Solutions Manual, Chapter 5 51

Problem 5-26 (60 minutes)

1. The disadvantages or weaknesses of the company’s version of a

segmented income statement are as follows:

of the three regions taken together.

b. The regional expenses should be segregated into variable and fixed

and a regional segment margin.

should not be arbitrarily allocated.

2. Corporate advertising expenses have been allocated on the basis of

sales dollars; the general administrative expenses have been allocated

the segments—should be used to measure the performance of a

52 Managerial Accounting for Managers, 4th Edition

Problem 5-26 (continued)

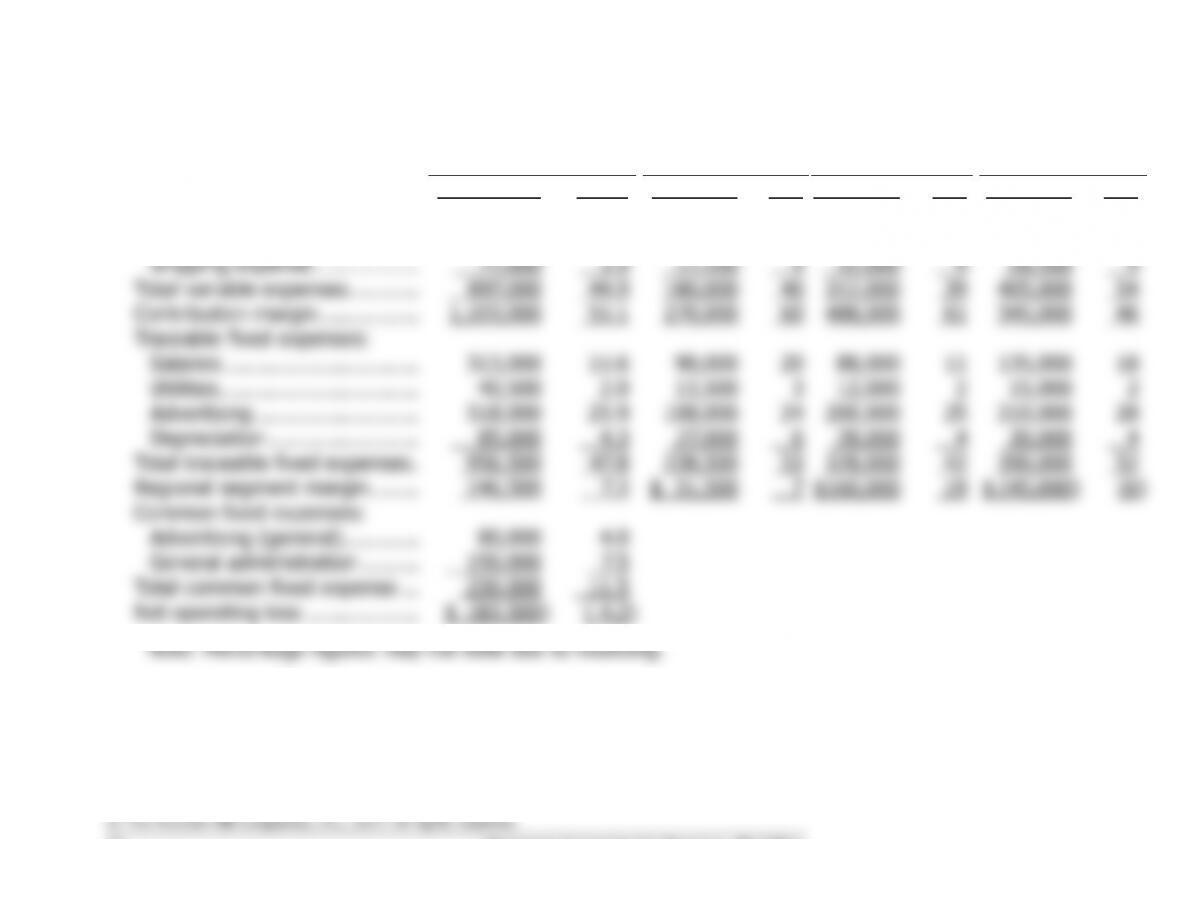

3.

Total Company

West

Central

East

Sales ……………………………….

$2,000,000

100.0

$450,000

100

$800,000

100

$750,000

100

Variable expenses:

Cost of goods sold ……………

819,400

41.0

162,900

36

280,000

35

376,500

50

Shipping expense ……………..

77,600

3.9

17,100

4

32,000

4

28,500

4

Total variable expenses ………..

897,000

44.9

180,000

40

312,000

39

405,000

54

Contribution margin …………….

1,103,000

55.1

270,000

60

488,000

61

345,000

46

Traceable fixed expenses:

Salaries ………………………….

313,000

15.6

90,000

20

88,000

11

135,000

18

Utilities …………………………..

40,500

2.0

13,500

3

12,000

2

15,000

2

Advertising ……………………..

518,000

25.9

108,000

24

200,000

25

210,000

28

Depreciation ……………………

85,000

4.3

27,000

6

28,000

4

30,000

4

Total traceable fixed expenses .

956,500

47.8

238,500

53

328,000

42

390,000

52

Regional segment margin ……..

146,500

7.3

$ 31,500

7

$160,000

19

$ (45,000)

(6)

Common fixed expenses:

Advertising (general) …………

80,000

4.0

General administration ………

150,000

7.5

Total common fixed expense …

230,000

11.5

Net operating loss ………………

$ (83,500)

( 4.2)

Solutions Manual, Chapter 5 53

Problem 5-26 (continued)

4. The following points should be brought to the attention of management:

three regions.

b. The West is spending about half as much for advertising as the

Central Region. Perhaps this is the reason for the West’s lower sales.

d. The East appears to be overstaffed. Its salaries are about 50%

greater than in either of the other two regions.

e. The East is not covering its own traceable costs. Attention should be

region.

f. Apparently, the salespeople in all three regions are on a salary basis.

54 Managerial Accounting for Managers, 4th Edition

Problem 5-27 (30 minutes)

1. Because of soft demand for the Brazilian Division’s product, the

inventory should be drawn down to the minimum level of 50 units.

as follows during the last quarter:

Desired inventory, December 31 ……….

50 units

Expected sales, last quarter …………….

600 units

Total needs ………………………………….

650 units

Less inventory, September 30 …………..

400 units

Required production ………………………

250 units

insurance), interest, and obsolescence.

The number of units scheduled for production will not affect the

through the inventory account and income would be a function of the

number of units sold, rather than a function of the number of units

produced.

2. To maximize the Brazilian Division’s operating income, Mr. Cavalas could

produce as many units as storage facilities will allow. By building

inventory to the maximum level of 1,000 units would require production

as follows during the last quarter:

Desired inventory, December 31 ….

1,000 units

Expected sales, last quarter ……….

600 units

Total needs …………………………….

1,600 units

Less inventory, September 30 ……..

400 units

Required production …………………

1,200 units

Solutions Manual, Chapter 5 55

Problem 5-27 (continued)

maximize the current year’s operating income.

3. By setting a production schedule that will maximize his division’s net

The company’s bonus plan undoubtedly is intended to increase the

company’s profits by increasing sales and controlling expenses. If Mr.

In sum, producing as much as possible so as to maximize the division’s

Problem 5-28 (45 minutes)

1.

Total

Company

Cook–

book

Travel

Guide

Handy

Speller

Sales …………………………..……

$300,000

$90,000

$150,000

$60,000

Variable expenses:

Printing cost …………………….

102,000

27,000

63,000

12,000

Sales commissions…………….

30,000

9,000

15,000

6,000

Total variable expenses ………..

132,000

36,000

78,000

18,000

Contribution margin …………….

168,000

54,000

72,000

42,000

Traceable fixed expenses:

Advertising………………………

36,000

13,500

19,500

3,000

Salaries ………………………….

33,000

18,000

9,000

6,000

Equipment depreciation*

9,000

2,700

4,500

1,800

Warehouse rent** …………….

12,000

1,800

6,000

4,200

Total traceable fixed expenses .

90,000

36,000

39,000

15,000

Product line segment margin …

78,000

$18,000

$ 33,000

$27,000

Common fixed expenses:

General sales …………………..

18,000

General administration ……….

42,000

Depreciation—office facilities .

3,000

Total common fixed expenses ..

63,000

Net operating income …………..

$ 15,000

*

$9,000 × 30%, 50%, and 20%, respectively.

**

$48,000 square feet × $3 per square foot = $144,000; $144,000 ÷ 12

months = $12,000 per month. $12,000 ÷ 48,000 square feet = $0.25 per

square foot per month.

$0.25 per square foot × 7,200 square feet = $1,800; $0.25 per square

foot × 24,000 square feet = $6,000; and $0.25 per square foot × 16,800

square feet = $4,200.

Solutions Manual, Chapter 5 57

Problem 5-28 (continued)

b.

Cook–

book

Travel

Guide

Handy

Speller

Contribution margin (a) ………………

$54,000

$72,000

$42,000

Sales (b) ………………………………….

$90,000

$150,000

$60,000

Contribution margin ratio (a) ÷ (b) ..

60%

48%

70%

products. Nevertheless, we cannot say for sure which product should

which suggests that there is no idle capacity. If the equipment is

products.

58 Managerial Accounting for Managers, 4th Edition

Case 5-29 (45 minutes)

1 a. Under variable costing, only the variable manufacturing costs are included in product costs.

Year 1

Year 2

Year 3

Direct materials ………………………………

$32

$32

$32

Direct labor ……………………………………

20

20

20

Variable manufacturing overhead ……….

4

4

4

Variable costing unit product cost ……….

$56

$56

$56

1 b. The variable costing income statements appear below:

Year 1

Year 2

Year 3

Sales …………………………………………………………………

$6,000,000

$6,750,000

$5,625,000

Variable expenses:

Variable cost of goods sold @ $56 per unit ………………

4,480,000

5,040,000

4,200,000

Variable selling and administrative @ $3 per unit ………

240,000

270,000

225,000

Total variable expenses …………………………………………

4,720,000

5,310,000

4,425,000

Contribution margin ……………………………………………..

1,280,000

1,440,000

1,200,000

Fixed expenses:

Fixed manufacturing overhead ……………………………..

660,000

660,000

660,000

Fixed selling and administrative …………………………….

120,000

120,000

120,000

Total fixed expenses ……………………………………………..

780,000

780,000

780,000

Net operating income ……………………………………………

$ 500,000

$ 660,000

$ 420,000

2a. and 2b.

constant.

Solutions Manual, Chapter 5 59

Case 5-29 (continued)

3 a. The unit product costs under absorption costing:

Year 1

Year 2

Year 3

Direct materials ………………………………

$32.00

$32.00

$32.00

Direct labor ……………………………………

20.00

20.00

20.00

Variable manufacturing overhead ……….

4.00

4.00

4.00

Fixed manufacturing overhead …………..

*6.60

**8.80

***8.25

Absorption costing unit product cost ……

$62.60

$64.80

$64.25

* $660,000 ÷ 100,000 units = $6.60 per unit.

** $660,000 ÷ 75,000 units = $8.80 per unit.

*** $660,000 ÷ 80,000 units = $8.25 per unit.

3 b. The absorption costing income statements appear below (FIFO):

Year 1

Year 2

Year 3

Sales ……………………………………………..

$6,000,000

$6,750,000

$5,625,000

Cost of goods sold…………………………….

5,008,000

5,788,000

4,821,500

Gross margin …………………………………..

992,000

962,000

803,500

Selling and administrative expenses ……..

360,000

390,000

345,000

Net operating income ………………………..

$ 632,000

$ 572,000

$ 458,500

Cost of goods sold computations:

Year 1: 80,000 units × $62.60 per unit = $5,008,000

Year 2: (20,000 units × $62.60 per unit) + (70,000 units × $64.80 per unit) = $5,788,000

Year 3: (5,000 × $64.80 per unit) + (70,000 × $64.25 per unit) = $4,821,500

60 Managerial Accounting for Managers, 4th Edition

Case 5-29 (continued)

4 a. The unit product costs under absorption costing:

Year 1

Year 2

Year 3

Direct materials ………………………………

$32.00

$32.00

$32.00

Direct labor ……………………………………

20.00

20.00

20.00

Variable manufacturing overhead ……….

4.00

4.00

4.00

Fixed manufacturing overhead …………..

*6.60

**8.80

***8.25

Absorption costing unit product cost ……

$62.60

$64.80

$64.25

* $660,000 ÷ 100,000 units = $6.60 per unit.

** $660,000 ÷ 75,000 units = $8.80 per unit.

*** $660,000 ÷ 80,000 units = $8.25 per unit.

Year 1

Year 2

Year 3

Sales ……………………………………………..

$6,000,000

$6,750,000

$5,625,000

Cost of goods sold…………………………….

5,008,000

5,799,000

4,818,750

Gross margin …………………………………..

992,000

951,000

806,250

Selling and administrative expenses ……..

360,000

390,000

345,000

Net operating income ………………………..

$ 632,000

$ 561,000

$ 461,250

Cost of goods sold computations:

Year 1: 80,000 units × $62.60 per unit = $5,008,000

Year 2: (75,000 units × $64.80 per unit) + (15,000 units × $62.60 per unit) = $5,799,000

Year 3: 75,000 × $64.25 per unit = $4,818,750