CHAPTER

4

The Bookkeeping Process and

Transaction Analysis

CHAPTER OUTLINE:

I. The Bookkeeping/Accounting Process

II. The Balance Sheet Equation: A = L + SE

A. Stockholders’ Equity expanded:

1. SE = Paid-in Capital + Retained Earnings

3. Net income = Revenues – Expenses

4. SE = Paid-in Capital + Retained Earnings (beginning) + Revenues – Expenses

B. The Balance Sheet Equation expanded:

A = L + PIC + Retained Earnings (beginning) + Revenues – Expenses

III. Bookkeeping Jargon and Procedures

A. Transactions recorded in a journal, then posted to an account in the ledger.

B. Accounts use a “T” format

1. Left side of “T” is debit

1. Debit: Assets and expenses

2. Credit: Liabilities, stockholders’ equity, and revenues

D. Journal entries

IV. Effect of Transactions on the Financial Statements (Horizontal Model)

Chapter 4 The Bookkeeping Process and Transaction Analysis

VI. Transaction Analysis Methodology

A. Five questions:

1. What’s going on?

2. What accounts are affected?

3. How are they affected?

4. Does the balance sheet balance? (Do the debits equal the credits?)

5. Does my analysis make sense?

TEACHING/LEARNING OBJECTIVES:

Principal:

1. To have the student understand how transactions affect the financial statements.

3. To have the student learn to use the financial statement horizontal model to reason through

the impact of transactions on the financial statements.

Supporting:

4. To have the student learn to use the T-account model and understand the effect of a journal

entry.

5. To have the student understand why adjusting entries are necessary, and to see that they

result in more meaningful financial statements.

TEACHING OBSERVATIONS:

1. Develop the expanded balance sheet equation by relating net income to stockholders’ equity

(retained earnings) and explaining that income statement preparation is made easier if

3. Review the articulation of the income statement and balance sheet in Exhibit 4-2.

4. The normal balance and debit/credit behavior of T-accounts can be developed from the

expanded equation:

a. Assets = Liabilities + Stockholders’ Equity + Revenues – Expenses

d. Accounts to the left (or debit side) of the equal sign and vertical line have a normal balance

that is a debit. If a debit balance is normal, increases will be debits, and decreases will be

credits; it’s just the opposite for accounts on the right side.

6. Explain that the horizontal model directly illustrates the effects of transactions on the balance

7. Explain that in the horizontal model an increase in an expense is a negative amount because

an expense reduces net income, which reduces retained earnings and stockholders’ equity.

8. Introduce adjusting entries as changes in account balances needed to improve the accuracy of

Problem 4-28 can be used as an in-class demonstration of the 5 question analytical process.

Chapter 4 The Bookkeeping Process and Transaction Analysis

10. Students are easily confused by alternative methods of recording certain transactions (e.g.,

the purchase of supplies can be debited either to supplies expense or the supplies asset).

11. It is recommended that the horizontal model and the T-account model be used to help

students get a picture of the activity in an account, and/or to solve for the amount of an

12. “Matrix” assignments (see M4-1, M4-2, and E4-7 through E4-12) can be used to emphasize

student understanding of the effect of transactions on the financial statements. The same

format can be used on quizzes and exams. After subsequent chapters have been covered,

Instructor’s Manual / Solutions Manual

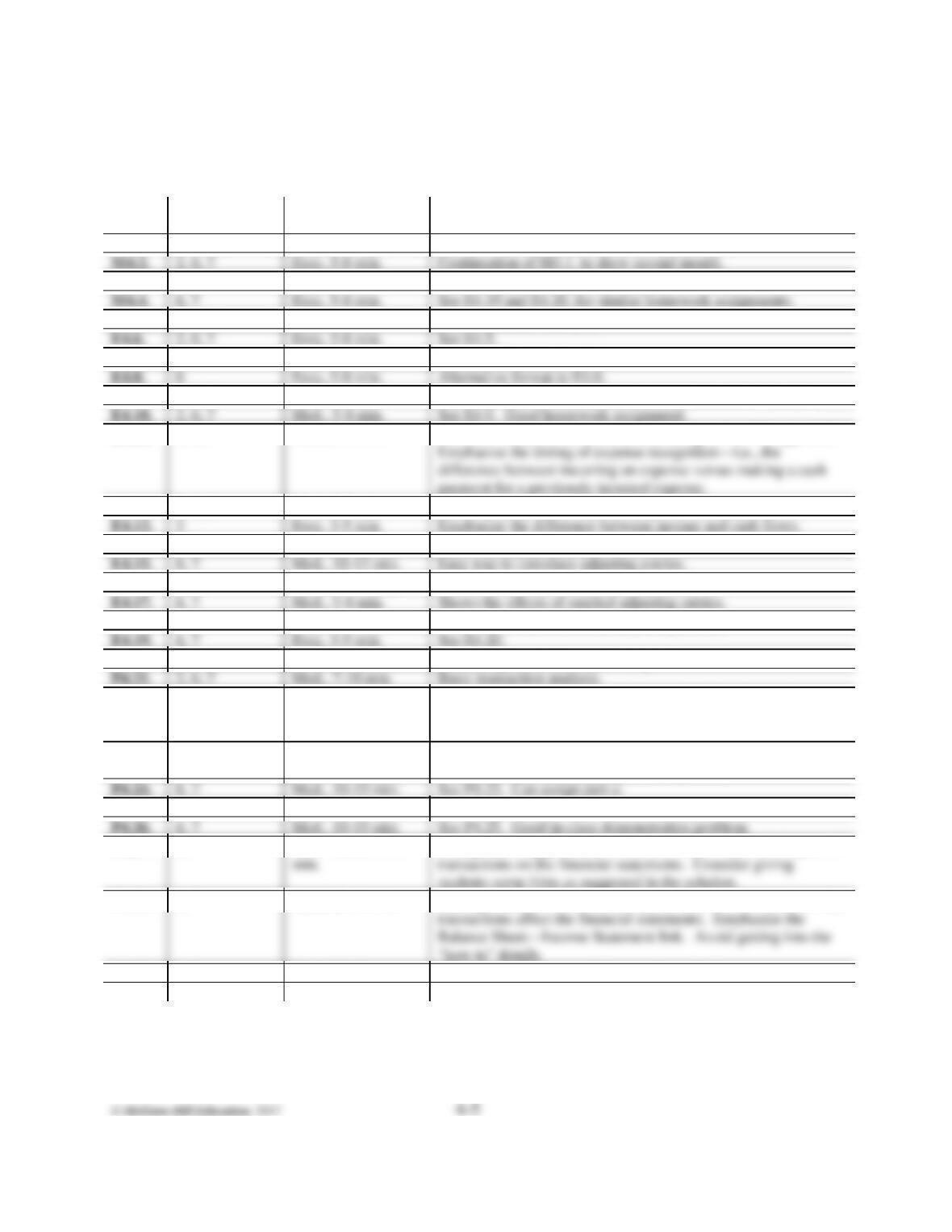

ASSIGNMENT OVERVIEW:

NO.

LEARNING

OBJECTIVES

DIFFICULTY &

TIME ESTIMATE

OTHER

COMMENTS

M4.1.

2, 6, 7

Easy, 5-8 min.

Basic transaction analysis without numbers.

M4.2.

2, 6, 7

Easy, 5-8 min.

Continuation of M4.1. to show second month.

M4.3.

6, 7

Easy, 5-8 min.

Use to emphasize T-account analysis.

M4.4.

6, 7

Easy, 5-8 min.

See E4.19 and E4.20. for similar homework assignments.

E4.5.

2, 6, 7

Easy, 5-8 min.

Basic transaction analysis.

E4.6.

2, 6, 7

Easy, 5-8 min.

See E4.5.

E4.7.

6

Easy, 5-8 min.

Alternative format to E4.5.

E4.8.

6

Easy, 5-8 min.

Alternative format to E4.6.

E4.9.

2, 6, 7

Med., 5-8 min.

Emphasize the effects of transactions on financial statements.

E4.10.

2, 6, 7

Med., 5-8 min.

See E4.9. Good homework assignment.

E4.11.

2, 6, 7

Med., 5-8 min.

Parts d, e, and f can be demonstrated using a time-line approach.

E4.12.

2, 6, 7

Med., 5-8 min.

Excel exercise. Good in-class demonstration exercise.

E4.13.

3

Easy, 3-5 min.

Emphasize the difference between income and cash flows.

E4.14.

6,7

Easy, 3-5 min.

See E4.13.

E4.15.

6, 7

Med., 10-12 min.

Easy way to introduce adjusting entries.

E4.16.

6, 7

Med., 10–12 min.

See E4.15. Good homework assignment.

E4.17.

6, 7

Med., 5-8 min.

Shows the effects of omitted adjusting entries.

E4.18.

6, 7

Med., 5-8 min.

Shows the effects of omitted adjusting entries.

E4.19.

6, 7

Easy, 3-5 min.

See E4.20.

E4.20.

6, 7

Med., 10–15

Use to emphasize T-account analysis.

P4.21.

2, 6, 7

Med., 7-10 min.

Basic transaction analysis.

P4.22.

1

Med., 10-12 min.

Group learning problem. Assign with P4.21. Emphasize the

need for liquidity and profitability planning. Ask “What went

wrong with this company?”

P4.23.

6, 7

Med., 10-15 min.

Emphasizes the form of income statement presentation.

CAN USE LATER as a Chapter 9 assignment.

P4.25.

6, 7

Med., 10-15 min.

See P4.23.

P4.26.

6, 7

Med., 10-15 min.

See P4.25. Good in-class demonstration problem.

P4.27.

6, 7

Med.-Hard, 10-20

Group learning problem. Excellent way to stress the impact of

P4.28.

6, 7

Hard, 20-30 min.

Excel problem. Worksheet should be used to show students that

C4.29.

6, 7

Hard, 25-35 min.

Group learning case. Makes students think!

C4.30.

6, 7

Hard, 25-35 min.

Group learning case. Makes students think!

Chapter 4 The Bookkeeping Process and Transaction Analysis

SOLUTIONS:

M4.1.

a.

Transaction/Adjustment A = L + SE Net Income

Issued common stock to the initial + Cash + Common

stockholders in exchange for their Stock

cash investment……………………..

M4.2.

a.

b.

Transaction/Adjustment A = L + SE Net Income

Paid wages that had been accrued – Cash – Wages

at the end of the prior month………… Payable

Collected accounts receivable from + Cash

sales recorded in the prior month…… – Acc. Rec.

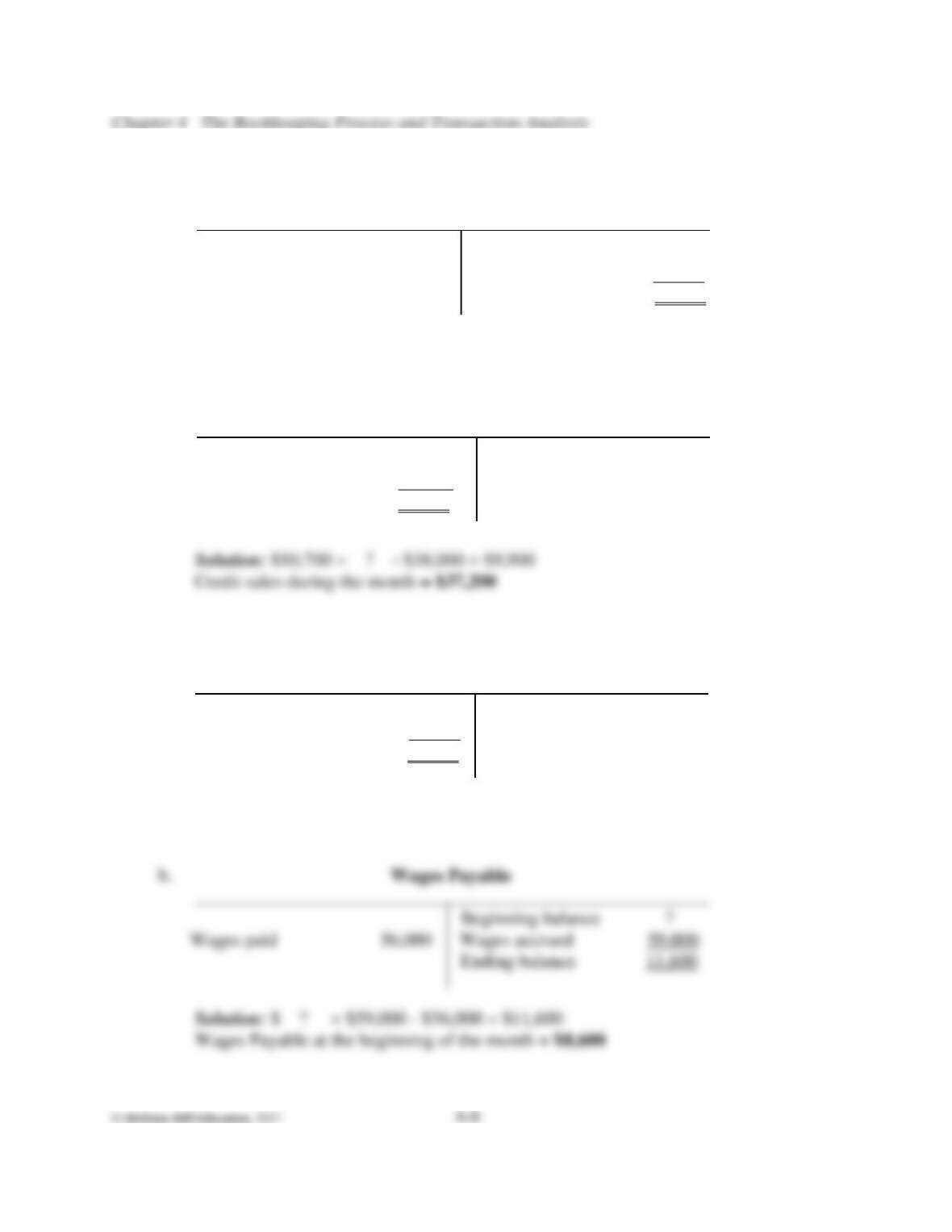

M4.3.

a.

Accounts Payable

Beginning balance 9,000

Payments to suppliers ? . Purchases on account 18,300

Ending balance 10,200

Solution: $9,000 + $18,300 – ? = $10,200

Payments to suppliers during the month = $17,100

b.

Accounts Receivable

Beginning balance 10,700 Collections from

Credit sales ? customers 38,000

Ending balance 9,900

M4.4.

a.

Supplies

Beginning balance 4,800

Supplies purchased 15,600 Supplies used ?

Ending balance 6,400

Solution: $4,800 + $15,600 – ? = $6,400

Supplies used during the month = $14,000

b.

Wages Payable

Net income for the month: Revenues $40,000 – Expenses $32,700 = Net income $7,300

Net income (this exercise ignores income taxes)…………………..

E4.5.

Assets = Liabilities + Stockholders’ Equity

b.

d.

-2,800 -2,800

-18,000 +30,000 +12,000

-2,400 +8,400 +6,000

+7,800 +19,200 –18,000 +27,000 – 18,000

+6,320 -6,320

k.

l.

-9,440 -9,440

______ ______ ______ _____ ______ ______ ______ _____ ______ ______

16,980 + 12,880 + 12,400 + 3,500 = 10,000 + 12,460 + 16,000 + + 40,000 – 32,700

Month-end totals: Assets $45,760 = Liabilities $22,460 + Stockholders’ equity $23,300

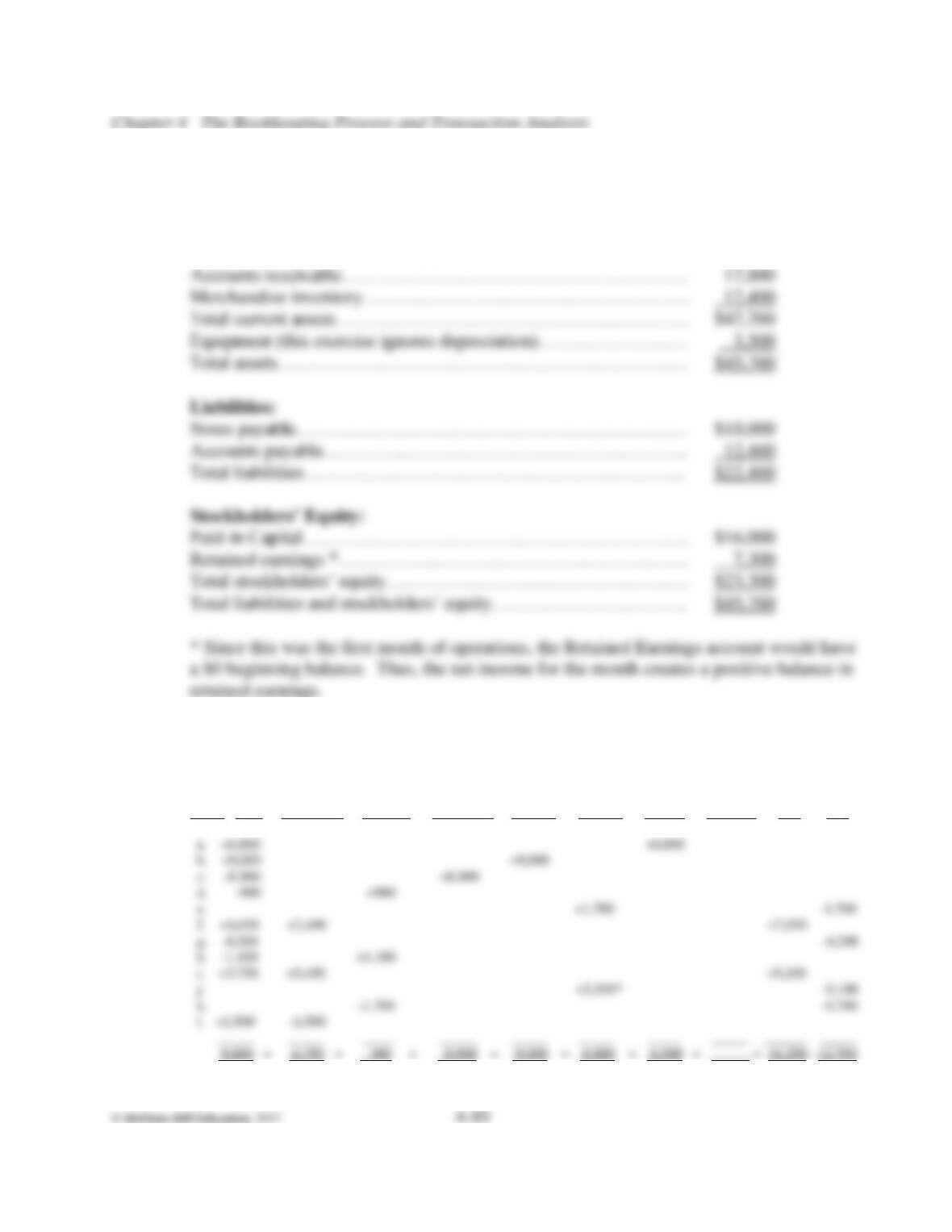

E4.5.

(continued)

BLUE CO. STORES, INC.

Balance Sheet

Assets:

Cash…………………………………………………………………

$16,980

Merchandise inventory……………………………………………..

12,400

Liabilities:

Notes payable………………………………………………………

$10,000

$22,460

Retained earnings *…………………………………………………

7,300

Total liabilities and stockholders’ equity…………………………..

$45,760

E4.6.

Assets = Liabilities + Stockholders Equity

Trans- Accounts Notes Accounts Paid-in Retained

action Cash + Receivable + Supplies + Equipment = Payable + Payable + Capital + Earnings + Rev – Exp