Solutions Manual, Appendix 11A 67

Problem 11A-11 (continued)

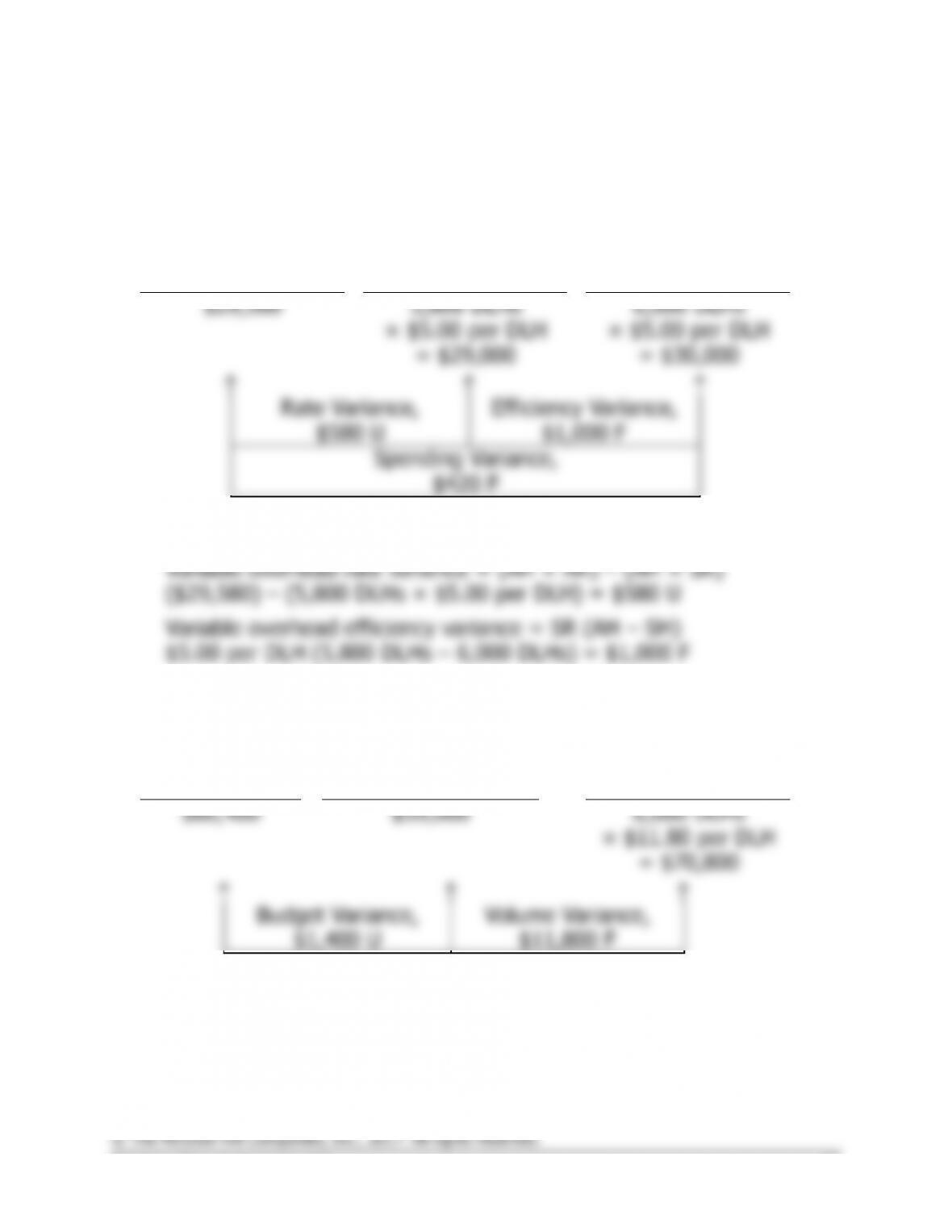

3. Variable overhead variances:

Actual DLHs of

Input, at the

Actual Rate

Actual DLHs of

Input, at the

Standard Rate

Standard DLHs

Allowed for Output,

at the Standard Rate

(AH × AR)

(AH × SR)

(SH × SR)

$29,580

5,800 DLHs

× $5.00 per DLH

6,000 DLHs

× $5.00 per DLH

= $29,000

= $30,000

Rate Variance,

$580 U

Efficiency Variance,

$1,000 F

Spending Variance,

$420 F

Alternative solution for the variable overhead variances:

Fixed overhead variances:

Actual Fixed

Overhead

Budgeted Fixed

Overhead

Fixed Overhead

Applied to

Work in Process

$60,400

$59,000

6,000 DLHs

× $11.80 per DLH

= $70,800

Budget Variance,

$1,400 U

Volume Variance,

$11,800 F

Problem 11A-11 (continued)

Alternative approach to the budget variance:

Budget Actual fixed Budgeted fixed

= –

variance overhead overhead

= $60,400 – $59,000

= $1,400 U

Alternative approach to the volume variance:

æö

÷

ç÷

ç÷

ç÷

ç÷

÷

ç

èø

´

Fixed portion of Standard

Volume Denominator

= the predetermined – hours

Variance hours

overhead rate allowed

= $11.80 per DLH (5,000 DLHs – 6,000 DLHs)

= $11,800 F

4. The choice of a denominator activity level affects standard unit costs in

rises.

The volume variance cannot be controlled by controlling spending. The

volume variance simply reflects whether actual activity was greater than

Solutions Manual, Appendix 11A 69

Problem 11A–12 (45 minutes)

1.

and 2.

Per Direct Labor-Hour

Variable

Fixed

Total

Denominator of 30,000 DLHs:

$135,000 ÷ 30,000 DLHs ……………..

$4.50

$ 4.50

$270,000 ÷ 30,000 DLHs ……………..

$9.00

9.00

Total predetermined rate ………………..

$13.50

Denominator of 40,000 DLHs:

$180,000 ÷ 40,000 DLHs ……………..

$4.50

$ 4.50

$270,000 ÷ 40,000 DLHs ……………..

$6.75

6.75

Total predetermined rate ………………..

$11.25

3.

Denominator Activity:

30,000 DLHs

Denominator Activity:

40,000 DLHs

Direct materials, 4 feet ×

$8.75 per foot ……………

$35.00

Same ………………………

$35.00

Direct labor, 2 DLHs ×

$15 per DLH ……………..

30.00

Same ………………………

30.00

Variable overhead, 2

DLHs × $4.50 per DLH ..

9.00

Same ………………………

9.00

Fixed overhead, 2 DLHs ×

$9.00 per DLH …………..

18.00

Fixed overhead, 2 DLHs

× $6.75 per DLH ……..

13.50

Standard cost per unit …..

$92.00

Standard cost per unit ..

$87.50

b.

Manufacturing Overhead

Actual costs

446,400

Applied costs

486,000

*

Overapplied

overhead

39,600

70 Managerial Accounting for Managers, 4th Edition

Problem 11A-12 (continued)

c. Variable overhead variances:

Actual DLHs of

Input, at the

Actual Rate

Actual DLHs of

Input, at the

Standard Rate

Standard DLHs

Allowed for Output,

at the Standard Rate

(AH × AR)

(AH × SR)

(SH × SR)

$174,800

38,000 DLHs ×

$4.50 per DLH

36,000 DLHs ×

$4.50 per DLH

= $171,000

= $162,000

Rate Variance,

$3,800 U

Efficiency Variance,

$9,000 U

Alternative solution:

Variable overhead rate variance = (AH × AR) – (AH × SR)

Fixed overhead variances:

Actual Fixed

Overhead

Budgeted Fixed

Overhead

Fixed Overhead Applied to

Work in Process

$271,600

$270,000*

36,000 DLHs × $9 per DLH

= $324,000

Budget Variance,

$1,600 U

Volume Variance,

$54,000 F

Problem 11A-12 (continued)

Alternative solution:

Budget variance:

Budget Actual fixed Budgeted fixed

= –

variance overhead overhead

= $271,600 – $270,000

= $1,600 U

Volume variance:

æö

÷

ç÷

ç÷

ç÷

ç÷

÷

ç

èø

´

Fixed portion of Standard

Volume Denominator

= the predetermined – hours

Variance hours

overhead rate allowed

= $9.00 per DLH (30,000 DLHs – 36,000 DLHs)

= $54,000 F

Summary of variances:

Variable overhead rate variance …………….

$ 3,800

U

Variable overhead efficiency variance ……..

9,000

U

Fixed overhead budget variance …………….

1,600

U

Fixed overhead volume variance ……………

54,000

F

Overapplied overhead …………………………

$39,600

F

72 Managerial Accounting for Managers, 4th Edition

Problem 11A–12 (continued)

5. The major disadvantage of using normal activity is the large volume

favorable volume variance that may be difficult for management to

interpret. In addition, the large favorable volume variance in this case

On the other hand, using long-run normal activity as the denominator