Exercise 11A-2 (continued)

3. Variable overhead rate variance:

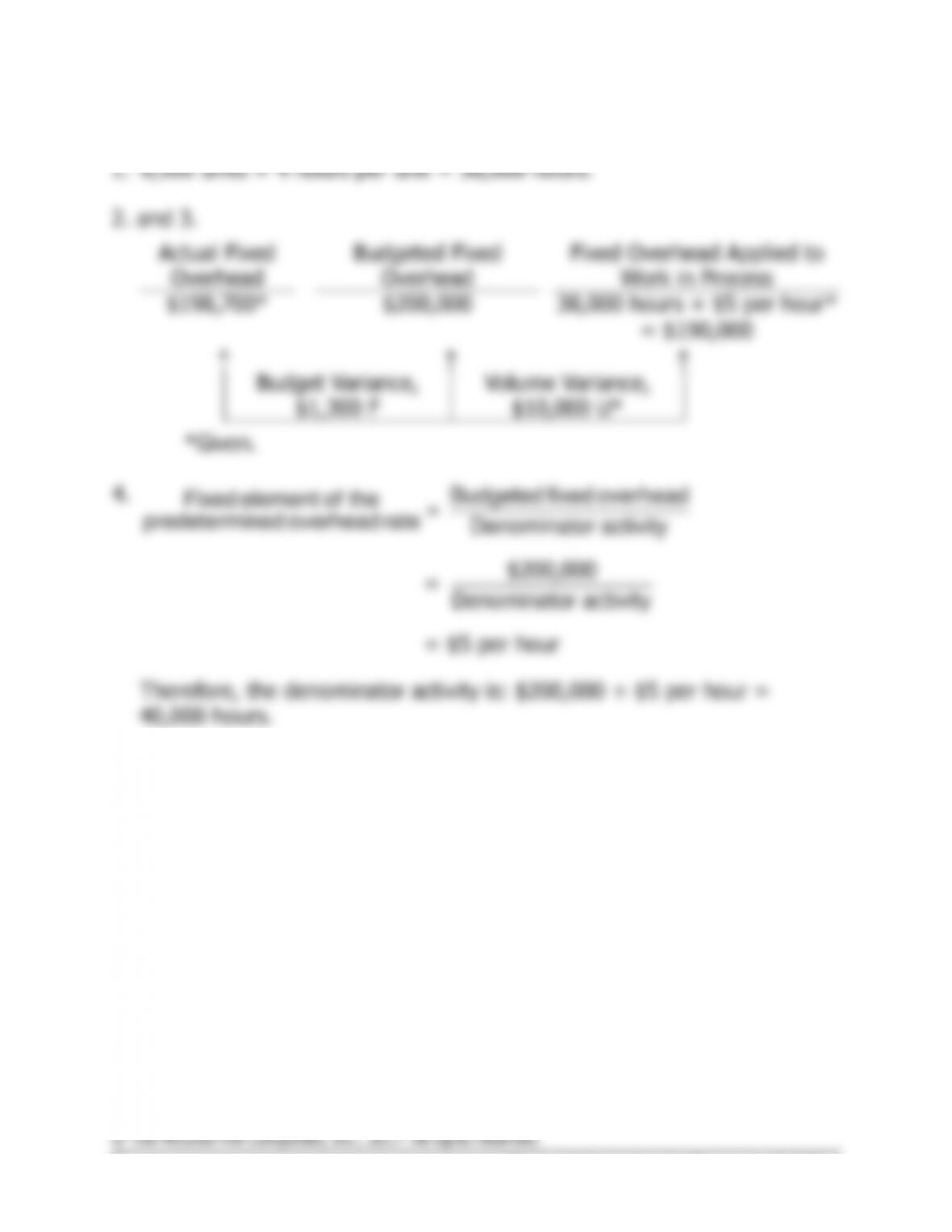

Exercise 11A–3 (15 minutes)

1. The total overhead cost at the denominator level of activity must be

determined before the predetermined overhead rate can be computed.

Total fixed overhead cost per year …………………………...

$250,000

Total variable overhead cost

($2 per DLH × 40,000 DLHs) ………………………………..

80,000

Total overhead cost at the denominator level of activity ..

$330,000

Overhead at the denominator level of activity

Predetermined =

overhead rate Denominator level of activity

$330,000

= = $8.25 per DLH

40,000 DLHs

2.

Standard direct labor-hours allowed for

the actual output (a) ………………………

38,000

DLHs

Predetermined overhead rate (b) ………..

$8.25

per DLH

Overhead applied (a) × (b) ………………..

$313,500

Solutions Manual, Appendix 11A 53

Exercise 11A-4 (10 minutes)

Company A:

This company has a favorable volume variance because the

standard hours allowed for the actual production are greater

than the denominator hours.

Company B:

This company has an unfavorable volume variance because

the standard hours allowed for the actual production are less

than the denominator hours.

Company C:

This company has no volume variance because the standard

hours allowed for the actual production and the denominator

hours are the same.

54 Managerial Accounting for Managers, 4th Edition

Exercise 11A-5 (15 minutes)

Solutions Manual, Appendix 11A 55

2.

Direct materials, 2.5 yards × $8.60 per yard ………………….

$21.50

Direct labor, 3 DLHs* × $12.00 per DLH ……………………….

36.00

Variable manufacturing overhead, 3 DLHs × $1.90 per DLH

5.70

Fixed manufacturing overhead, 3 DLHs × $5.60 per DLH ….

16.80

Total standard cost per unit ……………………………………….

$80.00

*30,000 DLHs ÷ 10,000 units = 3 DLHs per unit.

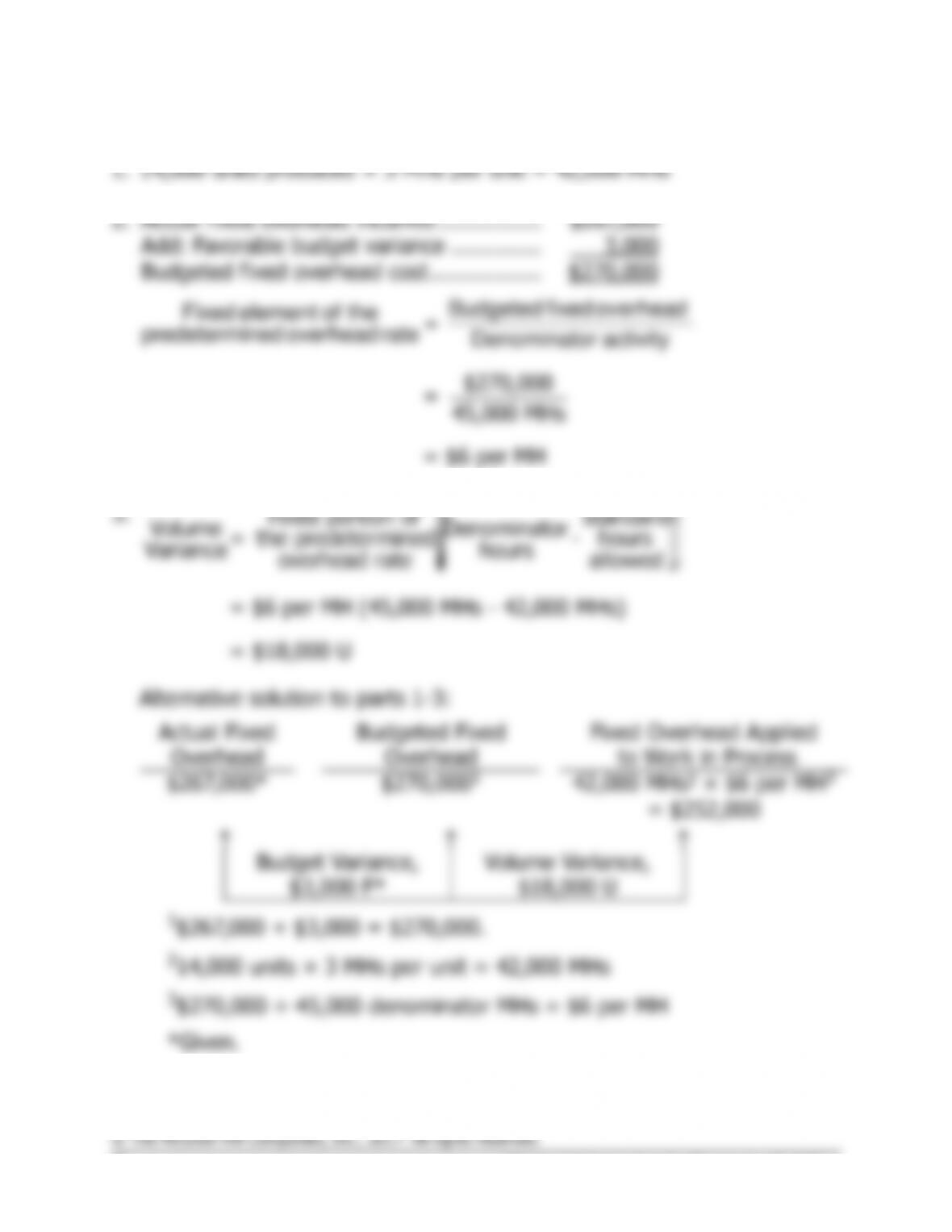

Exercise 11A-7 (15 minutes)

2.

Actual fixed overhead incurred …………….

$267,000

Add: Favorable budget variance …………..

3,000

Budgeted fixed overhead cost ……………..

$270,000

$270,000

= 45,000 MHs

= $6 per MH

Budgeted fixed overhead

Fixed element of the =

predetermined overhead rate Denominator activity

3.

Fixed portion of Standard

Volume Denominator

= the predetermined – hours

Variance hours

overhead rate allowed

= $6 per MH (45,000 MHs – 42,000 MHs)

= $18,000 U

æö

÷

ç÷

ç÷

ç÷

ç÷

ç

èø

Alternative solution to parts 1-3:

Actual Fixed

Overhead

Budgeted Fixed

Overhead

Fixed Overhead Applied

to Work in Process

$267,000*

$270,0001

42,000 MHs2 × $6 per MH3

= $252,000

Budget Variance,

$3,000 F*

Volume Variance,

$18,000 U

1$267,000 + $3,000 = $270,000.

214,000 units × 3 MHs per unit = 42,000 MHs

3$270,000 ÷ 45,000 denominator MHs = $6 per MH

*Given.

Solutions Manual, Appendix 11A 57

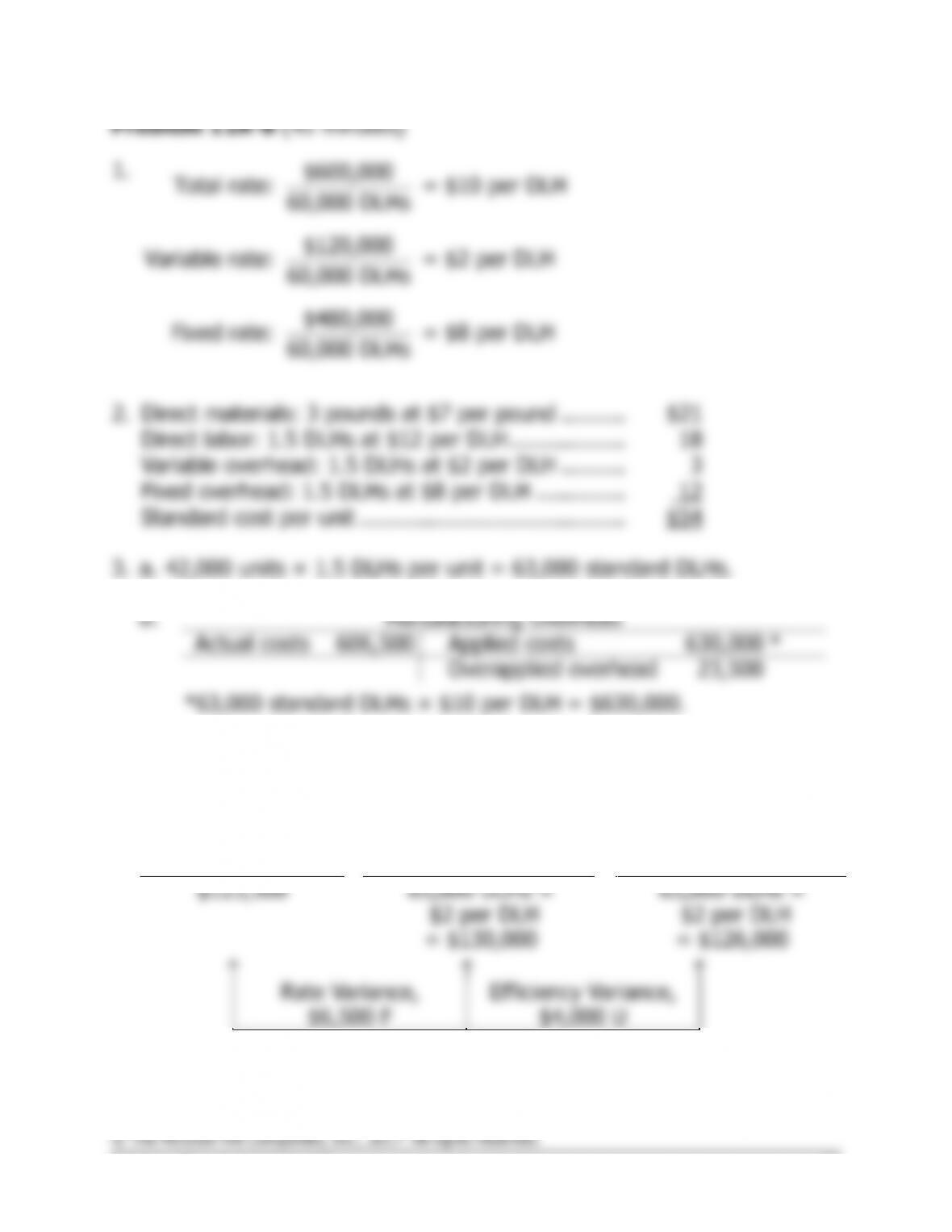

Direct labor: 1.5 DLHs at $12 per DLH ………………

Variable overhead: 1.5 DLHs at $2 per DLH ……….

Fixed overhead: 1.5 DLHs at $8 per DLH …………..

Standard cost per unit …………………………………..

b.

Manufacturing Overhead

Actual costs

606,500

Applied costs

630,000

*

Overapplied overhead

23,500

*63,000 standard DLHs × $10 per DLH = $630,000.

4. Variable overhead variances:

Actual Hours of

Input, at the

Actual Rate

Actual Hours of Input,

at the Standard Rate

Standard Hours

Allowed for Output, at

the Standard Rate

(AH × AR)

(AH × SR)

(SH × SR)

$123,500

65,000 DLHs ×

$2 per DLH

63,000 DLHs ×

$2 per DLH

= $130,000

= $126,000

Rate Variance,

$6,500 F

Efficiency Variance,

$4,000 U

Problem 11A-8 (continued)

Alternative solution:

Variable overhead rate variance = (AH × AR) – (AH × SR)

Fixed overhead variances:

Actual Fixed

Overhead

Budgeted Fixed

Overhead

Fixed Overhead

Applied to Work in Process

$483,000

$480,000*

63,000 DLHs × $8 per DLH

= $504,000

Budget Variance,

$3,000 U

Volume Variance,

$24,000 F

Alternative solution:

Budget variance:

Budget Actual fixed Budgeted fixed

= –

variance overhead overhead

= $483,000 – $480,000

= $3,000 U

Volume variance:

æö

÷

ç÷

ç÷

ç÷

ç÷

÷

ç

èø

´

Fixed portion of Standard

Volume Denominator

= the predetermined – hours

Variance hours

overhead rate allowed

= $8 per DLH (60,000 DLHs – 63,000 DLHs)

= $24,000 F

Solutions Manual, Appendix 11A 59

Problem 11A-8 (continued)

The company’s overhead variances can be summarized as follows:

Variable overhead:

Rate variance …………………………...

$ 6,500

F

Efficiency variance……………………..

4,000

U

Fixed overhead:

Budget variance ………………………..

3,000

U

Volume variance ………………………..

24,000

F

Overapplied overhead—see part 3 …..

$23,500

F

DLHs (65,000 DLHs).

60 Managerial Accounting for Managers, 4th Edition

3. Variable overhead variances:

Actual Hours of

Input, at the

Actual Rate

Actual Hours of Input,

at the Standard Rate

Standard Hours

Allowed for Output, at

the Standard Rate

(AH × AR)

(AH × SR)

(SH × SR)

$78,000

30,000 hours ×

$2.50 per hour

32,000 hours ×

$2.50 per hour

= $75,000

= $80,000

Rate Variance,

$3,000 U

Efficiency Variance,

$5,000 F

Alternative solution: