E16.17.

Product A

Product B

Contribution margin per unit…………………………..

$ 300

$ 400

Machine hours required per unit……………………….

6

8

Contribution margin per machine hour…………………

($50 contribution margin per machine hour x 1,200 machine hours).

E16.18.

Product X

Product Y

Product Z

Selling price…………………………………

$100

$ 80

$ 25

Variable costs………………………………

70

40

20

Contribution margin per unit……………….

$ 30

$ 40

$ 5

Machine hours per unit……………………..

Contribution margin per machine hour…….

$ 20

Monthly demand (units)……………………

Machine hours per unit……………………..

Total machine hours required………………

To assign the 1,200 available machine hours to achieve the most profitable mix of

products, start by producing the product with the highest contribution per machine

hour, then the next highest, and so on.

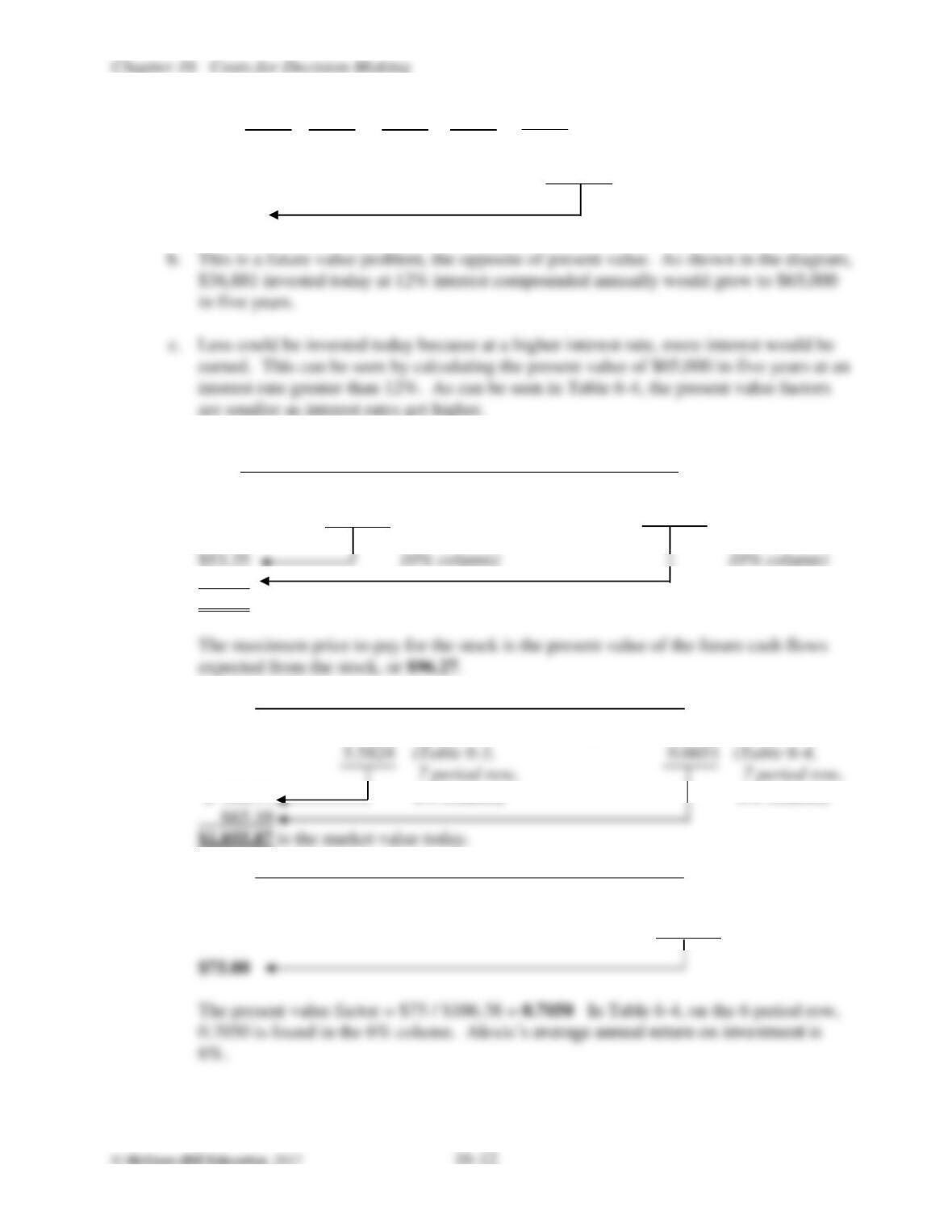

E16.19.

a.

0 1 2 3 4 5

$65,000

0.5674 (Table 6-4, 5 period row,

12% column)

$36,881

in five years.

E16.20.

a.

0 8

Dividend = $10 per year Market price = $92

5.3349 (Table 6-5, 0.4665 (Table 6-4,

8 period row, 8 period row,

42.92

$96.27

b.

0 5

Interest = $ 70 per year Maturity value = $1,000

$ 390.77 6% column) 6% column)

c.

0 6

$106.38

???

E16.21.

a.

If the investment is too high, the net present value will be too low.

If the cost of capital is too low, the net present value will be too high.

c.

If the cash flows from the project are too high, the net present value will be too high.

d.

If the number of years over which the project will generate cash flows is too low, the

net present value will be too low.

E16.22.

a.

to provide for a margin of error in the estimates used in the capital budgeting

calculations, and to recognize the risk associated with proposed capital expenditures.

ROI of 9%, because that rate of return reflects the composite expectation of all

E16.23.

a.

b.

Because the net present value is negative, the internal rate of return on this project will

be lower than the cost of capital of 10%.

0 1 2 3 4 5 6 7 8

5.3349 (Table 6-5 0.4665 (Table 6-4

$(85,000) 8 period row, 8 period row,

E16.24.

a.

Investment in machinery and equipment………………………………

$(6,700,000)

Investment in working capital …………………………………………

(1,200,000)

Annual cash inflows, by year: …………………………………………

2016 = $2,000,000 * 0.9259 …………………………………………

1,851,800

2017 = 3,600,000 * 0.8573 …………………………………………

3,086,280

Salvage value = $1,000,000 * 0.7938 …………………………………

Release of working capital = $1,200,000 * 0.7938.……………………

Net present value ………………………………………………………

b.

the cost of capital which is 8%.

Because the net present value is positive, the internal rate of return will be higher than

E16.24.

(continued)

c.

Estimate:

Effect if estimate is less than actual:

Investment cost …………………

Actual NPV and ROI will be less than indicated.

Annual cash inflows ……………

Actual NPV and ROI will be more than indicated.

Cost of capital……………………

Actual NPV and ROI will be less than indicated.

E16.25.

a.

investment of $24,000). Therefore, the return on investment is greater than 20%.

The payback period should not carry much weight at all, because it does not recognize

the time value of money.

The net present value is positive $2,220 (present value of inflows of $26,220 less the

E16.26.

a.

The present value of an annuity = (Annuity amount * present value factor). If the

present value of the annuity equals the investment, the IRR will equal the discount rate.

b.

Annual net cash flow required…………………………………………

$600,000

Annual direct cash costs (50%) ……………………………………..…

300,000

Annual total revenues required…………………………………………

$900,000

Procedures capacity ……………………………………………………

Utilization factor ………………………………………………………

Number of procedures per year …………………………..……………

Fee per procedure ($900,000 / 6,000 procedures) ……………..………

P16.27.

a.

Relevant costs for the special sales order include the following:

Per Gallon

Raw materials.………………………….……………

$3.00

Direct labor ……………………………….…………

1.50

Variable overhead……………………………………

1.00

Distribution …………………………………………

1.50

Total relevant costs per gallon ………………………

$7.00

b.

Per Gallon

Sales price ……………………………………………

$8.00

Less: relevant costs ………………..…………………

7.00

Contribution margin per gallon………………………

$ 1.00

Daily sales in gallons…………………………………

Daily increase in operating income ….………………

P16.27.

(continued)

c.

Since Delmar is now operating at full capacity, relevant costs for the special sales order

would include any forgone contribution margin (opportunity cost) on regular sales

given up by Delmar to fulfill the special sales order:

Per Gallon

Current sales …………………………………………

$10.00

Less variable costs……………………………………

Raw materials ………………………………………

3.00

Direct labor…………………………………………

1.50

Variable overhead …………………………………

1.00

Distribution (on current sales)………………………

6.50

Current contribution margin …………………………

$ 3.50

Current sales …………………………………………

$10.00

Per Gallon

Current contribution margin …………………………

Contribution margin from special order………………

Daily sales in gallons…………………………………

d.

When Delmar is operating under conditions of idle capacity, the only relevant costs

incurred in producing the gallons of root beer needed to fulfill the special order are the

incremental variable costs – Delmar would not be giving up any of their current sales.

P16.28.

a.

Step 1: Calculate total amount of fixed costs before the addition of plant capacity:

Current total cost per unit ……………………………………

$ 76

Less: Variable cost per unit ……………………….…………

60

Fixed cost per unit……………………………………………

$ 16

Units at full capacity…………………………………………

* 75,000

Total fixed costs …………………………..…………………

Original total fixed cost………………………………………

Annual increase in fixed costs ($6,000,000 / 10 years) …..…

Total fixed costs ………………………..……………………

Fixed costs per unit at full capacity: $1,800,000 / 100,000 = $18

P16.28.

(continued)

a.

Step 3: Calculate cost per unit after the addition of plant capacity:

Variable cost per unit ……………………………..…………

$ 60

Fixed cost per unit……………………………………………

18

Cost per unit …………………………………………………

$ 78

b.

because the capacity has already been added (sunk cost) and the commissions and

freight are not relevant because they will not be paid (avoidable cost) on the special

order.

Relevant costs associated with the special order from LawnPro.com would include

variable manufacturing costs per motor ($60) and the costs associated with storing

the motors in the PMI warehouse to await shipment. Fixed costs are not relevant

c.

Yes, assuming no other option currently exists to provide more than $15 contribution

margin per motor or that the costs associated with storing each motor in the PMI

warehouse will not exceed $15 per motor.

Selling price per unit…………………………………………

$ 75

Less variable cost per unit……………………………………

60

Contribution margin per unit…………………………………

$ 15

d.

No, because the full absorption cost per unit will indicate a loss on the sale.

Selling price per unit…………………………………………

$ 75

Less full cost per unit ……………………..…………………

Loss per unit …………………………………………………

e.

sale, will LawnPro.com expect this price of future additional orders if the Web site

sales prove to be successful, whether there are there more profitable opportunities on

the horizon for the use of the new additional capacity, or whether the sale at this

discounted price is in violation of the Robinson-Patman Act.

Key qualitative factors to consider would include whether PMI’s current customers

would expect the same $60 price if they became aware of the sale, whether PMI’s

current customers would stop doing business with them if they became aware of the

P16.28.

(continued)

f.

PMI will no longer have enough idle capacity to produce the motors needed to fulfill

the LawnPro.com special order without sacrificing sales to existing customers at the

normal selling price. Therefore, relevant costs, in addition to the relevant costs

described in part b, will now include an opportunity cost equal to the amount of

contribution foregone if PMI were to accept the special order:

Current sales in units…………………………………………

75,000

Expected increase in sales (75,000 * 20%) ………….………

15,000

Expected sales to current customers …………………………

90,000

Plant capacity in units ……………………….………………

Expected sales to current customers …………………………

Idle capacity in units…………………………………………

Selling price per unit…………………………………………

Less: Variable cost per unit ……….…………………………

Commission ($100 * 10%) ……………………………

Contribution margin per unit…………………………………

Sales to LawnPro.com in units ………………………………

20,000

Idle capacity in units…………………………………………

10,000

Lost sales to existing customers in units ….…………………

10,000

Contribution margin per unit…………………………………

$ 30

Opportunity cost of lost sales …………………………………

$ 300,000

g.

Calculation of operating income without the special order:

Sales (90,000 * $100) ……………………………………

$9,000,000

Less variable costs:

Manufacturing costs (90,000 * $60)……………………

$5,400,000

Commission (90,000 * $10) ……………………………

Contribution margin ………………………..……………

$2,700,000

Less fixed costs …………………….……………………

1,800,000

Operating income ……………………………..…………

$ 900,000

P16.28.

(continued)

g.

Calculation of operating income with the special order:

Sales (80,000 * $100)…………………………………….

$8,000,000

(20,000 * $75)………………………………………

1,500,000

$9,500,000

Less variable costs:

Manufacturing costs (100,000 * $60)…………………..

$6,000,000

Commission (80,000 * $10)…………………………….

800,000

6,800,000

Contribution margin………………………………………

$2,700,000

Less fixed costs…………………………………………..

1,800,000

Operating income…………………………………………

$ 900,000

P16.29.

a.

Sales………………………………………………………

$ 120,000

Variable operating expenses:

Cost of sales (food, beverages, and snack items @ 40%)

48,000

Food service items (spoons, napkins, etc.).……………..

1,800

Wages for part time employees..………………………..

24,000

73,800

Contribution Margin.……………………………………..

$ 46,200

Fixed operating expenses:

Utilities….………………………………………………

Convenience operation manager’s salary……………….

General manager’s salary……………………………….

9,000

Advertising………………………………………………

Insurance………………………………………………..

6,000

Property taxes……………………………………………

1,500

Food equipment depreciation……………………………

3,000

Building depreciation……………………………………

74,400

Operating loss…..…………………………………………

P16.29.

(continued)

b.

Note – relevant revenues and costs are those items that would be eliminated if the

segment is discontinued:

Relevant

Amount

Sales………………………………………………………

120,000

Cost of sales (food, beverages, and snack items @ 40%)..

48,000

Food service items (spoons, napkins, etc.)……………….

1,800

Wages for part time employees…………………………..

24,000

Utilities (50% of total)……………………………………

1,800

Convenience operation manager’s salary…………………

33,000

General manager’s salary…………………………………

Advertising……………………………………………….

2,700

Insurance…………………………………………………

1,500

Property taxes…………………………………………….

Food equipment depreciation…………………………….

Building depreciation…………………………………….

c.

Loss of contribution margin………………………………

$ (46,200)

Less direct fixed costs:

Utilities (50% of total)…………………………………

1,800

Convenience operation manager’s salary………………

33,000

Advertising…………………………………………….

2,700

Insurance………………………………………………

1,500

39,000

Decrease in operating income……………………………

d.

if the convenience operation were discontinued. For example, would it be more

profitable to replace the convenience operation with an additional service bay?

MMV should continue the convenience operation. The quantitative results of the

relevant cost analysis indicate that if MMV discontinued the convenience operation he

would see overall profits for this location decrease by $7,200 because he would lose

P16.30.

a.

Loss of contribution margin………………………………

$ (600,000)

Less direct fixed expenses………………………………..

296,000

Decrease in operating income……………………………

$ (304,000)

Operating income will decrease by $304,000 for the XYZ Company if it discontinues

Product A.

P16.30.

(continued)

b.

XYZ COMPANY

Segmented Income Statement

For the Year Ended December 31, 2016

Total

Company

Product A

Product B

Product C

Sales………………….….

$1,200,000

$ –

$480,000

$720,000

Variable expenses…….…

504,000

–

216,000

288,000

Contribution margin….…

$ 696,000

$ –

$264,000

$432,000

Direct fixed expenses……

112,000

–

Common fixed expenses…

720,000

–

288,000*

Operating income….……

from an operating income of $168,000 to an operating loss of $(136,000).

c.

XYZ COMPANY

Segmented Income Statement

For the Year Ended December 31, 2016

Total

Company

Product A

Product B

Product C

Sales…………………….

$2,400,000

$1,200,000

$480,000

$720,000

Variable expenses………

1,104,000

600,000

216,000

288,000

Contribution margin……

$1,296,000

$ 600,000

$264,000

$432,000

Direct fixed expenses…..

408,000

296,000

Segment margin………..

$ 888,000

$ 304,000

$224,000

$360,000

Common fixed expenses..

720,000

Operating income………

$ 168,000

d.

As explained in Chapter 15, a key feature of this more appropriately designed

segmented income statement is that common fixed expenses have not been arbitrarily

allocated to the segments. This approach more clearly illustrates that when a segment

is covering its direct expenses, it should not be discontinued. By comparing the results