CHAPTER

5

Accounting for and Presentation

of Current Assets

CHAPTER OUTLINE:

I. Preliminary topics

A. Operating Cycle

II. Cash and Cash Equivalents

A. Balance sheet valuation — amount available

B. The Bank Reconciliation as a Control Over Cash

1. Timing differences

a. Deposits in transit

b. Outstanding checks

c. Charges for bank services

d. Interest added to the account

e. NSF checks

3. Adjustments required

III. Short-Term Marketable Securities

A. Reasons for investing in debt and equity securities

IV. Accounts Receivable

A. Balance sheet valuation — net realizable value

B. Bad debts/uncollectible accounts

1. Expense recognition/valuation adjustment

2. Write-off of uncollectible accounts

C. Cash discounts

1. Credit terms

2. Cash discounts subtracted from revenues in income statement

Chapter 5 Accounting for and Presentation of Current Assets

V. Notes Receivable

A. Comparison with accounts receivable

B. Interest accrual

VI. Inventories

A. Alternative generally accepted practices exist

B. Flow of costs from inventory to cost of goods sold

C. Inventory cost flow assumptions

2. Weighted-average cost

4. LIFO

1. Perpetual

2. Periodic

G. Inventory errors

H. Balance sheet valuation at the lower of cost or market

VII. Prepaid Expenses and Other Current Assets

Instructor’s Manual / Solutions Manual

PRELIMINARY WARNING:

The coverage of six current asset elements in this chapter includes descriptions of many

accounting/bookkeeping procedures that enhance the student’s understanding of business and

make the coverage more complete; however, these procedures do not have to be mastered by the

TEACHING/LEARNING OBJECTIVES:

Principal:

1. To have the student understand and be able to analyze the transactions that affect current

3. To have the student understand the significance of inventories to many entities; to recognize

4. To have the student integrate accounting for current assets with its impact on profitability

Supporting:

5. To continue to build the student’s understanding of the double entry system and the use of

journal entries to record transactions and adjustments.

7. To have the student understand the reasons for, and valuation of, short-term investments.

8. To introduce the student to the concept and components of the system of internal control.

Chapter 5 Accounting for and Presentation of Current Assets

TEACHING OBSERVATIONS/ASSIGNMENT SUGGESTIONS:

1. The discussion of cash provides an opportunity to explain the bank reconciliation process,

which many students follow for their own checking account. Exercises 5-7 through 5-8 are

3. A key to understanding the allowance for bad debts account is to have students understand

the idea of detailed accounts receivable records and an allowance account that applies to

4. The Business In Practice box about Internal Control should be emphasized, because students

will encounter internal controls in their work, and now is the time to learn why they exist.

6. Inventory accounting is the first topic in the text coverage for which alternative accounting

practices exist.

Problems 5-31 through 5-34 are straightforward “numbers” assignments.

8. The impact of changing price levels is the most important integrating concept for the student

9. It is important to integrate the inventory cost flow assumption material with its impact on

10. Illustrations from actual annual reports should be utilized extensively so students become

more familiar with “reading” the financial statements and to illustrate the application of the

Instructor’s Manual / Solutions Manual

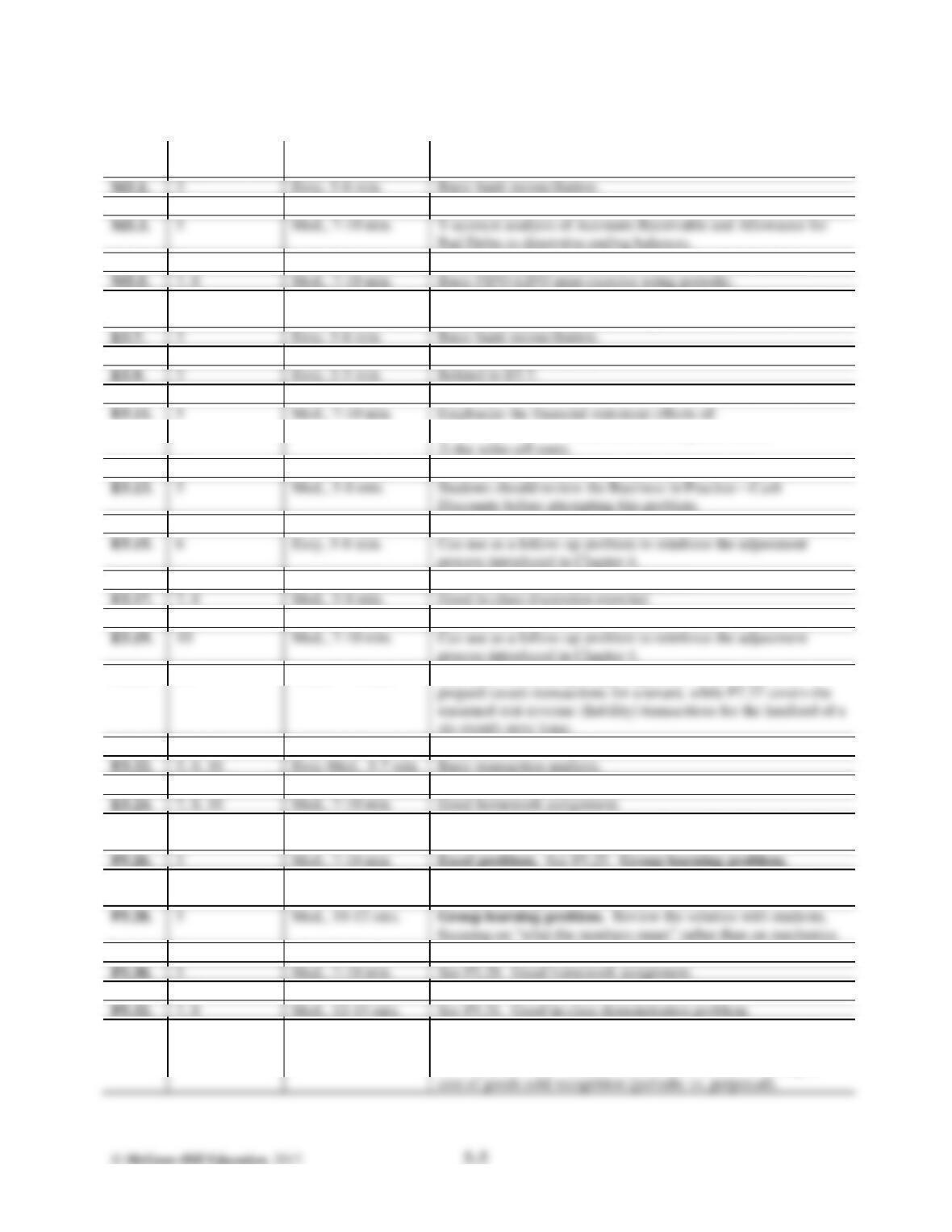

ASSIGNMENT OVERVIEW:

NO.

LEARNING

OBJECTIVES

DIFFICULTY &

TIME ESTIMATE

OTHER

COMMENTS

M5.1.

3

Easy, 5-8 min.

Basic bank reconciliation.

M5.2.

3

Easy, 2-3 min.

Related to M5.1.

M5.3.

5

Med., 7-10 min.

T-account analysis of Accounts Receivable and Allowance for

Bad Debts to determine ending balances.

M5.4.

5

Med., 7-10 min.

See M5.3. T-account analysis of Allowance for Bad Debts.

M5.5.

7, 8

Med., 7-10 min.

Basic FIFO-LIFO mini-exercise using periodic.

M5.6.

7, 8

Med., 7-10 min.

See M5.5. Basic FIFO-LIFO mini-exercise with an interesting

twist to calculate number of units purchased in October.

E5.7.

3

Easy, 5-8 min.

Basic bank reconciliation.

E5.8.

3

Easy, 5-8 min.

Basic bank reconciliation.

E5.9.

3

Easy, 2-3 min.

Related to E5.7.

E5.10.

3

Easy, 2-3 min.

Related to E5.8.

1) the adjustment to accrue bad debts expense, versus

E5.12.

5

Med., 7-10 min.

See E5.11. Good in-class demonstration exercise.

E5.13.

5

Med., 5-8 min.

Students should review the Business in Practice—Cash

Discounts before attempting this problem.

E5.14.

5

Easy, 4-6 min.

See E5.13. Good in-class demonstration exercise.

E5.15.

6

Easy, 5-8 min.

Can use as a follow-up problem to reinforce the adjustment

process introduced in Chapter 4.

E5.16.

6

Easy, 5-8 min.

See E5.15. Good homework assignment.

E5.17.

7, 8

Med., 5-8 min.

Good in-class discussion exercise.

E5.18.

7, 8

Med., 5-8 min.

See E5.17.

E5.20.

10

Med., 7-10 min.

See P7.27 for an integrating assignment. E5.20 covers the

E5.21.

5, 6, 8

Easy-Med., 5-7 min.

Basic transaction analysis.

E5.22.

Easy-Med., 5-7 min.

E5.23.

5, 6, 7

Easy-Med., 5-7 min.

Basic transaction analysis.

E5.24.

7, 8, 10

Med., 7-10 min.

Good homework assignment.

P5.25.

3

Med., 7-10 min.

Emphasize the bank reconciliation format (“book” vs. “bank”)

and solve for the beginning balances.

P5.26.

3

Med., 7-10 min.

P5.27.

5

Med., 7-10 min.

Part b can be used to explain why the allowance method is

conceptually superior to the direct write-off method.

P5.28.

5

Med., 10-12 min.

P5.29.

5

Med., 7-10 min.

Excellent “T–accounts” problem.

P5.30.

5

Med., 7-10 min.

See P5.29. Good homework assignment.

P5.31.

7, 8

Med., 12-15 min.

Basic FIFO-LIFO problem using periodic.

P5.32.

7, 8

Med., 12-15 min.

See P5.31. Good in-class demonstration problem.

P5.33.

7, 8

Med.-Hard,

15-20 min.

cost of goods sold recognition (periodic vs. perpetual).

Students should review Business in Practice—The Perpetual

Inventory System before attempting this problem. Emphasize

the Balance Sheet—Income Statement link, and the timing of

Chapter 5 Accounting for and Presentation of Current Assets

ASSIGNMENT OVERVIEW (continued):

NO.

LEARNING

OBJECTIVES

DIFFICULTY &

TIME ESTIMATE

OTHER

COMMENTS

P5.34.

15-20 min.

7-10 min.

attempting this problem.

12-15 min.

stress the importance of inventory valuation.

C5–38.

5, 7

Med.-Hard,

12-15 min.

Take a quick look at the solutions. Parts a and b provide an

opportunity to discuss how to “read between the numbers” to

make better use of your knowledge about a company’s

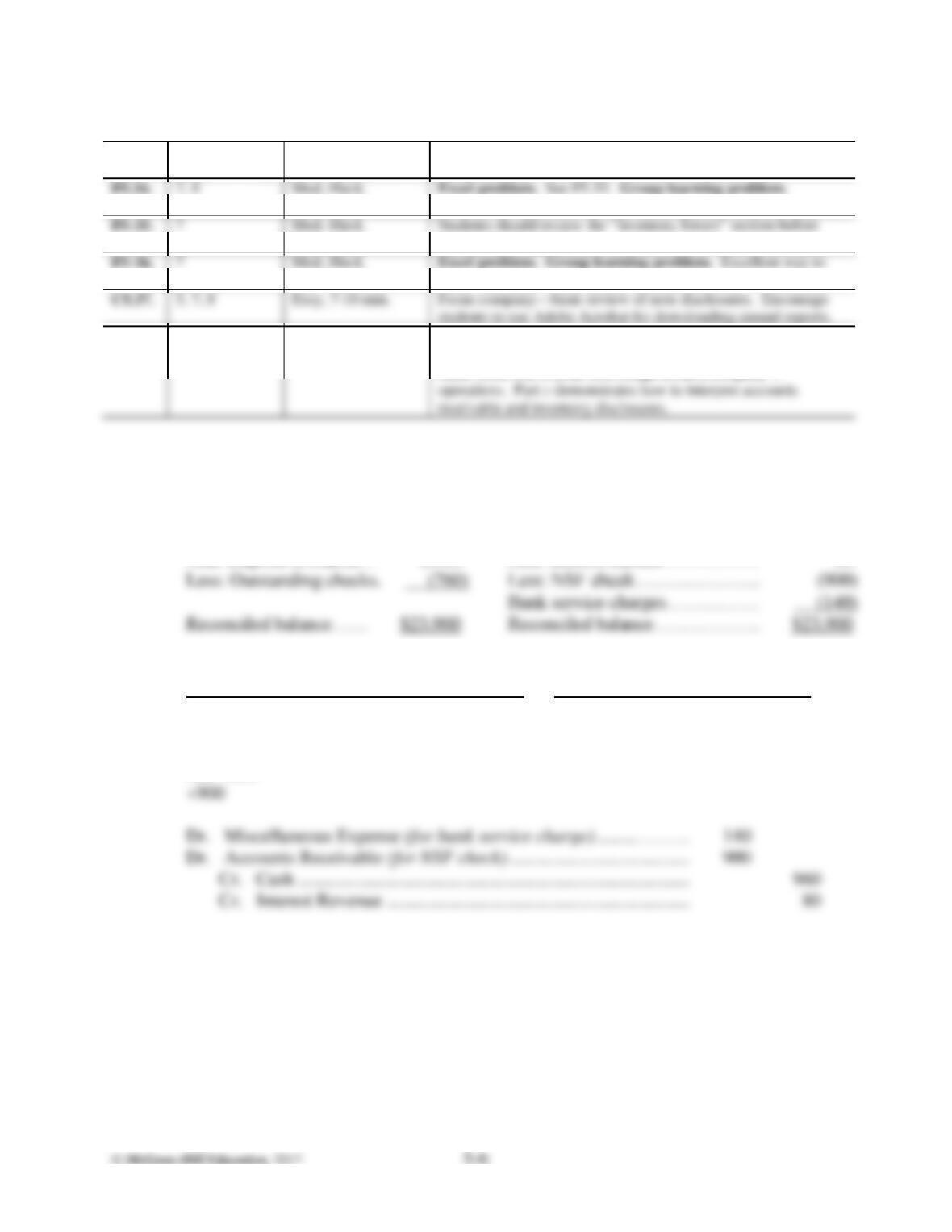

SOLUTIONS:

M5.1.

Balance per bank………

$22,260

Balance per books………………

$24,860

Add: Deposit in transit…

2,400

Add: Interest earned…………….

80

Less: Outstanding checks.

(760)

Less: NSF check…………………

Bank service charges……………

Reconciled balance……

$23,900

Reconciled balance………………

$23,900

M5.2.

a.

Balance Sheet Income Statement .

Assets = Liabilities + Stockholders’ Equity Net income = Revenues – Expenses

Cash Int.Rev. Misc.Exp.

-960 +80 -140

Acc. Rec.

b.

The cash amount to be shown on the balance sheet is the $23,900 reconciled amount.

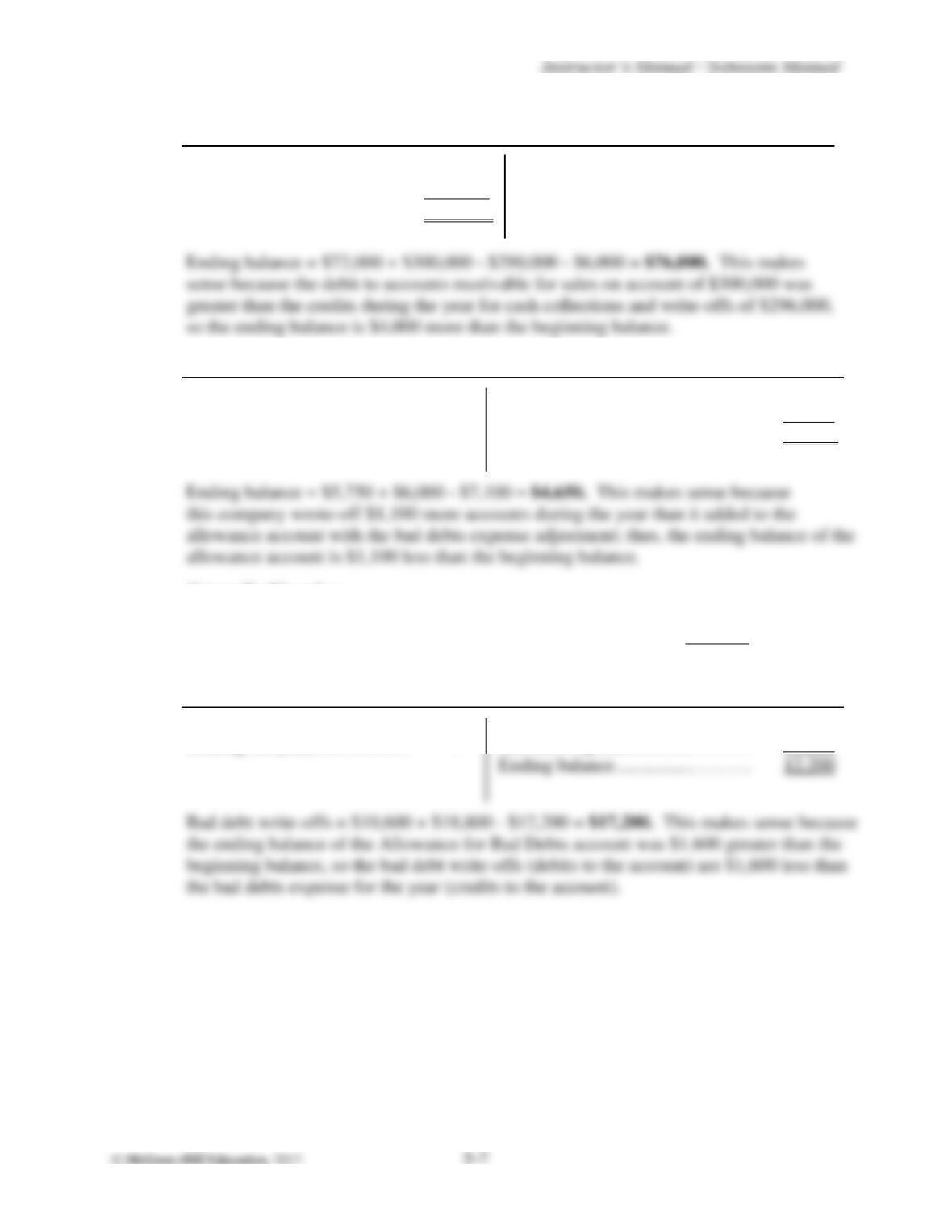

M5.3.

Accounts Receivable

Beginning balance ……………… 72,000 Cash collections …………………. 290,000

Sales on account ………………… 300,000 Accounts written off ………… 6,000

Ending balance ………………….. ? .

Allowance for Bad Debts

Bad debt write-offs Beginning balance………..………. 5,750

(During the year) ……………….. 7,100 Bad debt expense …………………. 6,000

Ending balance …………….………. ? .

Net realizable value:

Accounts receivable ……………………………………………………..…… $76,000

Less: Allowance for bad debts ………………………………………..…… (4,650) $71,350

M5.4.

Allowance for Bad Debts

Bad debt write-offs Beginning balance………..………. 10,600

(During the year) ……………….. ? Bad debt expense………….………. 18,800

M5.5.

Calculation ending inventory in units:

Beginning inventory .. ……….. ……….. ……….. ……….. ……….. ……….. 400 units

Purchase 1 …… ……….. ……….. ……….. ……….. ……….. ……….. ……….. 500 units

Calculation of cost of goods sold amounts:

a. ——- FIFO ——- b. ——- LIFO ——-

Beginning inventory.. 400 @ $10 = $4,000 Purchase 2 … ……. 300 @ $14 = $4,200

Calculation of ending inventory amounts:

a. ——- FIFO ——- b. ——- LIFO ——-

Purchase 2 …… ……….. 300 @ $14 = $4,200 Beg. inventory….. 400 @ $10 = $4,000

M5.6.

a.

b.

Beginning inventory .. ……….. ……….. ……….. 600 units @ $20 per unit = $ ?

May purchases ……….. ……….. ……….. ……….. 1,200 units @ ? per unit = 26,400

Solution approach:

Use the information available to solve for the missing information.

Number of units purchased in October = 2,600 – 600 – 1,200 = 800 units

Number of units sold = 2,600 – 1,100 = 1,500 units

Calculation of cost of goods sold amounts:

——— FIFO ——— ——— LIFO ——–

Beginning inventory.. 600 @ $20 = $12,000 October purchases.… 800 @ $24 = $19,200

M5.6.

b.

Ending inventory ……. ……….. $25,800 Ending inventory………………. $23,000

(continued)

Calculation of ending inventory amounts:

——— FIFO ——— —–—- LIFO ——–

October purchases ….. 800 @ $24 = $19,200 Beg. inventory……. 600 @ $20 = $12,000

E5.7.

Balance per bank…………

$ 746

Balance per books………………….

$1,688

Less: Outstanding checks

Error in recording check

($26 + $100)……………

(126)

(as $46 instead of $64)……………

Reconciled balance………

Reconciled balance………………..

E5.8.

Balance per bank…………

$9,810

Balance per books………………….

$9,488

Add: Deposit in transit……

1,260

Add: Interest earned……………….

Less: Outstanding checks…

(1,890)

Less: Check charge…………………

Error in recording payment………..

Reconciled balance…………………

$9,180

E5.9.

a.

Balance Sheet Income Statement .

Assets = Liabilities + Stockholders’ Equity Net income = Revenues – Expenses

Accounts Accounts

b.

The cash amount to be shown on the balance sheet is the $1,520 reconciled amount.

E5.10.

a.

Balance Sheet Income Statement .

Assets = Liabilities + Stockholders’ Equity Net income = Revenues – Expenses

Cash Acc. Pay. Int.Rev. Misc.Exp.

-308 -360 +108 -56

E5.11.

Allowance for Bad Debts

Bad debt write-offs 1/1/16 balance …………….… $26,800

(from 1/1 to 11/30) ……………… ? Bad debt expense

(from 1/1 to 11/30) ……… 42,924

11/30/16 balance ………… $19,526

Adjustment required (12/31/16)… ?

12/31/16 balance …………… $19,000

a.

Solution approach: The bad debt write-offs from January through November can be

determined by subtracting the November 30 balance from the total of the beginning

b.

The adjustment required at December 31, 2016 can be determined by comparing the

November 30 balance in the allowance account to the desired ending balance.

Bad debt expense adjustment = $19,526 – $19,000 = $526