Solutions Manual, Chapter 2 31

Problem 2-19 (45 minutes)

1.

Marwick’s Pianos, Inc.

Traditional Income Statement

For the Month of August

Sales (40 pianos × $3,125 per piano) ……………

$125,000

Cost of goods sold

(40 pianos × $2,450 per piano) …………………

98,000

Gross margin …………………………………………..

27,000

Selling and administrative expenses:

Selling expenses:

Advertising …………………………………………

$ 700

Sales salaries and commissions

[$950 + (8% × $125,000)] ………………….

10,950

Delivery of pianos

(40 pianos × $30 per piano)…………………

1,200

Utilities ………………………………………………

350

Depreciation of sales facilities …………………

800

Total selling expenses ……………………………..

14,000

Administrative expenses:

Executive salaries …………………………………

2,500

Insurance …………………………………………..

400

Clerical

[$1,000 + (40 pianos × $20 per piano)] …

1,800

Depreciation of office equipment ……………..

300

Total administrative expenses ……………………

5,000

Total selling and administrative expenses ……….

19,000

Net operating income ………………………………..

$ 8,000

32 Managerial Accounting for Managers, 4th edition

Problem 2-19 (continued)

2.

Marwick’s Pianos, Inc.

Contribution Format Income Statement

For the Month of August

Total

Per

Piano

Sales (40 pianos × $3,125 per piano) ……………..

$125,000

$3,125

Variable expenses:

Cost of goods sold

(40 pianos × $2,450 per piano) ………………..

98,000

2,450

Sales commissions (8% × $125,000) ……………

10,000

250

Delivery of pianos (40 pianos × $30 per piano)

1,200

30

Clerical (40 pianos × $20 per piano) …………….

800

20

Total variable expenses ………………………………..

110,000

2,750

Contribution margin …………………………………….

15,000

$ 375

Fixed expenses:

Advertising ……………………………………………..

700

Sales salaries …………………………………………..

950

Utilities …………………………………………………..

350

Depreciation of sales facilities ……………………..

800

Executive salaries …………………………………….

2,500

Insurance ……………………………………………….

400

Clerical …………………………………………………..

1,000

Depreciation of office equipment …………………

300

Total fixed expenses ……………………………………

7,000

Net operating income ………………………………….

$ 8,000

3. Fixed costs remain constant in total but vary on a per unit basis

inversely with changes in the activity level. As the activity level

increases, for example, the fixed costs will decrease on a per unit basis.

Showing fixed costs on a per unit basis on the income statement might

Solutions Manual, Chapter 2 33

Problem 2-20 (45 minutes)

1. Maintenance cost at the 90,000 machine-hour level of activity can be

isolated as follows:

Level of Activity

60,000 MHs

90,000 MHs

Total factory overhead cost ……..

$174,000

$246,000

Deduct:

Utilities cost @ $0.80 per MH* .

48,000

72,000

Supervisory salaries …………….

21,000

21,000

Maintenance cost ………………….

$105,000

$153,000

2. High-low analysis of maintenance cost:

Machine-

Hours

Maintenance

Cost

High activity level ………………..

90,000

$153,000

Low activity level …………………

60,000

105,000

Change ……………………………..

30,000

$ 48,000

Variable rate:

Change in cost $48,000

= = $1.60 per MH

Change in activity 30,000 MHs

Total fixed cost:

Total maintenance cost at the high activity level ..

$153,000

Less variable cost element

(90,000 MHs × $1.60 per MH) …………………….

144,000

Fixed cost element ……………………………………..

$ 9,000

$1.60 per machine-hour or

34 Managerial Accounting for Managers, 4th edition

Problem 2-20 (continued)

3.

Variable Cost per

Machine-Hour

Fixed Cost

Utilities cost ………………..

$0.80

Supervisory salaries cost ..

$21,000

Maintenance cost …………

1.60

9,000

Total overhead cost ………

$2.40

$30,000

4. Total overhead cost at an activity level of 75,000 machine-hours:

Fixed costs ………………………………………….

$ 30,000

Variable costs: 75,000 MHs × $2.40 per MH

180,000

Total overhead costs ……………………………..

$210,000

Solutions Manual, Chapter 2 35

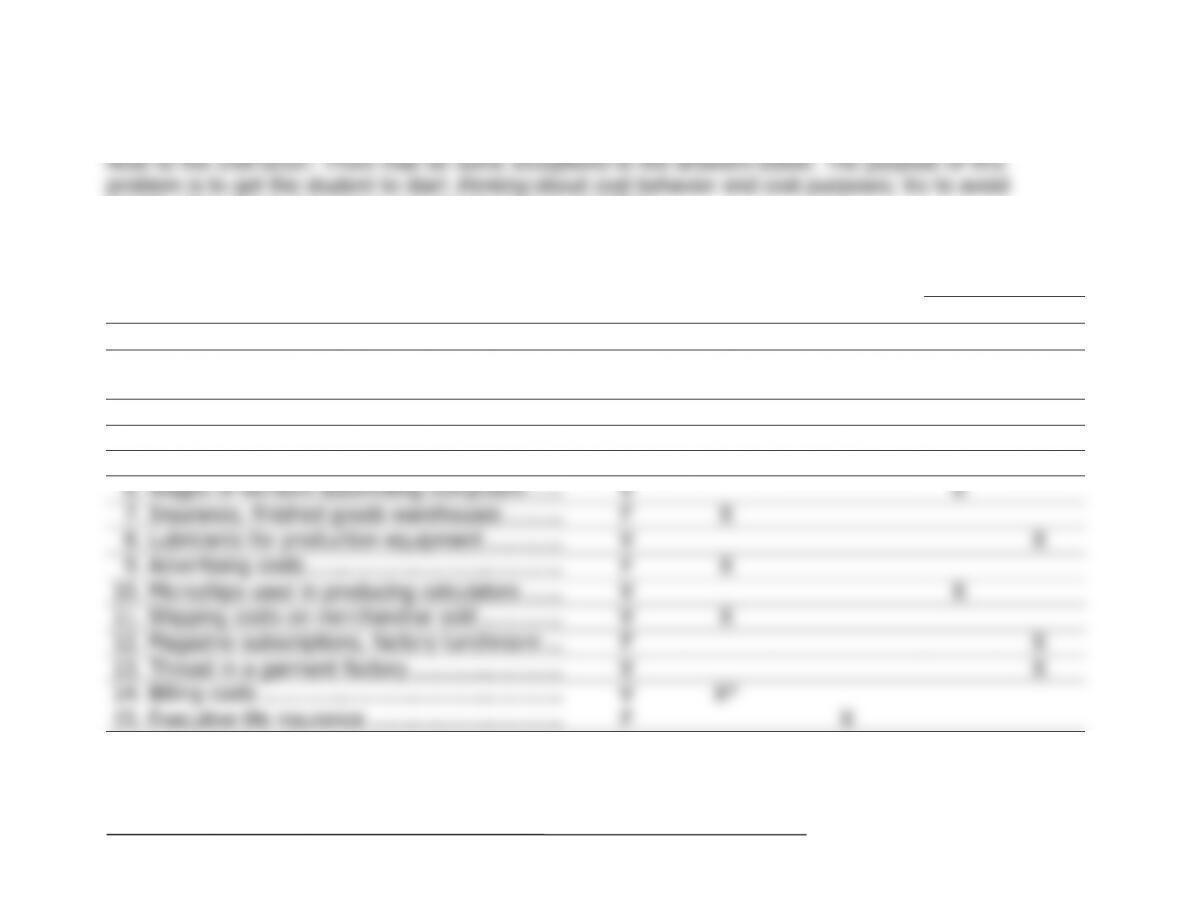

Problem 2-21 (30 minutes)

lengthy discussions about how a particular cost is classified.

Variable or

Selling

Administrative

Manufacturing

(Product) Cost

Cost Item

Fixed

Cost

Cost

Direct

Indirect

1.

Property taxes, factory …………………………..

F

X

2.

Boxes used for packaging detergent

produced by the company …………………….

V

X

3.

Salespersons’ commissions ……………………..

V

X

4.

Supervisor’s salary, factory ……………………..

F

X

5.

Depreciation, executive autos ………………….

F

X

6.

Wages of workers assembling computers …..

V

X

7.

Insurance, finished goods warehouses ………

F

X

8.

Lubricants for production equipment …………

V

X

9.

Advertising costs …………………………………..

F

X

10.

Microchips used in producing calculators ……

V

X

11.

Shipping costs on merchandise sold ………….

V

X

12.

Magazine subscriptions, factory lunchroom …

F

X

13.

Thread in a garment factory ……………………

V

X

14.

Billing costs …………………………………………

V

X*

15.

Executive life insurance ………………………….

F

X

36 Managerial Accounting for Managers, 4th edition

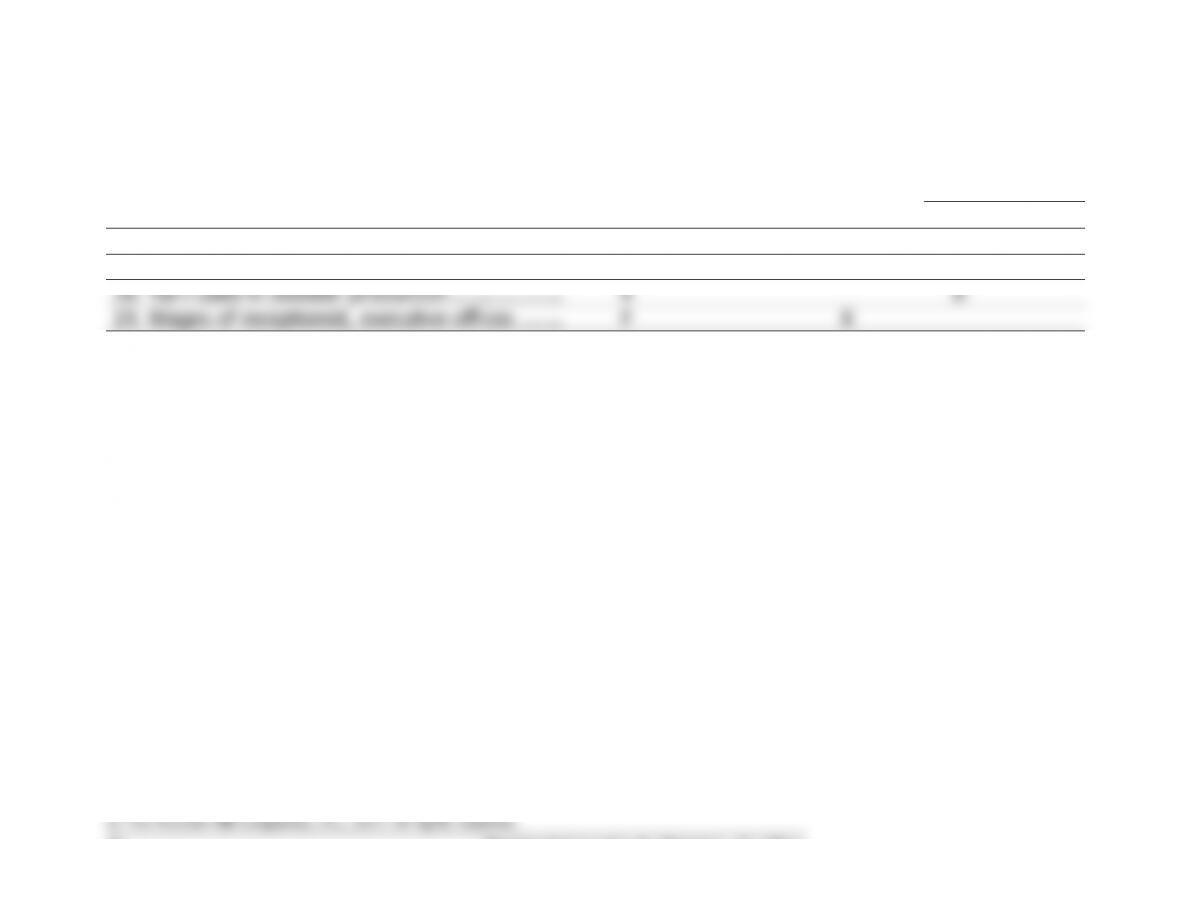

Problem 2-21 (continued)

Variable or

Selling

Administrative

Manufacturing

(Product) Cost

Cost Item

Fixed

Cost

Cost

Direct

Indirect

16.

Ink used in textbook production ……………….

V

X

17.

Fringe benefits, materials handling workers ..

V

X

18.

Yarn used in sweater production ………………

V

X

19.

Wages of receptionist, executive offices …….

F

X

* Could be administrative cost.

Solutions Manual, Chapter 2 37

Problem 2-22 (45 minutes)

1. High-low method:

Number of

Scans

Utilities Cost

High level of activity .

150

$4,000

Low level of activity ..

60

2,200

Change ………………..

90

$1,800

Change in cost $1,800

Variable rate: = =$20 per scan

Change in activity 90 scans

Fixed cost:

Total cost at high level of activity ………..

$4,000

Less variable element:

150 scans × $20 per scan ……………….

3,000

Fixed cost element …………………………..

$1,000

Therefore, the cost formula is: Y = $1,000 + $20X.

© The McGraw-Hill Companies, Inc., 2017. All rights reserved.

38 Managerial Accounting for Managers, 4th edition

Problem 2-22 (continued)

3. The high-low estimate of fixed costs is $170.90 lower than the estimate

provided by least-squares regression. The high-low estimate of the

variable cost per unit is $1.82 higher than the estimate provided by

least-squares regression. A straight line that minimized the sum of the

squared errors would intersect the Y-axis at $1,170.90 instead of

$1,000. It would also have a flatter slope because the estimated variable

cost per unit is lower than the high-low method.

Problem 2-23 (45 minutes)

1. High-low method:

Units

Sold

Shipping

Expense

High activity level …………..

20,000

$210,000

Low activity level ……………

10,000

119,000

Change ………………………..

10,000

$91,000

Change in cost

Variable cost per unit = Change in activity

$91,000

= = $9.10 per unit

10,000 units

Fixed cost element:

Total shipping expense at high activity

level ……………………………………………..

$210,000

Less variable element:

20,000 units × $9.10 per unit …………….

182,000

Fixed cost element …………………………….

$ 28,000

40 Managerial Accounting for Managers, 4th edition

Problem 2-23 (continued)

2.

Milden Company

Budgeted Contribution Format Income Statement

For the First Quarter, Year 3

Sales (12,000 units × $100 per unit) ………..

$1,200,000

Variable expenses:

Cost of goods sold

(12,000 units × $35 unit) ………………….

$420,000

Sales commission (6% × $1,200,000) …….

72,000

Shipping expense

(12,000 units × $9.10 per unit) …………..

109,200

Total variable expenses ………………………….

601,200

Contribution margin ………………………………

598,800

Fixed expenses:

Advertising expense …………………………...

210,000

Shipping expense ………………………………

28,000

Administrative salaries ………………………..

145,000

Insurance expense ……………………………..

9,000

Depreciation expense ………………………….

76,000

Total fixed expenses ……………………………..

468,000

Net operating income …………………………...

$ 130,800