E9.11.

I would prefer to have operating income data, because this describes how well

E9.12.

2014 2013 2012 2011 2010

Operating income (earnings before

interest and taxes) … ……….. ……….. $1,192 $1,080 $1,155 $1,212 $1,272

E9.13.

January 1, 2016 through April 30, 2016 (20,000 shares * 4 months) ………. 80,000

May 1, 2016 through November 30, 2016 (25,000 shares * 7 months) ……. 175,000

E9.14.

a.

Total shares outstanding (by month * 12) ….. ……….. ……….. ……….. ……….. 645,000

Weighted-average number of shares outstanding (645,000 / 12 months) ….. 53,750

Net income ….. ……….. ……….. ……….. ……….. ……….. ……….. ……….. ……….. $191,150

common stock, would also have to be calculated.

February 1, 2016 through October 31, 2016 (50,000 shares * 9 months)…. 450,000

November 1, 2016 through January 31, 2017 (65,000 shares * 3 months)… 195,000

E9.15.

a.

($560,000 sales on account + $34,000 decrease in accounts receivable) = $594,000

source of cash. Since accounts receivable decreased during the year, more accounts were

collected in cash than were created by credit sales.

Accounts Receivable

b.

($118,000 income tax expense + $44,000 decrease in income taxes payable) = $162,000

use of cash. Tax payments exceeded the current year’s income tax expense because the

payable account decreased.

c.

($338,000 cost of goods sold + $34,000 increase in inventory – $49,000 increase in

accounts payable) = $323,000 use of cash. Cost of goods sold reflects inventory uses.

Inventory purchases were greater than inventory uses because inventory increased during

the year, but part of the inventory purchases were not paid for in cash because accounts

payable also increased during the year.

Inventory

Inventory purchases 372,000 Cost of goods sold 338,000

E9.15.

(continued)

d.

($290,000 increase in net book value + $130,000 depreciation expense) = $420,000 use

of cash. Since depreciation is an expense that does not affect cash, the amount of cash

paid to purchase new buildings exceeded the increase in net book value. (Note: In some

years, a firm may spend an enormous amount of cash to acquire new buildings and

equipment, yet still report a decrease in net book value.)

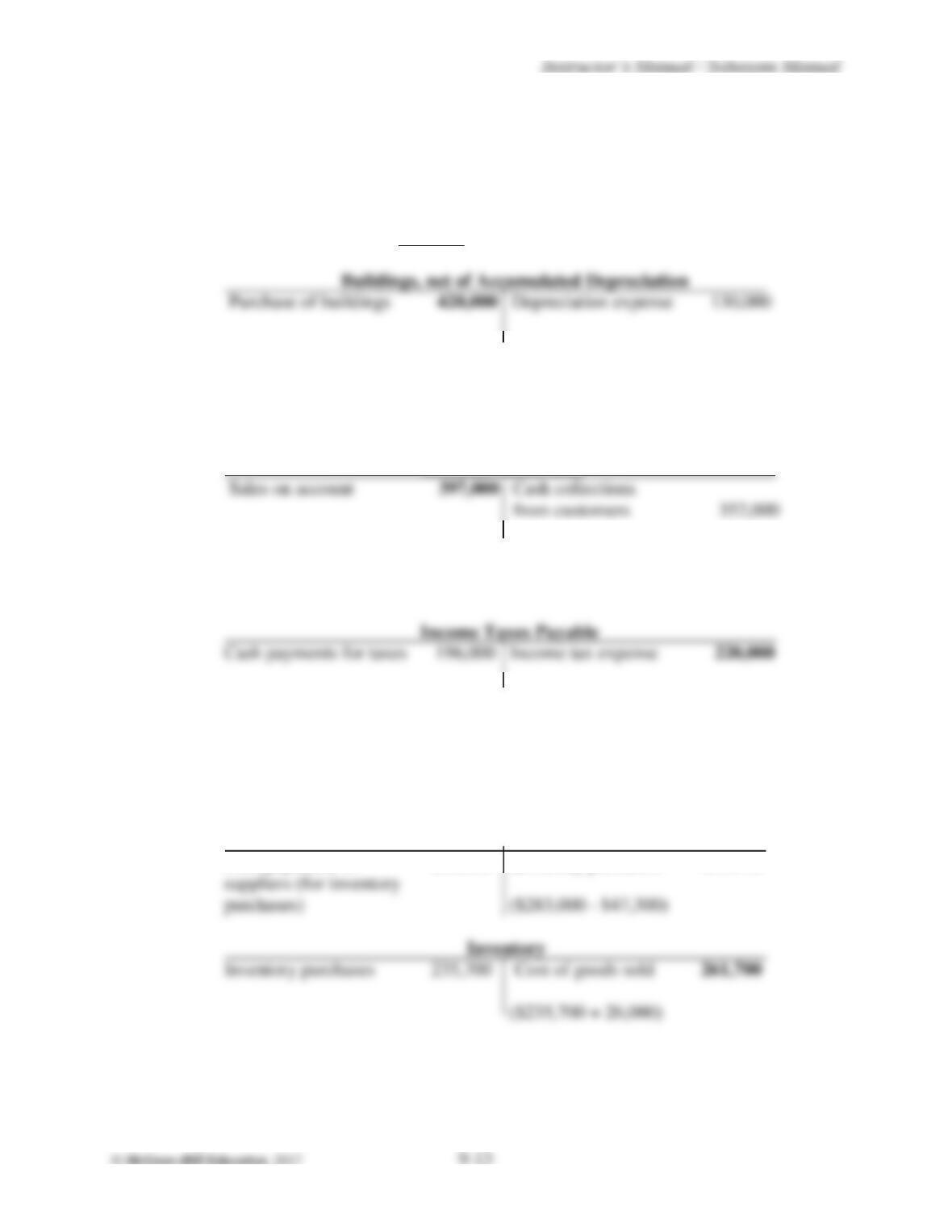

E9.16.

a.

($352,000 cash collected from customers + $45,000 increase in accounts receivable) =

$397,000 revenues earned. Since accounts receivable increased during the year, more

sales were made on account than were collected in cash during the year.

Accounts Receivable

b

($196,000 cash payments for income taxes + $24,000 increase in income taxes payable) =

$220,000 expense incurred. Income tax expense exceeded cash payments for taxes in the

current year because the payable account increased.

c.

($283,000 cash paid to suppliers + $26,000 decrease in inventory – $47,300 decrease in

accounts payable) = $261,700 expense incurred. Inventory purchases were less than cash

payments to suppliers because accounts payable decreased. Cost of goods sold reflects

inventory uses. Inventory uses were greater than inventory purchases because inventory

decreased during the year.

Accounts Payable

Cash payments to 283,000 Inventory purchases 235,700

E9.17.

a.

Campbell’s uses the multiple-step format. The multiple-step format is generally easier to

read and interpret because it provides intermediate captions and subtotals that are useful

b.

The EPS disclosures (basic and diluted) are important measures to investors because they

express accrual accounting income on a per share basis. For Campbell Soup Company,

these disclosures are straight-forward. As discussed in the text, however, additional

Repayments of notes payable ……….. ……….. ……….. ……….. ……….. $ (700)

Dividends paid ……….. ……….. ……….. ……….. ……….. ……….. ……….. (391)

Cash used by the two most significant financing activities .. ……….. $(1,091)

Sale of business, net of cash divested………………………………. $ 520

E9.16.

(continued)

d.

($210,000 cost of new building purchased – $125,000 increase in net book value) =

$85,000 expense incurred. The cost of new buildings purchased exceeded the increase in

net book value, and no buildings were sold, so the difference was the depreciation

expense recorded during the year (for old buildings).

E9.18.

a.

Amounts in millions:

Net earnings .. ……….. ……….. ……….. ……….. ……….. ……….. ……….. $ 807

Depreciation and amortization expense ……… ……….. ……….. ……….. 305

Cash provided by the two most significant operating sources…….. $1,112

P9.19.

a.

Net sales ……… ……….. ……….. ……….. ……….. ……….. ……….. ……….. ……….. $966,000

Cost of goods sold…… ……….. ……….. ……….. ……….. ……….. ……….. ……….. (552,000)

Gross profit …. ……….. ……….. ……….. ……….. ……….. ……….. ……….. ……….. $414,000

Advertising expense … ……….. ……….. ……….. ……….. ……….. ……….. ……….. (67,000)

Other selling expenses ……….. ……….. ……….. ……….. ……….. ……….. ……….. (20,000)

General and administrative expenses . ……….. ……….. ……….. ……….. ……….. (214,000)

Operating income ……. ……….. ……….. ……….. ……….. ……….. ……….. ……….. $113,000

Income from continuing operations … ……….. ……….. ……….. ……….. ……….. $ 74,000

Loss from discontinued operations, net of tax savings of $70,000 …. ……….. (155,000)

Net loss ………. ……….. ……….. ……….. ……….. ……….. ……….. ……….. ……….. $ (81,000)

P9.20.

a.

Operating income (or Income from operations) …….. ……….. ……….. ……….. $129,000

Income from continuing operations before taxes …… ……….. ……….. ……….. $ 65,000

Provision for income taxes …. ……….. ……….. ……….. ……….. ……….. ……….. (18,000)

Income from continuing operations … ……….. ……….. ……….. ……….. ……….. $ 47,000

Loss from discontinued operations, net of tax savings of $5,000 ….. ……….. (17,000)

Net income ….. ……….. ……….. ……….. ……….. ……….. ……….. ……….. ……….. $ 30,000

Net sales ……… ……….. ……….. ……….. ……….. ……….. ……….. ……….. ……….. $489,000

Cost of goods sold…… ……….. ……….. ……….. ……….. ……….. ……….. ……….. (272,000)

Gross profit …. ……….. ……….. ……….. ……….. ……….. ……….. ……….. ……….. $217,000

Selling, general, and administrative expenses ……….. ……….. ……….. ……….. (51,000)

P9.21.

Solution approach: Calculate ending inventory in the cost of goods sold model for the

high (33%) and low (30%) gross profit ratios, and select the ratio that yields the highest

ending inventory.

Gross Profit Ratio .

Calculation

33% 30% Sequence

Sales … ……….. ……….. ……….. $ 71,340 $ 71,340 Given

Cost of goods sold:

Beginning inventory .. ……….. $ 31,795 $ 31,795 Given

P9.22.

Solution approach: Using the cost of goods sold model for a periodic inventory system,

enter the known amounts and solve for ending inventory. The cost of goods sold amount

can be determined by multiplying sales by the complement of the gross profit ratio

(1 – 40%).

Sales … ……….. ……….. ……….. ……….. ……….. ……….. ……….. ……….. $319,200

Cost of goods sold:

Beginning inventory .. ……….. ……….. ……….. ……….. ……….. ……….. $157,100

P9.23.

a.

Cash flows from operating activities: ($000 omitted)

Net income ….. ……….. ……….. ……….. ……….. ……….. ……….. ……….. $ 840

Add (deduct) items not affecting cash:

b.

Net income is based on accrual accounting, and revenues may be earned before or after

cash is received. Likewise, expenses may be incurred before or after cash payments are

made. Thus, net income and cash flows provided by operations may differ because of the

timing of cash receipts and payments versus the timing of recognition on the income

statement. In addition to the timing issue, other adjustments to net income may be

P9.24.

Solution approach: Have the students review the statement of cash flows–indirect

method (see Exhibit 9-9). Emphasize that investing activities relate primarily to changes

in non-operating asset accounts, and that financing activities relate primarily to changes

non-operating liability and stockholders’ equity accounts.

POUCHIE CO.

Statement of Cash Flows

For the Year Ended December 31, 2016

Cash flows from operating activities: (in millions)

Net income ….. ……….. ……….. ……….. ……….. ……….. ……….. ……….. ……….. $ 768

Add (deduct) items not affecting cash:

Depreciation and amortization expense ……… ……….. ……….. ……….. ……….. 520

Cash flows from investing activities:

Purchase of equipment ……….. ……….. ……….. ……….. ……….. ……….. ……….. $(1,640)

Sale of building (at book value) ……… ……….. ……….. ……….. ……….. ……….. 424

Net cash used for investing activities ……….. ……….. ……….. ……….. ……….. $(1,216)

Cash flows from financing activities:

Common stock issued ……….. ……….. ……….. ……….. ……….. ……….. ……….. $ 296

P9.25.

a.

Solution approach: Prepare a statement of cash flows–direct method (see Exhibit 9-9).

P9.25.

(continued)

b.

Net cash used for investing activities ……….. ……….. ……….. ……….. ……….. $ ( 390)

Issuance of preferred stock …. ……….. ……….. ……….. ……….. ……….. ……….. 900

Net cash used for financing activities ……….. ……….. ……….. ……….. ……….. $ (780)

Cash flows from investing activities:

Purchase of land and buildings ………. ……….. ……….. ……….. ……….. ……….. $ (510)

P9.26.

a.

Cash flows from operating activities: (in millions)

Cash collected from customers ………. ……….. ……….. ……….. ……….. ……….. $4,720

Interest and taxes paid ……….. ……….. ……….. ……….. ……….. ……….. ……….. (220)

Cash paid to suppliers and employees ……….. ……….. ……….. ……….. ……….. ( ? ) .

Net cash provided by operating activities …… ……….. ……….. ……….. ……….. $1,800

Solving for the missing amount, cash paid to suppliers and employees = $2,700 million.

b.

Cash flows from investing activities:

Cash flows from financing activities:

Retirement of bonds at maturity …….. ……….. ……….. ……….. ……….. ……….. $ (300)

Issuance of common stock ….. ……….. ……….. ……….. ……….. ……….. ……….. 825

Cash dividends declared and paid …… ……….. ……….. ……….. ……….. ……….. (525)

Net cash provided (used) for financing activities …… ……….. ……….. ……….. $ 0

Net increase in cash for the year …….. ……….. ……….. ……….. ……….. ……….. $ 400

Net cash used by investing activities = ($1,800 operating – ??? investing + $0 financing

P9.27.

a.

HOEMAN, INC.

Comparative Balance Sheets

December 31, 2017, and 2016

Assets:

Current assets: 2017 2016

Cash … ……….. ……….. ……….. ……….. ……….. ……….. ……….. $ 26,000 $ 23,000

Accounts receivable … ……….. ……….. ……….. ……….. ……….. (1) 62,000 67,000

Inventory …….. ……….. ……….. ……….. ……….. ……….. ……….. 78,000 88,000

Liabilities:

Current liabilities:

Accounts payable …… ……….. ……….. ……….. ……….. ……….. (7) $ 83,500 $ 98,500

Calculations:

1. $67,000 – $5,000 = $62,000

2. $26,000 + $62,000 + $78,000 = $166,000

3. Land is carried at historical cost = $70,000

8. Same as total assets = $383,500

11. $383,500 – $126,500 – $161,000 = $96,000