Solutions Manual, Chapter 5 61

Case 5-30 (75 minutes)

1. See the segmented statement on the second following page.

Supporting computations for the statement are given below:

Sales:

Membership dues (20,000 × $100) ……………………..

$2,000,000

Assigned to Magazine Subscriptions Division

(20,000 × $20) …………………………………………….

400,000

Assigned to Membership Division ………………………..

$1,600,000

Non-member magazine subscriptions (2,500 × $30) .

$ 75,000

Reports and texts (28,000 × $25) ……………………….

$ 700,000

Continuing education courses:

One-day (2,400 × $75) …………………………………..

$ 180,000

Two-day (1,760 × $125) …………………………………

220,000

Total revenue ………………………………………………….

$ 400,000

Salary and personnel costs:

Salaries

Personnel Costs

(25% of Salaries)

Membership Division …………………

$210,000

$ 52,500

Magazine Subscriptions Division …..

150,000

37,500

Books and Reports Division …………

300,000

75,000

Continuing Education Division ……..

180,000

45,000

Total assigned to divisions ………….

840,000

210,000

Corporate staff …………………………

80,000

20,000

Total ………………………………………

$920,000

$230,000

Case 5-30 (continued)

Some may argue that, except for the $50,000 in rental cost directly

attributed to the Books and Reports Division, occupancy costs are

common costs that should not be allocated. The correct treatment of

the occupancy costs depends on whether they could be avoided in part

by eliminating a division. In the solution below, we have assumed they

could be avoided.

Solutions Manual, Chapter 5 63

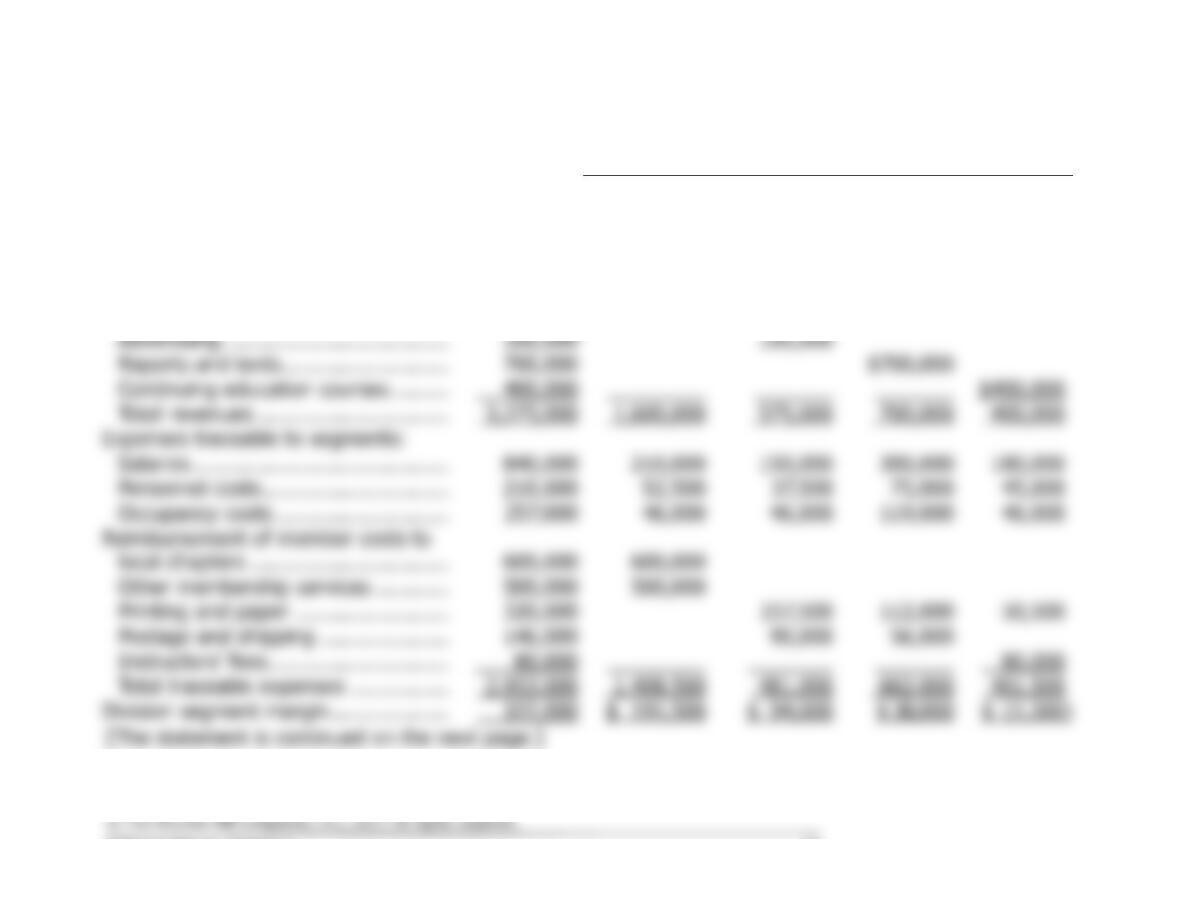

Case 5-30 (continued)

Division

Association

Total

Membership

Magazine

Subscriptions

Books &

Reports

Continuing

Education

Sales:

Membership dues ………………………

$2,000,000

$1,600,000

$400,000

Non-member magazine

subscriptions ………………………….

75,000

75,000

Advertising …………………………..….

100,000

100,000

Reports and texts ………………………

700,000

$700,000

Continuing education courses ………

400,000

$400,000

Total revenues ………………………….

3,275,000

1,600,000

575,000

700,000

400,000

Expenses traceable to segments:

Salaries …………………………………..

840,000

210,000

150,000

300,000

180,000

Personnel costs …………………………

210,000

52,500

37,500

75,000

45,000

Occupancy costs ……………………….

257,000

46,000

46,000

119,000

46,000

Reimbursement of member costs to

local chapters …………………………..

600,000

600,000

Other membership services …………

500,000

500,000

Printing and paper …………………….

320,000

157,500

112,000

50,500

Postage and shipping …………………

146,000

90,000

56,000

Instructors’ fees ………………………..

80,000

80,000

Total traceable expenses …………….

2,953,000

1,408,500

481,000

662,000

401,500

Division segment margin ……………….

322,000

$ 191,500

$ 94,000

$ 38,000

$ (1,500)

[The statement is continued on the next page.]

64 Managerial Accounting for Managers, 4th Edition

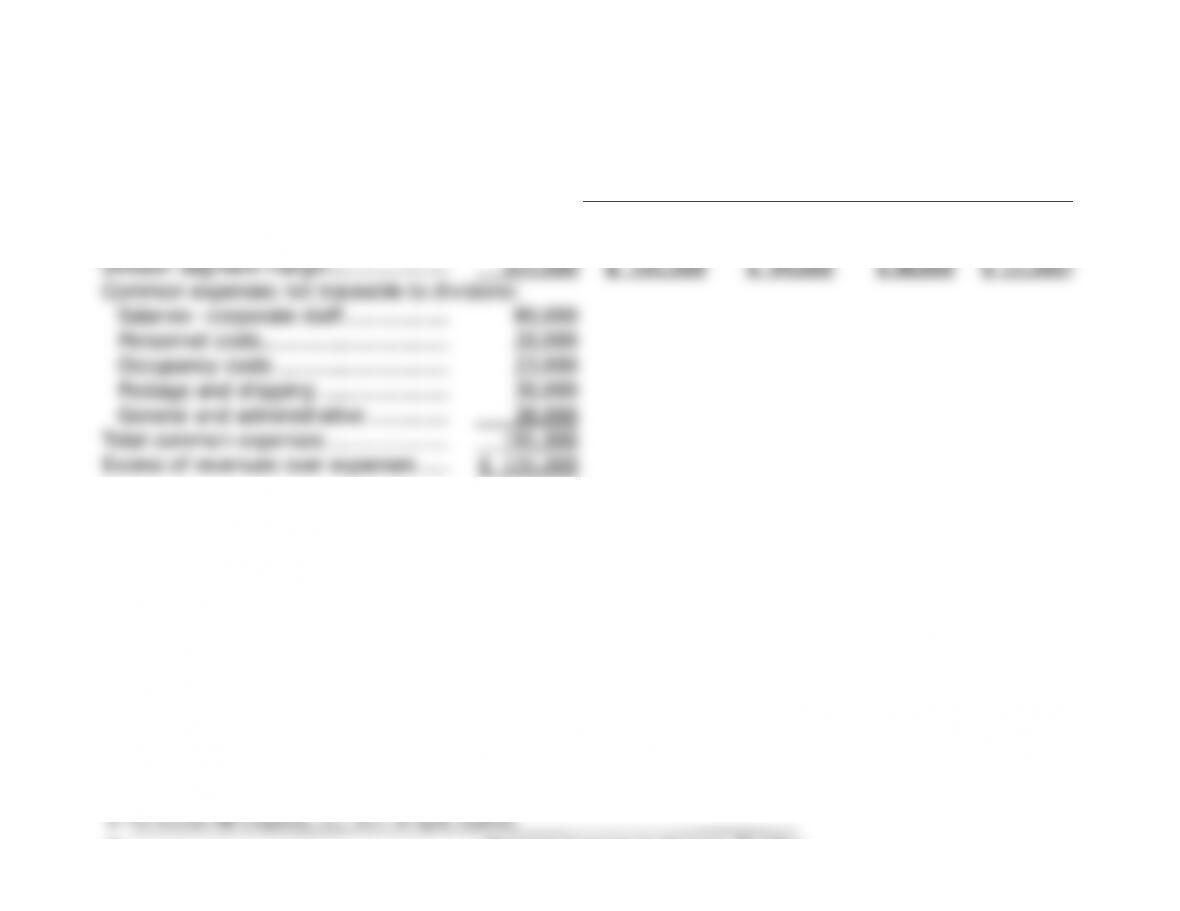

Case 5-30 (continued)

[Continuation of the segmented income statement.]

Division

Association

Total

Membership

Magazine

Subscriptions

Books &

Reports

Continuing

Education

Division segment margin ……………….

322,000

$ 191,500

$ 94,000

$ 38,000

$ (1,500)

Common expenses not traceable to divisions:

Salaries—corporate staff ……………..

80,000

Personnel costs …………………………

20,000

Occupancy costs ……………………….

23,000

Postage and shipping …………………

30,000

General and administrative ………….

38,000

Total common expenses ………………..

191,000

Excess of revenues over expenses …..

$ 131,000

Solutions Manual, Appendix 5A 65

Case 5–30 (continued)

2. While we do not favor the allocation of common costs to segments, the

Arguments against allocation of all costs:

• Allocation bases will need to be chosen arbitrarily because no cause–

• Management may be misled into eliminating a profitable segment

• Segment managers usually have little control over common costs.

no control.

the entire performance report as arbitrary and unfair.

66 Managerial Accounting for Managers, 4th Edition

Appendix 5A

Super-Variable Costing

Exercise 5A-1 (10 minutes)

1. a. The unit product cost under super-variable costing would include

direct materials of $18.

b. The super–variable costing income statement would be:

Sales (20,000 units × $50 per unit) …………

$1,000,000

Variable cost of goods sold

(20,000 units × $18 per unit) ……………

360,000

Contribution margin …………………………….

640,000

Fixed expenses:

Direct labor ……………………………………..

$200,000

Fixed manufacturing overhead …………….

250,000

Fixed selling and administrative expense ..

80,000

530,000

Net operating income …………………………..

$ 110,000

Solutions Manual, Appendix 5A 67

Exercise 5A-2 (20 minutes)

1. a. The unit product cost under super-variable costing would include

direct materials of $13.

b. The super–variable costing income statement would be:

Sales (52,000 units × $40 per unit) …………

$2,080,000

Variable cost of goods sold

(52,000 units × $13 per unit) ……………

676,000

Contribution margin …………………………….

1,404,000

Fixed expenses:

Direct labor ……………………………………..

$750,000

Fixed manufacturing overhead …………….

420,000

Fixed selling and administrative expense ..

110,000

1,280,000

Net operating income …………………………..

$ 124,000

2. a. The unit product cost under variable costing would be:

Direct materials……………………………………………………..

$13.00

Direct labor ($750,000 ÷ 60,000 units) ………………………

12.50

Variable costing unit product cost ………………………………

$25.50

Sales (52,000 units × $40 per unit) ………..

$2,080,000

Variable cost of goods sold

(52,000 units × $25.50 per unit) ……….

1,326,000

Contribution margin …………………………...

754,000

Fixed expenses:

Fixed manufacturing overhead ……………

420,000

Fixed selling and administrative

expense ………………………………………

110,000

530,000

Net operating income ………………………….

$ 224,000

68 Managerial Accounting for Managers, 4th Edition

Exercise 5A-2 (continued)

3. The difference between the super-variable costing and variable costing

net operating incomes is explained as follows:

= 8,000 units

Super-variable costing net operating income ………………

$124,000

Add direct labor cost deferred in inventory under

variable costing …………………………………………………

100,000

Variable costing net operating income ………………………

$224,000