Solutions Manual, Chapter 11 21

Problem 11-9 (continued)

2. Many students will miss parts 2 and 3 because they will try to use

product

costs as if they were

hourly

costs. Pay particular attention to

the computation of the standard direct labor time per unit and the

standard direct labor rate per hour.

Actual Hours of

Input, at the

Actual Rate

Actual Hours of

Input, at the

Standard Rate

Standard Hours

Allowed for Output,

at the Standard Rate

(AH × AR)

(AH × SR)

(SH × SR)

2,800 hours ×

$6.00 per hour*

3,000 hours** ×

$6.00 per hour*

$18,200

= $16,800

= $18,000

Rate Variance,

$1,400 U

Efficiency Variance,

$1,200 F

Spending Variance,

$200 U

*

2,850 standard hours ÷ 1,900 sets = 1.5 standard hours per set,

$9.00 standard cost per set ÷ 1.5 standard hours per set =

$6.00 standard rate per hour.

**

2,000 sets × 1.5 standard hours per set = 3,000 standard hours.

Alternatively, the variances can be computed using the formulas:

Labor rate variance = AH (AR – SR)

22 Managerial Accounting for Managers, 4th Edition

Problem 11-9 (continued)

3.

Actual Hours of

Input, at the

Actual Rate

Actual Hours of

Input, at the

Standard Rate

Standard Hours

Allowed for Output,

at the Standard Rate

(AH × AR)

(AH × SR)

(SH × SR)

2,800 hours ×

$2.40 per hour*

3,000 hours ×

$2.40 per hour*

$7,000

= $6,720

= $7,200

Rate Variance,

$280 U

Efficiency Variance,

$480 F

Spending Variance,

$200 F

*$3.60 standard cost per set ÷ 1.5 standard hours per set

= $2.40 standard rate per hour

Alternatively, the variances can be computed using the formulas:

Solutions Manual, Chapter 11 23

Problem 11-10 (45 minutes)

1.

Standard

Quantity or

Hours

Standard Price

or Rate

Standard

Cost

Alpha6:

Direct materials—X442 ……

1.8 kilos

$3.50 per kilo

$ 6.30

Direct materials—Y661 ……

2.0 liters

$1.40 per liter

2.80

Direct labor—Sintering …….

0.20 hours

$19.80 per hour

3.96

Direct labor—Finishing …….

0.80 hours

$19.20 per hour

15.36

Total …………………………..

$28.42

Zeta7:

Direct materials—X442 ……

3.0 kilos

$3.50 per kilo

$10.50

Direct materials—Y661 ……

4.5 liters

$1.40 per liter

6.30

Direct labor—Sintering …….

0.35 hours

$19.80 per hour

6.93

Direct labor—Finishing …….

0.90 hours

$19.20 per hour

17.28

Total …………………………..

$41.01

24 Managerial Accounting for Managers, 4th Edition

Problem 11-10 (continued)

2. The computations to follow will require the standard quantities allowed

for the actual output for each material.

Standard Quantity Allowed

Material X442:

Production of Alpha6 (1.8 kilos per unit × 1,500 units) ……

2,700 kilos

Production of Zeta7 (3.0 kilos per unit × 2,000 units) ……..

6,000 kilos

Total ……………………………………………………………………

8,700 kilos

Material Y661:

Production of Alpha6 (2.0 liters per unit × 1,500 units) …..

3,000 liters

Production of Zeta7 (4.5 liters per unit × 2,000 units) …….

9,000 liters

Total ……………………………………………………………………

12,000 liters

Direct Materials Variances—Material X442:

Direct Materials Variances—Material Y661:

Materials price variance = AQ (AP – SP)

Solutions Manual, Chapter 11 25

Problem 11-10 (continued)

3. The computations to follow will require the standard quantities allowed

for the actual output for direct labor in each department.

Standard Hours Allowed

Sintering:

Production of Alpha6 (0.20 hours per unit × 1,500 units) ..

300 hours

Production of Zeta7 (0.35 hours per unit × 2,000 units) ….

700 hours

Total ……………………………………………………………………

1,000 hours

Finishing:

Production of Alpha6 (0.80 hours per unit × 1,500 units) ..

1,200 hours

Production of Zeta7 (0.90 hours per unit × 2,000 units) ….

1,800 hours

Total ……………………………………………………………………

3,000 hours

Direct Labor Variances—Sintering:

Direct Labor Variances—Finishing:

Labor rate variance = AH (AR – SR)

Input, at Actual Price

Problem 11-11 (45 minutes)

1. a. Materials quantity variance = SP (AQ – SQ)

*

$3,200 units × 3 foot per unit

**

When used with the formula, unfavorable variances are

positive and favorable variances are negative.

Therefore, $55,650 ÷ 10,500 feet = $5.30 per foot

b. Materials price variance = AQ (AP – SP)

Solutions Manual, Chapter 11 27

Problem 11-11 (continued)

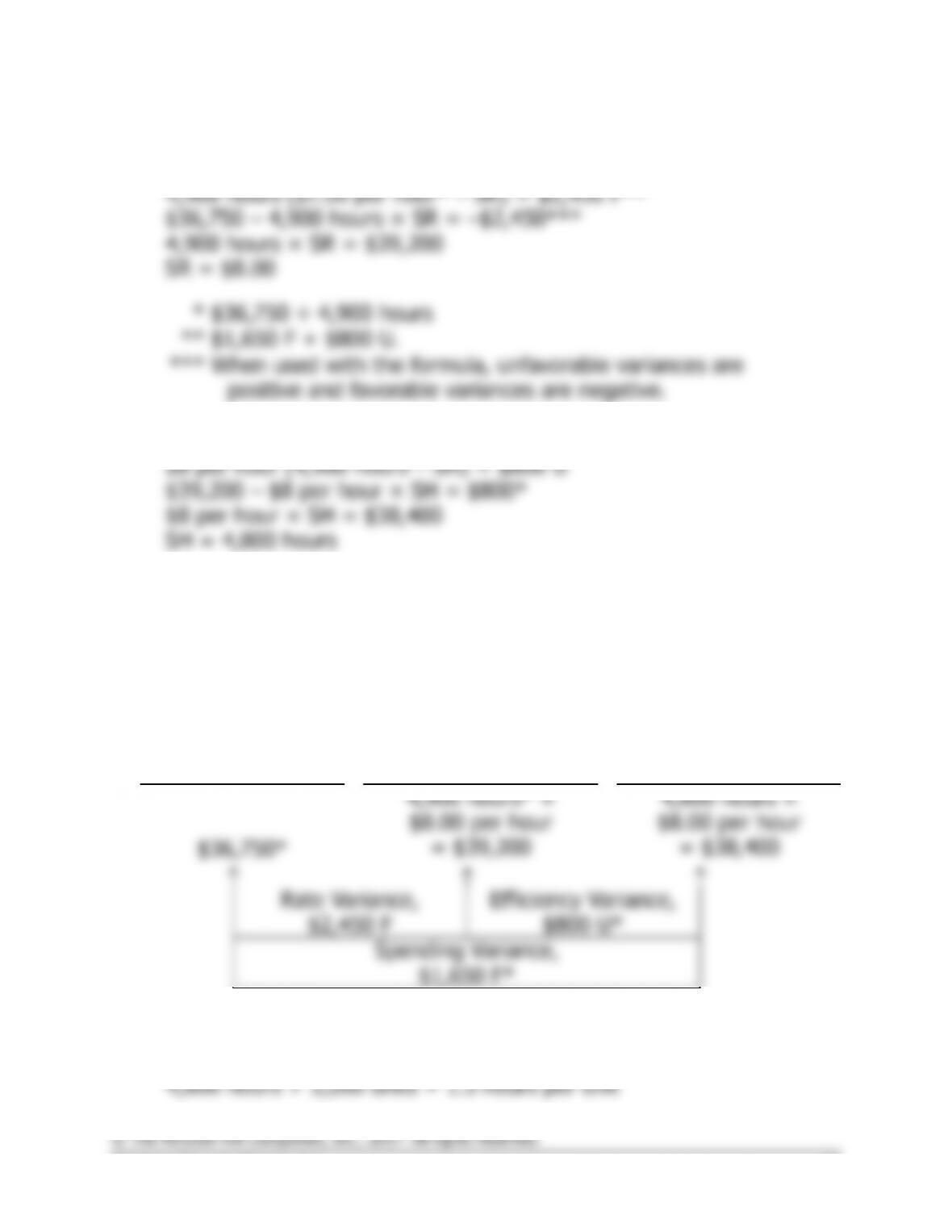

2. a. Labor rate variance = AH (AR – SR)

*

$36,750 ÷ 4,900 hours

**

$1,650 F + $800 U.

***

When used with the formula, unfavorable variances are

positive and favorable variances are negative.

b. Labor efficiency variance = SR (AH – SH)

*

When used with the formula, unfavorable variances are positive

and favorable variances are negative.

Alternative approach to parts (a) and (b):

Actual Hours of

Input, at the

Actual Rate

Actual Hours of Input,

at the Standard Rate

Standard Hours

Allowed for Output,

at the Standard Rate

(AH × AR)

(AH × SR)

(SH × SR)

4,900 hours* ×

$8.00 per hour

4,800 hours ×

$8.00 per hour

$36,750*

= $39,200

= $38,400

Rate Variance,

$2,450 F

Efficiency Variance,

$800 U*

Spending Variance,

$1,650 F*

*Given.

c. The standard hours allowed per unit of product are:

28 Managerial Accounting for Managers, 4th Edition

Problem 11-12 (45 minutes)

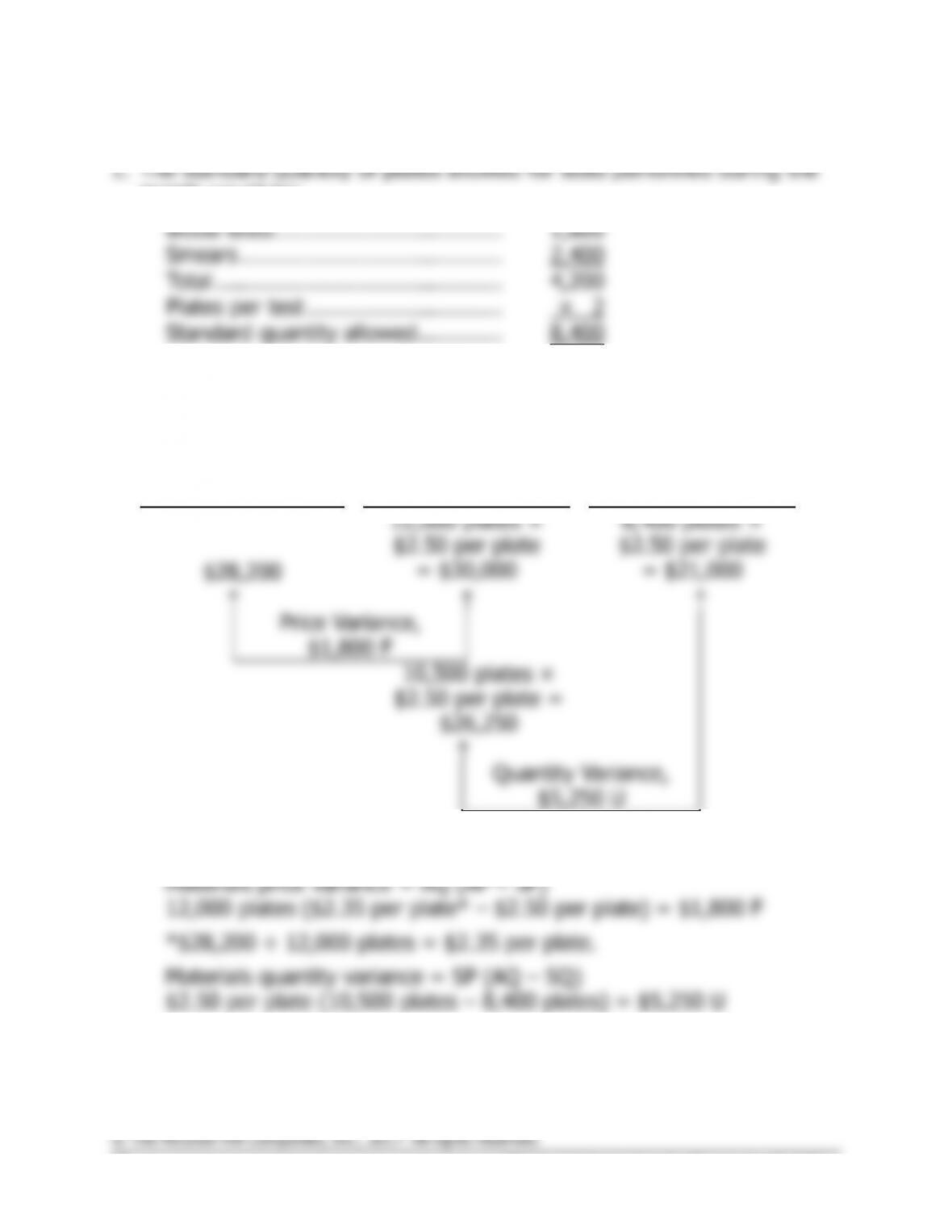

month would be:

Blood tests ……………………………..

1,800

Smears ………………………………….

2,400

Total ……………………………………..

4,200

Plates per test …………………………

× 2

Standard quantity allowed ………….

8,400

The variance analysis for plates would be:

Actual Quantity of

Input, at Actual Price

Actual Quantity

of Input, at

Standard Price

Standard Quantity

Allowed for Output,

at Standard Price

(AQ × AP)

(AQ × SP)

(SQ × SP)

12,000 plates ×

$2.50 per plate

8,400 plates ×

$2.50 per plate

$28,200

= $30,000

= $21,000

Price Variance,

$1,800 F

10,500 plates ×

$2.50 per plate =

$26,250

Quantity Variance,

$5,250 U

Alternatively, the variances can be computed using the formulas:

Solutions Manual, Chapter 11 29

Problem 11-12 (continued)

Note that all of the price variance is due to the hospital’s 6% quantity

discount. Also note that the $5,250 quantity variance for the month is

equal to 25% of the standard cost allowed for plates.

2. a. The standard hours allowed for tests performed during the month

would be:

Blood tests: 0.3 hour per test × 1,800 tests ……….

540

hours

Smears: 0.15 hour per test × 2,400 tests …………..

360

hours

Total standard hours allowed …………………………..

900

hours

The variance analysis would be:

Actual Hours of

Input, at the

Actual Rate

Actual Hours of Input,

at the Standard Rate

Standard Hours

Allowed for Output, at

the Standard Rate

(AH × AR)

(AH × SR)

(SH × SR)

1,150 hours ×

$14.00 per hour

900 hours ×

$14.00 per hour

$13,800

= $16,100

= $12,600

Rate Variance,

$2,300 F

Efficiency Variance,

$3,500 U

Spending Variance,

$1,200 U

Alternatively, the variances can be computed using the formulas:

30 Managerial Accounting for Managers, 4th Edition

Problem 11-12 (continued)

is traceable to inadequate supervision of assistants in the lab.

3. The variable overhead variances follow:

Actual Hours of

Input, at the

Actual Rate

Actual Hours of Input,

at the Standard Rate

Standard Hours

Allowed for Output,

at the Standard Rate

(AH × AR)

(AH × SR)

(SH × SR)

1,150 hours ×

$6.00 per hour

900 hours ×

$6.00 per hour

$7,820

= $6,900

= $5,400

Rate Variance,

$920 U

Efficiency Variance,

$1,500 U

Spending Variance,

$2,420 U

Alternatively, the variances can be computed using the formulas:

be favorable (or unfavorable).