Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

E14.16.

(continued)

Manufacturing overhead:

b.

The relevant cost would exclude the fixed manufacturing overhead, which is incurred

whether or not the extra pads are made.

P14.17.

July

August

September

Sales forecast …………………………………

$250,000

$220,000

$310,000

Cost of sales @ 54% …………………………

135,000

118,800

167,400

Purchases budget:

Beginning inventory …………………………

$410,000

$356,400

Purchases………………………………………

? .

? .

P14.18.

a.

Sales – Cost of goods sold = Gross profit, or

Cost of goods sold = Sales * (1 - gross profit ratio)

P14.18.

(continued)

b.

Purchases budget for May:

Jewelry

Watches

Beginning inventory (200% of current month’s CGS)

$ 99,200

$ 75,000

Add: Purchases………………………………………

? = 27,200

? = 26,250

P14.19.

a.

September

October

Sales forecast …………………….………………………

$42,000

$54,000

Purchases budget…………………………………………

37,800

44,000

Operating expense budget ……….………………………

10,500

12,800

Beginning cash ……..……………………………………

$40,000

b.

PrimeTime Sportswear's management should try to accelerate the collection of

accounts receivable, slow down the payment of accounts payable and accrued

P14.20.

a.

October

November

December

Sales forecast ……………………………

$54,000

$68,000

$59,000

Purchases budget…………………………

44,000

48,900

33,100

Cash receipts:

August 31 accounts receivable …..………

15,000

0

September sales …….……………………

21,000

18,900

Cash disbursements:

September purchases …………….………

$ 9,450

$ 0

October purchases ……..…………………

33,000

11,000

November purchases …..…………………

0

36,675

b.

December

January

February

Sales forecast …………………….………

$59,000

$59,000

$59,000

Purchases budget…………………………

33,100

33,100

33,100

Operating expense budget …………..……

16,100

16,100

16,100

P14.20.

(continued)

Cash disbursements:

December

January

February

November purchases ………..……………

$ 12,225

$ 0

$ 0

December purchases …..…………………

24,825

8,275

0

January purchases ……..…………………

0

24,825

8,275

February purchases …..…..………………

0

0

24,825

By reviewing the summarized cash budget results shown below for the six-month budget

period from September-February, it becomes clear that PrimeTime Sportswear must

obtain a seasonal bank loan during September to help finance the additional cost of

building up inventory levels to meet peak sales. Perhaps PrimeTime should apply for an

open line of credit. Obviously, it would not be possible to actually have a negative

balance in the cash account (as suggested by the budget results).

Sept.

Oct.

Nov.

Dec.

Jan.

Feb.

Beginning cash …………

$40,000

$ (225)

$(18,900)

$(34,600)

$(29,000)

$(18,100)

Total cash receipts ……..

20,000

36,000

45,900

58,300

60,100

56,050

P14.21.

Answer (and one possible numbered sequence of solving the problem):

April

May

June

Total

P14.21.

(continued)

April

May

June

Total

Less disbursements:

Purchase of inventory …………

3. 50

60

48

18. 158

Operating expenses

30

7. 40

16. 24

19. 94

Capital additions

34

8

15. 2

44

Solution approach:

1. $94 - $26 = $68

2. $94 + 20 (deficiency of cash available) = $114

4. Minimum month-end balance

5. $30 + 20 (deficiency of cash available) = $50

7. $108 - $60 - $8 = $40

8. $108 + $30 (excess of cash available) = $138

10. Ending cash balance from May is carried forward to beginning cash balance of

June = $30

12. Ending cash balance for the third quarter is the ending cash balance for June = $33

14. Total dividends = $8, and no dividends were paid in April and May

16. $82 - $48 - $2 - $8 = $24

17. $338 - $26 = $312

21. Borrowings from April

P14.22.

a.

SEATECH, INC.

Cash Budget

For the months of April, May, and June, 2016

April

May

June

For cost of goods sold/operating expenses incurred in:

March ………………………………………

$ 22,600

$

$

April…………………………………………

78,400

19,600

May …………………………………………

95,200

23,800

June …………………………………………

106,400

The monthly cash budgets would appear as follows (revisions shown in bold):

April

May

June

Beginning cash balance………………………

$ 14,000

$ 10,000

$ 10,000

Cash Receipts:

From cash sales made in current month ……

42,000

51,000

57,000

P14.22.

(continued)

April

May

June

Cash Disbursements:

For cost of goods sold/operating expenses incurred in:

March ………………………………………

$ 22,600

$

$

P14.23.

a.

April

May

June

Total

Expected sales in units

7,000

10,000

8,000

25,000

b.

Cash collections from:

April

May

June

Total

March sales

$132,000a

$132,000

April sales

112,000

$154,000

266,000

P14.23.

(continued)

April

May

June

Total

c.

Beginning inventory of

finished goods ……………

3,500

5,000

4,000

3,500

Units to be produced…………

8,500

9,000

8,500

26,000

Goods available for sale …….

12,000

14,000

12,500

29,500

d.

April

May

June

Total

Beginning inventory of

raw materials …………………

10,200

10,800

10,200

10,200

Purchases of raw materials ……

26,100

26,400

24,300

76,800

Raw materials available for use.

36,300

37,200

34,500

87,000

Desired ending inventory of

raw materials (40% of next

month’s estimated usage)b ……

(10,800)

(10,200)

(9,000)c

(9,000)

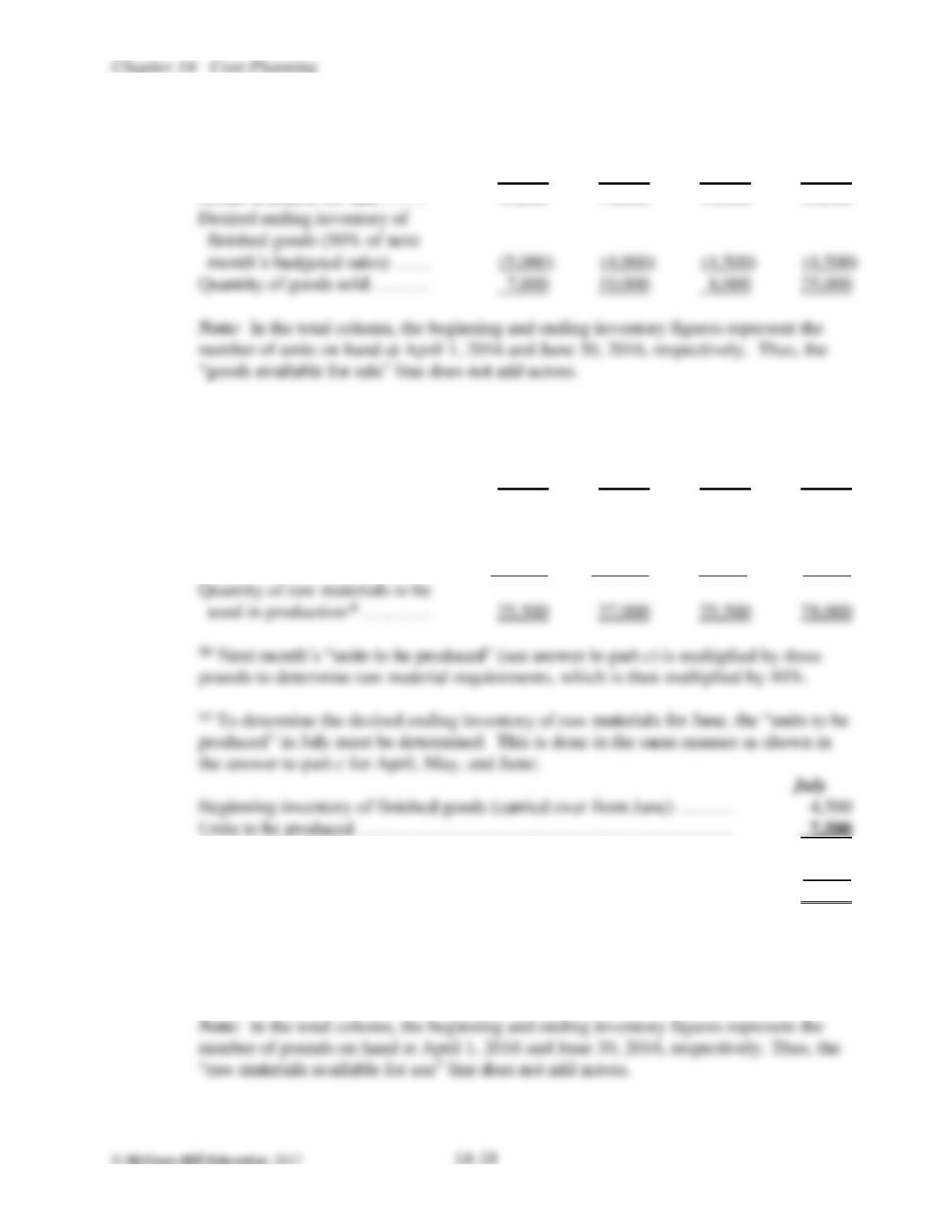

Goods available for sale…………………………………………………

12,000

Desired ending inventory of finished goods (50% of August’s sales) …

(3,000)

Quantity of goods sold …………………………………………………

9,000

7,500 * 3 pounds * 40% = 9,000

(d) “Units to be produced” each month (see answer to part c) * 3 pounds per unit.

P14.23.

(continued)

e.

Cash payments for:

April

May

June

Total

March purchases …………….

$ 26,280e

$ 26,280

April purchases ………………

125,280

$ 31,320

156,600

P14.24.

a.

October

November

December

Total

Expected sales in units ………

12,000

14,000

20,000

46,000

b.

Cash collections from:

October

November

December

Total

September sales………………

$499,200a

$ 499,200

October sales…………………

230,400

$460,800

691,200

c.

October

November

December

Total

Beginning inventory of

finished goods………………

4,800

5,600

8,000

4,800

Units to be produced…………

12,800

16,400

15,600

44,800