Solutions Manual, Chapter 11 1

Chapter 11

Standard Costs and Variances

Solutions to Questions

11-1 A quantity standard indicates how much

11-2 Separating an overall variance into a

11-3 The materials price variance is usually

11-4 The materials price variance can be

computed either when materials are purchased

11-5 This combination of variances may

used to find someone to blame for problems.

labor rate variance. For example, skilled workers

variance. Or unskilled or untrained workers can

be assigned to tasks that should be filled by

11-8 If poor quality materials create

11-9 If overhead is applied on the basis of

direct labor-hours, then the variable overhead

rate, differs between the two variances.

produce at capacity, the bottleneck will be

2 Managerial Accounting for Managers, 4th Edition

inventory will build up in front of the

workstations with the least capacity.

Solutions Manual, Chapter 11 3

The Foundational 15

for cost variances as follows:

Actual Quantity of

Input,

at Actual Price

(AQ × AP)

Actual Quantity of

Input,

at Standard Price

(AQ × SP)

Standard Quantity

Allowed

for Actual Output,

at Standard Price

(SQ × SP)

160,000 pounds ×

$7.50 per pound

= $1,200,000

160,000 pounds ×

$8.00 per pound

= $1,280,000

150,000 pounds* ×

$8.00 per pound

= $1,200,000

Materials price

variance = $80,000 F

Materials quantity

variance = $80,000 U

Spending variance = $0

*30,000 units × 5 pounds per unit = 150,000 pounds

Materials price variance = AQ (AP – SP)

= $80,000 U

The Foundational 15 (continued)

5. and 6.

The materials price variance ($85,000 F) and the materials quantity

variance ($80,000 U) can be computed as follows:

Actual Quantity

of Input,

at Actual Price

(AQ × AP)

Actual Quantity

of Input,

at Standard Price

(AQ × SP)

Standard Quantity

Allowed for Actual

Output,

at Standard Price

(SQ × SP)

170,000 pounds ×

$7.50 per pound

= $1,275,000

170,000 pounds ×

$8.00 per pound

= $1,360,000

150,000 pounds* ×

$8.00 per pound

= $1,200,000

Materials price variance

= $85,000 F

160,000 pounds ×

$8.00 per pound

= $1,280,000

Materials quantity

variance = $80,000 U

*30,000 units × 5 pounds per unit = 150,000 units

Alternatively, the variances can be computed using the formulas:

Solutions Manual, Chapter 11 5

The Foundational 15 (continued)

7. The direct labor cost included in the planning budget is $700,000 (=

The direct labor cost included in the flexible budget (SH × SR = $840,000),

Alternatively, the variances can be computed using the formulas:

6 Managerial Accounting for Managers, 4th Edition

The Foundational 15 (continued)

12. The variable manufacturing overhead cost included in the planning

The variable overhead cost included in the flexible budget (SH × SR =

$300,000), the variable overhead rate variance ($55,000 U), and the

variable overhead efficiency variance ($25,000 F) can be computed using

the general model for cost variances as follows:

Actual Hours of Input,

at Actual Rate

(AH × AR)

Actual Hours of Input,

at Standard Rate

(AH × SR)

Standard Hours Allowed

for Actual Output,

at Standard Rate

(SH × SR)

55,000 hours ×

$5.10 per hour**

= $280,500

55,000 hours ×

$5.00 per hour

= $275,000

60,000 hours* ×

$5.00 per hour

= $300,000

Variable overhead rate

variance = $5,500 U

Variable overhead

efficiency variance

= $25,000 F

Spending variance = $19,500 F

*30,000 units × 2.0 hours per unit = 60,000 hours

** $280,500 ÷ 55,000 hours = $5.10 per hour

Alternatively, the variances can be computed using the formulas:

Variable overhead efficiency variance = SR (AH – SH)

Solutions Manual, Chapter 11 7

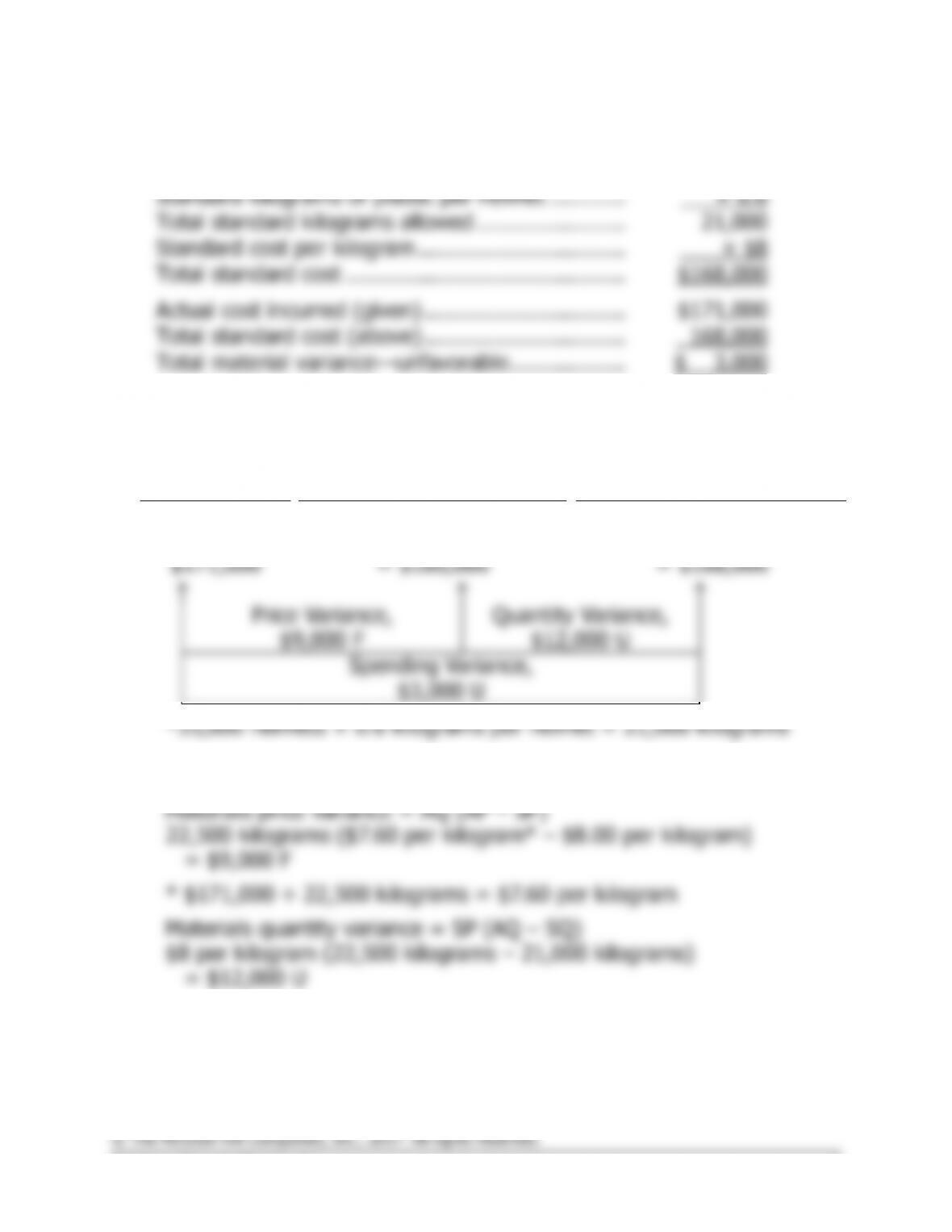

Exercise 11-1 (20 minutes)

1.

Number of helmets …………………………………….

35,000

Standard kilograms of plastic per helmet …………

× 0.6

Total standard kilograms allowed …………………..

21,000

Standard cost per kilogram …………………………..

× $8

Total standard cost …………………………………….

$168,000

Actual cost incurred (given) ………………………….

$171,000

Total standard cost (above) ………………………….

168,000

Total material variance—unfavorable ………………

$ 3,000

2.

Actual Quantity

of Input, at

Actual Price

Actual Quantity of Input,

at Standard Price

Standard Quantity

Allowed for Output, at

Standard Price

(AQ × AP)

(AQ × SP)

(SQ × SP)

22,500 kilograms ×

21,000 kilograms* ×

$8 per kilogram

$8 per kilogram

$171,000

= $180,000

= $168,000

Price Variance,

$9,000 F

Quantity Variance,

$12,000 U

Spending Variance,

$3,000 U

Alternatively, the variances can be computed using the formulas:

8 Managerial Accounting for Managers, 4th Edition

Exercise 11-2 (20 minutes)

1.

Number of meals prepared ……………….

4,000

Standard direct labor-hours per meal ….

× 0.25

Total direct labor-hours allowed …………

1,000

Standard direct labor cost per hour …….

× $9.75

Total standard direct labor cost ………….

$9,750

Actual cost incurred …………………………

$9,600

Total standard direct labor cost (above)

9,750

Total direct labor variance ………………..

$ 150

Favorable

2.

Actual Hours of

Input, at the

Actual Rate

Actual Hours of Input,

at the Standard Rate

Standard Hours

Allowed for Output, at

the Standard Rate

(AH×AR)

(AH×SR)

(SH×SR)

960 hours ×

$10.00 per hour

960 hours ×

$9.75 per hour

1,000 hours ×

$9.75 per hour

= $9,600

= $9,360

= $9,750

Rate Variance,

$240 U

Efficiency Variance,

$390 F

Spending Variance,

$150 F

Labor rate variance = AH(AR – SR)

Solutions Manual, Chapter 11 9

Exercise 11-3 (20 minutes)

1.

Number of items shipped …………………………...

120,000

Standard direct labor-hours per item …………….

× 0.02

Total direct labor-hours allowed …………………..

2,400

Standard variable overhead cost per hour ………

× $3.25

Total standard variable overhead cost …………..

$ 7,800

Actual variable overhead cost incurred ………….

$7,360

Total standard variable overhead cost (above) ..

7,800

Total variable overhead variance ………………….

$ 440

Favorable

2.

Actual Hours of

Input, at the

Actual Rate

Actual Hours of Input,

at the Standard Rate

Standard Hours

Allowed for Output, at

the Standard Rate

(AH×AR)

(AH×SR)

(SH×SR)

2,300 hours ×

$3.20 per hour*

2,300 hours ×

$3.25 per hour

2,400 hours ×

$3.25 per hour

= $7,360

= $7,475

= $7,800

Variable Overhead Rate

Variance, $115 F

Variable Overhead

Efficiency Variance,

$325 F

Spending Variance,

$440 F

Alternatively, the variances can be computed using the formulas:

Variable overhead rate variance:

Variable overhead efficiency variance:

10 Managerial Accounting for Managers, 4th Edition

Exercise 11-4 (30 minutes)

1.

Number of units manufactured ………………………..

20,000

Standard labor time per unit

(18 minutes ÷ 60 minutes per hour) ………………

× 0.3

Total standard hours of labor time allowed …………

6,000

Standard direct labor rate per hour …………………..

× $12

Total standard direct labor cost ……………………….

$72,000

Actual direct labor cost …………………………..……..

$73,600

Standard direct labor cost ………………………………

72,000

Total variance—unfavorable …………………………...

$ 1,600

2.

Actual Hours of

Input, at the

Actual Rate

Actual Hours of Input,

at the Standard Rate

Standard Hours Allowed

for Output, at the

Standard Rate

(AH × AR)

(AH × SR)

(SH × SR)

5,750 hours ×

$12.00 per hour

6,000 hours* ×

$12.00 per hour

$73,600

= $69,000

= $72,000

Rate Variance,

$4,600 U

Efficiency Variance,

$3,000 F

Spending Variance,

$1,600 U

Alternatively, the variances can be computed using the formulas:

Labor rate variance = AH (AR – SR)