Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

NOTE – ADDITIONAL BACKGROUND READING AND VIDEO:

Historically, the global beer industry has looked to acquisitions or product innovations to

fuel growth in the past. In this report from 2008 it appears that the opportunities for

continued acquisitions were becoming limited. This meant major players would have to

look at regional/local brewers if they wanted to grow through acquisition – or they would

have to do internal development:

http://www.businessweek.com/globalbiz/content/jul2008/gb20080714_615944.htm

In June 2013, Anheuser-Busch InBev audaciously completed its acquisition of Grupo

Modelo. This means the brands Corona, Modelo Especial, and Pacifico, which occupy

top places in market share of U.S. imported beer sales, will now add clout to the A-B

InBev stable of products. A-B InBev now has Corona to add to Budweiser, Stella Artois,

and Beck’s, positioning the company as a global powerhouse in beer products. See

http://online.wsj.com/article/SB10001424052702303649504577495921266834262.html

for the history of this merger, which gives A-B InBev considerable ability to see

synergies in its overall operations. The merger had been delayed by the U.S. antitrust

watchdogs, who prevented A-B InBev from taking control of the U.S. distributor Crown

Imports. This means the Grupo Modelo/InBev products will still be sold in the U.S. under

the Constellation Brands/Crown Imports. But control over brewing the beer itself now

resides with A-B InBev. See http://www.stltoday.com/business/local/a-b-inbev-

completes-grupo-modelo-deal/article_c6c7cfd1-883b-5d1d-bdea-dc7a0111bac2.html for

more details.

From early 2013, here is a story about this consolidation in the beer industry. See this

video discussing Anheuser-Busch InBev’s acquisition of Mexican’s Modelo:

http://www.bloomberg.com/news/videos/b/b96f37ba-d801-44fa-b549-ada5fc44eaa5

According to this report, it takes only 5 minutes of work in the U.S. to be able to afford a

beer, which is why this is a competitive market. Corona is the top brand in 36 countries,

so no wonder A-B InBev was so anxious to acquire it.

Here’s a fun facts graphic on A-B InBev: http://www.businessweek.com/articles/2012-10-

25/99-facts-about-beer-on-the-wall-dot-dot-dot

The merger of Modelo and A-B InBev left Molson Coors SABMiller at a disadvantage.

To compete, in 2013 Molson Coors said it planned to restructure the business, including

the international segment, reduce overhead expenses, and execute global procurement

and global standardization. But then in September 2015 InBev announced it had

approached SABMiller about a takeover, “a potential move that would combine the

world’s two biggest beer makers and mark the biggest shakeup in the industry in nearly a

decade amid a growing craft beer expansion.” See the full story here

http://www.usatoday.com/story/money/business/2015/09/16/sabmiller-takeover-

approach/32488403/

This proposed merger would have implications for Molson Coors, due to its joint

venture with SABMiller. Speculation was that “Molson Coors likely would stand to

profit greatly from the deal, despite not actually truly being a part of it… If there were to

be a merger of SABMiller and Anheuser Busch in the near future, U.S. regulators would

likely force SABMiller to dispose of their stake in the joint venture, and with Molson

Coors having the right to first refusal, Molson Coors could buy the business at a

reasonable price. This would be a major positive for Molson Coors for two main

reasons. First, the purchasing of SABMiller's stake by Molson Coors would allow it to

take strategic control over its operations in its biggest market. The second reason would

be that with the purchase, Molson Coors would have the chance for significant potential

synergies, which would allow for the company to quickly cut costs. As the U.S. beer

market grows slowly, a cutting of costs is key for Molson Coors to grow its profits in the

coming years.” Read more: http://www.nasdaq.com/article/why-an-anheuser-busch-

sabmiller-merger-could-be-huge-for-molson-coors-cm520764

Molson Coors had been receiving criticism from small beermakers regarding its Blue

Moon brand, for not “spelling out their corporate parentage in ads or on their

packaging.” The fear was that the public would think this beer was truly a “craft beer”,

when, from the perspective of the real craft beer makers, this was “a phony artisanal

brew created by a mega-company to exploit a rapidly expanding market.” For their part,

Molson Coors was “taking credit for helping popularize the craft beer movement. ‘We

should be proud to make beers that grow and are popular—that’s the American way,’

says MillerCoors Chief Executive Officer Tom Long. ‘Being small and unpopular,

what’s the utility in that?’… The fight over Blue Moon’s legitimacy peaked in 2013

when the Brewers Association, craft beer’s primary U.S. trade group, published a list of

companies, including MillerCoors, that didn’t fit its definition of a ‘craft brewer.’ The

association knocked some brands for excluding parent companies from their labels.

Craft brewers are ‘small, independent, and traditional,’ according to the group’s

definition. That means they produce fewer than 6 million barrels a year—it used to be

2 million until Samuel Adams maker Boston Beer got too big to qualify. They also must

be less than 25 percent-owned by a megabrewer and meet certain ingredient thresholds.”

Some wonder if those designations make the craft breweries “snobs” – why not let

everyone benefit from flavorful beer, no matter who makes it? See

http://www.businessweek.com/articles/2013-08-08/blue-moon-vs-dot-craft-beer-rivals-

millercoors-strikes-back?campaign_id=yhoo for the whole story. ALSO see additional

articles and video in the sidebar that accompanies this article.

Here’s a video story about this battle for the craft beer designation. THIS IS GOOD TO

WATCH TO ILLUSTRATE THE STATEGIC GROUPS INVOLVED:

http://www.bloomberg.com/news/videos/b/475f9df2-1683-4f5a-b29b-5a963a2e3361

In addition, here’s a report from the Beer Institute on the demographics of beer drinking

in the U.S., explaining why “the top five states for beer consumption per capita are North

Dakota, New Hampshire, Montana, South Dakota and Wisconsin,” which drank about

45.8 gallons of beer per resident 21 and older in 2012 (partly explained by the large

numbers of young males with blue-collar jobs in these states). In contrast, residents of

Utah, with its large Mormon population, drank about 20.2 gallons of beer. See the article,

plus two interesting embedded videos at http://finance.yahoo.com/blogs/big-data-

download/states-drink-most-beer-183941283.html

Regarding the global socioeconomic challenges of beer, here’s a story issued by Russia's

biggest beer brand, Baltika, a division of international brewer Carlsberg about the outlook

for beer and alcohol consumption in Russia. Macroeconomic issues reduced opportunity

in Russia in 2015, and the brand's long-term growth opportunities in the region are very

uncertain. http://www.themoscowtimes.com/article/520630.html

3. What internal assets does Boston Beer have that may help it deal with its

challenges?

Referencing Chapter 3: Analyzing the Internal Environment -

When one firm attempts to outperform others, it’s important to figure out how this could

be done. The answer may lie in how that firm arranges its activities and creates unique

Remember, value-chain analysis is a strategic analysis of an organization that uses value-

creating activities. Value is the amount that buyers are willing to pay for what a firm

provides them and is measured by total revenue, a reflection of the price a firm’s product

Every activity should add value. Take a look at Chapter 3, Exhibit 3.1 to see the value

chain activities. Based on the relationships between these elements, Boston Beer can

As it says in the case, beer distribution in the U.S. is regulated with a “tier” structure.

This means that brewers have limited options for vertical integration within the industry.

The supply chain in the industry can look like this:

raw material grower (hops, barley, etc.) ➔ supplier (aggregator of raw

materials) ➔ brewer (can be the actual company, or can be outsourced

to a contracted brewer) ➔ bottler (can be the actual company, or can

NOTE: see the end of this teaching note for an Appendix entry explaining exactly how

beer is made.

The only activities that a brewer can “own” are the brewing and/or bottling activities. All

Boston Beer’s value chain is captured visually in the diagram below:

Value chain activity How does Boston Beer create value for the

customer? What challenges does Boston Beer have in

its value chain?

Primary:

Inbound logistics (distribution

systems, warehouse layouts)

Hard to assess. Need information on inbound raw

Operations (efficient work flow

Invested in brewery production efficiencies to lower

Outbound logistics

processing)

Focused on on-time service, forecasting, production

Marketing and Sales (motivated

effective pricing, proper ID of

customer segments &

distribution channels)

300 member salesforce with high level of product

Service (ability to solicit

Rewarded loyal customers in the past by advertising

Secondary (or support):

Procurement (win-win

relationships with suppliers,

Relied on about 400 distribution partners for selling

products, multiple foreign suppliers for raw material

Technology development (state

personnel)

Creation of Alchemy & Science to research brewing

Human resource management

& retention mechanisms)

Anecdotal reports are that employees support the

General Administration

Jim Koch owns significant stock in the company, able to

access to capital, effective top

stakeholders)

good decisions so far. Has tried to help other small

Primary Activities

In terms of primary activities, the key to Boston Beer’s ability to differentiate itself in the

market appeared to reside in its operations, outbound logistics, and marketing. In all three

Support Activities

With regards to support activities, a competitive advantage can be achieved by

developing a strong general administration that is built around visionary leadership and a

culture that pushes for technological innovation. Jim Koch appeared to be able to inspire

In addition, see the concept of the resource-based view of the firm, and the three key

types of resources: tangible resources, intangible resources, and organizational

capabilities. A firm’s strengths and capabilities – no matter how unique or impressive –

do NOT necessarily lead to a competitive advantage. The resource-based view of the firm

An important issue to focus on here is the importance of intangible resources like

innovation and reputation. Especially in mature brands, sustaining reputation is essential.

Tangible Resources:

Financial: Financially sound. However, capital was tied up in large investments in

brewing facilities.

Physical: Owned significant brewery capacity – 90% of products could be produced in

Technological: Creation of subsidiary Alchemy & Science to research brewing

Organizational: Good relationships with its subsidiary and distributors indicate it has the

Intangible Resources:

Human: Knowledgeable sales people able to increase brand awareness, educate

distributors and the public on the benefits of craft beer in general and Boston Beer

products in specific.

Innovation and creativity: Appears to be a strength based on the continual expansion of

Reputation: So far, a real strength based on awards won in competition against both

Determining whether the internal resources are valuable, rare, difficult to imitate, or

difficult to substitute (VRIN) can help a firm sustain a competitive advantage. See

Chapter 3, Exhibit 3.6. Applying the VRIN concept, it’s hard to identify any true in-

APPENDICES:

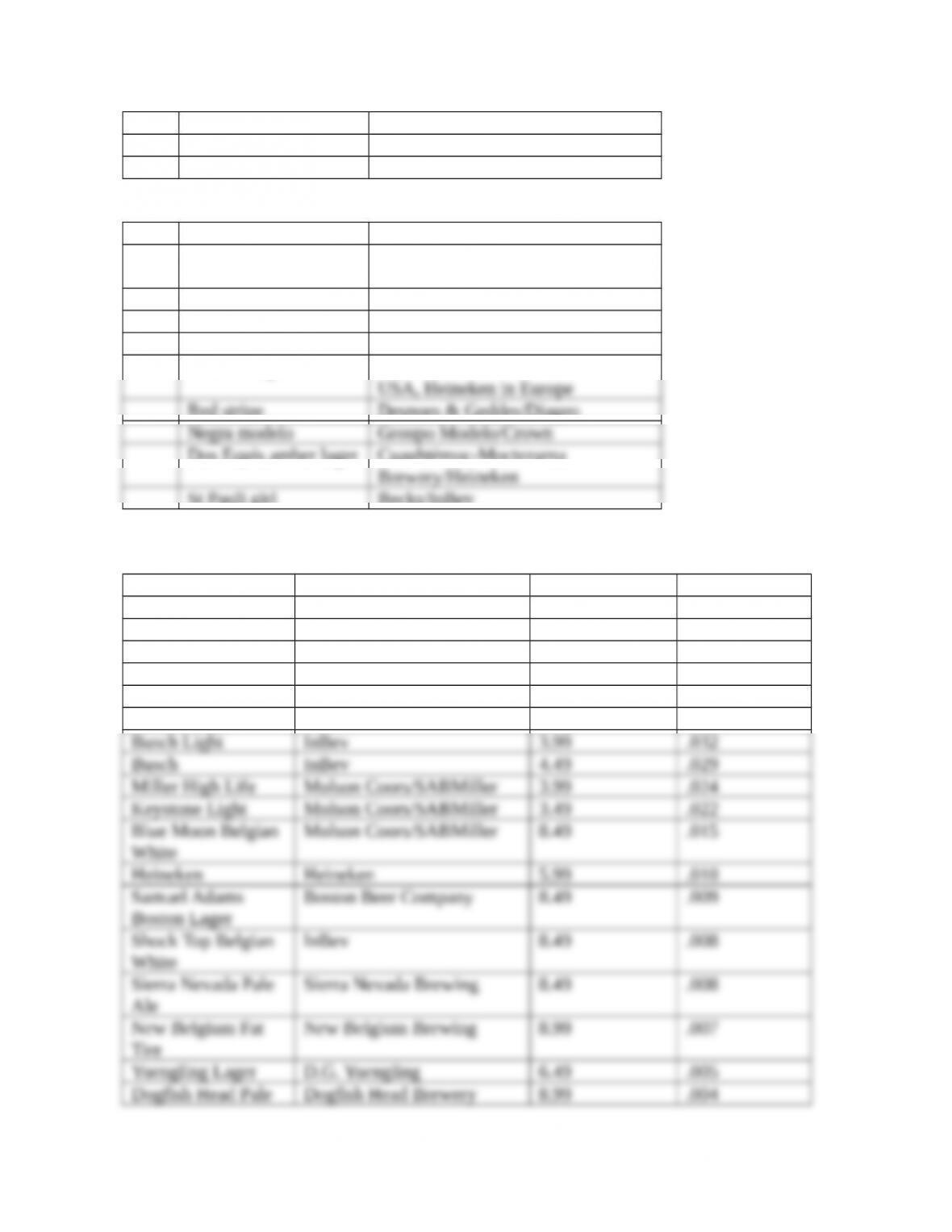

Exhibit 5 - Top Imported Beers/Brewers in U.S.

Ran

k

Brand Brewer/Importer

1 Corona Grupo Modelo/Crown

2 Heineken Heineken

3 Modelo especial Groupo Modelo/Crown

4 Dos Equis XX Lager

Cuauhtémoc-Moctezuma

5 Corona light Groupo Modelo/Crown

6 Stella artois InBev

7 Tecate Cuauhtémoc-Moctezuma

8 Labatt blue Labatt Brewing/InBev

8 Labatt blue light Labatt Brewing/InBev

10 Newcastle brown ale John Smith’s Brewery/Heineken

11 Heineken premium Heineken

UNRANKED Order from 2011 Results

Guinness draught St. James Gate/Guinness &

Co./Diageo

Beck’s InBev

Pacifico Groupo Modelo/InBev/Crown

Amstel light Heineken

Foster’s lager Fosters/Molson/SABMiller in the

Red stripe Desnoes & Geddes/Diageo

Dos Equis amber lager Cuauhtémoc-Moctezuma

St Pauli girl Becks/InBev

Exhibit 9 - U.S. Domestic Beer Brands, including Brewers

Beer Brewer $ Price/6 pack Market share

Bud Light InBev 4.99 .198

Coors Light Molson Coors/SABMiller 4.99 .097

Budweiser InBev 4.99 .074

Miller Light Molson Coors/SABMiller 4.99 .041

Corona Extra Crown 7.99 .035

Natural Light InBev 3.49 .035

Ale

Brooklyn Brewery

Lager

Brooklyn Brewery 7.99 .004

HOW DOES BEER GET MADE?

For fun, see National Geographic’s Ultimate Factories Budweiser episode at

http://channel.nationalgeographic.com/channel/videos/budweiser/

The steps in brewing:

What processes do you think Anheuser-Busch InBev might outsource?

See http://www.budweiser.com/en/our-beer/default.aspx#/our-beer/five-ingredients-no-

compromise/index for more info on the Budweiser process. See

http://www.howtobrew.com/section1/chapter2-3.html for info on how to brew beer at