Solutions Manual, Chapter 11 41

Problem 11-15 (continued)

2. Summary of variances:

Material price variance ……………………..

$ 3,000

F

Material quantity variance …………………

8,400

U

Labor rate variance ………………………….

11,800

U

Labor efficiency variance…………………..

1,200

F

Variable overhead rate variance ………….

590

U

Variable overhead efficiency variance ….

300

F

Net variance …………………………………..

$16,290

U

Budgeted cost of goods sold at $12 per pool ………

$180,000

Add the net unfavorable variance, as above ……….

16,290

Actual cost of goods sold ……………………………….

$196,290

operating income for the month.

Budgeted net operating income ……………………….

$36,000

Deduct the net unfavorable variance added to cost

of goods sold for the month …………………………

16,290

Net operating income ……………………………………

$19,710

3. The two most significant variances are the materials quantity variance

and the labor rate variance. Possible causes of the variances include:

Materials quantity variance:

Outdated standards, unskilled workers,

poorly adjusted machines,

carelessness, poorly trained workers,

inferior quality materials.

Labor rate variance:

Outdated standards, change in pay

scale, overtime pay.

42 Managerial Accounting for Managers, 4th Edition

Problem 11-16 (60 minutes)

1.

Standard cost for March production:

Materials ……………………………………………………………..

$16,800

Direct labor ………………………………………………………….

10,500

Variable manufacturing overhead ………………………………

4,200

Total standard cost (a) ……………………………………………

$31,500

Number of backpacks produced (b) …………………………..

1,000

Standard cost of a single backpack (a) ÷ (b) ………………

$31.50

2.

Standard cost of a single backpack (above) …………………

$31.50

Deduct difference between standard and actual cost …….

0.15

Actual cost per backpack …………………………………………

$31.35

3.

Total standard cost of materials allowed during March

(a) …………………………………………………………………

$16,800

Number of backpacks produced during March (b) ……….

1,000

Standard materials cost per backpack (a) ÷ (b) ………….

$16.80

Standard materials cost per backpack $16.80 per backpack

=

Standard materials cost per yard $6.00 per yard

= 2.8 yards per backpack

4.

Standard cost of material used …………

$16,800

Actual cost of material used …………….

15,000

Total variance ……………………………….

$ 1,800

F

The price and quantity variances together equal the total variance. If

Price variance ……………………………….

$ 3,000

F

Quantity variance ………………………….

1,200

U

Total variance ……………………………….

$ 1,800

F

Solutions Manual, Chapter 11 43

Problem 11-16 (continued)

Alternative Solution:

Actual Quantity

of Input, at

Actual Price

Actual Quantity

of Input, at

Standard Price

Standard Quantity

Allowed for Output,

at Standard Price

(AQ × AP)

(AQ × SP)

(SQ × SP)

3,000 yards ×

$5.00 per yard

3,000 yards ×

$6.00 per yard*

2,800 yards** ×

$6.00 per yard*

= $15,000*

= $18,000

= $16,800*

Price Variance,

$3,000 F

Quantity Variance,

$1,200 U*

Spending Variance,

$1,800 F

*

Given.

**

1,000 units × 2.8 yards per unit = 2,800 yards

5. The first step in computing the standard direct labor rate is to determine

the standard direct labor-hours allowed for the month’s production. The

direct labor-hours worked:

Standard variable manufacturing overhead cost for March (a) .

$4,200

Standard variable manufacturing overhead rate per direct

labor-hour (b) ………………………………………………………….

$3.00

Standard direct labor-hours for March (a) ÷ (b) …………………

1,400

Total standard direct labor cost for March $10,500

=

Total standard direct labor-hours for March 1,400 DLHs

= $7.50 per DLH

44 Managerial Accounting for Managers, 4th Edition

Problem 11-16 (continued)

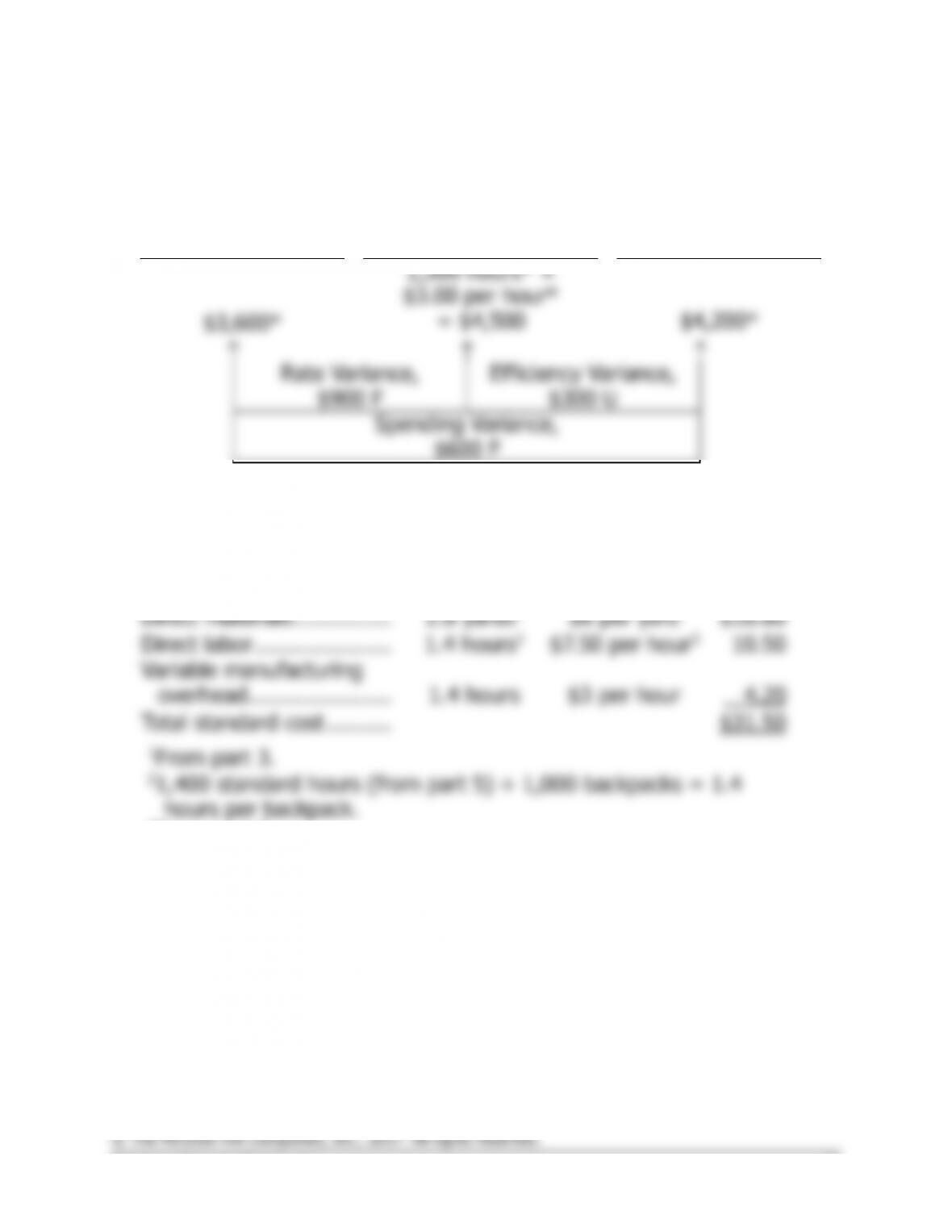

6. Before the labor variances can be computed, it is necessary to compute

the actual direct labor cost for the month:

Actual cost per backpack produced (part 2) ……..

$ 31.35

Number of backpacks produced ……………………..

× 1,000

Total actual cost of production ……………………….

$31,350

Less: Actual cost of materials ………………………..

$15,000

Actual cost of variable manufacturing

overhead ………………………………………..

3,600

18,600

Actual cost of direct labor …………………………….

$12,750

Actual Hours of

Input, at the

Actual Rate

Actual Hours of Input,

at the Standard Rate

Standard Hours

Allowed for Output, at

the Standard Rate

(AH × AR)

(AH × SR)

(SH × SR)

1,500 hours* ×

$7.50 per hour

$12,750

= $11,250

$10,500*

Rate Variance,

$1,500 U

Efficiency Variance,

$750 U

Spending Variance,

$2,250 U

*Given.

Solutions Manual, Chapter 11 45

Problem 11-16 (continued)

7.

Actual Hours of

Input, at the

Actual Rate

Actual Hours of Input,

at the Standard Rate

Standard Hours

Allowed for Output,

at the Standard Rate

(AH × AR)

(AH × SR)

(SH × SR)

1,500 hours* ×

$3.00 per hour*

$3,600*

= $4,500

$4,200*

Rate Variance,

$900 F

Efficiency Variance,

$300 U

Spending Variance,

$600 F

*Given.

8.

Standard

Quantity or

Hours

Standard

Price or

Rate

Standard

Cost

Direct materials ……………

2.8 yards1

$6 per yard

$16.80

Direct labor …………………

1.4 hours2

$7.50 per hour3

10.50

Variable manufacturing

overhead ………………….

1.4 hours

$3 per hour

4.20

Total standard cost ……….

$31.50

1From part 3.

21,400 standard hours (from part 5) ÷ 1,000 backpacks = 1.4

hours per backpack.

3From part 5.

46 Managerial Accounting for Managers, 4th Edition

Case 11–17 (60 minutes)

1. The number of units produced can be computed by using the total

standard cost applied for the period for

any

input—direct materials,

direct labor, or variable manufacturing overhead. Using the standard

cost applied for direct materials, we have:

Total standard cost applied for the period $405,000

=

Standard cost per unit $18 per unit

= 22,500 units

The same answer can be obtained by using direct labor or variable

manufacturing overhead.

6.

Standard variable overhead cost applied

$54,000

Add: Overhead efficiency variance ………

4,200

U

(see below)

Deduct: Overhead rate variance …………

1,300

F

Actual variable overhead cost incurred …

$56,900

Solutions Manual, Chapter 11 47

Case 11-17 (continued)

Direct materials analysis:

Actual Quantity of

Inputs, at Actual

Price

Actual Quantity

of Inputs, at

Standard Price

Standard Quantity

Allowed for Output,

at Standard Price

(AQ × AP)

(AQ × SP)

(SQ × SP)

138,000 pounds

× $2.95 per pound***

138,000 pounds**

× $3 per pound

135,000 pounds*

× $3 per pound

= $407,100

= $414,000

= $405,000

Price Variance,

$6,900 F

Quantity Variance,

$9,000 U

Spending Variance,

$2,100 U

*

22,500 units × 6 pounds per unit = 135,000 pounds

**

$414,000 ÷ $3 per pound = 138,000 pounds

***

$407,100 ÷ 138,000 pounds = $2.95 per pound

Direct labor analysis:

Actual Hours of Input,

at the Actual Rate

Actual Hours of

Input, at the

Standard Rate

Standard Hours

Allowed for Output,

at the Standard Rate

(AH × AR)

(AH × SR)

(SH × SR)

19,400 DLHs ×

$15.75 per DLH***

19,400 DLHs** ×

$15 per DLH

18,000 DLHs* ×

$15 per DLH

= $305,550

= $291,000

= $270,000

Rate Variance,

$14,550 U

Efficiency Variance,

$21,000 U

Spending Variance,

$35,550 U

*

22,500 units × 0.8 DLHs per unit = 18,000 DLHs

**

$291,000 ÷ $15 per DLH = 19,400 DLHs

***

$305,550 ÷ 19,400 DLHs = $15.75 per DLH

48 Managerial Accounting for Managers, 4th Edition

Case 11-17 (continued)

Variable overhead analysis:

Actual Hours of Input,

at the Actual Rate

Actual Hours of

Input, at the

Standard Rate

Standard Hours

Allowed for Output,

at the Standard Rate

(AH × AR)

(AH × SR)

(SH × SR)

$56,900**

19,400 DLHs ×

$3 per DLH

18,000 DLHs ×

$3 per DLH

= $58,200

= $54,000

Rate Variance,

$1,300 F

Efficiency Variance,

$4,200 U*

*

Computed using 19,400 actual DLHs at the $3 per DLH standard rate.

**

$58,200 – $1,300 = $56,900.

Appendix 11A

Predetermined Overhead Rates and Overhead

Analysis in a Standard Costing System

© The McGraw-Hill Companies, Inc., 2017. All rights reserved.

50 Managerial Accounting for Managers, 4th Edition