CONSTRAINTS

Time Horizon. Two-time horizons are applicable to Fairfax’s life. The first time horizon

represents the period during which Fairfax should set up her financial situation in

preparation for the balance of the second time horizon, her retirement period of

Liquidity. With liquidity defined either as income needs or as cash reserves to meet

Taxes. Fairfax’s taxable income (salary, taxable investment income, and realized capital

gains on securities) is taxed at a 35 percent rate. Careful tax planning and coordination with

Laws and Regulations. Fairfax should be aware of, and abide by, any securities (or other)

laws or regulations relating to her insider status at Reston and her holding of Reston stock.

Although there is no trust instrument in place, if Fairfax’s future investing is handled by an

Unique Circumstances and/or Preferences. The value of the Reston stock dominates the

value of Fairfax’s portfolio. A well-defined exit strategy needs to be developed for the stock

as soon as is practical and appropriate. If the value of the stock increases, or at least does not

Synopsis. The policy governing investment in Fairfax’s Savings Portfolio will put emphasis

on realizing a 3 percent real, after-tax return from a mix of high-quality assets with less than

b. Critique. The Coastal proposal produces a real, after-tax expected return of

approximately 5.18 percent, which exceeds the 3 percent level sought by Fairfax. The

expected return for this proposal can be calculated by first subtracting the tax-exempt

The 4 percent inflation rate is subtracted to produce the expected real after-tax return:

This result can also be obtained by computing these returns for each of the individual

From the data available, it is not possible to determine specifically the inherent degree of

Allocation of equity assets. Exposure to equity assets will be necessary in order to achieve

the return requirements specified by Fairfax; however, greater diversification of these

assets among other equity classes is needed to produce a more efficient, potentially less

volatile portfolio that would meet both her risk tolerance parameters and her return

Cash allocation. Within the proposed fixed-income component, the 15 percent

Corporate/municipal bond allocation. The corporate bond allocation (10 percent) is

Venture capital allocation. The allocation to venture capital is questionable given Fairfax’s

policy statement indicating that she is quite risk averse. Although venture capital may

Lack of risk/volatility information. The proposal concentrates on return expectations and

c. (i) Fairfax has stated that she is seeking a 3 percent real, after-tax return. Table 28G provides

nominal, pretax figures, which must be adjusted for both taxes and inflation in order to

ascertain which portfolios meet Fairfax’s return objective. A simple solution is to subtract

Alternatively, this can be calculated as follows: multiply the taxable returns by their

respective allocations, sum these products, adjust for the tax rate, add the result to the

product of the nontaxable (municipal bond) return and its allocation, and deduct the

inflation rate from this sum. For Allocation A:

Allocation

Return Measure A B C D E

(ii) Fairfax has stated that a worst case return of –10 percent in any 12-month period

would be acceptable. The expected return less two times the portfolio risk (expected

standard deviation) is the relevant risk tolerance measure. In this case, three allocations

meet the criterion: A, C, and E.

Allocation

Parameter A B C D E

Expected return 9.9% 11.0% 8.8% 14.4% 10.3%

d. (i) The Sharpe Ratio for Allocation D, using the cash equivalent rate of 4.5

e. The recommended allocation is A. The allocations that meet both the minimum real,

after-tax objective and the maximum risk tolerance objective are A and E. These

allocations have identical Sharpe Ratios and both of these allocations have large

7. a. The key elements that should determine the foundation’s grant-making (spending)

policy are

(i) Average expected inflation over a long time horizon;

To preserve the real value of its assets and to maintain its spending in real terms, the

foundation cannot pay out more, on average over time, than the real return it earns from its

b. OBJECTIVES

Return Requirement: Production of current income, the committee’s focus before Mr.

Franklin’s gift, is no longer a primary objective, given the increase in the asset base and

the committee’s understanding that investment policy must accommodate long-term as

well as short-term goals. The need for a minimum annual payout equal to 5 percent of

Risk Tolerance: The increase in the foundation’s financial flexibility arising from Mr.

CONSTRAINTS

Liquidity Requirements: Liquidity needs are low, with little likelihood of unforeseen

demands requiring either forced asset sales or immense cash. Such needs as exist,

Time Horizon: The foundation has a virtually infinite life; the need to plan for future as

Taxes: Tax-exempt under present U.S. law if the annual minimum payout requirement

Legal and Regulatory: Governed by state law and prudent person standards; ongoing

Unique Circumstances: The need to maintain real value after grants is a key

Narrative: Investment actions shall take place in a long-term, tax-exempt context,

c. To meet requirements of this scenario, it is first necessary to identify a spending rate that

is both sufficient (i.e., 5 percent or higher in nominal terms) and feasible (i.e., prudent

and attainable under the circumstances represented by the Table 26H data and the

The allocation philosophy will reflect the foundation’s need for real returns at or above

the grant rate, its total return orientation, its above-average risk tolerance, its low liquidity

1. Allocations to fixed income instruments will be less than 50 percent as bonds have

provided inferior real returns in the past, and while forecasted real returns from 1993 to

2. Allocations to equities will be greater than 50 percent, and this asset class will be the

3. Within the equity universe there is room in this situation for small-cap as well as

4. Given its value as an alternative to stocks and bonds as a way to maintain real return

An example of an appropriate, modestly aggressive allocation is shown below. Table 28H

contains an array of historical and expected return data which was used to develop real

Intermediate Term

Forecast of

Real Returns

Recommended

Allocation

Real Return

Contribution

Cash (U.S.) T-bills 0.7% *0%

Bonds:

International 4.9 10 0.490

*Cash is excluded— ongoing cash flow from the portfolio should be sufficient to

meet all normal working capital needs.

8. a. The Maclins’ overall risk objective must consider both willingness and ability to take

risk.

Willingness: The Maclins have a below-average willingness to take risk, based on their

Ability: The Maclins have an average ability to take risk. While their large asset base and

a long time horizon would otherwise suggest an above-average ability to take risk, their

Overall: The Maclins’ overall risk tolerance is below average, as their below-average

b. The Maclins’ return objective is to grow the portfolio to meet their educational and

retirement needs as well as to provide for ongoing net expenses. The Maclins will require

The after-tax return required to accumulate £2 million in 18 years, beginning with an

investable base of £1,235,000 (calculated below) and with annual outflows of

Annual cash flow = –£26,000

Asset base = £1,235,000

Less one-time needs:

Note: No inflation adjustment is required in the return calculation because increases

in living expenses will be offset by increases in Christopher’s salary.

c. The Maclins’ investment policy statement should include the following constraints:

(i) Time horizon: The Maclins have a two-stage time horizon because of their changing

(ii) Liquidity requirements: The Maclins have one-time immediate expenses (£50,000)

(iii) Tax concerns: The U.K. has a 40 percent marginal tax rate on both ordinary income

and capital gains. Therefore there is no preference for investment returns from taxable

(iv) Unique circumstances: The large holding of the Barnett Co. common stock

(representing 18 percent of the Maclins’ total portfolio) and the resulting lack of

9. a. 1. The cash reserve is too high.

The 15 percent (or £185,250) cash allocation is not consistent with the liquidity

constraint.

2. The 15 percent allocation to Barnett Co. common stock is too high.

The risk of holding a 15 percent position in Barnett stock, with a standard deviation of

3. Shortfall risk exceeds the limitation of –12 percent return in any one year.

The Maclins have stated that their shortfall risk limitation is –12 percent return in any

This is below their shortfall risk limitation.

4. The expected return is too low (the allocation between stocks and bonds is not consistent

with return objective).

The portfolio’s expected return of 6.70 percent is less than the return objective of 7.38

percent.

b. Note: The Maclins have purchased their home and made their charitable contribution.

Cash: 0% to 3%

U.K. corporate bonds: 50% to 60%

The Maclins need significant exposure to this less volatile asset class, given their

The Maclins must meet their return objective while addressing their risk tolerance. U.S.

The Maclins’ below-average risk tolerance includes a shortfall risk limitation of –12

percent return in any one year, and the Barnett stock is very volatile. There is too much

stock-specific (nonsystematic) risk in this concentrated position for such an investor. They

also have employment risk with Barnett. Therefore the lowest allocation to Barnett stock is

most appropriate.

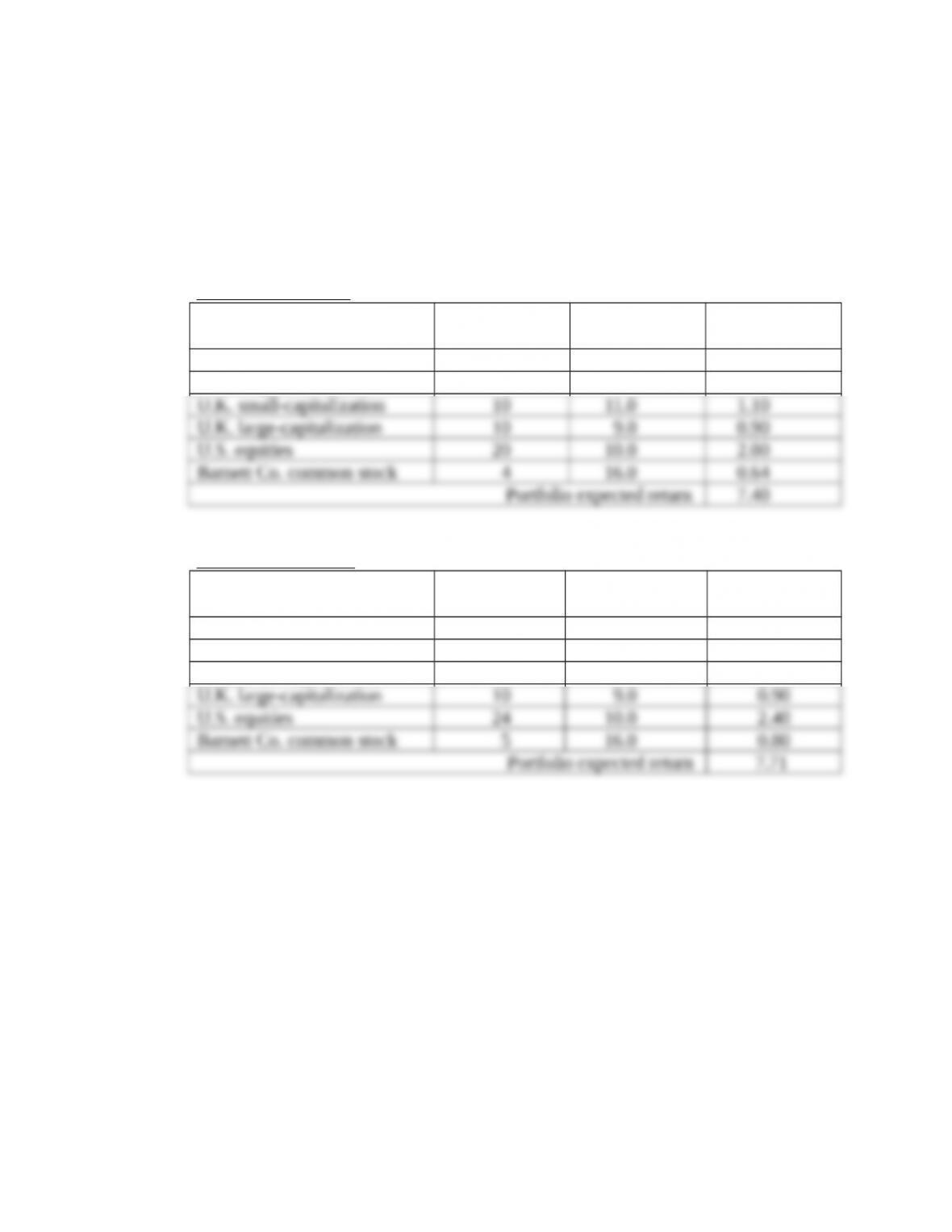

The following sample allocations are provided to illustrate that selected ranges meet

the return objective.

Sample allocation 1:

Asset Class Weight (%) Return (%)

Weighted

Return (%)

Cash 1 1.0 0.01

U.K. corporate bonds 55 5.0 2.75