18 Managerial Accounting for Managers, 4th Edition

Problem A-7 (continued)

erating income.

Solutions Manual, Pricing Appendix 19

Problem A-7 (continued)

3. The price elasticity of demand, as defined in the text, is computed as

follows:

d =

ln(1 + % change in quantity sold)

ln(1 + % change in price)

=

ln(1+0.08)

ln(1-0.05)

=

ln(1.08)

ln(0.95)

=

0.07696

-0.05129

= -1.500

The profit-maximizing price can be estimated using the following formu-

la from the text:

Profit-maximizing price =

d

d

εVariable cost per unit

1+ε

æö

÷

ç÷

ç÷

ç÷

ç

èø

=

-1.5 $6.00

1+(-1.5)

æö

÷

ç÷

ç÷

÷

ç

ç

èø

= 3.00 × $6.00 = $18.00

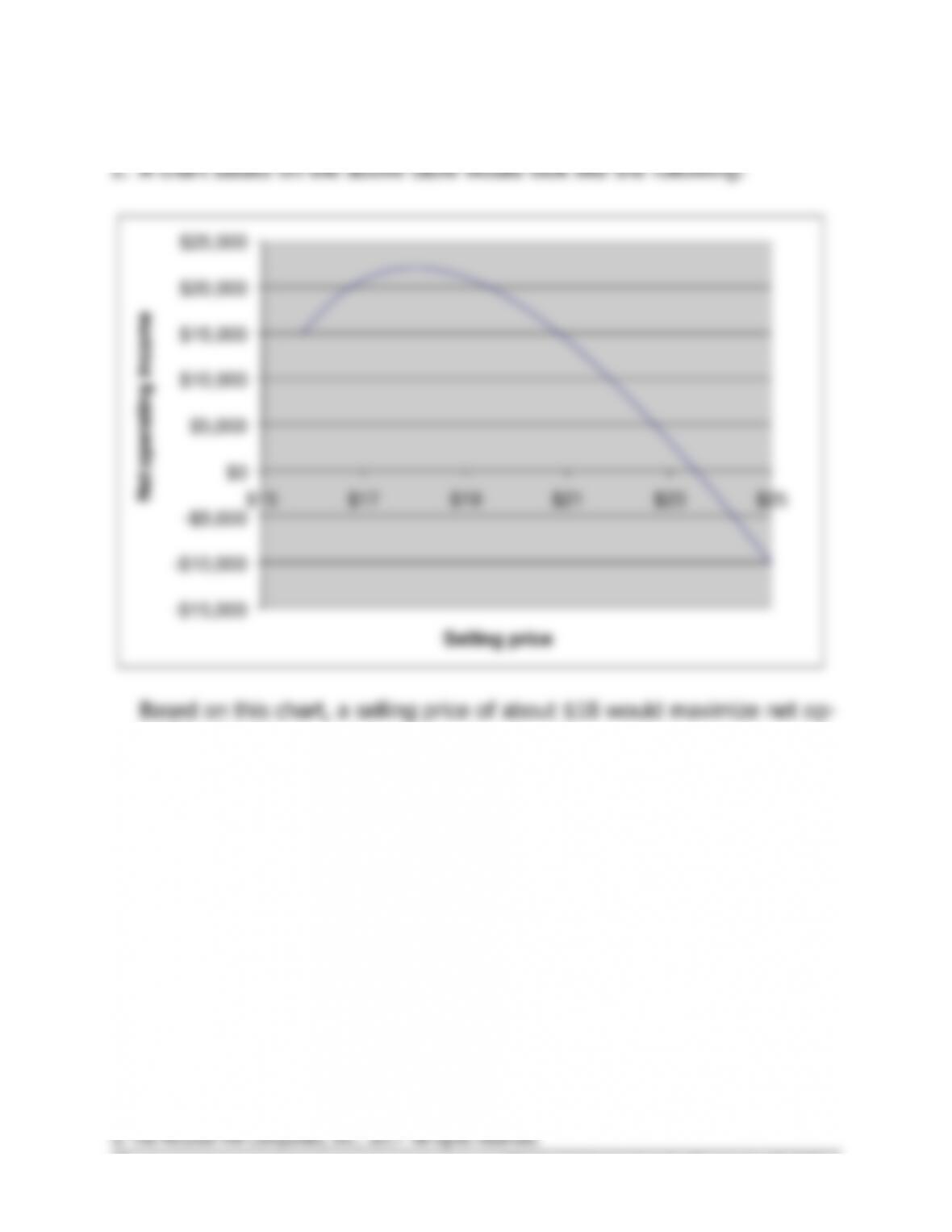

Note that this answer is consistent with the plot of the data in part (2)

above. The formula for the profit-maximizing price works in this case

because the demand is characterized by constant price elasticity. Every

5% decrease in price results in an 8% increase in unit sales.

Problem A-7 (continued)

4. We must first compute the markup percentage, which is a function of

( )

Required ROI Selling and administrative

+

× Investment expenses

Markup percentage =

on absorption cost Unit sales × Unit product cost

(2% × $2,000,000) + $960,000

= 50,000 units × $6 per unit

= 3.33 (rounded) or 333%

Unit product cost ………….

$ 6.00

Markup ($6.00 × 3.33) …..

19.98

Selling price …………………

$25.98

ware at this price.

Note: It can be shown that the unit sales at the $25.98 price would be

Sales (47,198 units × $25.98 per unit) …….

$1,226,204

Variable cost (47,198 units × $6 per unit) ..

283,188

Contribution margin …………………………….

943,016

Fixed expenses …………………………………..

960,000

Net operating loss ……………………………….

$ (16,984)

Problem A-8 (45 minutes)

1.

Projected sales (100 machines × $4,950 per machine) ..

$495,000

Less desired profit (15% × $600,000) ……………………..

90,000

Target cost for 100 machines …………………………………

$405,000

Target cost per machine ($405,000 ÷ 100 machines) ….

$4,050

Less National Restaurant Supply’s variable selling cost

per machine …………………………………………………….

650

Maximum allowable purchase price per machine ………..

$3,400

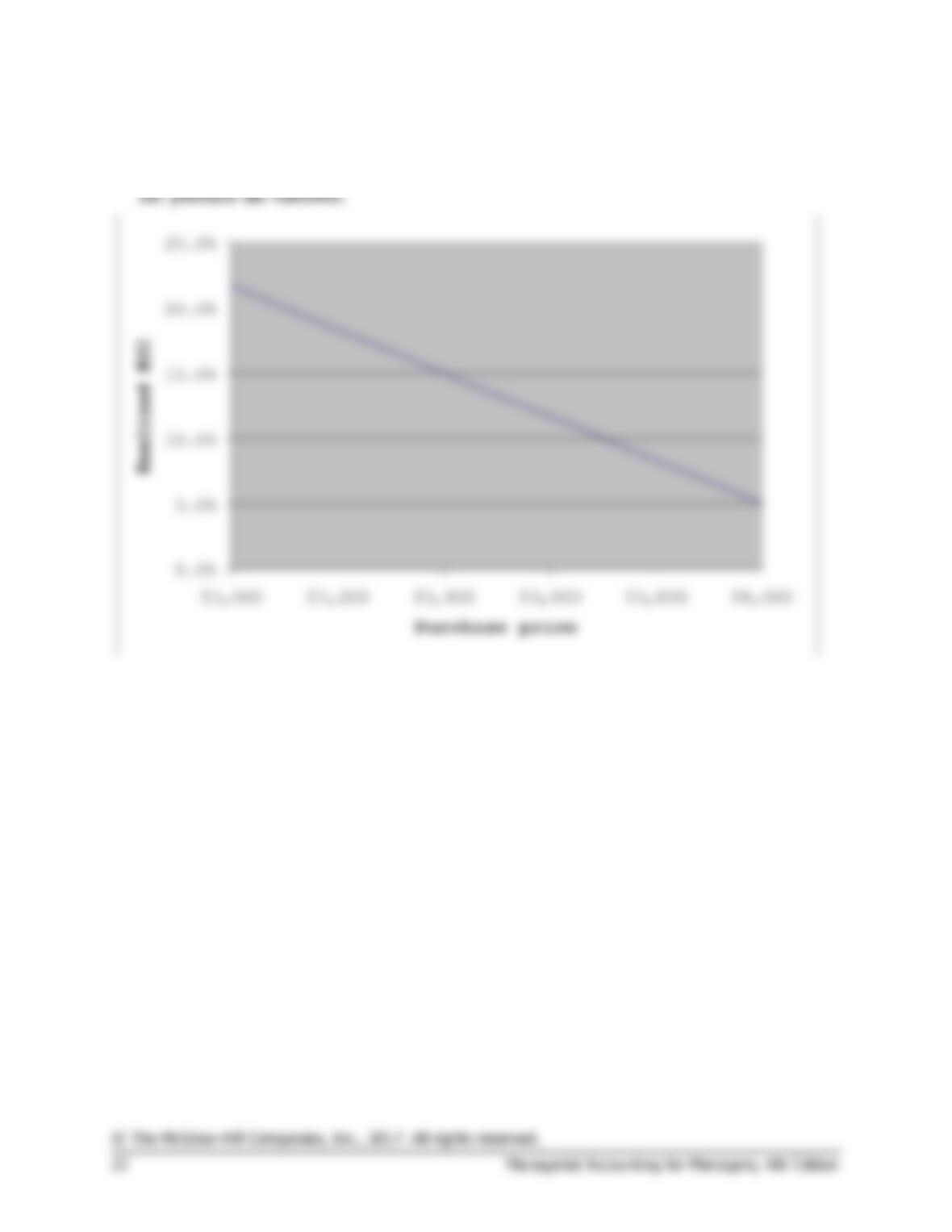

2. The relation between the purchase price of the machine and ROI can

be developed as follows:

Total projected sales – Total cost

ROI = Investment

$495,000 – ($650 + Purchase price of machines) × 100

= $600,000

Purchase price

ROI

$3,000

21.7%

$3,100

20.0%

$3,200

18.3%

$3,300

16.7%

$3,400

15.0%

$3,500

13.3%

$3,600

11.7%

$3,700

10.0%

$3,800

8.3%

$3,900

6.7%

$4,000

5.0%

22 Managerial Accounting for Managers, 4th Edition

Problem A-8 (continued)

Using the above data, the relation between purchase price and ROI can

© The McGraw-Hill Companies, Inc., 2017. All rights reserved.

Solutions Manual, Pricing Appendix 23

Problem A-8 (continued)

3. A number of options are available in addition to simply giving up on

adding the new sorbet machines to the company’s product lines. These

options include:

more profitable.

• Rethink the investment that would be required to carry this new prod-

uct. Can the size of the inventory be reduced? Are the new warehouse

fixtures really necessary?

this much to acquire more funds?