CHAPTER 18 B – 1

14. The interest rate for the term of the discount is:

Interest rate = .01/.99

Interest rate = .0101, or 1.01%

And the interest is for:

25 – 10 = 15 days

So, using the EAR equation, the effective annual interest rate is:

a. The periodic interest rate is:

Interest rate = .03/.97

Interest rate = .0309, or 3.09%

And the EAR is:

b. The EAR is:

c. The EAR is:

15. The total sales of the firm are equal to the total credit sales since all sales are on credit, so:

Total credit sales = 3,500($395)

Total credit sales = $1,382,500

The average collection period is the percentage of accounts taking the discount times the discount

period, plus the percentage of accounts not taking the discount times the days’ until full payment is

required, so:

CHAPTER 18 B – 2

And the average receivables are the credit sales divided by the receivables turnover so:

16. The receivables turnover is:

Receivables turnover = 365/Average collection period

Receivables turnover = 365/36

Receivables turnover = 10.1389 times

And the annual credit sales are:

Intermediate

17. a. If you borrow $55,000,000 for one month, you will pay interest of:

Interest = $55,000,000(.0068)

Interest = $374,000

However, with the compensating balance, you will only get the use of:

b. To end up with $20,000,000, you must borrow:

Amount to borrow = $20,000,000/(1 – .04)

Amount to borrow = $20,833,333.33

The total interest you will pay on the loan is:

18. a. The EAR of your investment account is:

b. To calculate the EAR of the loan, we can divide the interest on the loan by the amount of the

loan. The interest on the loan includes the opportunity cost of the compensating balance. The

opportunity cost is the amount of the compensating balance times the potential interest rate you

could have earned. The compensating balance is only on the unused portion of the credit line, so:

Opportunity cost = .05($60,000,000 – 45,000,000)(1.0074)4

And the interest you will pay to the bank on the loan is:

c. The compensating balance is only applied to the unused portion of the credit line, so the EAR of

a loan on the full credit line is:

EAR = 1.01634 – 1

19. a. A 45-day collection period means sales collections each quarter are:

Collections = 1/2 current sales + 1/2 old sales

A 36-day payables period means payables each quarter are:

Payables = 3/5 current orders + 2/5 old orders

So, the cash inflows each quarter are:

Q1 = $63 + 1/2($160) – 2/5(.45)($160) – 3/5(.45)($145) – .30($160) – $15

CHAPTER 18 B – 4

The company’s cash budget will be:

WILDCAT, INC.

Cash Budget

(in millions)

Q1

Q2

Q3

Q4

Beginning cash balance

$36.00

$48.05

$19.65

$21.55

Net cash inflow

12.05

–28.40

1.90

37.15

Ending cash balance

$48.05

$19.65

$21.55

$58.70

Minimum cash balance

–20.00

–20.00

–20.00

–20.00

Cumulative surplus (deficit)

$28.05

–$0.35

$1.55

$38.70

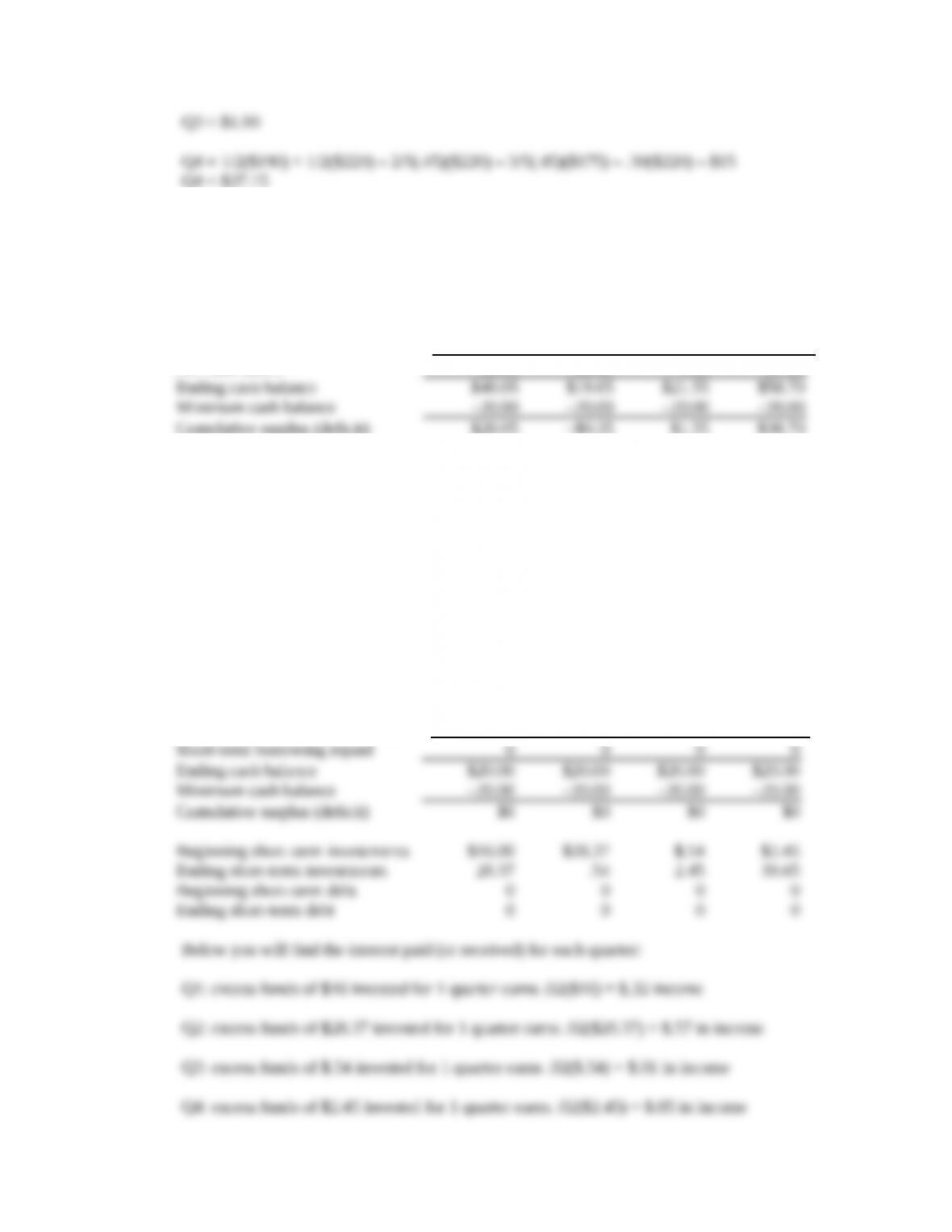

With a $20,000,000 minimum cash balance, the short-term financial plan will be:

WILDCAT, INC.

Short-Term Financial Plan

(in millions)

b.

Q1

Q2

Q3

Q4

Minimum cash balance

$20.00

$20.00

$20.00

$20.00

Net cash inflow

12.05

–28.40

1.90

37.15

New short-term investments

–12.37

0

–1.91

–37.20

Income on short-term investments

.32

.57

.01

.05

Short-term investments sold

0

27.83

0

0

New short-term borrowing

0

0

0

0

Interest on short-term borrowing

0

0

0

0

Short-term borrowing repaid

0

0

0

0

Ending cash balance

$20.00

$20.00

$20.00

$20.00

Minimum cash balance

–20.00

–20.00

–20.00

–20.00

Cumulative surplus (deficit)

$0

$0

$0

$0

Beginning short-term investments

$16.00

$28.37

$.54

$2.45

Ending short-term investments

28.37

.54

2.45

39.65

Beginning short-term debt

0

0

0

0

Ending short-term debt

0

0

0

0

CHAPTER 18 B – 5

WILDCAT, INC.

Short-Term Financial Plan

(in millions)

Q1

Q2

Q3

Q4

Minimum cash balance

$30.00

$30.00

$30.00

$30.00

Net cash inflow

12.05

–28.40

1.90

37.15

New short-term investments

–12.17

0

0

–28.64

Income on short-term investments

.12

.36

0

0

Short-term investments sold

0

18.17

0

0

New short-term borrowing

0

9.87

0

0

Interest on short-term borrowing

0

0

–.30

–.25

Short-term borrowing repaid

0

0

–1.60

–8.26

Ending cash balance

$30.00

$30.00

$30.00

$30.00

Minimum cash balance

–30.00

–30.00

–30.00

–30.00

Cumulative surplus (deficit)

$0

$0

$0

$0

Beginning short-term investments

$6.00

$18.17

$0

$0

Ending short-term investments

18.17

0

0

28.64

Beginning short-term debt

0

0

9.87

8.26

Ending short-term debt

0

9.87

8.26

0

Below you will find the interest paid (or received) for each quarter:

Q1: excess funds of $6 invested for 1 quarter earns .02($6) = $.12 income

b. And with a minimum cash balance of $10,000,000, the short-term financial plan will be:

WILDCAT, INC.

Short-Term Financial Plan

(in millions)

Q1

Q2

Q3

Q4

Minimum cash balance

$10.00

$10.00

$10.00

$10.00

Net cash inflow

12.05

–28.40

1.90

37.15

New short-term investments

–12.57

0

–2.12

–37.41

Income on short-term investments

.52

.77

.22

.26

Short-term investments sold

0

27.63

0

0

New short-term borrowing

0

0

0

0

Interest on short-term borrowing

0

0

0

0

Short-term borrowing repaid

0

0

0

0

CHAPTER 18 B – 6

Ending cash balance

$10.00

$10.00

$10.00

$10.00

Minimum cash balance

–10.00

–10.00

–10.00

–10.00

Cumulative surplus (deficit)

$0

$0

$0

$0

Beginning short-term investments

$26.00

$38.57

$10.94

$13.06

Ending short-term investments

38.57

10.94

13.06

50.47

Beginning short-term debt

0

0

0

0

Ending short-term debt

0

0

0

0

Below you will find the interest paid (or received) for each quarter:

Since cash has an opportunity cost, the firm can boost its profit if it keeps its minimum cash

balance low and invests the cash instead. However, the tradeoff is that in the event of unforeseen

circumstances, the firm may not be able to meet its short–run obligations if enough cash is not

available.

Challenge

21. a. For every dollar borrowed, you pay interest of:

Interest = $1(.0185) = $.0185

You also must maintain a compensating balance of 5 percent of the funds borrowed, so for each

dollar borrowed, you will only receive:

At the end of the year the compensating will be returned, so your net cash flow at the end of the

year will be:

CHAPTER 18 B – 7

End of year cash flow = $1.07608 – .05

End of year cash flow = $1.02608

The present value of the end of year cash flow is the amount you receive at the beginning of the

year, so the EAR is:

FV = PV(1 + R)

$1.02608 = $.95(1 + R)

effective annual interest rate, so:

Interest = $150,000,000[(1.0185)4 – 1]

Interest = $11,411,841.55

credit line also has a fee of .165 percent, so you will only get to use:

Amount received = .95($150,000,000) – .00165($400,000,000)

Amount received = $141,840,000

EAR = .08046, or 8.046%

Interest = $20,000,000(.087) = $1,740,000

Additionally, the compensating balance on the loan is:

Compensating balance = $20,000,000(.04) = $800,000

Since this is a discount loan, you will receive the loan amount minus the interest payment. You will

also not get to use the compensating balance. So, the amount of money you will actually receive on a

$20 million loan is:

Cash received = $20,000,000 – 1,740,000 – 800,000 = $17,460,000

The EAR is the interest amount divided by the loan amount, so:

CHAPTER 18 B – 8

year is $17,460,000. At the end of the year, your cash flow is the loan repayment, but you will also

receive your compensating balance back, so:

End of year cash flow = $20,000,000 – 800,000

$19,200,000 = $17,460,000(1 + R)

R = $19,200,000/$17,460,000 – 1