Solutions Manual, Chapter 3 1

Chapter 3

Cost-Volume-Profit Relationships

Solutions to Questions

3-1 The contribution margin (CM) ratio is

the ratio of the total contribution margin to total

sales revenue. It can also be expressed as the

3-2 Incremental analysis focuses on the

profits when sales increase.

3-6 (a) If the selling price decreased, then

the total revenue line would rise less steeply,

and the break-even point would occur at a

higher unit volume. (b) If the fixed cost

increased, then both the fixed cost line and the

total cost line would shift upward and the break-

3-7 The margin of safety is the excess of

budgeted (or actual) sales over the break-even

3-9 A higher break-even point and a lower

net operating income could result if the sales

contribution margin ratio, the break-even point

2 Managerial Accounting for Managers, 4th Edition

The Foundational 15

1. The contribution margin per unit is calculated as follows:

Total contribution margin (a) …………..

$8,000

Total units sold (b) ……. …….. …………

1,000

units

Contribution margin per unit (a) ÷ (b) .

$8.00

per unit

2. The contribution margin ratio is calculated as follows:

Total contribution margin (a) …………..

$8,000

Total sales (b) ………….. …….. …………

$20,000

Contribution margin ratio (a) ÷ (b) ……

40%

3. The variable expense ratio is calculated as follows:

Total variable expenses (a) ……………..

$12,000

Total sales (b) ………….. …….. …………

$20,000

Variable expense ratio (a) ÷ (b) ……….

60%

4. The increase in net operating is calculated as follows:

Contribution margin per unit (a) …………………

$8.00

per unit

Increase in unit sales (b) ………………………….

1

unit

Increase in net operating income (a) × (b) …..

$8.00

5. If sales decline to 900 units, the net operating would be computed as

follows:

Total

Per Unit

Sales (900 units) ……….

$18,000

$20.00

Variable expenses ………

10,800

12.00

Contribution margin ……

7,200

$ 8.00

Fixed expenses ………….

6,000

Net operating income ….

$ 1,200

Solutions Manual, Chapter 3 3

The Foundational 15 (continued)

6. The new net operating income would be computed as follows:

Total

Per Unit

Sales (900 units) ……….

$19,800

$22.00

Variable expenses ………

10,800

12.00

Contribution margin ……

9,000

$10.00

Fixed expenses ………….

6,000

Net operating income ….

$ 3,000

7. The new net operating income would be computed as follows:

Total

Per Unit

Sales (1,250 units) ……..

$25,000

$20.00

Variable expenses ………

16,250

13.00

Contribution margin ……

8,750

$ 7.00

Fixed expenses ………….

7,500

Net operating income ….

$ 1,250

8. The equation method yields the break-even point in unit sales, Q, as

follows:

Profit

= Unit CM × Q − Fixed expenses

$0

= ($20 − $12) × Q − $6,000

$0

= ($8) × Q − $6,000

$8Q

= $6,000

Q

= $6,000 ÷ $8

Q

= 750 units

9. The equation method yields the dollar sales to break-even as follows:

Profit

= CM ratio × Sales − Fixed expenses

$0

= 0.40 × Sales − $6,000

0.40 × Sales

= $6,000

Sales

= $6,000 ÷ 0.40

Sales

= $15,000

The dollar sales to break-even ($15,000) can also be computed by

4 Managerial Accounting for Managers, 4th Edition

The Foundational 15 (continued)

10. The equation method yields the target profit as follows:

Profit

= Unit CM × Q − Fixed expenses

$5,000

= ($20 − $12) × Q − $6,000

$5,000

= ($8) × Q − $6,000

$8Q

= $11,000

Q

= $11,000 ÷ $8

Q

= 1,375 units

11. The margin of safety in dollars is calculated as follows:

Sales ……………………………………………………..

$20,000

Break-even sales (at 750 units) ……………………

15,000

Margin of safety (in dollars) ………………………..

$ 5,000

Margin of safety (in dollars) (a) ……………..

$5,000

Sales (b) …………………………………………..

$20,000

Margin of safety percentage (a) ÷ (b) …….

25%

12. The degree of operating leverage is calculated as follows:

Contribution margin (a) …………………..

$8,000

Net operating income (b) ………………….

$2,000

Degree of operating leverage (a) ÷ (b) ..

4.0

operating income, computed as follows:

Degree of operating leverage (a) ………………………..

4.0

Percent increase in sales (b) ………………………………

5%

Percent increase in net operating income (a) × (b) …

20%

14. The degree of operating leverage is calculated as follows:

Contribution margin (a) . ………………….

$14,000

Net operating income (b) …………………

$2,000

Degree of operating leverage (a) ÷ (b) .

7.0

Solutions Manual, Chapter 3 5

The Foundational 15 (continued)

15. A 5% increase in sales should result in 35% increase in net operating

income, computed as follows:

Degree of operating leverage (a) ………………………..

7.0

Percent increase in sales (b) ………………………………

5%

Percent increase in net operating income (a) × (b) …

35%

6 Managerial Accounting for Managers, 4th Edition

Exercise 3-1 (20 minutes)

1. The new income statement would be:

Total

Per Unit

Sales (10,100 units) ……..

$353,500

$35.00

Variable expenses ………..

202,000

20.00

Contribution margin ………

151,500

$15.00

Fixed expenses ……………

135,000

Net operating income ……

$ 16,500

approach:

Original net operating income ….

$15,000

Change in contribution margin

(100 units × $15.00 per unit) ..

1,500

New net operating income ………

$16,500

2. The new income statement would be:

Total

Per Unit

Sales (9,900 units) …………

$346,500

$35.00

Variable expenses ………….

198,000

20.00

Contribution margin ………..

148,500

$15.00

Fixed expenses ……………..

135,000

Net operating income ……..

$ 13,500

approach:

Original net operating income ………….

$15,000

Change in contribution margin

(-100 units × $15.00 per unit) ……….

(1,500)

New net operating income ………………

$13,500

Solutions Manual, Chapter 3 7

Exercise 3-1 (continued)

3. The new income statement would be:

Total

Per Unit

Sales (9,000 units) …….

$315,000

$35.00

Variable expenses ……..

180,000

20.00

Contribution margin ……

135,000

$15.00

Fixed expenses …………

135,000

Net operating income …

$ 0

8 Managerial Accounting for Managers, 4th Edition

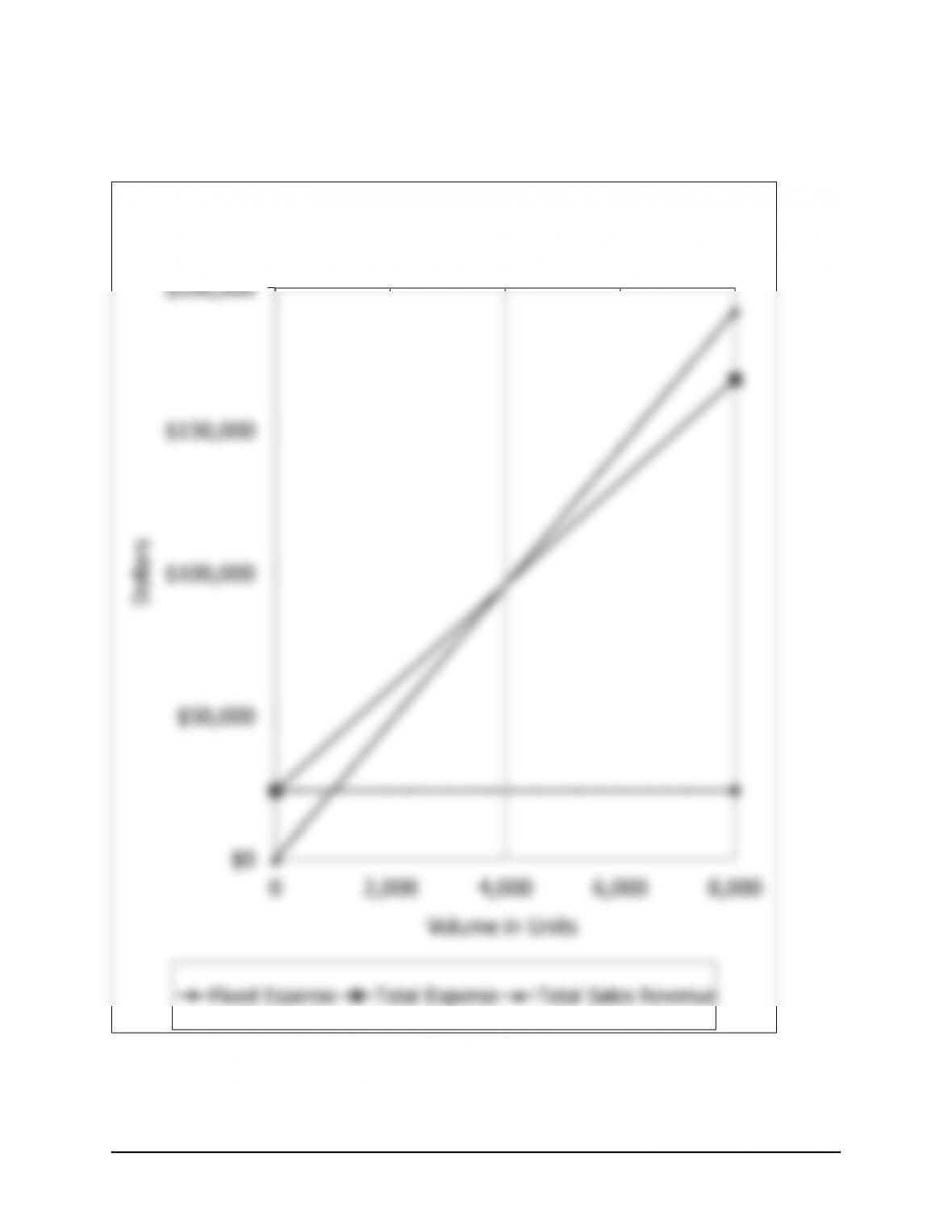

Exercise 3-2 (30 minutes)

1. The CVP graph can be plotted using the three steps outlined in the text.

The graph appears on the next page.

Step 2. Choose some volume of sales and plot the point representing

total expenses (fixed and variable) at the activity level you have

Fixed expenses ……………………………………………

$ 24,000

Variable expenses (8,000 units × $18 per unit) …..

144,000

Total expense ……………………………………………..

$168,000

sales level of 8,000 units again.

Total sales revenue (8,000 units × $24 per unit) …

$192,000

2. The break-even point is the point where the total sales revenue and the

can be verified as follows:

Profit

= Unit CM × Q − Fixed expenses

= ($24 − $18) × 4,000 − $24,000

= $6 × 4,000 − $24,000

= $24,000− $24,000

= $0

Exercise 3-2 (continued)

$150,000

$200,000

CVP Graph

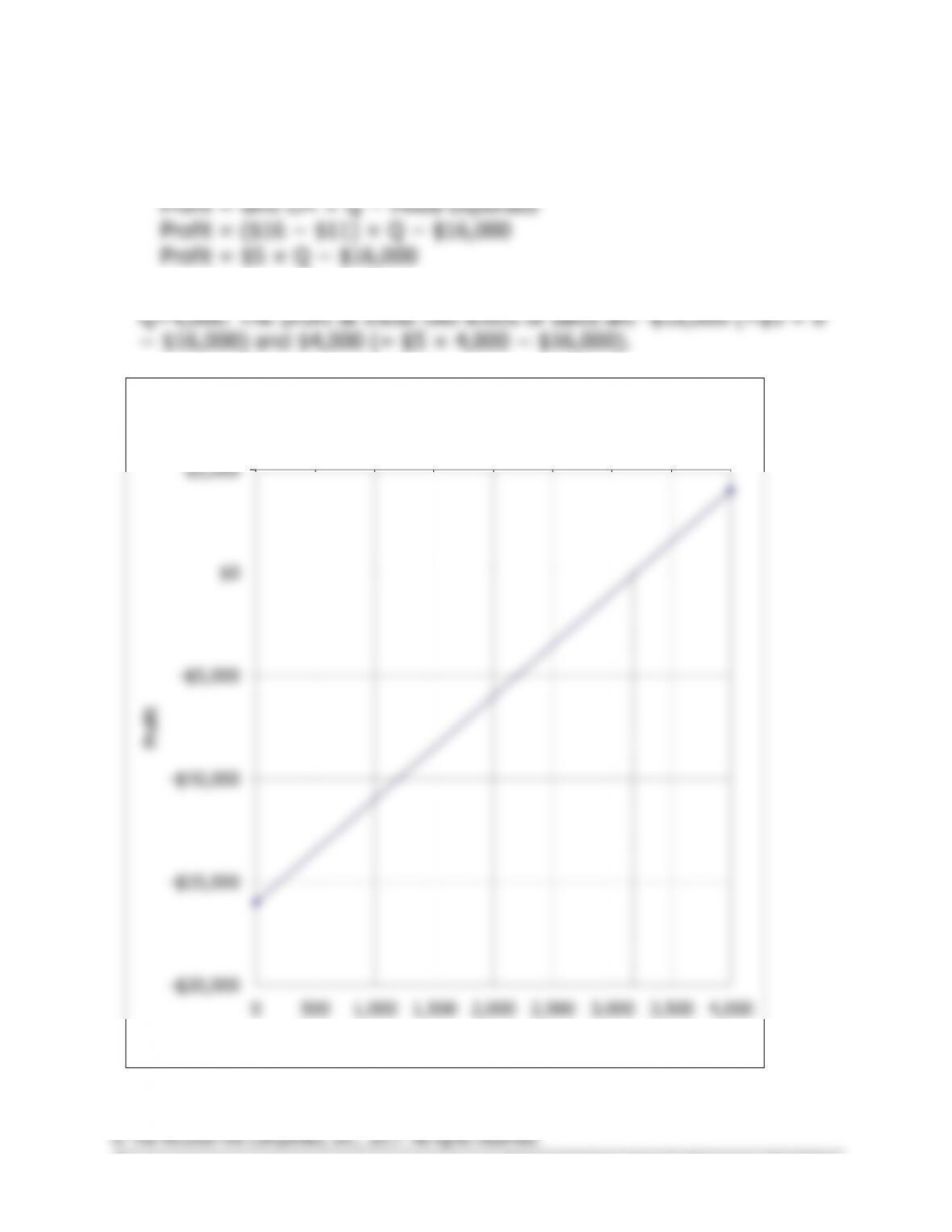

Exercise 3-3 (15 minutes)

1. The profit graph is based on the following simple equation:

Profit

= Unit CM × Q − Fixed expenses

Profit

= ($16 − $11) × Q − $16,000

Profit

= $5 × Q − $16,000

To plot the graph, select two different levels of sales such as Q=0 and

$0

$5,000

Profit Graph