14. The marketing study and the research and development are both sunk costs and should be ignored. We

will calculate the sales and variable costs first. Since we will lose sales of the expensive clubs and gain

sales of the cheap clubs, these must be accounted for as erosion. The total sales for the new project

will be:

Sales

New clubs

$725 45,000 = $32,625,000

Exp. clubs

$1,200 (–11,000) = –13,200,000

Cheap clubs

$390 10,000 = 3,900,000

$23,325,000

For the variable costs, we must include the units gained or lost from the existing clubs. Note that the

variable costs of the expensive clubs are an inflow. If we are not producing the sets any more, we will

save these variable costs, which is an inflow. So:

Var. costs

New clubs

–$315 45,000 = –$14,175,000

Exp. clubs

–$640 (–11,000) = 7,040,000

Cheap clubs

–$175 10,000 = –1,750,000

–$8,885,000

The pro forma income statement will be:

Sales

$23,325,000

Variable costs

8,885,000

Costs

5,900,000

Depreciation

1,850,000

EBT

6,690,000

Taxes

2,676,000

Net income

$ 4,014,000

Using the bottom up OCF calculation, we get:

IRR = 35.27%

15. The best-case and worst-case for the variables are:

Base Case Best Case Worst Case

Unit sales (new) 45,000 49,500 40,500

Price (new) $725 $798 $653

VC (new) $315 $284 $347

We will calculate the sales and variable costs first. Since we will lose sales of the expensive clubs and

gain sales of the cheap clubs, these must be accounted for as erosion. The total sales for the new project

will be:

Sales

New clubs

$798 49,500 = $39,476,250

Exp. clubs

$1,200 (–9,900) = – 11,880,000

Cheap clubs

$390 11,000 = 4,290,000

$31,886,250

For the variable costs, we must include the units gained or lost from the existing clubs. Note that the

variable costs of the expensive clubs are an inflow. If we are not producing the sets any more, we will

save these variable costs, which is an inflow. So:

Var. costs

New clubs

–$284 49,500 = –$14,033,250

Exp. clubs

–$640 (–9,900) = 6,336,000

Cheap clubs

–$175 11,000 = – 1,925,000

–$9,622,250

The pro forma income statement will be:

Sales

$31,886,250

Variable costs

9,622,250

Costs

5,310,000

Depreciation

1,850,000

EBT

$15,104,000

Taxes

6,041,600

Net income

$9,062,400

Using the bottom up OCF calculation, we get:

NPV = –$12,950,000 – 1,900,000 + $10,912,400(PVIFA14%,7) + 1,900,000/1.147

NPV = $32,705,008.64

Worst-case

We will calculate the sales and variable costs first. Since we will lose sales of the expensive clubs and

gain sales of the cheap clubs, these must be accounted for as erosion. The total sales for the new project

will be:

Sales

New clubs

$653 40,500 = $26,426,250

Exp. clubs

$1,200 (– 12,100) = – 14,520,000

Cheap clubs

$390 9,000 = 3,510,000

$15,416,250

For the variable costs, we must include the units gained or lost from the existing clubs. Note that the

variable costs of the expensive clubs are an inflow. If we are not producing the sets any more, we will

save these variable costs, which is an inflow. So:

Var. costs

New clubs

–$347 40,500 = –$14,033,250

Exp. clubs

–$640 (–12,100) = 7,744,000

Cheap clubs

–$175 9,000 = –1,575,000

–$7,864,250

Sales

Variable costs

Costs

Depreciation

EBT

Taxes

*assumes a tax credit

Net income

We will calculate the sales and variable costs first. Since we will lose sales of the expensive clubs and

gain sales of the cheap clubs, these must be accounted for as erosion. The total sales for the new project

To calculate the sensitivity of the NPV to changes in the quantity sold of the new club, we need to

will be the same no matter what quantity we choose.

We will calculate the sales and variable costs first. Since we will lose sales of the expensive clubs and

gain sales of the cheap clubs, these must be accounted for as erosion. The total sales for the new project

will be:

NPV/Q = $1,054.92

17. a. The base-case NPV is:

NPV = –$3,650,000 + $693,000(PVIFA11%,10)

NPV = $431,237.78

$1,550,000 = ($63)Q(PVIFA11%,9)

Q = $1,550,000/[$63(5.5370)]

Q = 4,443.37

Abandon the project if Q < 4,443, because the NPV of abandoning the project is greater than the

NPV of the future cash flows.

18. a. If the project is a success, the present value of the future cash flows will be:

one year, the expected value of the project in one year is the average of the success and failure

cash flows, plus the cash flow in one year, so:

Expected value of project at year 1 = [($5,930,177.91 + $1,550,000)/2] + $693,000

The NPV is the present value of the expected value in one year plus the cost of the equipment,

so:

NPV = –$3,650,000 + ($4,433,088.95)/1.11

value of the option to abandon today is:

Option value = (.50)($363,964.42)/1.11

19. If the project is a success, the present value of the future cash flows will be:

PV future CFs = $63(22,000)(PVIFA11%,9)

PV future CFs = $7,674,347.88

If the sales are only 3,400 units, from Problem 17, we know we will abandon the project, with a value

value of the project in one year is the average of the success and failure cash flows, plus the cash flow

in one year, so:

Expected value of project at year 1 = [($7,674,347.88 + $1,550,000)/2] + $693,000

find the value of the option to expand today, so:

Option value = (.50)($5,930,177.91)/1.11

Option value = $2,671,251.31

20. a. The accounting breakeven is the aftertax sum of the fixed costs and depreciation charge divided

QA = [(FC + Depreciation)(1 – tC)]/[(P – VC)(1 – tC)]

QA = [($0 + 8,300) (1 – .30)]/[($13 – 4.45)(1 – .30)]

QA = 970.76

b. When calculating the financial breakeven point, we express the initial investment as an equivalent

annual cost (EAC). The initial investment is the $20,000 in licensing fees. Dividing the initial

PVA = C({1 – [1/(1 + R)t]}/R)

$20,000 = C{[1 – (1/1.12)3 ]/.12}

C = $8,326.98

QF = [EAC + FC(1 – tC) – Depreciation(tC)]/[(P – VC)(1 – tC)]

QF = ($8,326.98 + 0 – 0)/[($13 – 4.45)(.70)]

QF = 1,391.31

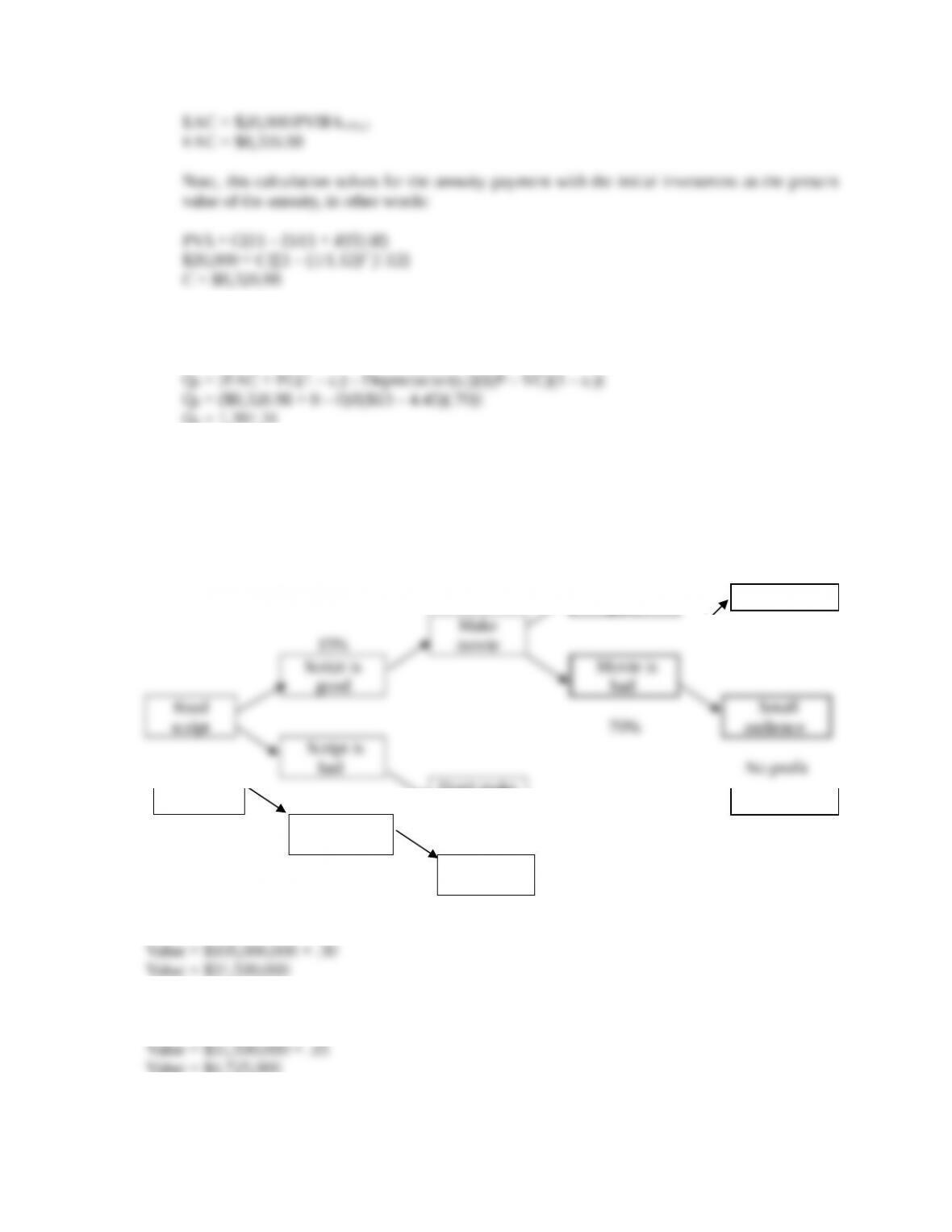

21. The payoff from taking the lump sum is $50,000, so we need to compare this to the expected payoff

from taking one percent of the profit. The decision tree for the movie project is:

Big audience

30%

$105,000,000

Movie is

good

15%

Make

movie

Script is

good

Movie is

bad

Read

script

70%

Small

audience

Script is

bad

No profit

85%

Don’t make

movie

No profit

good, and the audience is big, so the expected value of this outcome is:

Value = $105,000,000 × .30

The expected value that the movie is good, and has a big audience, assuming the script is good is:

Value = $31,500,000 × .15

Value = $4,725,000

The screenwriter should take the cash offered today.