Chapter 12: Monopolistic Competition

Solutions Manual

Questions for Discussion

1. What is the source of Starbucks’ “confidence” in the News on page 266?

(LO 12-01)

Answer: Starbucks’ dominant market position gives it unique pricing flexibility.

2. Why do 4,000 new pizzerias open every year? Why do just as many close? (LO 12-04)

3. Name three products each for which you have (a) high brand loyalty and (b) low brand

loyalty. (LO 12-02)

4. If one gas station reduces its prices, must other gas stations match the price reduction?

Why or why not? (LO 12-02)

5. The News article on page 273 suggests that most consumers can’t identify their favorite

cola in blind taste tests. Why, then, do people stick with one brand? What accounts for

brand loyalty in bottled water (News, p. 268)? (LO 12-01)

6. How do new product offerings like breakfast sandwiches (News, p. 269) affect Starbucks’

sales and profits? What is the “saturation point” referred to in the News on page 272?

(LO 12-04)

1

© 2016 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any

manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole or part.

7. Why is the mix of output produced in competitive markets more desirable than that in

monopolistically competitive markets? (LO 12-03)

8. How would our consumption of cereal change if cereal manufacturers stopped advertising?

Would we be better or worse off? (LO 12-03)

9. Why are people willing to pay more for Dreyer’s ice cream when it has a Starbucks brand on

it? (LO 12-02)

Answer: Some people associate a certain taste or quality with the Starbucks name. If

Dreyer’s included this name on some of its ice cream, certain consumers would be

willing to pay extra for the added assurance of this taste and quality associated with the

Starbucks name.

10. According to the World View on page 275, what gives brand names their value?

(LO 12-02)

2

© 2016 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any

manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole or part.

Problems

1. What is the concentration ratio in an industry with the following market shares?

(LO 12-01)

Firm A 14.1 Firm C 5.2 Firm E 3.6 Firm G 1.6

Firm B 8.6 Firm D 4.0 Firm F 2.2 Other

Firms

60.7

Feedback: The concentration ratio is the proportion of total industry output produced by

2. If Starbucks raises its price by 5 percent and McDonald’s experiences a 0.3 percent

increase in demand for its coffee, what is the cross-price elasticity of demand?

(LO 12-02)

Feedback:

In this scenario the percentage change in quantity demanded for McDonald’s coffee is an

increase of 0.3 and the percentage increase in Starbuck’s price is 5.

3. In Figure 12.3, at what output rate is economic profit equal to zero? (LO 12-03)

3

© 2016 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any

manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole or part.

Feedback:

Barriers to entry are low in monopolistic competition. Hence, new firms will enter if

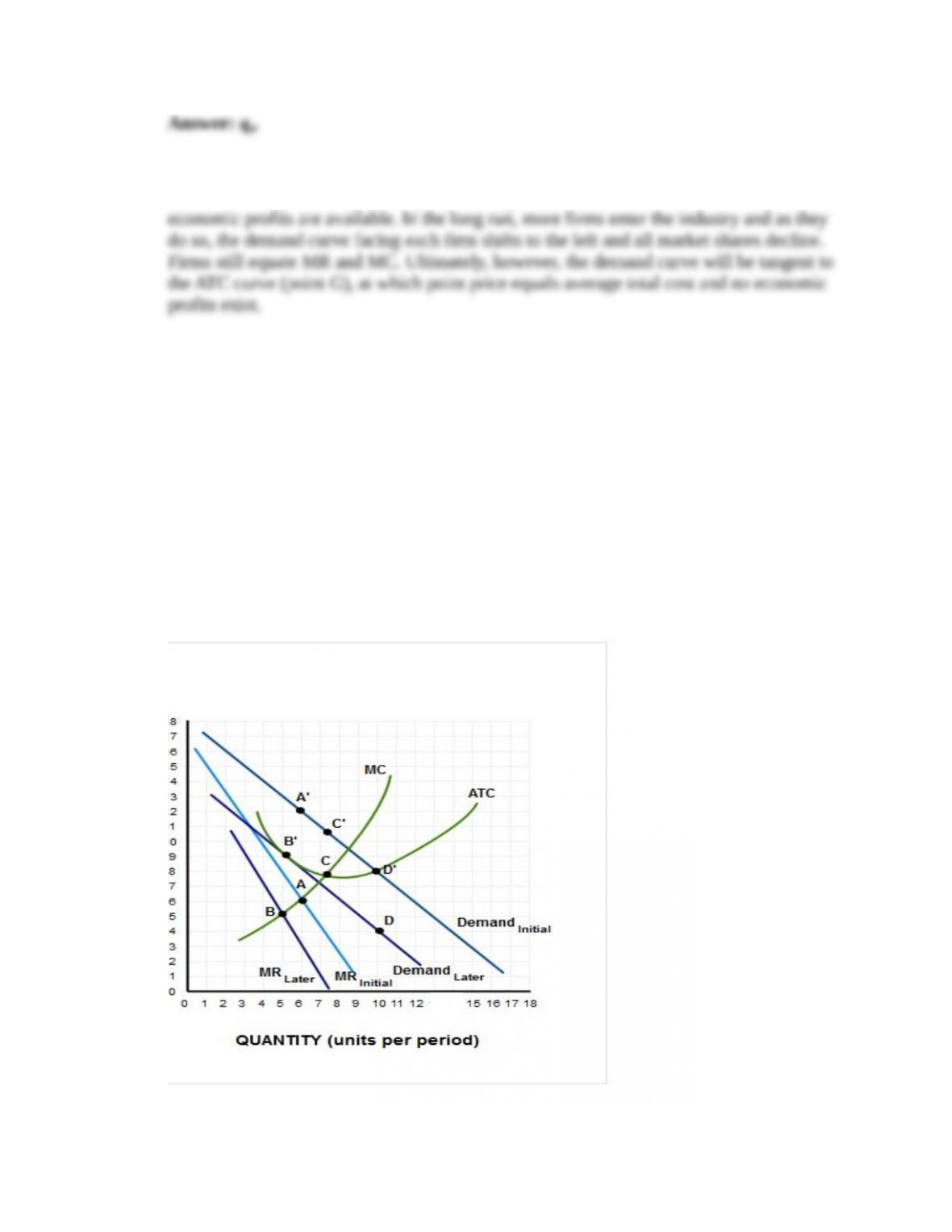

4. (a) Use the accompanying graph to illustrate the short-run equilibrium of a

monopolistically competitive firm.

(b) At that equilibrium, what is

(i) Price?

(ii) Output?

(iii) Total profit?

(c) Identify the long-run equilibrium of the same firm.

(d) In long-run equilibrium, what is (approximately)

(i) Price?

(ii) Output?

(iii) Total profit? (LO 12-03)

Answers:

4

© 2016 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any

manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole or part.

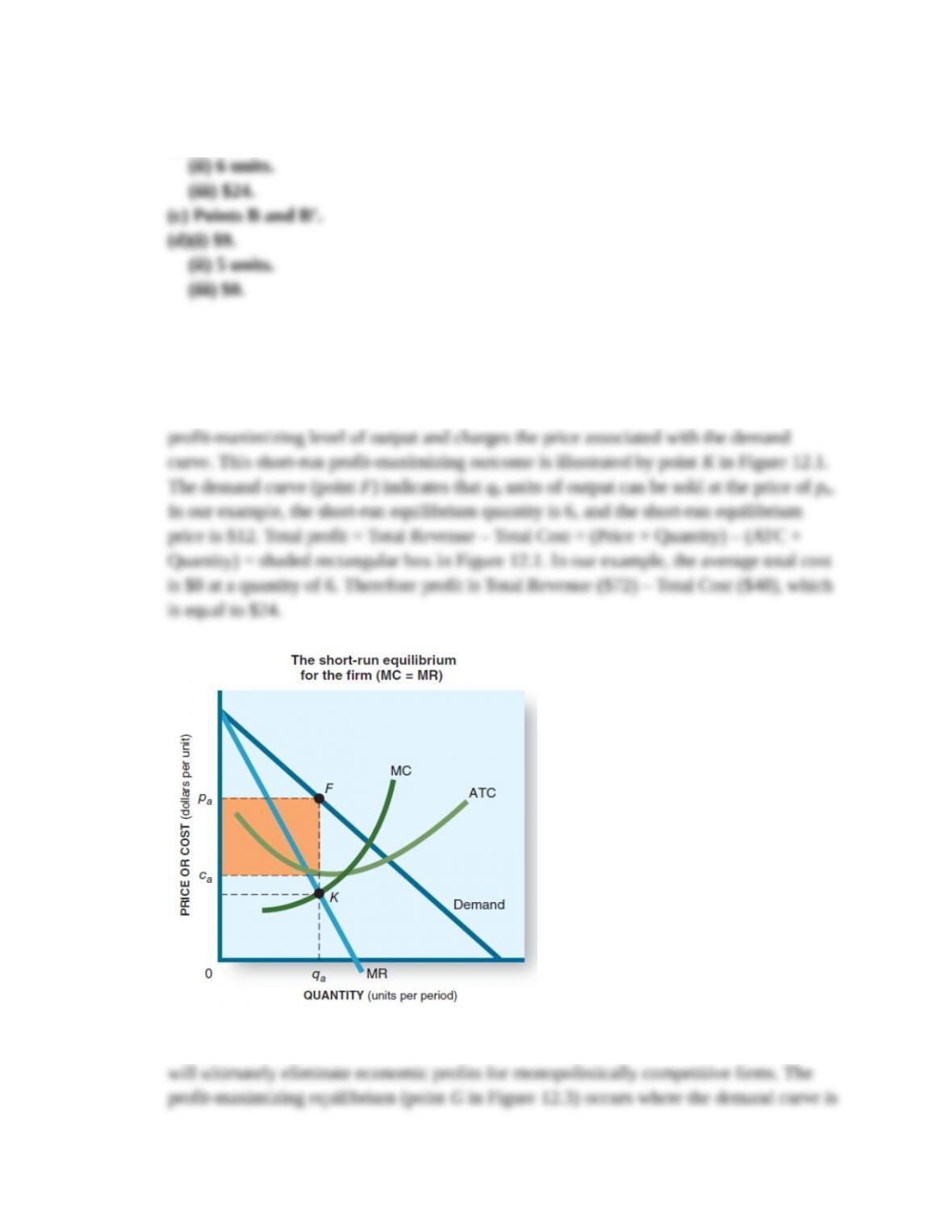

(a) Points A and A’.

(b)(i) $12.

Feedback:

(a), (b) In the short run, a monopolistically competitive firm produces where marginal

revenue equals marginal cost in order to maximize profits. It produces this

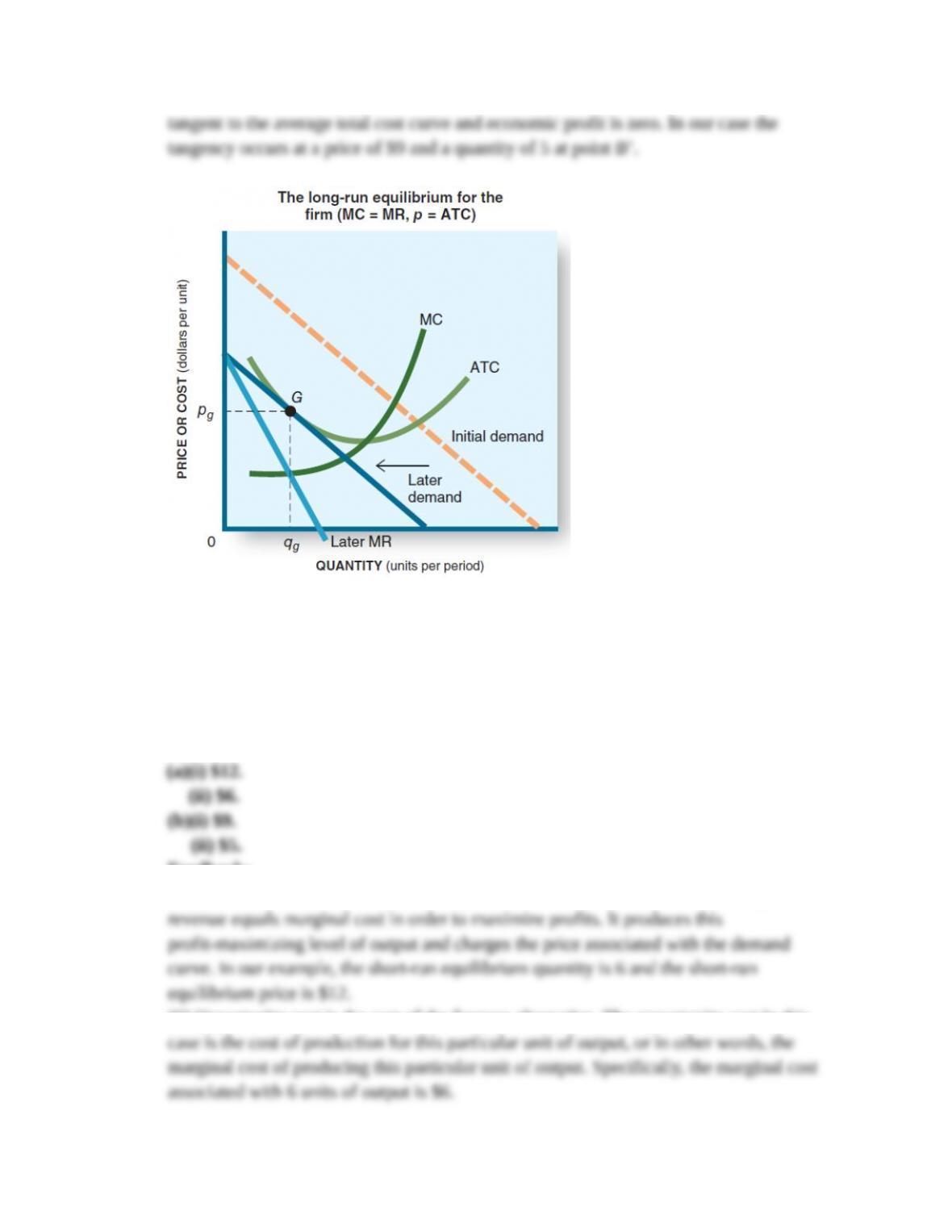

(c), (d) In the long run, entry-induced leftward shifts of the demand curve facing the firm

5

© 2016 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any

manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole or part.

..

5. (a) In the short-run equilibrium of the previous problem, what is

(i) The price of the product?

(ii) The opportunity cost of producing the last unit?

(b) In the long-run equilibrium of the previous problem, what is

(i) The price of the product?

(ii) The opportunity cost of producing the last unit? (LO 12-04)

Answers:

Feedback:

(a)(i) In the short run, a monopolistically competitive firm produces where marginal

(ii) Opportunity cost is the cost of the forgone alternative. The opportunity cost in this

6

© 2016 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any

manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole or part.

(b)(i) In the long run, entry-induced leftward shifts of the demand curve facing the firm

(ii) Once again, opportunity cost is the cost of the forgone alternative, or the marginal

6. According to the News on page 266,

(a) By how much could unit sales of coffee beans at Starbucks decline after the 2006

price increase without reducing total revenue?

(b) If the price elasticity of demand for Starbucks was 0.20, by how much would coffee

bean unit sales have fallen? (LO 12-01)

Answers:

Feedback:

(a) According to the article, Starbucks is “jacking up” the price of its coffee beans by

(b) If the price elasticity of demand for Starbucks is 0.20 then:

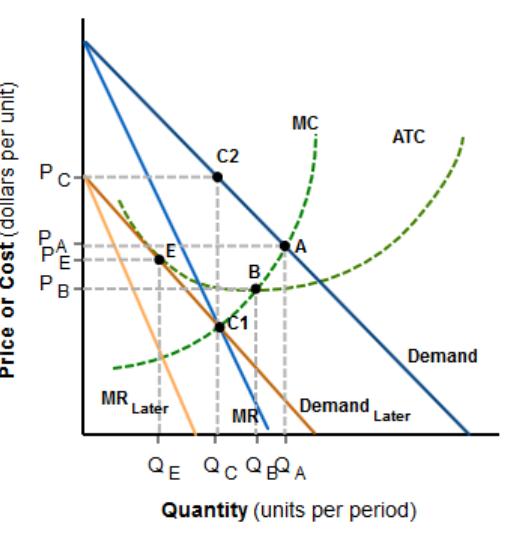

7. On the accompanying graph, identify each of the following market outcomes:

(a) Short-run equilibrium output in competition.

(b) Long-run equilibrium output in competition.

(c) Long-run equilibrium output in monopoly.

(d) Long-run equilibrium output in monopolistic competition. (LO 12-04)

Answers:,,,

7

© 2016 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any

manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole or part.

,,

(a) QA (associated with point A).

(b) QB (associated with point B).

(c) QC (associated with points C1 and C2).

(d) QE (associated with point E).

Feedback:

(a) Competitive firms strive for the rate of output at which marginal cost (MC) equals

price—here at point A, where market price is determined by the intersection of the

industry supply (MC curve) and demand curve. When a competitive market reaches this

rate of output, short-run equilibrium is achieved. Recall that Demand = Marginal

Revenue = Price for competitive firms.

(b) If the short-run equilibrium is profitable (p > ATC), other firms will want to enter the

industry. As they do, market price will fall until it reaches the minimum level of the

average total cost curve at point B. In this long-run equilibrium for the perfectly

competitive market, economic profits are zero and no additional firms want to enter or

exit the industry.

(c) The profit-maximizing rate of output for a monopoly occurs where the marginal cost

and marginal revenue curves intersect (point C1). The demand curve associated with this

level of output indicates the price (point C2) that consumers will pay. Barriers to entry

prevent other firms from entering this monopolistic market; therefore a monopolist’s

demand curve will never shift left.

(d) For monopolistic competition, in the long run more firms enter the industry. As they

do so, the demand curve facing each firm shifts to the left as all market shares decline.

Firms still equate MR and MC. Ultimately, long-run equilibrium will be found where the

8

© 2016 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any

manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole or part.

demand curve becomes tangent to the ATC curve (point E), at which point price equals

average total cost and no economic profits exist.

9

© 2016 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any

manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole or part.