CHAPTER 24: PORTFOLIO PERFORMANCE EVALUATION

CHAPTER 24: PORTFOLIO PERFORMANCE EVALUATION

PROBLEM SETS

1. The dollar-weighted average will be the internal rate of return between the initial and

final value of the account, including additions and withdrawals. Using Excel’s XIRR

function, utilizing the given dates and values, the dollar-weighted average return is as

follows:

Date Account

1/1/2016 -$148,000.00

1/3/2016 $2,500.00

Since the dates of additions and withdrawals are not equally spaced, there really is no

way to solve this problem using a financial calculator. Excel can solve this very

quickly.

2. As established in the following result from the text, the Sharpe ratio depends on both

alpha for the portfolio (

P

a

) and the correlation between the portfolio and the market

index (ρ):

( ) αρ

σ σ

P f P

M

P P

E r r S

–= +

Specifically, this result demonstrates that a lower correlation with the market index

reduces the Sharpe ratio. Hence, if alpha is not sufficiently large, the portfolio is

3. The IRR (i.e., the dollar-weighted return) cannot be ranked relative to either the

geometric average return (i.e., the time-weighted return) or the arithmetic average

24-1

CHAPTER 24: PORTFOLIO PERFORMANCE EVALUATION

return. Under some conditions, the IRR is greater than each of the other two averages,

and similarly, under other conditions, the IRR can also be less than each of the other

averages. A number of scenarios can be developed to illustrate this conclusion. For

4. It is not necessarily wise to shift resources to timing at the expense of security

selection. There is also tremendous potential value in security analysis. The decision as

Stock XYZ has greater dispersion.

(Note: We used 5 degrees of freedom in calculating standard deviations.)

c. Geometric average:

Despite the fact that the two stocks have the same arithmetic average, the

e. Even though the dispersion is greater, your expected rate of return would

still be the arithmetic average, or 10%.

f. In terms of “forward-looking” statistics, the arithmetic average is the

6. a. Time-weighted average returns are based on year-by-year rates of return:

24-2

CHAPTER 24: PORTFOLIO PERFORMANCE EVALUATION

Year Return = (Capital gains + Dividend)/Price

2016 − 2017

[($120 – $100) + $4]/$100 = 24.00%

2017 – 2018 [($90 – $120) + $4]/$120 = –21.67%

2018 − 2019 [($100 – $90) + $4]/$90 = 15.56%

Arithmetic mean: (24% – 21.67% + 15.56%)/3 = 5.96%

Geometric mean: (1.24 × 0.7833 × 1.1556)1/3 – 1 = 0.0392 = 3.92%

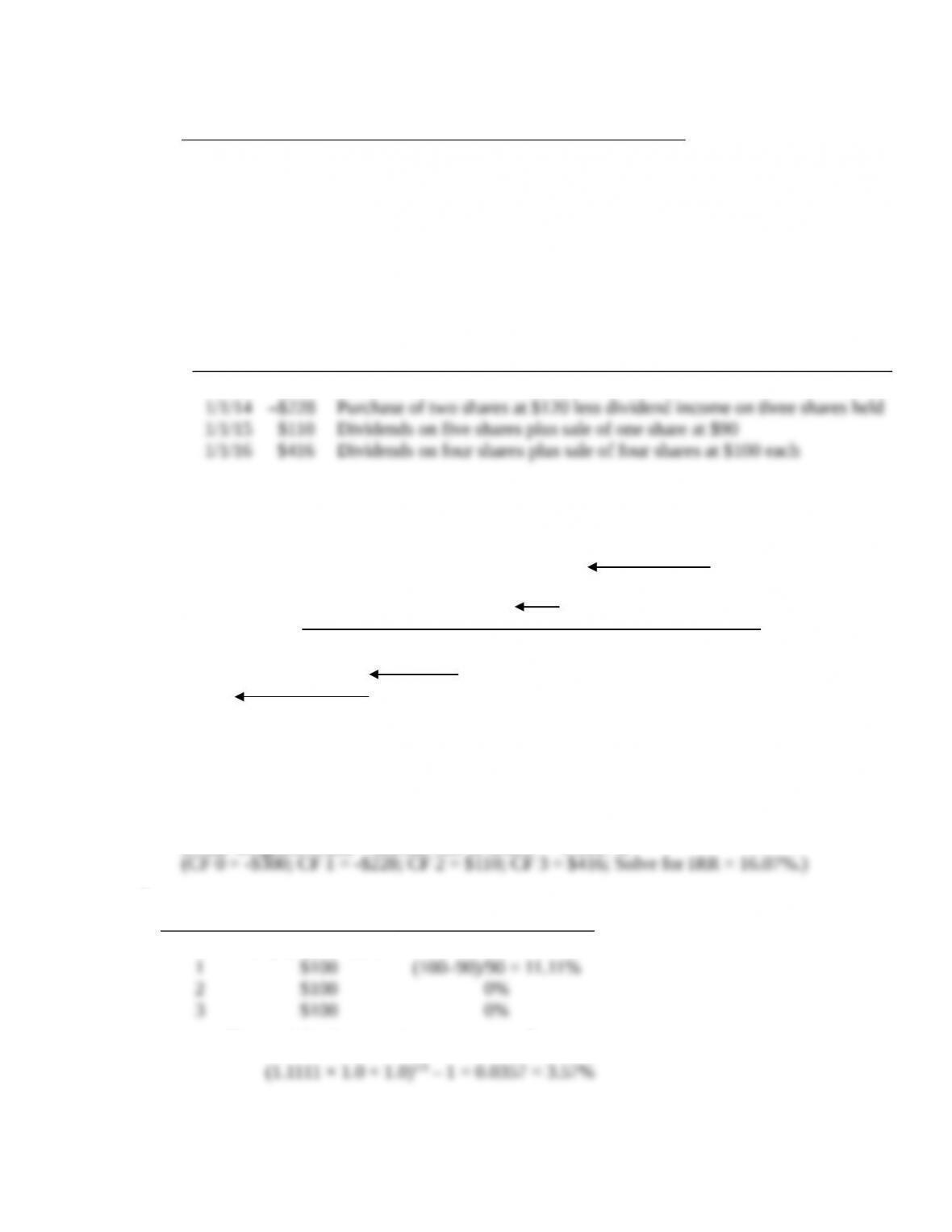

b.

Date

Cash

Flow Explanation

1/1/13 –$300 Purchase of three shares at $100 each

416

110

Date: 1/1/13 1/1/14 1/1/15 1/1/16

228

300

Dollar-weighted return = Internal rate of return = –0.1607%

7.

Time Cash Flow Holding Period Return

0 3×(–$90) = –$270

a. Time-weighted geometric average rate of return =

24-3

CHAPTER 24: PORTFOLIO PERFORMANCE EVALUATION

c. Dollar-weighted average rate of return = IRR = 5.46%

8. a. The alphas for the two portfolios are:

Ideally, you would want to take a long position in Portfolio A and a short position

in Portfolio B.

b. If you will hold only one of the two portfolios, then the Sharpe measure is the

appropriate criterion:

.12 .05 0.583

.12

A

S–

= =

.16 .05 0.355

.31

B

S–

= =

Using the Sharpe criterion, Portfolio A is the preferred portfolio.

9.

a. Stock A Stock B

(i) Alpha = regression intercept 1.0% 2.0%

Information ratio =

α

P

β

P

24-4

CHAPTER 24: PORTFOLIO PERFORMANCE EVALUATION

* To compute the Sharpe measure, note that for each stock, (rP – rf ) can be

computed from the right-hand side of the regression equation, using the assumed

† The beta to use for the Treynor measure is the slope coefficient of the

regression equation presented in the problem.

b. (i) If this is the only risky asset held by the investor, then Sharpe’s measure is the

(ii) If the stock is mixed with the market index fund, then the contribution to the

(iii) If the stock is one of many stocks, then Treynor’s measure is the

10. We need to distinguish between market timing and security selection abilities. The

intercept of the scatter diagram is a measure of stock selection ability. If the

Timing ability is indicated by the curvature of the plotted line. Lines that become

steeper as you move to the right along the horizontal axis show good timing ability.

We can therefore classify performance for the four managers as follows:

Selection

Ability Timing Ability

A. Bad Good

24-5

CHAPTER 24: PORTFOLIO PERFORMANCE EVALUATION

b. Security Selection:

(1) (2) (3) = (1) × (2)

Market

Differential Return

within Market

(Manager – Index)

Manager’s

Portfolio

Weight

Contribution to

Performance

Equity –0.5% 0.70 −0.35%

c. Asset Allocation:

(1) (2) (3) = (1) × (2)

Market

Excess Weight

(Manager – Benchmark)

Index

Return

Contribution to

Performance

Equity 0.10% 2.5% 0.25%

Summary:

b. Added value from country allocation:

(1) (2) (3) = (1) × (2)

Country Excess Weight

(Manager – Benchmark)

Index Return

minus Bogey

Contribution to

Performance

U.K. 0.15 −1.8% −0.27%

c. Added value from stock selection:

(1) (2) (3) = (1) × (2)

Differential Return

within Country Manager’s Contribution to

24-6

CHAPTER 24: PORTFOLIO PERFORMANCE EVALUATION

Country (Manager – Index) Country

weight Performance

U.K. 0.08 0.30% 2.4%

Summary:

13. Support: A manager could be a better performer in one type of circumstance than in

another. For example, a manager who does no timing but simply maintains a high beta, will

Contradict: If we adequately control for exposure to the market (i.e., adjust for beta),

14. The use of universes of managers to evaluate relative investment performance does,

b. From Black-Jensen-Scholes and others, we know that, on average, portfolios

with low beta have historically had positive alphas. (The slope of the empirical

16. a. The most likely reason for a difference in ranking is due to the absence of

diversification in Fund A. The Sharpe ratio measures excess return per unit of

24-7

CHAPTER 24: PORTFOLIO PERFORMANCE EVALUATION

17. The within sector selection calculates the return according to security selection. This is

done by summing the weight of the security in the portfolio multiplied by the return of

the security in the portfolio minus the return of the security in the benchmark:

Large Cap Sector: 0.6 (.17-.16)= 0.6%

Mid Cap Sector: 0.15 (.24 –.26) -0.3%

Small Cap Sector: 0.25 (.20-.18)= 0.5%

Total Within-Sector Selection = 0.6% – 0.3% 0.5% 0.8%

´

´ =

´

+ =

18. Primo Return

0.6 17% 0.15 24% 0.25 20% 18.8%= ´ + ´ + ´ =

Benchmark Return

0.5 16% 0.4 26% 0.1 18% 20.2%= ´ + ´ + ´ =

Primo – Benchmark = 18.8% − 20.2% = -1.4% (Primo underperformed benchmark)

To isolate the impact of Primo’s pure sector allocation decision relative to the

benchmark, multiply the weight difference between Primo and the benchmark

portfolio in each sector by the benchmark sector returns:

(0.6 0.5) (.16) (0.15 0.4) (.26) (0.25 0.1) (.18) 2.2%– ´ + – ´ + – ´ =-

To isolate the impact of Primo’s pure security selection decisions relative to the

benchmark, multiply the return differences between Primo and the benchmark for each

sector by Primo’s weightings:

(.17 .16) (.6) (.24 .26) (.15) (.2 0.18) (.25) 0.8%– ´ + – ´ + – ´ =

19. Because the passively managed fund is mimicking the benchmark, the

2

R

of the

20. a. The euro appreciated while the pound depreciated. Primo had a greater stake in

the euro-denominated assets relative to the benchmark, resulting in a positive

CHAPTER 24: PORTFOLIO PERFORMANCE EVALUATION

24-9