Problem 12-16 (continued)

3. Students’ answers may differ in some details from this solution.

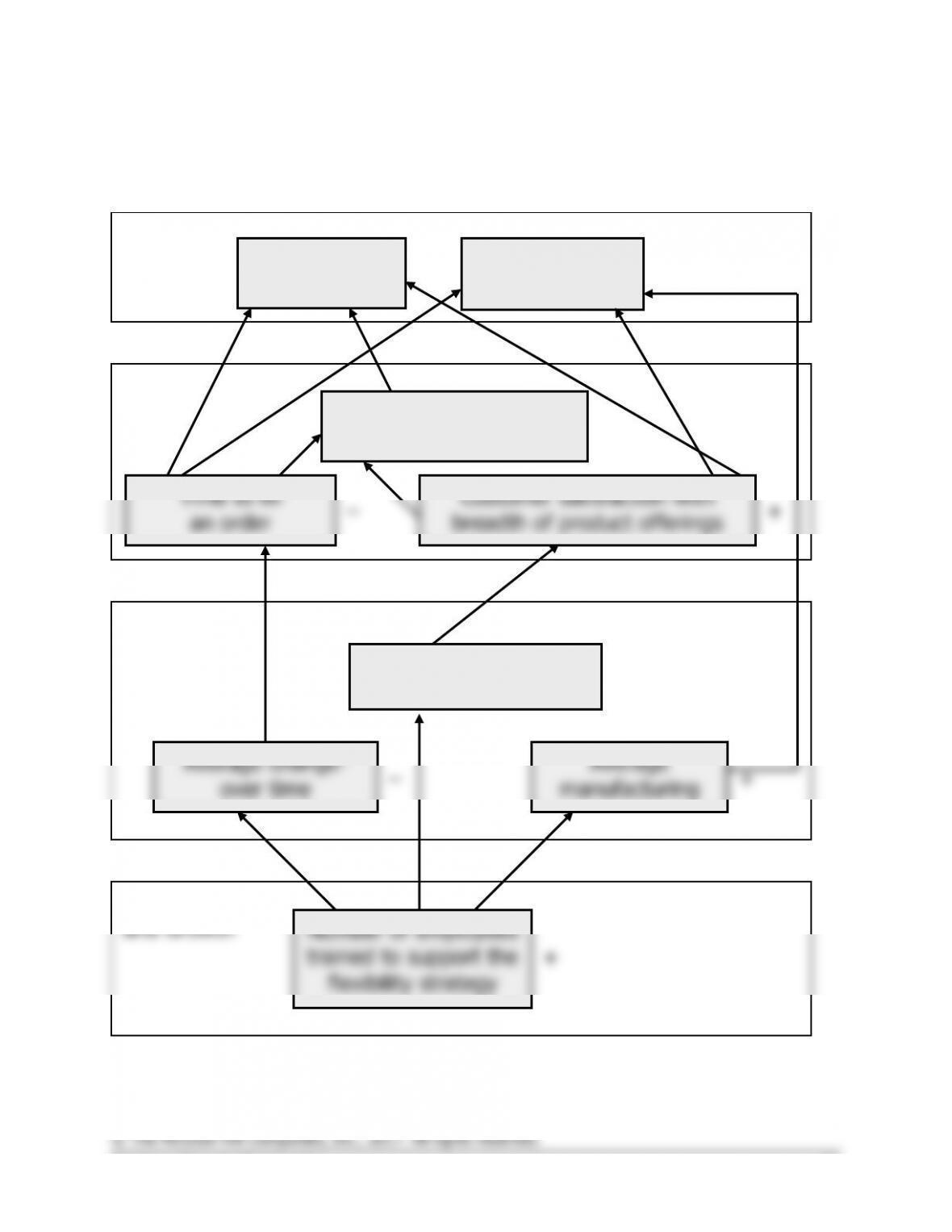

Sales

Contribution

margin per ton

Financial

Time to fill

an order

Customer satisfaction with

breadth of product offerings

Number of new

customers acquired

Customer

Average change-

over time

Number of different

paper grades produced

Average

manufacturing

Internal

Business

Processes

Number of employees

trained to support the

flexibility strategy

Learning

and Growth

+

–

+

+

–

+

+

+

+

32 Managerial Accounting for Managers, 4th Edition

Problem 12-16 (continued)

4. The hypotheses underlying the balanced scorecard are indicated by the

arrows in the diagram. Reading from the bottom of the balanced

scorecard, the hypotheses are:

° If the number of employees trained to support the flexibility strategy

° If the average changeover time decreases, then the time to fill an

order will decrease.

° If the average manufacturing yield increases, then the contribution

margin per ton will increase.

° If the time to fill an order decreases, then the number of new

° If the customer satisfaction with breadth of product offerings

° If the number of new customers acquired increases, then sales will

increase.

Each of these hypotheses can be questioned. For example, the time to

product diversity, smaller batch sizes, and more frequent shipments.

The fact that each of the hypotheses mentioned above can be

accordingly.

Solutions Manual, Chapter 12 33

Problem 12-17 (30 minutes)

1. Breaking the ROI computation into two separate elements reveals

important relationships that otherwise might remain hidden. First, the

breaking the ROI computation into margin and turnover elements

stresses the possibility of trading one off for the other in attempts to

comparisons between segments of the organization.

2. The missing information is as follows:

Companies in the Same Industry

A

B

C

Sales ………………………………

$600,000

*

$500,000

*

$2,000,000

Net operating income …………

$84,000

*

$70,000

*

$70,000

Average operating assets …….

$300,000

*

$1,000,000

$1,000,000

*

Margin …………………………….

14%

14%

3.5%

*

Turnover ………………………….

2.0

0.5

2.0

*

Return on investment (ROI) …

28%

7%

*

7%

*Given.

NAA Report No. 35

states (p. 35):

Company B supports only fifty cents in sales each period. This suggests

that the analyst should look carefully at Company B’s investment. Is the

company keeping an inventory larger than necessary for its sales

volume? Are receivables being collected promptly? Or did Company A

34 Managerial Accounting for Managers, 4th Edition

Problem 12-17 (continued)

Thus, by including sales specifically in ROI computations the manager is

or is it due to other factors? ROI computations raise questions such as

these, which form the basis for managerial action.

To summarize, in order to bring B’s ROI into line with A’s, it seems

operating expenses.

Solutions Manual, Chapter 12 35

Problem 12-18 (30 minutes)

1.

Present

New Line

Total

(1)

Sales ……………………..

$10,000,000

$2,000,000

$12,000,000

(2)

Net operating income ..

$800,000

$160,000

*

$960,000

(3)

Operating assets ………

$4,000,000

$1,000,000

$5,000,000

(4)

Margin (2) ÷ (1) ………

8%

8%

8%

(5)

Turnover (1) ÷ (3) ……

2.5

2.0

2.4

(6)

ROI (4) × (5) ………….

20.0%

16.0%

19.2%

*

Sales …………………………………………………

$2,000,000

Variable expenses (60% × $2,000,000) …….

1,200,000

Contribution margin ………………………………

800,000

Fixed expenses …………………………………….

640,000

Net operating income…………………………….

$ 160,000

2. Dell Havasi will be inclined to reject the new product line because

increase the company’s overall ROI.

4.

a.

Present

New Line

Total

Operating assets …………………

$4,000,000

$1,000,000

$5,000,000

Minimum return required ………

× 12%

× 12%

× 12%

Minimum net operating

income …………………………..

$ 480,000

$ 120,000

$ 600,000

Actual net operating income ….

$ 800,000

$ 160,000

$ 960,000

Minimum net operating

income (above) ………………..

480,000

120,000

600,000

Residual income ………………….

$ 320,000

$ 40,000

$ 360,000

above.

36 Managerial Accounting for Managers, 4th Edition

Problem 12-19 (30 minutes)

1. a., b., and c.

Month

1

2

3

4

Throughput time in days:

Process time …………………………….

2.1

2.0

1.9

1.8

Inspection time …………………………

0.8

0.7

0.7

0.7

Move time ……………………………….

0.3

0.4

0.4

0.5

Queue time during production ……..

2.8

4.4

6.0

7.0

Total throughput time …………………

6.0

7.5

9.0

10.0

Manufacturing cycle efficiency (MCE):

Process time ÷ Throughput time …..

35.0%

26.7%

21.1%

18.0%

Delivery cycle time in days:

Wait time to start of production ……

9.0

11.5

12.0

14.0

Throughput time ……………………….

6.0

7.5

9.0

10.0

Total delivery cycle time ……………..

15.0

19.0

21.0

24.0

2. a. Areas where the company is improving:

Quality control.

The number of defects has decreased by over 50% in

significantly improved.

Material control.

The purchase order lead time is only half of what it

was four months ago, which indicates that purchases are arriving in

JIT purchasing.

to 1.8 days over the last four months.

Solutions Manual, Chapter 12 37

Problem 12-19 (continued)

b. Areas of deterioration:

the last four months.

Machine performance.

Machine downtime has doubled over the last

four months. This may be a result of the greater setup time, or it may

declining rapidly.

3. a. and b.

Month

5

6

Throughput time in days:

Process time ……………………………………

1.8

1.8

Inspection time ………………………………..

0.7

0.0

Move time ………………………………………

0.5

0.5

Queue time during production …………….

0.0

0.0

Total throughput time ……………………….

3.0

2.3

Manufacturing cycle efficiency (MCE):

Process time ÷ Throughput time………….

60.0%

78.3%

Problem 12-20 (continued)

Sales (1.20 × $4,000,000) …..

$4,800,000

100

%

Variable expenses ………………

3,360,000

70

Contribution margin ……………

1,440,000

30

%

Fixed expenses …………………

840,000

Net operating income …………

$ 600,000

$600,000 $4,800,000

ROI = ×

$4,800,000 $2,000,000

= 12.5% × 2.4 = 30%

(Increase) (Increase) (Increase)

6.

$320,000 $4,000,000

ROI = ×

$4,000,000 $1,960,000

= 8% × 2.04 = 16.3%

(Decrease) (Increase) (Decrease)

7.

$360,000 $4,000,000

ROI = ×

$4,000,000 $1,800,000

= 9% × 2.22 = 20%

(Unchanged) (Increase) (Increase)

© The McGraw-Hill Companies, Inc., 2017. All rights reserved.

40 Managerial Accounting for Managers, 4th Edition

a service-focused company. Applied Pharmaceuticals’ training resources

organization. Applied Pharmaceuticals’ technology investments are

defect from an external customer interaction standpoint.