EPILOGUE

In July 2010, GreenWood’s senior management submitted the final investment report for

the Luxi project to the investment committee for approval. The committee rejected the

Although GreenWood worked out a payment agreement with the Luxi Forestry Bureau so

that only half of the annual land lease expenses would have to be paid upfront (and the

Jeff voted in favor of the project but he said he understood the concerns expressed by the

Brian believed that the decision reflected Oriental’s lack of familiarity with the Chinese

market. A key consequence of this decision was that GreenWood completely dropped

Shortly afterwards, the investment committee also accepted GreenWood’s senior

management’s recommendation not to pursue the Dongji project because of the potential

reputation risk. As described in the case, Wanli Afforestation Group and Yilin Wood

With both the Luxi and Dongji projects out of consideration, a potential project in Jiangxi

province which was initially not a priority (but still being considered) came into the

Brian explained that the reason this project moved so fast was partly due to the

experiences resulting from the Luxi and Dongji projects and partly due to the Chinese

The tree assets acquired, however, were mainly pine and fir trees whose rotation is about

20-25 years, which appeared to be inconsistent with GreenWood’s expertise and strategic

focus. Brian explained that GreenWood updated its strategy to capture and expand its

References

Porter, M., & Kramer, M. 2006. “Strategy and Society: The Link between Competitive

Hennart, J. F. 2009. “Down with MNE-centric theories! Market entry and expansion as

Appendices

EXHIBIT IM-1: GREENWOOD’S RESOURCES AND CAPABILITIES PRIOR TO

INTERNATIONAL EXPANSION IN 2005

GreenWood’s

Tangible Resources

Physical Resources • Small tree plantations, nurseries, and office facilities in Oregon, U.S.

Financial Resources • Fees from managing the tree plantation assets.

Human Resources • Strategic staff (in research) acquired.

Organizational Resources • Certain cultivation methods (mechanical and chemical methods of

• Elite plant materials.

GreenWood’s Intangible

Resources and Capabilities

Qualities of Human

Resources • Accumulated knowledge of the Chinese market and culture.

• Experience in plantation management and scientific development.

Organizational capabilities • Ability to envision the future of tree plantation and its role as a

• Research capabilities for developing elite plant materials

continuously.

•Expertise in poplar hybridization and genetic improvement.

•Some experience in adapting elite plant materials to the

•Integrated silvicultural management including land preparation, spacing

• Social networking:

•Jeff Nuss’s professional networking capabilities.

•Dr. Stanton’s relationship with the WorldBank and various

•GreenWood’s relationship development with the practitioners

EXHIBIT IM-2: COMPARISON OF ALTERNATIVE ENTRY MODES

Advantages Disadvantages

Licensing or selling plant materials No need to get directly involved in

Earning licensing fees or sales

Lack of control and global

Developing potential competitors.

High transaction costs due to

Joint Venture Risk sharing with local partners.

Getting access to the resources and

Circumventing institutional and

Possible benefits due to local

Potential dilution of ownership

advantages.

Difficult to achieve global

Acquisition Rapid market entry.

Ownership of local facilities and

Likely pay a premium.

Difficult post-acquisition integration

Greenfield Full control of know-how and

Global coordination and knowledge

Potential high costs and risks due to

EXHIBIT IM-3: POTENTIAL BENEFITS AND RISKS IN PARTNERING

Benefits Risks

Luxi Forestry Bureau Provision of access to

Possible dilution of some ownership

land

Provision of crop care labor forces.

Assistance in overcoming cultural

and institutional distances due to its

Unpredictable change of leadership.

Dongji Lideng Forestry

Provision of access to

Provision of crop care labor forces.

Contributing plant materials

Assisting in circumventing

Becoming a potential competitor in

Reputation risks due to its close

collaboration with two large private

EXHIBIT IM-4: COMPARISON OF ECONOMIC IMPLICATIONS: LUXI VERSUS DONGJI

Luxi Dongji

Pros ●Favorable natural conditions

●Luxi’s estimated annual tree growth

rate will increase from 1.2 m3/mu

(e.g., 2600 mills in Linyi —huge

●Accessible to the export markets.

●It is cheap to acquire tree

●The land lease rate is low.

●Lideng has patented deep

●Lideng has government approval

to establish an additional 300,000

●Local demand in Dongji far

Cons ●The upfront investment in the

●It can be difficult and risky to work

with the government agencies. For

●The environmental conditions are

●Not readily accessible to the

Conclusion Both projects seem to be economically attractive; the economic risks appear to

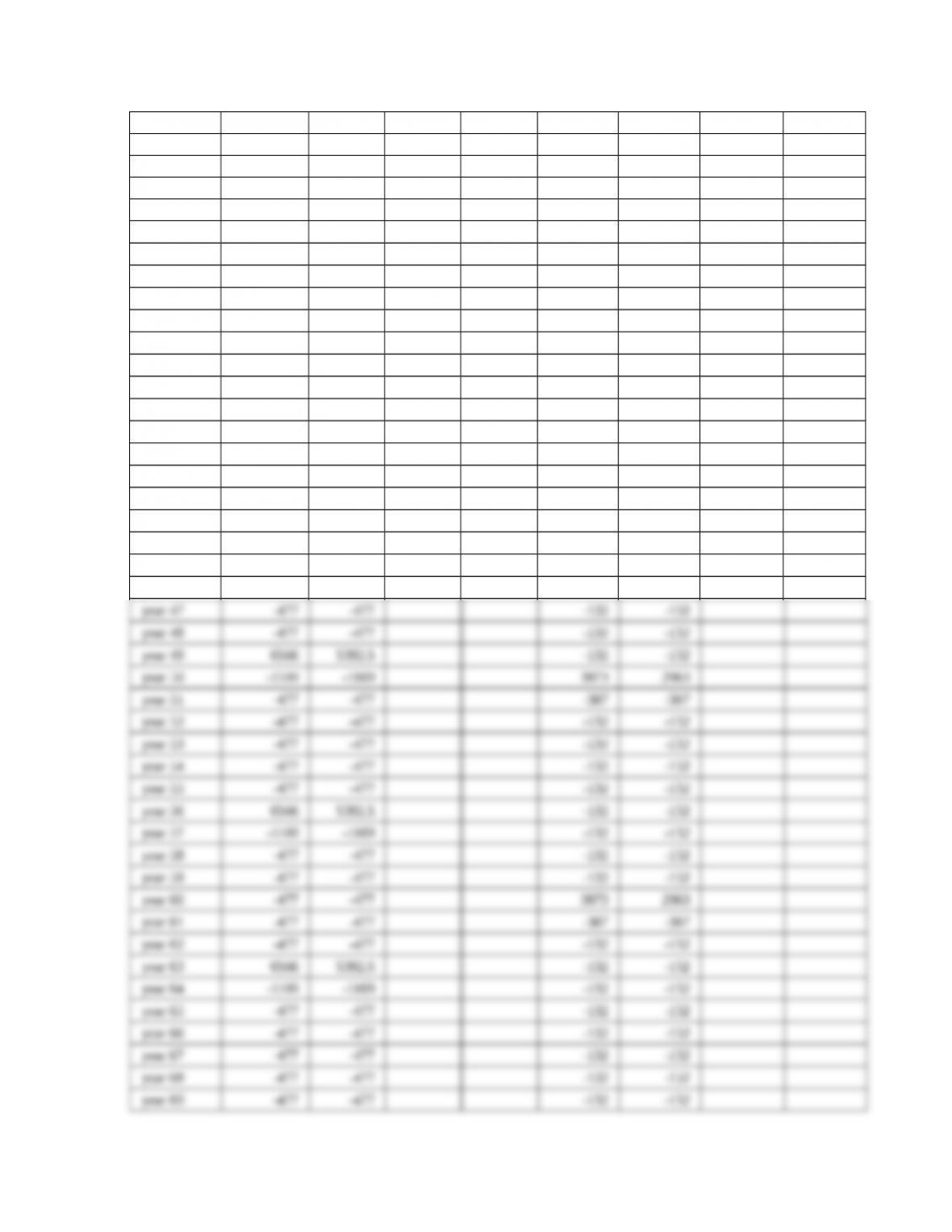

EXHIBIT IM-5: IRR AND NPV ESTIMATES (PER MU): LUXI VERSUS DONGJI

Luxi Dongji

Senario 1 Senario 2 Senario 3 Senario 4 Senario 1 Senario 2 Senario 3 Senario 4

Luxi (1.8) Luxi (1.5) Luxi (1.5) Luxi (1.5) Dongji

(0.9)

Dongji

(0.7)

Dongji

(0.7)

Dongji

(0.7)

NPV ¥1,473.10 ¥237.06 ¥260.14 ¥220.22 ¥815.90 ¥257.66 ¥275.98 ¥242.50

IRR 16.2% 11.1% 11.3% 11.1% 17.0% 12.5% 12.7% 12.5%

year 1 -1109 -1109 -1109 -1109 -387 -387 -387 -387

year 2 -477 -477 -477 -477 -132 -132 -132 -132

year 3 -477 -477 -477 -477 -132 -132 -132 -132

year 4 -477 -477 -477 -477 -132 -132 -132 -132

year 5 -477 -477 -477 -477 -132 -132 -132 -132

year 6 -477 -477 -477 -477 -132 -132 -132 -132

year 7 6566 5392.5 5392.5 5392.5 -132 -132 -132 -132

year 8 -1109 -1109 -1109 -1109 -132 -132 -132 -132

year 9 -477 -477 -477 -477 -132 -132 -132 -132

year 10 -477 -477 -477 -477 3873 2983 2983 2983

year 25 -477 -477 -477 -477 -132 -132 -132 -132

year 26 -477 -477 -477 -477 -132 -132 -132 -132

year 27 -477 -477 -477 -477 -132 -132 -132 -132

year 28 6566 5392.5 5392.5 5392.5 -132 -132 -132 -132

year 29 -1109 -1109 633.25 0 -132 -132 -132 -132

year 30 -477 -477 3873 2983 2983 2983

year 31 -477 -477 -387 -387 642.5 0

year 32 -477 -477 -132 -132

year 33 -477 -477 -132 -132

year 34 -477 -477 -132 -132

year 35 6566 5392.5 -132 -132

year 36 -1109 -1109 -132 -132

year 37 -477 -477 -132 -132

year 38 -477 -477 -132 -132

year 39 -477 -477 -132 -132

year 40 -477 -477 3873 2983

year 41 -477 -477 -387 -387

year 42 6566 5392.5 -132 -132

year 43 -1109 -1109 -132 -132

year 44 -477 -477 -132 -132

year 45 -477 -477 -132 -132

year 46 -477 -477 -132 -132

EXHIBIT IM-6: SOCIAL AND ENVIRONMENTAL IMPACT ANALYSIS: LUXI VERSUS

DONGJI

Strategic :

long term

competitive

advantages

Luxi

● GreenWood’s investment in tree plantation assets can facilitate local economic development. For

● GreenWood’s advanced silvicultural management (including adopting FSC standards) can generate

●Locally tested, GreenWood’s elite poplar plant materials can enhance tree growth rate and pest

Non-strategic ●GreenWood can help set up a small wood •

GreenWood can help combat

processing mill with an estimated investment desertification in Dongji (1.5

of US$750,000. The mill, associated with million mu is available for poplar

high value-added activities, will provide plantation), which will also help

GreenWood.)

●GreenWood’s investment can help

“clean up” local business practices

Strategic

Importance

Activities

Overall, GreenWood’s long term competitive advantages and positive social impact will be

more mutually reinforcing from the Luxi project than from the Dongji project because

Dongji

●GreenWood’s investment in tree

plantation assets can facilitate

local economic development. For

●GreenWood’s advanced

silvicultural management