Solutions Manual, Chapter 12 11

Exercise 12-4 (continued)

3. Management will be able to tell if a hypothesis is false if an

improvement in a performance measure at the bottom of an arrow does

particular hypothesis.

12 Managerial Accounting for Managers, 4th Edition

Exercise 12-5 (15 minutes)

Division

Alpha

Bravo

Charlie

Sales……………………………..

$4,000,000

$11,500,000

*

$3,000,000

Net operating income ………..

$160,000

$920,000

*

$210,000

*

Average operating assets …..

$800,000

*

$4,600,000

$1,500,000

Margin …………………………..

4%*

8%

7%*

Turnover ………………………..

5*

2.5

2

Return on investment (ROI) .

20%

20%*

14%*

turnover, whereas Division Bravo has just the opposite.

*Given.

Solutions Manual, Chapter 12 13

Exercise 12-6 (20 minutes)

1. ROI computations:

Net operating income Sales

ROI = ×

Sales Average operating assets

Osaka Division:

$210,000 $3,000,000

ROI = × = 7% × 3 = 21%

$3,000,000 $1,000,000

Yokohama Division:

$720,000 $9,000,000

ROI = × = 8% × 2.25 = 18%

$9,000,000 $4,000,000

2.

Osaka

Yokohama

Average operating assets (a)………………….

$1,000,000

$4,000,000

Net operating income …………………………..

$210,000

$720,000

Minimum required return on average

operating assets: 15% × (a) ……………….

150,000

600,000

Residual income ………………………………….

$ 60,000

$120,000

3. No, the Yokohama Division is simply larger than the Osaka Division and

for this reason one would expect that it would have a greater amount of

for Osaka.

Exercise 12-7 (45 minutes)

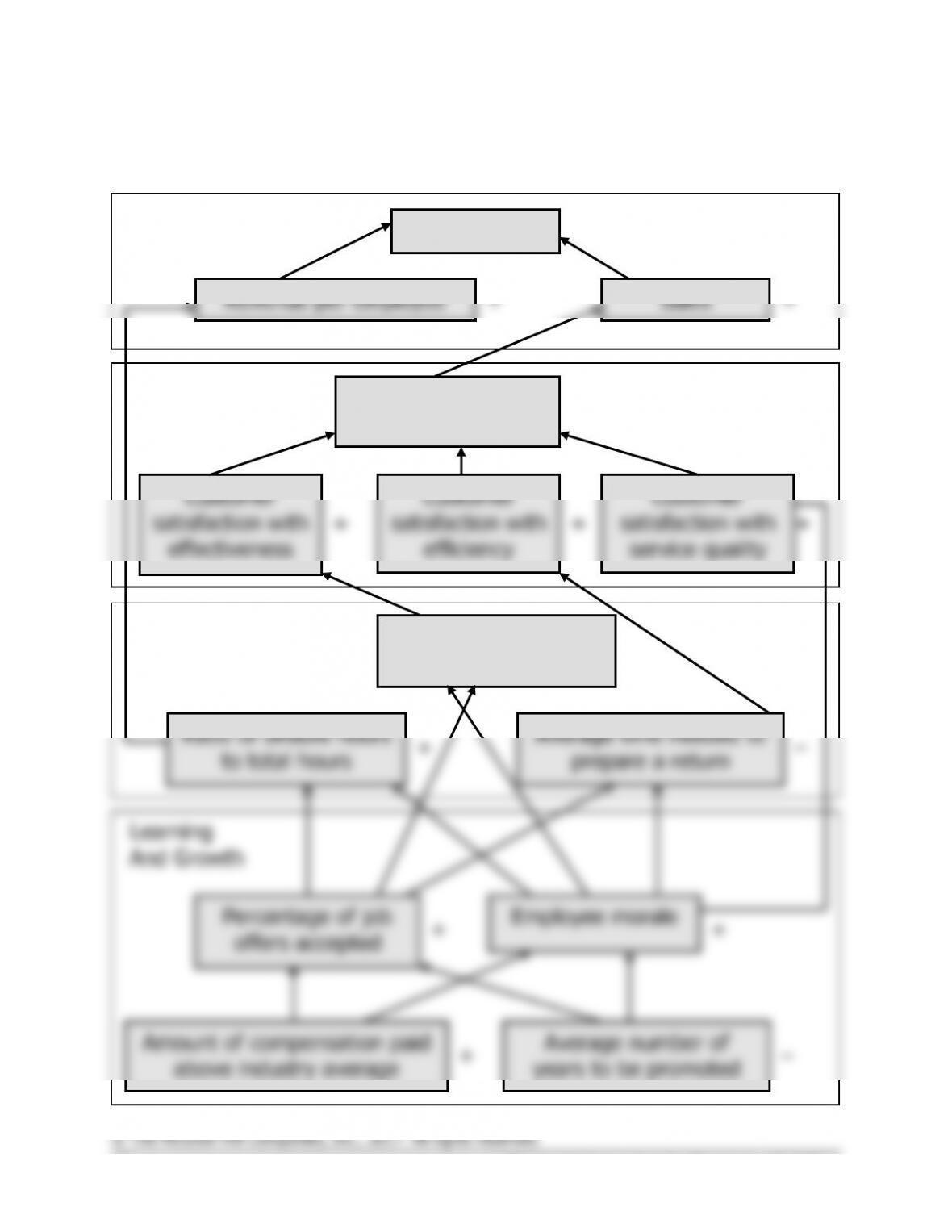

1. Students’ answers may differ in some details from this solution.

Revenue per employee

Sales

Profit margin

Financial

Ratio of billable hours

to total hours

Average number of

errors per tax return

Average time needed to

prepare a return

Percentage of job

offers accepted

Employee morale

Amount of compensation paid

above industry average

Average number of

years to be promoted

Customer

Internal Business

Processes

Learning

And Growth

+

–

+

+

+

–

Customer

satisfaction with

effectiveness

Customer

satisfaction with

efficiency

Customer

satisfaction with

service quality

Number of new

customers acquired

+

+

+

+

+

+

+

–

Solutions Manual, Chapter 12 15

Exercise 12-7 (continued)

2. The hypotheses underlying the balanced scorecard are indicated by the

arrows in the diagram. Reading from the bottom of the balanced

scorecard, the hypotheses are:

° If the amount of compensation paid above the industry average

° If the average number of years to be promoted decreases, then the

percentage of job offers accepted and the level of employee morale

will increase.

° If the percentage of job offers accepted increases, then the ratio of

prepare a return should decrease.

decrease.

° If employee morale increases, then the customer satisfaction with

service quality should increase.

per employee should increase.

customer satisfaction with efficiency should increase.

° If the customer satisfaction with effectiveness, efficiency, and service

should increase.

° If revenue per employee and sales increase, then the profit margin

should increase.

16 Managerial Accounting for Managers, 4th Edition

Exercise 12-7 (continued)

decline would probably puzzle Ariel because, although the firm prepared

what it believed to be error-free returns, it overlooked opportunities to

minimize customers’ taxes. In this example, Ariel’s internal business

process measure of the average number of errors per tax return does

accordingly.

3. The performance measure “total dollar amount of tax refunds

generated” would motivate Ariel’s employees to aggressively search for

customers. Overall, it would probably be unwise to use this performance

measure in Ariel’s scorecard.

opportunities.

Solutions Manual, Chapter 12 17

Exercise 12-7 (continued)

4. Each office’s individual performance should be based on the scorecard

measures only if the measures are controllable by those employed at

typically made at the branch offices. On the other hand, it would make

sense to measure the branch offices with respect to internal business

each office.

18 Managerial Accounting for Managers, 4th Edition

Exercise 12-8 (15 minutes)

1. ROI computations:

Net operating income Sales

ROI = ×

Sales Average operating assets

Queensland Division:

$360,000 $4,000,000

ROI = × = 9% × 2 = 18%

$4,000,000 $2,000,000

New South Wales Division:

$420,000 $7,000,000

ROI = × = 6% × 3.5 = 21%

$7,000,000 $2,000,000

2. The manager of the New South Wales Division seems to be doing the

better job. Although her margin is three percentage points lower than

the margin of the Queensland Division, her turnover is higher (a

division.

Notice that if you look at margin alone, then the Queensland Division

appears to be the stronger division. This fact underscores the

Solutions Manual, Chapter 12 19

Exercise 12-9 (15 minutes)

Company A

Company B

Company C

Sales ………………………………….

$9,000,000

*

$7,000,000

*

$4,500,000

*

Net operating income …………….

$540,000

$280,000

*

$360,000

Average operating assets ………..

$3,000,000

*

$2,000,000

$1,800,000

*

Return on investment (ROI) …….

18%*

14%*

20%

Minimum required rate of return:

Percentage ………………………..

16%*

16%

15%*

Dollar amount …………………….

$480,000

$320,000

*

$270,000

Residual income ……………………

$60,000

$(40,000)

$90,000

*

*Given.

20 Managerial Accounting for Managers, 4th Edition

Exercise 12-10 (20 minutes)

1.

(b)

(c)

Net

Average

(a)

Operating

Operating

ROI

Sales

Income*

Assets

(b) ÷ (c)

$2,500,000

$475,000

$1,000,000

47.5%

$2,600,000

$500,000

$1,000,000

50.0%

$2,700,000

$525,000

$1,000,000

52.5%

$2,800,000

$550,000

$1,000,000

55.0%

$2,900,000

$575,000

$1,000,000

57.5%

$3,000,000

$600,000

$1,000,000

60.0%

*Sales × Contribution Margin Ratio – Fixed Expenses

company’s ROI of 2.5%.

Increase in sales ……………………………………………

$100,000

(a)

Contribution margin ratio …………………………………

25%

(b)

Increase in contribution margin and net operating

income (a) × (b) …………………………………………

$25,000

(c)

Average operating assets…………………………………

$1,000,000

(d)

Increase in return on investment (c) ÷ (d) ………….

2.5%