Solutions Manual, Chapter 2 21

Exercise 2-13 (20 minutes)

1. Traditional income statement

The Alpine House, Inc.

Traditional Income Statement

Sales ……………………………………………………….

$150,000

Cost of goods sold

($30,000 + $100,000 – $40,000) …………………

90,000

Gross margin ……………………………………………..

60,000

Selling and administrative expenses:

Selling expenses (($50 per unit × 200 pairs of

skis*) + $20,000) …………………………………..

30,000

Administrative expenses (($10 per unit × 200

pairs of skis) + $20,000)………………………….

22,000

52,000

Net operating income ………………………………….

$ 8,000

2. Contribution format income statement

The Alpine House, Inc.

Contribution Format Income Statement

Sales ……………………………………………………….

$150,000

Variable expenses:

Cost of goods sold

($30,000 + $100,000 – $40,000) ………………

$90,000

Selling expenses

($50 per unit × 200 pairs of skis) ………………

10,000

Administrative expenses

($10 per unit × 200 pairs of skis) ………………

2,000

102,000

Contribution margin …………………………………….

48,000

Fixed expenses:

Selling expenses ………………………………………

20,000

Administrative expenses …………………………….

20,000

40,000

Net operating income ………………………………….

$ 8,000

22 Managerial Accounting for Managers, 4th edition

Exercise 2-13 (continued)

2. Since 200 pairs of skis were sold and the contribution margin totaled

Solutions Manual, Chapter 2 23

Exercise 2-14 (30 minutes)

1.

Guest-

Days

Custodial

Supplies

Expense

High activity level (July) ……………

12,000

$13,500

Low activity level (March) …………

4,000

7,500

Change …………………………………

8,000

$ 6,000

Variable cost per guest-day:

Change in expense $6,000

= =$0.75 per guest-day

Change in activity 8,000 guest-days

Fixed cost per month:

Custodial supplies expense at high activity level ….

$13,500

Less variable cost element:

12,000 guest–days × $0.75 per guest-day ……….

9,000

Total fixed cost …………………………………………….

$ 4,500

2. Custodial supplies expense for 11,000 guest-days:

Variable cost:

11,000 guest-days × $0.75 per guest-day .

$ 8,250

Fixed cost …………………………………………..

4,500

Total cost ……………………………………………

$12,750

24 Managerial Accounting for Managers, 4th edition

Exercise 2-14 (continued)

5. Expected custodial supplies expense for 11,000 guest-days:

Variable cost: 11,000 guest–days × $0.77 per day …..

$ 8,470.00

Fixed cost ………………………………………………………

3,973.10

Total cost ……………………………………………………….

$12,443.10

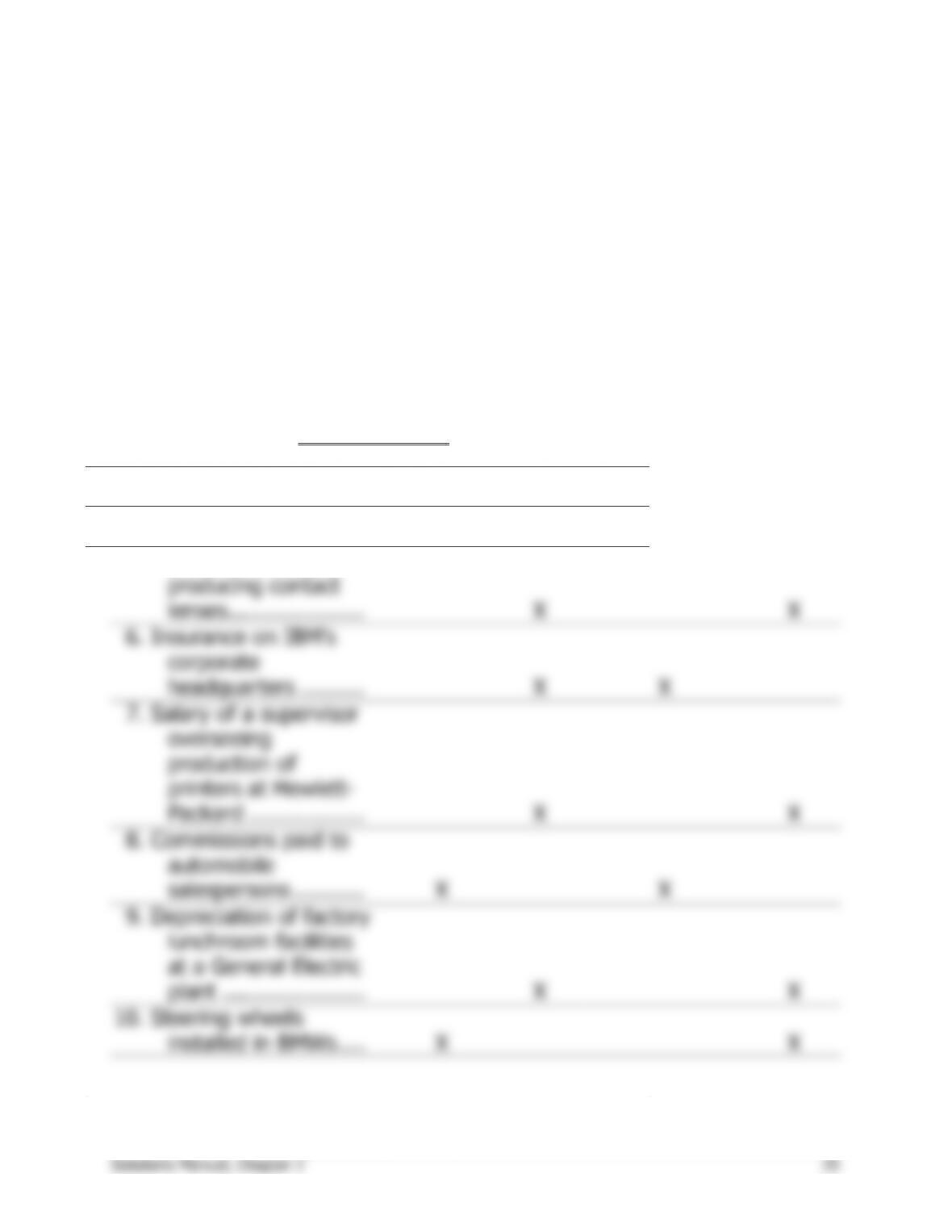

Exercise 2-15 (15 minutes)

Selling and

Cost Behavior

Administrative

Product

Cost Item

Variable

Fixed

Cost

Cost

1.

Hamburger buns at a

Wendy’s outlet ……..

X

X

2.

Advertising by a dental

office ………………….

X

X

3.

Apples processed and

canned by Del Monte

X

X

4.

Shipping canned

apples from a Del

Monte plant to

customers ……………

X

X

5.

Insurance on a Bausch

& Lomb factory

producing contact

lenses …………………

X

X

6.

Insurance on IBM’s

corporate

headquarters ……….

X

X

7.

Salary of a supervisor

overseeing

production of

printers at Hewlett-

Packard ………………

X

X

8.

Commissions paid to

automobile

salespersons ………..

X

X

9.

Depreciation of factory

lunchroom facilities

at a General Electric

plant ………………….

X

X

10.

Steering wheels

installed in BMWs ….

X

X

Problem 2-16 (45 minutes)

1.

Cost of goods sold ……………….

Variable

Advertising expense …………….

Fixed

Shipping expense ………………..

Mixed

Salaries and commissions ……..

Mixed

Insurance expense ………………

Fixed

Depreciation expense …………..

Fixed

2. Analysis of the mixed expenses:

Units

Shipping

Expense

Salaries and

Commissions

Expense

High level of activity …..

5,000

$38,000

$90,000

Low level of activity ……

4,000

34,000

78,000

Change ……………………

1,000

$ 4,000

$12,000

Variable cost element:

Change in cost

Variable rate = Change in activity

$4,000

Shipping expense: = $4 per unit

1,000 units

$12,000

Salaries and commissions expense: = $12 per unit

1,000 units

Fixed cost element:

Shipping

Expense

Salaries and

Commissions

Expense

Cost at high level of activity ….

$38,000

$90,000

Less variable cost element:

5,000 units × $4 per unit …..

20,000

5,000 units × $12 per unit …

60,000

Fixed cost element ……………..

$18,000

$30,000

Solutions Manual, Chapter 2 27

Problem 2-16 (continued)

The cost formulas are:

Shipping expense:

3.

Morrisey & Brown, Ltd.

Income Statement

For the Month Ended September 30

Sales (5,000 units × $100 per unit) ………..

$500,000

Variable expenses:

Cost of goods sold

(5,000 units × $60 per unit) ……………

$300,000

Shipping expense

(5,000 units × $4 per unit) ………………

20,000

Salaries and commissions expense

(5,000 units × $12 per unit) …………….

60,000

380,000

Contribution margin …………………………….

120,000

Fixed expenses:

Advertising expense ………………………….

21,000

Shipping expense …………………………….

18,000

Salaries and commissions expense ……….

30,000

Insurance expense …………………………...

6,000

Depreciation expense ………………………..

15,000

90,000

Net operating income ………………………….

$ 30,000

28 Managerial Accounting for Managers, 4th edition

Problem 2-17 (30 minutes)

isolated as follows:

Level of Activity

50,000 DLHs

75,000 DLHs

Total factory overhead cost ……………..

$14,250,000

$17,625,000

Deduct:

Indirect materials @ $100 per DLH* .

5,000,000

7,500,000

Rent …………………………………………

6,000,000

6,000,000

Maintenance cost ………………………….

$ 3,250,000

$ 4,125,000

* $5,000,000 ÷ 50,000 DLHs = $100 per DLH

2. High-low analysis of maintenance cost:

Direct

Labor-Hours

Maintenance

Cost

High level of activity ……..

75,000

$4,125,000

Low level of activity ………

50,000

3,250,000

Change ………………………

25,000

$ 875,000

Variable cost element:

Change in cost $875,000

= =$35 per DLH

Change in activity 25,000 DLH

Fixed cost element:

Total cost at the high level of activity ………………

$4,125,000

Less variable cost element

(75,000 DLHs × $35 per DLH) …………………….

2,625,000

Fixed cost element ……………………………………..

$1,500,000

$35 per direct labor-hour or

Solutions Manual, Chapter 2 29

Problem 2-17 (continued)

3. Total factory overhead cost at 70,000 direct labor-hours is:

Indirect materials

(70,000 DLHs × $100 per DLH) …………

$ 7,000,000

Rent ………………………………………………

6,000,000

Maintenance:

Variable cost element

(70,000 DLHs × $35 per DLH) ………..

$2,450,000

Fixed cost element ………………………….

1,500,000

3,950,000

Total factory overhead cost …………………

$16,950,000

30 Managerial Accounting for Managers, 4th edition

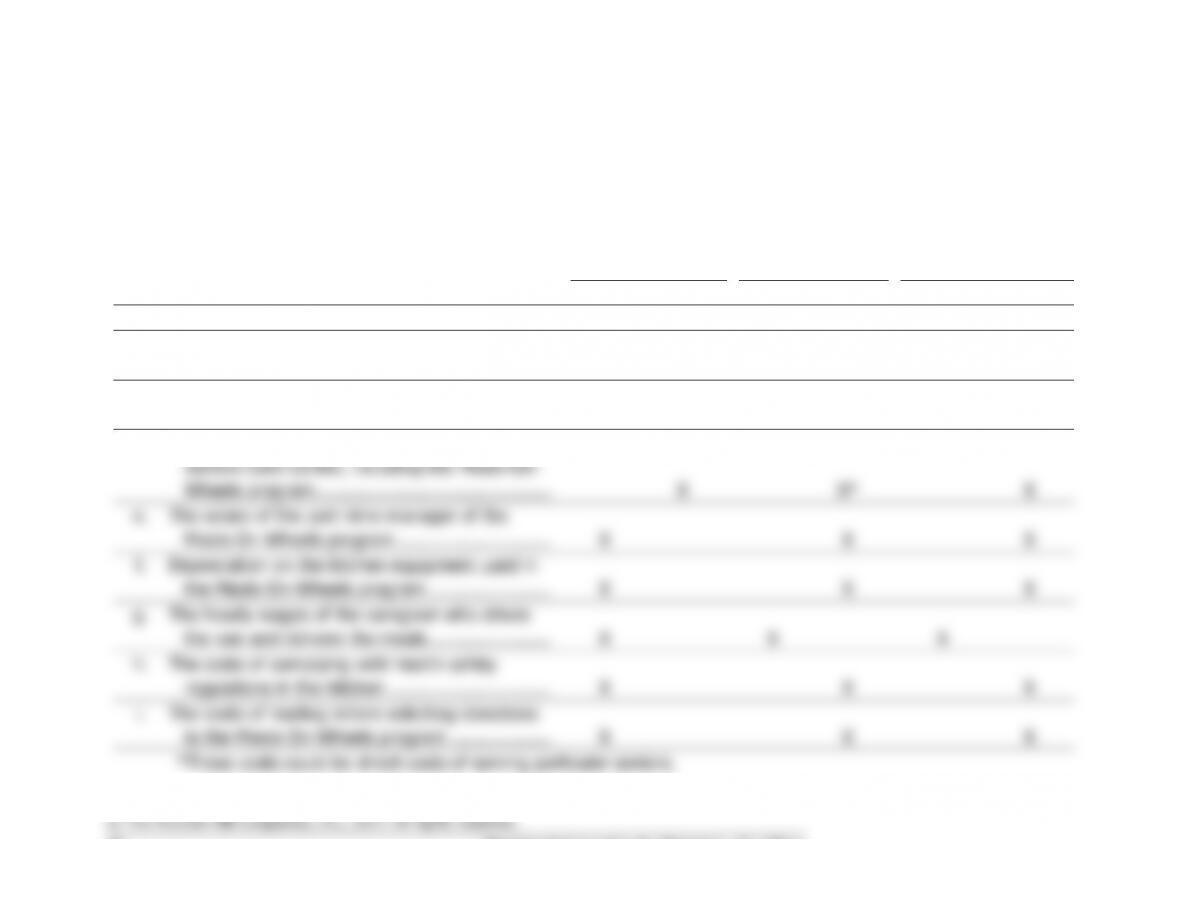

Problem 2-18 (20 minutes)

Direct or Indirect

Cost of the Meals-

On-Wheels

Program

Direct or Indirect

Cost of Particular

Seniors Served

by the Meals-On–

Wheels Program

Variable or Fixed

with Respect to the

Number of Seniors

Served by the

Meals-On-Wheels

Program

Item

Description

Direct

Indirect

Direct

Indirect

Variable

Fixed

a.

The cost of leasing the Meals-On-Wheels van…..

X

X

X

b.

The cost of incidental supplies such as salt,

pepper, napkins, and so on ……………………….

X

X*

X

c.

The cost of gasoline consumed by the Meals-On-

Wheels van ……………………………………………

X

X

X

d.

The rent on the facility that houses Madison

Seniors Care Center, including the Meals-On-

Wheels program ……………………………………..

X

X*

X

e.

The salary of the part-time manager of the

Meals-On-Wheels program ………………………..

X

X

X

f.

Depreciation on the kitchen equipment used in

the Meals-On-Wheels program …………………..

X

X

X

g.

The hourly wages of the caregiver who drives

the van and delivers the meals …………………..

X

X

X

h.

The costs of complying with health safety

regulations in the kitchen ………………………….

X

X

X

i.

The costs of mailing letters soliciting donations

to the Meals-On-Wheels program ……………….

X

X

X

*These costs could be direct costs of serving particular seniors.