38 Managerial Accounting for Managers, 4th Edition

Problem 10-25 (45 minutes)

1. The cost control report compares the planning budget, which was

prepared by the company should

not

be used to evaluate how well costs

were controlled.

Solutions Manual, Chapter 10 39

Problem 10-25 (continued)

2. A report that would be helpful in assessing how well costs were controlled appears below:

Freemont Corporation—Machining Department

Flexible Budget Performance Report

For the Month Ended June 30

Actual

Results

Spending

Variances

Flexible

Budget

Activity

Variances

Planning

Budget

Machine-hours (q) ……………………

38,000

38,000

35,000

Direct labor wages ($2.30q) ……….

$ 86,100

$ 1,300

F

$ 87,400

$6,900

U

$ 80,500

Supplies ($0.60q) …………………….

23,100

300

U

22,800

1,800

U

21,000

Maintenance ($92,000 + $1.20q) ..

137,300

300

F

137,600

3,600

U

134,000

Utilities ($11,700 + $0.10q) ……….

15,700

200

U

15,500

300

U

15,200

Supervision ($38,000) ………………

38,000

0

38,000

0

38,000

Depreciation ($80,000) ……………..

80,000

0

80,000

0

80,000

Total …………………………………….

$380,200

$ 1,100

F

$381,300

$12,600

U

$368,700

Note that in this new report the overall spending variance is favorable—indicating that costs were

most likely under control.

40 Managerial Accounting for Managers, 4th Edition

Case 10–26 (30 minutes)

It is difficult to imagine how Tom Kemper could ethically agree to go along

recommendations.” Failing to disclose the entire amount owed on the

industrial engineering contract violates this standard.

Individuals will differ in how they think Kemper should handle this

situation. In our opinion, he should firmly state that he is willing to call

Laura, but even if the bill does not arrive, he is ethically bound to properly

It is important to note that the problem may be a consequence of

inappropriate use of performance reports by corporate headquarters. If the

Solutions Manual, Chapter 10 41

Case 10–27 (45 minutes)

1. The flexible budget would be prepared as follows:

Boyne University Motor Pool

Spending Variances

For the Month Ended March 31

Actual

Results

Flexible

Budget

Spending

Variances

Miles (q1) …………………………………..

63,000

63,000

Autos (q2) ………………………………….

21

21

Gasoline ($0.15q1) ………………………

$ 9,350

$ 9,450

$100

F

Oil, minor repairs, parts ($0.04q1) …..

2,360

2,520

160

F

Outside repairs ($75q2) ………………..

1,420

1,575

155

F

Insurance ($100q2) ……………………..

2,120

2,100

20

U

Salaries and benefits ($7,540) ……….

7,540

7,540

0

Vehicle depreciation ($250q2) ………..

5,250

5,250

0

Total ………………………………………..

$28,040

$28,435

$395

F

2. The original report is based on a static budget approach that does not

allow for variations in the number of miles driven from month to month,

miles rather than the 63,000 miles actually driven during the month.

42 Managerial Accounting for Managers, 4th Edition

Case 10-28 (75 minutes)

1. The cost formulas for The Little Theatre appear below, where q1 is the

number of productions and q2 is the number of performances:

o Theater hall rent: $500q2. Variable with respect to the number of

o Administrative expenses: $32,400 + $1,080q1 +$40q2.

The Little Theatre

Flexible Budget

For the Year Ended December 31

Actual number of productions (q1) ……………………………..

7

Actual number of performances (q2) …………………………..

168

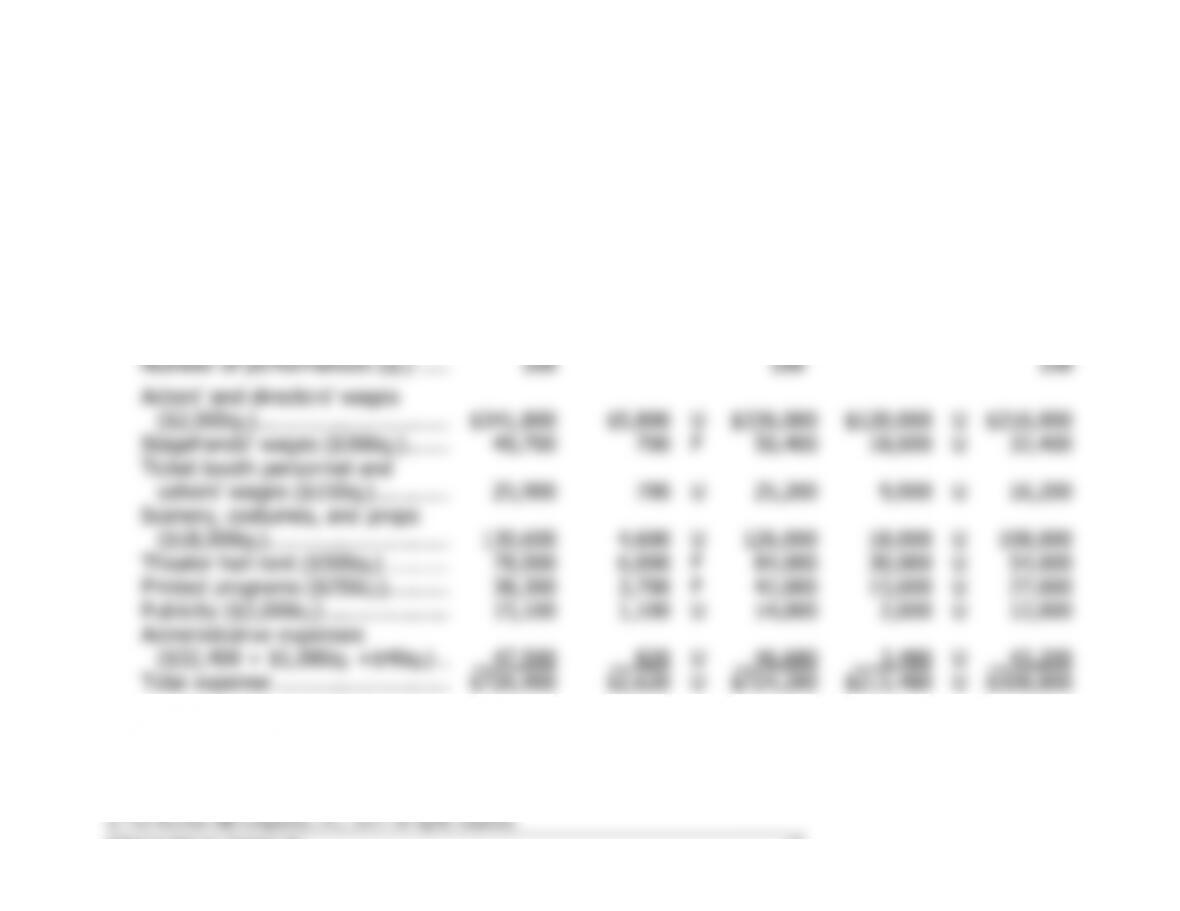

Actors’ and directors’ wages ($2,000q2) ………………………

$336,000

Stagehands’ wages ($300q2) …………………………………….

50,400

Ticket booth personnel and ushers’ wages ($150q2) ………

25,200

Scenery, costumes, and props ($18,000q1) ………………….

126,000

Theater hall rent ($500q2) ………………………………………..

84,000

Printed programs ($250q2) ……………………………………….

42,000

Publicity ($2,000q1) …………………………..……………………

14,000

Administrative expenses ($32,400 + $1,080q1 +$40q2)…..

46,680

Total expense ………………………………………………………..

$724,280

Solutions Manual, Chapter 10 43

Case 10-28 (continued)

2. The flexible budget performance report follows:

The Little Theatre

Flexible Budget Performance Report

For the Year Ended December 31

Actual

Results

Spending

Variances

Flexible

Budget

Activity

Variances

Planning

Budget

Number of productions (q1) ……..

7

7

6

Number of performances (q2) …..

168

168

108

Actors’ and directors’ wages

($2,000q2) ………………………….

$341,800

$5,800

U

$336,000

$120,000

U

$216,000

Stagehands’ wages ($300q2) …….

49,700

700

F

50,400

18,000

U

32,400

Ticket booth personnel and

ushers’ wages ($150q2) …………

25,900

700

U

25,200

9,000

U

16,200

Scenery, costumes, and props

($18,000q1) ………………………..

130,600

4,600

U

126,000

18,000

U

108,000

Theater hall rent ($500q2) ……….

78,000

6,000

F

84,000

30,000

U

54,000

Printed programs ($250q2) ……….

38,300

3,700

F

42,000

15,000

U

27,000

Publicity ($2,000q1) ………………..

15,100

1,100

U

14,000

2,000

U

12,000

Administrative expenses

($32,400 + $1,080q1 +$40q2) ..

47,500

820

U

46,680

3,480

U

43,200

Total expense ……………………….

$726,900

$2,620

U

$724,280

$215,480

U

$508,800

44 Managerial Accounting for Managers, 4th Edition

Case 10-28 (continued)

3. The overall unfavorable spending variance is a very small percentage of

favorable variances for theater hall rent and the printed programs.

Assuming that the quality of the printed programs has not noticeably

4. Average costs may not be very good indicators of the additional costs of

any particular production or performance. The averages gloss over

elaborate and costly costumes and props. Consequently, both the

production costs and the cost per performance will be much higher for