18. The present value of the company is the present value of the future cash flows generated by the

company. Here we have real cash flows, a real interest rate, and a real growth rate. The cash flows are

a growing perpetuity, with a negative growth rate. Using the growing perpetuity equation, the present

value of the cash flows is:

PV = $5,492,753.62

19. To find the EAC, we first need to calculate the NPV of the incremental cash flows. We will begin with

the aftertax salvage value, which is:

Taxes on salvage value = (BV – MV)tC

So, the NPV of the cost of the decision to buy is:

20. We will find the EAC of the EVF first. There are no taxes since the university is tax-exempt, so the

maintenance costs are the operating cash flows. The NPV of the decision to buy one EVF is:

Since the university must buy five of the mowers, the total EAC of the decision to buy the EVF mower

is:

Total EAC = 5(–$4,710.42)

So, the EAC per mower is:

EAC = –$19,141.46/(PVIFA9%,7)

21. We will calculate the aftertax salvage value first. The aftertax salvage value of the equipment will be:

Taxes on salvage value = (BV – MV)tC

Taxes on salvage value = ($0 – 35,000)(.34)

Taxes on salvage value = –$11,900

Market price

$35,000

Tax on sale

–11,900

Aftertax salvage value

$23,100

Equipment

–$655,000

NWC

55,000

Total

–$600,000

So, the NPV of purchasing the new machine, including the recovery of the net working capital,

is:

And the IRR is:

0 = –$9,820,000 + $2,226,000(PVIFAIRR,4) + $160,000/(1 + IRR)4

Using a spreadsheet or financial calculator, we find the IRR is:

IRR = –3.10%

Now we can calculate the decision to keep the old machine:

Keep old machine:

The initial cash outlay for the new machine is the market value of the old machine, including any

potential tax. The decision to keep the old machine has an opportunity cost, namely, the company

could sell the old machine. Also, if the company sells the old machine at its current value, it will

of keeping the old machine will be:

Keep machine

–$4,370,000

Taxes

740,000

Total

–$3,630,000

Next, we can calculate the operating cash flow created if the company keeps the old machine.

There are no incremental cash flows from keeping the old machine, but we need to account for

the cash flow effects of depreciation. The income statement, adding depreciation to net income

to calculate the operating cash flow will be:

Depreciation

$630,000

EBT

–$630,000

Taxes

– 252,000

Net income

–$378,000

OCF

$252,000

So, the NPV of the decision to keep the old machine will be:

NPV = –$3,630,000 + $252,000(PVIFA10%,4)

NPV = –$2,831,193.91

And the IRR is:

0 = –$3,630,000 + $252,000(PVIFAIRR,4)

Using a spreadsheet or financial calculator, we find the IRR is:

IRR = –36.93%

The company should buy the new machine since it has a greater NPV.

There is another way to analyze a replacement decision that is often used. It is an incremental

cash flow analysis of the change in cash flows from the existing machine to the new machine,

assuming the new machine is purchased. In this type of analysis, the initial cash outlay would be

would be:

Purchase new machine

–$9,660,000

Net working capital

–160,000

Sell old machine

4,370,000

Taxes on old machine

–740,000

Total

–$6,190,000

The cash flows from purchasing the new machine would be the saved operating expenses. We

would also need to include only the change in depreciation. The old machine has a depreciation

of $630,000 per year, and the new machine has a depreciation of $2,415,000 per year, so the

increased depreciation will be $1,785,000 per year. The pro forma income statement and

operating cash flow under this approach will be:

Operating expense

$2,100,000

Depreciation

–1,785,000

EBT

$315,000

Taxes

126,000

Net income

$189,000

OCF

$1,974,000

The NPV under this method is:

NPV = –$6,190,000 + $1,974,000(PVIFA10%,4) + $160,000/1.104

And the IRR is:

0 = –$6,190,000 + $1,974,000(PVIFAIRR,4) + $160,000/(1 + IRR)4

So, this analysis still tells us the company should purchase the new machine. This is really the

same type of analysis we originally did. Consider this: Subtract the NPV of the decision to keep

the old machine from the NPV of the decision to purchase the new machine. You will get:

b. Even though the saved expenses are less than the cost of the machine, the cash flows are also

increased because of the higher depreciation of the new machine. The depreciation tax shield

23. We can find the NPV of a project using nominal cash flows or real cash flows. Either method will

result in the same NPV. For this problem, we will calculate the NPV using nominal cash flows. The

initial investment in either case is $1,910,000 since it will be spent today. We will begin with the

nominal cash flows. The revenues and production costs increase at different rates, so we must be

careful to increase each at the appropriate growth rate. The nominal cash flows for each year will be:

Year 0

Year 1

Year 2

Year 3

Revenues

$965,000.00

$1,013,250.00

$1,063,912.50

Costs

$425,000.00

442,000.00

459,680.00

Depreciation

272,857.14

272,857.14

272,857.14

EBT

$267,142.86

$298,392.86

$331,375.36

Taxes

90,828.57

101,453.57

112,667.62

Net income

$176,314.29

$196,939.29

$218,707.74

OCF

$449,171.43

$469,796.43

$491,564.88

Year 4

Year 5

Year 6

Year 7

Revenues

$1,117,108.13

$1,172,963.53

$1,231,611.71

$1,293,192.29

Costs

478,067.20

497,189.89

517,077.48

537,760.58

Depreciation

272,857.14

272,857.14

272,857.14

272,857.14

EBT

$366,183.78

$402,916.50

$441,677.08

$482,574.57

Taxes

124,502.49

136,991.61

150,170.21

164,075.35

Net income

$241,681.30

$265,924.89

$291,506.87

$318,499.21

OCF

$514,538.44

$538,782.03

$564,364.02

$591,356.36

Now that we have the nominal cash flows, we can find the NPV. We must use the nominal required

return with nominal cash flows. Using the Fisher equation to find the nominal required return, we get:

(1 + R) = (1 + r)(1 + h)

So, the NPV of the project using nominal cash flows is:

NPV = –$1,910,000 + $449,171.43/1.1235 + $469,796.43/1.12352 + $491,564.88/1.12353

Because the revenues and costs are growing annuities, we can find the present value of these

cash flows using the growing annuity equation. This will allow us to find the operating cash flow

using the tax shield approach. Since revenues and expenses are growing at different rates, we must

required return. We also need to account for the effect of taxes, so we will multiply by one minus the

tax rate. So, the present value of the aftertax revenues using the growing annuity equation is:

PV of aftertax revenues = C{[1/(r – g)] – [1/(r – g)] × [(1 + g)/(1 + r)]t}(1 – tC)

PV of aftertax revenues = $965,000{[1/(.07 – .05)] – [1/(.07 – .05)] × [(1 + .05)/(1 + .07)]7}(1 – .34)

PV of aftertax costs = C {[1/(r – g)] – [1/(r – g)] × [(1 + g)/(1 + r)]t}(1 – tC)

PV of aftertax costs = $425,000{[1/(.07 – .04)] – [1/(.07 – .04)] × [(1 + .04)/(1 + .07)]7}(1 – .34)

first year is a nominal value, so we can find the present value of the depreciation tax shield as an

ordinary annuity using the nominal required return. So, the present value of the depreciation tax shield

will be:

quantity sold each year by increasing the current year’s quantity by the growth rate. So, the quantity

sold each year will be:

Year 1 quantity = 9,500

Year 2 quantity = 9,500(1 + .07) = 10,165

Year 3 quantity = 10,165(1 + .07) = 10,877

and operating cash flow each year will be:

Year 0

Year 1

Year 2

Year 3

Year 4

Year 5

Revenues

$636,500.00

$681,055.00

$728,728.85

$779,739.87

$834,321.66

Fixed costs

265,000.00

265,000.00

265,000.00

265,000.00

265,000.00

Variable costs

313,500.00

335,445.00

358,926.15

384,050.98

410,934.55

Depreciation

85,000.00

85,000.00

85,000.00

85,000.00

85,000.00

EBT

–$27,000.00

–$4,390.00

$19,802.70

$45,688.89

$73,387.11

Taxes

–9,180.00

–1,492.60

6,732.92

15,534.22

24,951.62

Net income

–$17,820.00

–$2,897.40

$13,069.78

$30,154.67

$48,435.49

OCF

$67,180.00

$82,102.60

$98,069.78

$115,154.67

$133,435.49

Equipment

–$425,000

NWC

–60,000

$60,000

Total CF

–$485,000

$67,180.00

$82,102.60

$98,069.78

$115,154.67

$193,435.49

So, the NPV of the project is:

NPV = –$485,000 + $67,180/1.15 + $82,102.60/1.152 + $98,069.78/1.153

+ $115,154.67/1.154 + $193,435.49/1.155

NPV = –$138,007.09

and ordinary annuities. The sales and variable costs increase at the same rate as sales, so both are

growing annuities. The fixed costs and depreciation are both ordinary annuities. Using the growing

annuity equation, the present value of the revenues is:

PV of revenues = C{[1/(r – g)] – [1/(r – g)] × [(1 + g)/(1 + r)]t}(1 – tC)

PV of revenues = $636,500{[1/(.15 – .07)] – [1/(.15 – .07)] × [(1 + .07)/(1 + .15)]5}

PV of revenues = $2,408,228.85

PV of variable costs = C{[1/(r – g)] – [1/(r – g)] × [(1 + g)/(1 + r)]t}(1 – tC)

PV of variable costs = $313,500{[1/(.15 – .07)] – [1/(.15 – .07)] × [(1 + .07)/(1 + .15)]5}

PV of variable costs = $1,186,142.57

PV of fixed costs = C({1 – [1/(1 + r)]t }/r )

PV of fixed costs = $265,000({1 – [1/(1 + .15)]5 }/.15)

PV of fixed costs = $888,321.10

PV of depreciation = $284,933.18

NPV = –$485,000 + ($2,408,228.85 – 1,186,142.57 – 888,321.10)(1 – .34) + ($284,933.18)(.34)

+ $60,000/1.155

NPV = –$138,007.09

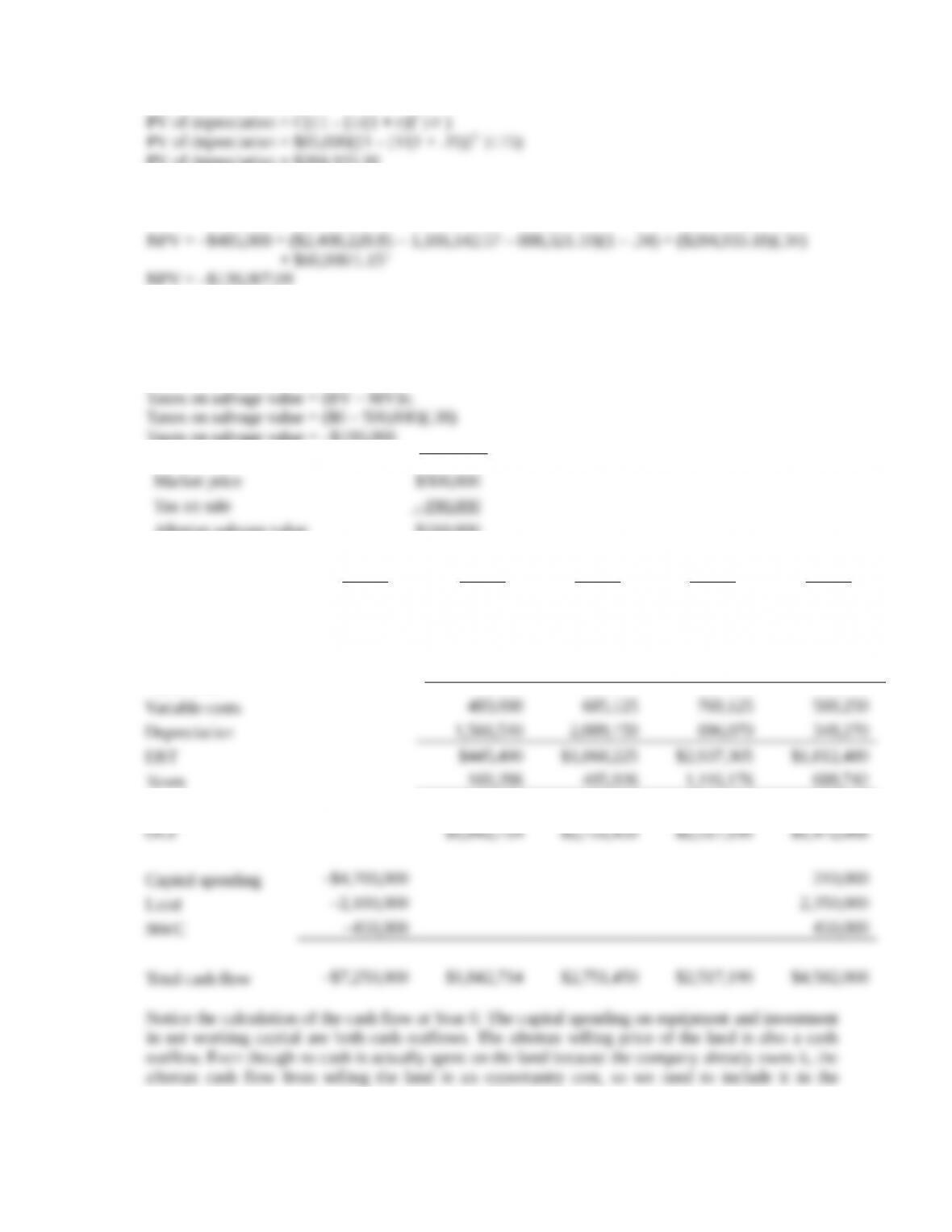

life. The aftertax salvage value is the market value of the equipment minus any taxes paid (or

refunded), so the aftertax salvage value in four years will be:

Taxes on salvage value = (BV – MV)tC

Taxes on salvage value = ($0 – 500,000)(.38)

Taxes on salvage value = –$190,000

Market price

$500,000

Tax on sale

–190,000

Aftertax salvage value

$310,000

Now we need to calculate the operating cash flow each year. Using the bottom up approach to

calculating operating cash flow, we find:

Year 0

Year 1

Year 2

Year 3

Year 4

Revenues

$3,220,000

$4,567,500

$5,127,500

$3,395,000

Fixed costs

725,000

725,000

725,000

725,000

Variable costs

483,000

685,125

769,125

509,250

Depreciation

1,566,510

2,089,150

696,070

348,270

EBT

$445,490

$1,068,225

$2,937,305

$1,812,480

Taxes

169,286

405,926

1,116,176

688,742

Net income

$276,204

$662,300

$1,821,129

$1,123,738

OCF

$1,842,714

$2,751,450

$2,517,199

$1,472,008

Capital spending

–$4,700,000

310,000

Land

–2,100,000

2,350,000

NWC

–450,000

450,000

Total cash flow

–$7,250,000

$1,842,714

$2,751,450

$2,517,199

$4,582,008

NPV = –$7,250,000 + $1,842,714/1.13 + $2,751,450/1.132 + $2,517,199/1.133

+ $4,582,008/1.134

NPV = $1,090,285.04