2,475,000

$2,925,000

Variable cost of goods sold (@ $16 per unit) …………..

960,000

880,000

1,040,000

Contribution margin …………………………………………..

1,740,000

1,595,000

1,885,000

Fixed expenses:

Direct labor ……………………………………………………

540,000

540,000

540,000

Fixed manufacturing overhead …………………………..

822,000

822,000

822,000

Fixed selling and administrative ………………………….

370,000

370,000

370,000

Total fixed expenses ………………………………………….

1,732,000

1,732,000

1,732,000

Net operating income (loss) ………………………………..

$ 8,000

$ (137,000)

$ 153,000

72 Managerial Accounting for Managers, 4th Edition

Problem 5A-4 (continued)

2 a. The unit product costs under variable costing:

Year 1

Year 2

Year 3

Direct materials …………………………………….

$16

$16

$16

Direct labor* ………………………………………..

9

9

9

Variable costing unit product cost ……………..

$25

$25

$25

2 b. The variable costing income statements appears below:

Year 1

Year 2

Year 3

Sales ………………………………………………………………

$2,700,000

$2,475,000

$2,925,000

Variable cost of goods sold (@ $25 per unit) …………..

1,500,000

1,375,000

1,625,000

Contribution margin …………………………………………..

1,200,000

1,100,000

1,300,000

Fixed expenses:

Fixed manufacturing overhead …………………………..

822,000

822,000

822,000

Fixed selling and administrative ………………………….

370,000

370,000

370,000

Total fixed expenses ………………………………………….

1,192,000

1,192,000

1,192,000

Net operating income (loss) ………………………………..

$ 8,000

$ (92,000)

$ 108,000

Solutions Manual, Appendix 5A 73

Problem 5A-4 (continued)

3. The net operating incomes are reconciled as follows:

Year 1

Year 2

Year 3

Units in beginning inventory ……………………

0

0

5,000

+ Units produced …………………………………

60,000

60,000

60,000

− Units sold ………………………………………..

60,000

55,000

65,000

= Units in ending inventory …………………….

0

5,000

0

Year 1

Year 2

Year 3

Direct labor cost in ending inventory (5,000

units × $9 per unit) …………………………...

$ 0

$45,000

$ 0

− Direct labor cost in beginning inventory

(5,000 units × $9 per unit) …………………..

0

45,000

= Direct labor cost deferred in (released

from) inventory………………………………….

$ 0

$45,000

$(45,000)

Year 1

Year 2

Year 3

Super-variable costing net operating income

(loss) ………………………………………………

$8,000

$(137,000)

$153,000

Add: Direct labor deferred in inventory

under variable costing …………………………

45,000

Deduct: Direct labor released from

inventory under variable costing ……………

(45,000)

Variable costing net operating income (loss)

$8,000

$ (92,000)

$108,000

74 Managerial Accounting for Managers, 4th Edition

Problem 5A-5 (45 minutes)

1. a. The unit product cost under super-variable costing would include

direct materials of $19.

b. The super-variable costing income statement would be:

Sales (18,000 units × $55 per unit) …………

$990,000

Variable cost of goods sold

(18,000 units × $19 per unit) ……………

342,000

Contribution margin …………………………….

648,000

Fixed expenses:

Direct labor ……………………………………..

$250,000

Fixed manufacturing overhead …………….

300,000

Fixed selling and administrative expense ..

90,000

640,000

Net operating income …………………………..

$ 8,000

2. a. The unit product cost under variable costing would be:

Direct materials……………………………………………………..

$19.00

Direct labor ($250,000 ÷ 20,000 units) ………………………

12.50

Variable costing unit product cost ………………………………

$31.50

b. The variable costing income statement would be:

Sales (18,000 units × $55 per unit) …………

$990,000

Variable cost of goods sold

(18,000 units × $31.50 per unit)………..

567,000

Contribution margin …………………………….

423,000

Fixed expenses:

Fixed manufacturing overhead …………….

$300,000

Fixed selling and administrative expense ..

90,000

390,000

Net operating income …………………………..

$ 33,000

Solutions Manual, Appendix 5A 75

Problem 5A-5 (continued)

3. a. The unit product cost under absorption costing would be:

Direct materials……………………………………………………..

$19.00

Direct labor ($250,000 ÷ 20,000 units) ………………………

12.50

Fixed manufacturing overhead ($300,000 ÷ 20,000 units)

15.00

Absorption costing unit product cost ………………………….

$46.50

b. The absorption costing income statement would be:

Sales (18,000 units × $55 per unit) ………………………

$990,000

Cost of goods sold (18,000 units × $46.50 per unit)…

837,000

Gross margin …………………………………………………..

153,000

Selling and administrative expenses ……………………..

90,000

Net operating income ………………………………………..

$ 63,000

Units in ending inventory = Units in beginning inventory + Units

= 2,000 units

Super-variable costing net operating income …………

$ 8,000

Add direct labor cost deferred in inventory under

variable costing ……………………………………………

25,000

Variable costing net operating income ………………….

$33,000

Direct labor and fixed manufacturing overhead cost deferred in

76 Managerial Accounting for Managers, 4th Edition

Problem 5A-5 (continued)

Super-variable costing net operating income …………

$8,000

Add direct labor and fixed manufacturing overhead

cost deferred in inventory under absorption

costing ……………………………………………………….

55,000

Absorption costing net operating income ……………..

$63,000