International Business

Geringer, McNett, Minor, Ball

Instructor Guide to Module 8

BONUS ACTIVITIES (additional resources not in the text)

VIDEO SUGGESTIONS

McGraw Hill’s collection of international business videos is available on pinterest at

https://pinterest.com/mheibvideos. The Foreign Exchange Market board is rich and varied,

updated monthly. It’s a great resource. See The BBC on Lithuania Changes from Litas to Euro

https://www.pinterest.com/pin/387591111656061819/ .

See “Out of the Ashes (Rebuilding the International Monetary System),“ posted by the IMF, at

https://www.youtube.com/watch?v=s2OeN-im044 /.

“Making Sense of SDRs” was uploaded by the IMF and offers a good introduction to the SDR.

See https://www.youtube.com/watch?v=s2OeN-im044/ .

To look at controversy about the international monetary system, you may want to suggest

students view “End of the International Monetary System Is Immanent,” an alarmist approach

by Jim Rickards on goldsilver.com, https://www.youtube.com/watch?v=s2OeN-im044/ .

TEAM EXERCISES

These may be done individually or in groups or teams, either in or out of class, for later class

presentation. Some are also appropriate for hybrid and online courses.

1. Islamic Financial Institutions

Many students are not aware of the difference between Islamic financial institutions and other

financial institutions. Assign small teams (5 students) to research Islamic financial institutions,

having each team focus on one topic. By dividing the topics, you can have all students focused on

aspects of Islamic finance and then share their knowledge in brief class or discussion board

presentations. Material from these presentations may be included in exams or quizzes. Here

are suggested topics:

▪ Summarize the history and religious basis of Islamic finances, including its

purpose.

▪ Summarize how Islamic financial institutions support trade

▪ Review the growth of Islamic banking and explain this phenomenon

▪ Review the role of women in Islamic banking

▪ Discuss the size and impact of Islamic banking

▪ Discuss non-bank institutions that play a role in Islamic finance

▪ Discuss where Islamic finance institutions play the largest roles and offer

explanations.

International Business

Geringer, McNett, Minor, Ball

Instructor Guide to Module 8

▪ Discuss the contributions Islamic banking has made in developing countries

2. Chinese devalue the yuan

The Chinese economy is the second largest in the world, yet its government controls the

3. Inflation rates by country

Assign small groups a country whose inflation rates they are to research. Good sites are

www.cia.gov and www.imf.org. Then ask them to list ways their findings would affect

international business decisions regarding that country. Report back to the class or using an

online collaboration tool to share findings with class members.

U.S. $3.50 range. Harvard Business Publishing

(https://cb.hbsp.harvard.edu/cbmp/pages/home) requires an account and offers downloadable

review copies for educators. The case prices begin in the $6 range.

“Debt and Development in Jamaica” describes the economic development problems faced by

Jamaica over most of the past half-century. This case allows students to explore the

complicated economic difficulties faced by Jamaica, which remains burdened by a self–

reinforcing set of interrelated factors, including high public debt, a sluggish private sector, an

inefficient public sector, poverty, and crime, among others. (Harvard)

“Can the Eurozone Survive?” covers the sovereign debt crisis that took Greece by storm in 2010

and spread to other European markets, Ireland and Portugal, with Spain and Italy next in line.

The European financial system became strained. Banks were found to be undercapitalized and

began to ration credit to the economy. The European Central Bank intervened to provide

liquidity to the system in order to avoid a credit crunch. Can the eurozone survive the storm?

International Business

Geringer, McNett, Minor, Ball

Instructor Guide to Module 8

cost of conducting business in Brazil, known as “Custo Brasil,” was hurting domestic

manufacturing, and incoming foreign investments threatened to overwhelm Brazilian markets.

Under President Dilma Rousseff, economic growth stagnated, and Brazil struggled to find the

best balance between reducing inflation, maintaining a flexible exchange rate, and improving

the competitiveness of Brazilian exports.

CONTROVERSIAL ISSUE

Inversions Still have Their Appeal

The U.S. Treasury restrictions tightened merger rules that went into effect recently, which make

it more difficult for U.S. companies to access their overseas cash unless it is taxed at U.S. rates

and tightens the conditions under which a merger can be an inversion. Inversions were once an

esoteric tax loophole, but in the past few years have come to be used more frequently as a way

to reduce tax rates. Essentially, they allow companies to lower their corporate tax rates by

buying foreign companies. Here’s how it works: the company either sets up or buys another

company in a country with a lower corporate tax rate and then calls the new country home.

Essentially, nothing moves. The company simply moves its legal address outside the U.S. Then

the company can move some of their profits to the new company and lower their tax rates.

U.S. corporate rates tend to be higher than those in many other countries. For example, U.K.

rates are around 20%, while U.S. rates are almost 40%, before tax credits. The average tax rate

in 2010 among the 10 most profitable U.S. companies was 25.4%, according to Forbes

(http://www.forbes.com/2011/04/13/ge-exxon-walmart-apple-business-washington-corporate-

taxes.html). So inversions lower tax rates and yet, the company still operates in the U.S.,

enjoying conditions supported by the taxes of other businesses and individuals.

Despite the Treasury clampdown, U.S. businesses continue to practice inversions as a part of

their corporate tax strategy. There were 14 inversions completed in 2014 and many are

planned as of mid-2015, including Coca Cola Enterprises (a bottler and distributor) and CF

Industries, both to the U.K.

• What is meant by an inversion deal?

• Another way to look at inversions is that they are examples of the benefits of

globalization. Companies are simply exploiting a comparative advantage. Evaluate this

viewpoint.

• A recent The Economist August 15, 2015) article suggests that U.S. tax law is

what has to change and that until it does, U.S. cash-rich companies abroad (who do not

pay U.S. taxes until profits are repatriated) will be targets for acquisition by non-U.S.

companies. Evaluate this perspective.

International Business

Geringer, McNett, Minor, Ball

Instructor Guide to Module 8

TEACHING SUGGESTIONS

1. This chapter is very important to students’ understanding of the importance of the

international monetary system and financial forces in international business.

2. Focusing on the boxed material and the case study will help students achieve the

objectives of the chapter. Answers for both the boxed material and case studies are provided in

this Instructor’s Manual.

3. The “Check Your Progress” section in the textbook will help in understanding chapter

content. These topics may be assigned as an outside class assignment. One of the problems in

giving textbook questions as outside assignments is that students frequently do not do the

assignments and wait for the instructor to give them the answers. Instructors can avoid these

problems in several ways: (1) collect assignments at random and assign a grade; (2) occasionally

give some of the same questions as a quiz, thus rewarding students who have done their

assignments; (3) have students hand in assignments and give credit for work submitted (or

penalties for work not submitted); and (4) call on students at random to present on specific

questions (giving a small number of points for correct answers).

4. Guest lecturers on the financial forces that affect management are a way to underscore the

importance of the information in this module. Possible guests include

• an economist who can speak to exchange rate volatility and its effects.

• a financial manager with experience in financial management would recount

some interesting experiences in addressing financial forces

• a retired IMF or Treasury employee whose work included some of the issues

addressed in this module

• someone who served in the Peace Corps might also have interesting

observations about financial forces and economic development

• faculty colleagues from other countries.

5. Students who view themselves as not strong in math may mistakenly think that this will be

a difficult chapter for them. The material is presented stressing the underlying concept to assist

such students.

6. To cover such a vast subject as financial forces and the monetary system in the short time

available is impossible. Students who become interested in this area might be encouraged to

explore an international finance course. Our aim is to help students realize that there are

financial forces and that international business managers must be aware of them and work with

them.

Tools & Tricks

International Business

Geringer, McNett, Minor, Ball

Instructor Guide to Module 8

CONNECT TOOLS FOR A SSESSEMENT OF LEARNING

Interactive Applications

Assigning Interactives

Consider assigning only 2 interactives per chapter. Interactive applications allow students to see

concepts in practice and assess higher order thinking skills. There are numerous exercises of

different types available. Click’n’drag, video cases, and case analysis are the types you will see

most frequently in this program.

Time-Saving Hints:

• Instructors may want to give students unlimited or multiple attempts on the first few

assignments so the students have a chance to learn and navigate the system before

selecting the option for one attempt only.

• The value of each question should probably be relatively low, since multiple questions

are usually assigned for each chapter. A good rule of thumb would be to make “Quiz

Questions” worth 1 point each and “Interactives” worth 5-10 points each since these

require more time and thought.

International Business

Geringer, McNett, Minor, Ball

Instructor Guide to Module 8

• Feedback given to students is time flexible. Selecting feedback to be displayed after the

assignment due date helps to limit students from giving the correct answers to other

students while the interactive is still available.

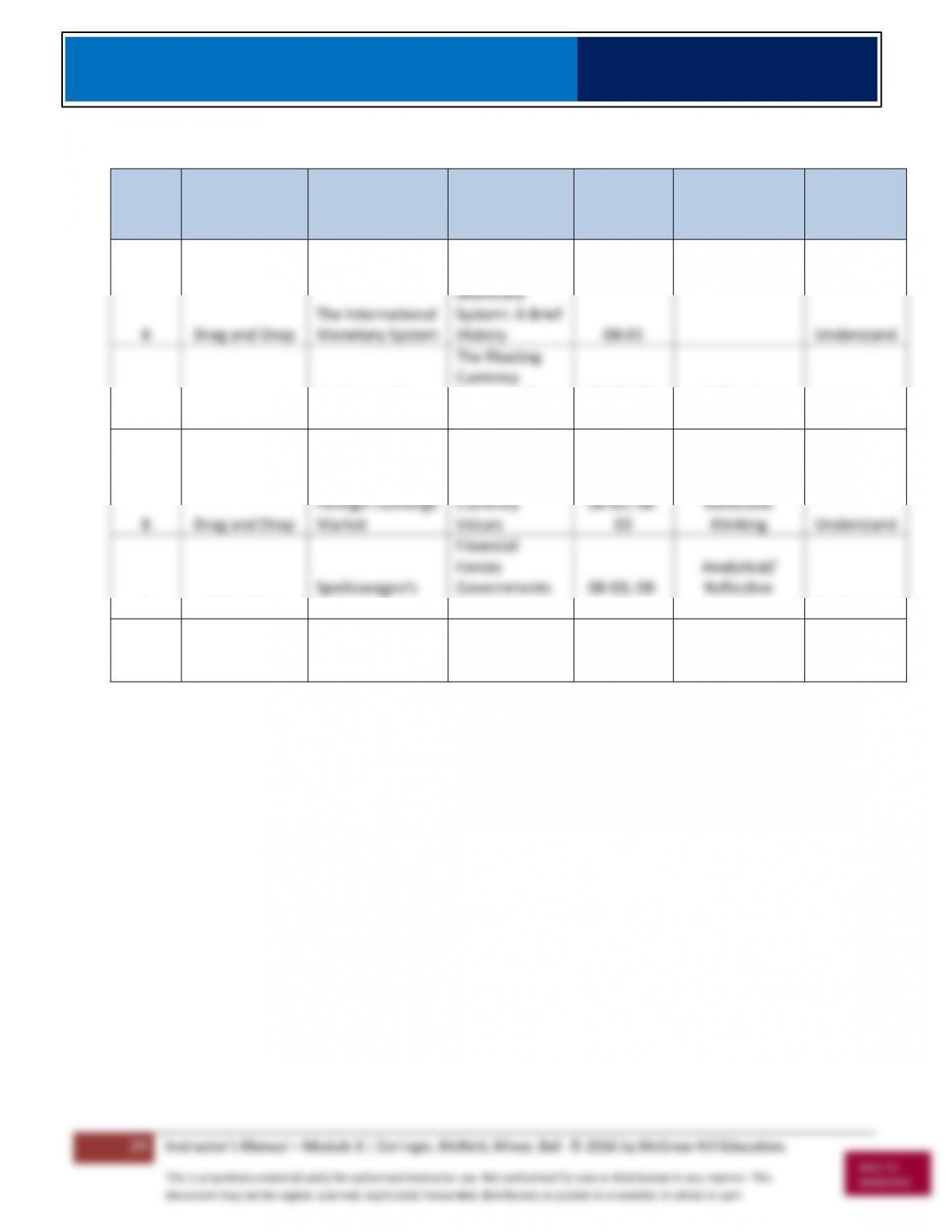

Connect Content Matrix

For every chapter, please refer to the Connect Content Matrix to see what application

exercises are available, what Learning Objectives they help reinforce/assess.

International Business

Geringer, McNett, Minor, Ball

Instructor Guide to Module 8

Module

Assignment

Type

Title

Topic(s)

Learning

Objective(s)

AACSB

Accreditation

Tagging

Bloom’s

Taxonomy

8

Drag and Drop

The International

Monetary System

The

International

Monetary

System: A Brief

History

08–01

Understand

8

Drag and Drop

Understanding

Exchange Rates

The Floating

Currency

Exchange Rate

System

08-02; 08-

03

Reflective

thinking

Understand

8

Drag and Drop

Foreign Exchange

Market

Financial

Forces:

Fluctuating

Currency

Values

08-02; 08-

03

Reflective

thinking

Understand

8

Video Case

Spolkswagen’s

Hedging Strategy

Financial

Forces

Governments

Can Exert

08-03; 08-

04

Analytical/

Reflective

thinking

Understand

8

Drag and Drop

The Balance of

Payments (BoP)

Explained

Balance-of–

Payments

08–05

Reflective

Thinking/ Apply

Application/

Understand