CHAPTER 22: FUTURES MARKETS

CHAPTER 22: FUTURES MARKETS

PROBLEM SETS

1. There is little hedging or speculative demand for cement futures, since cement prices

are fairly stable and predictable. The trading activity necessary to support the futures

2. The ability to buy on margin is one advantage of futures. Another is the ease with which

3. Short selling results in an immediate cash inflow, whereas the short futures

position does not:

Action Initial CF Final CF

4. a. False. For any given level of the stock index, the futures price will be lower

5. The futures price is the agreed-upon price for deferred delivery of the asset. If that

price is fair, then the value of the agreement ought to be zero; that is, the contract

6. Because long positions equal short positions, futures trading must entail a

22-1

CHAPTER 22: FUTURES MARKETS

7. a. The closing futures price for the September contract was 2082.70, which has a

dollar value of:

b. The futures price increases by: $2090.00 – 2082.70 = $7.30

c. Following the reasoning in part (b), any change in F is magnified by a ratio of

8. a. F0 = S0(1 + rf ) = $150 × 1.03 = $154.50

9. a. Take a short position in T-bond futures, to offset interest rate risk. If rates

c. You want to protect your cash outlay when the bond is purchased. If bond

b. If the T-bill rate is less than the dividend yield, then the futures price should be

11. The put-call parity relation states that: But spot-futures parity tells us that:

22-2

0(1 )T

f

X

C P S r

= + – +

0

(1 )

T

f

F S r= ´ +

CHAPTER 22: FUTURES MARKETS

Substituting, we find that:

12. According to the parity relation, the proper price for December futures is:

The actual futures price for December is low relative to the June price. You should

take a long position in the December contract and short the June contract.

b. The stock price falls to: 120 × (1 – 0.03) = $116.40

The increase in the futures price is 15.09, so the cash flow will be:

15. The treasurer would like to buy the bonds today but cannot. As a proxy for this

purchase, T-bond futures contracts can be purchased. If rates do in fact fall, the

Arbitrage Portfolio CF now CF in 1 year

22-3

0

0 0 0

[ (1 ) ]

(1 )

T

f

T

f

S r

P C S C S S C

r

´ +

= – + = – + =

+

CHAPTER 22: FUTURES MARKETS

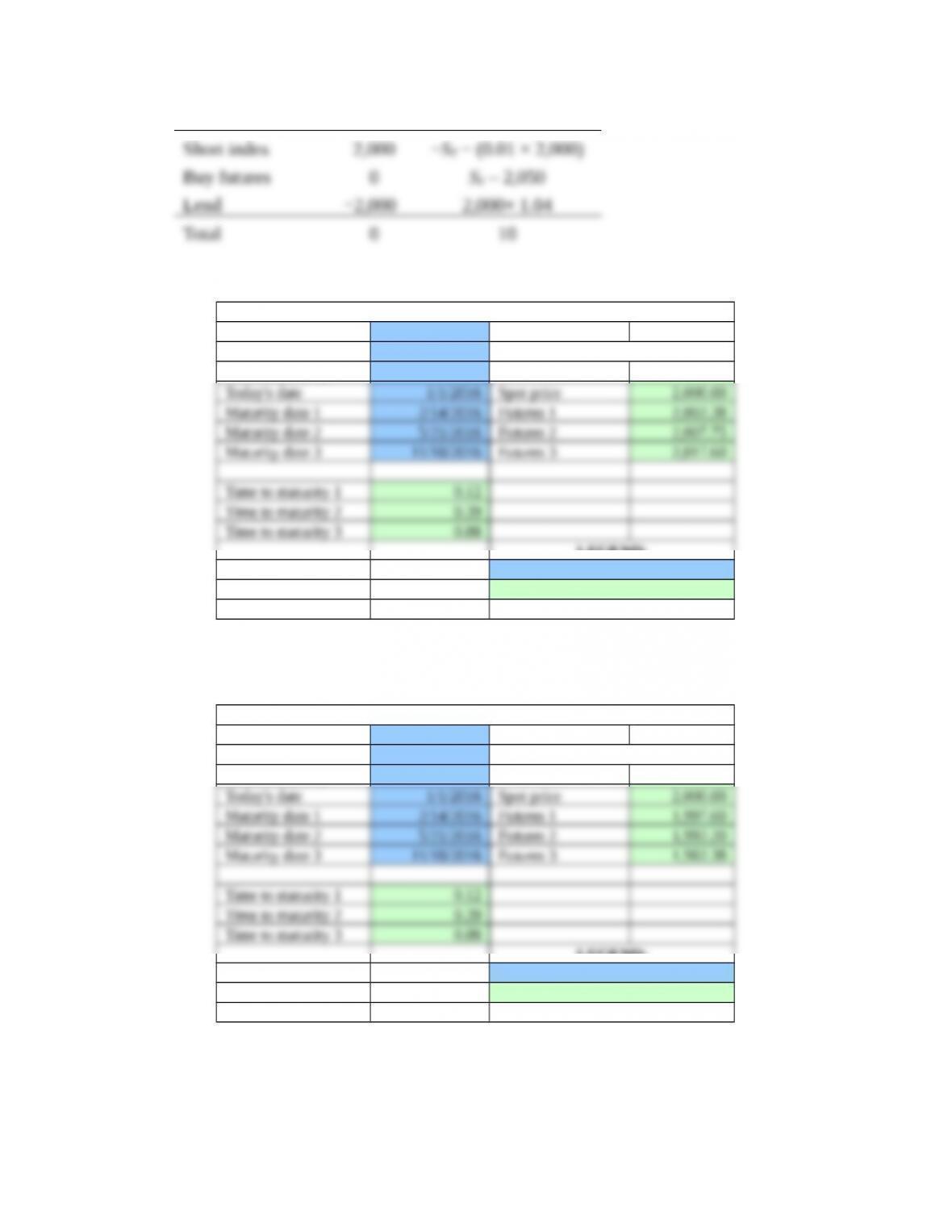

17. a. Futures prices are determined from the spreadsheet as follows:

Spot Futures Parity and Time Spreads

Spot price 2,000

Income yield (%) 2.0 Futures prices versus maturity

Interest rate (%) 3.0

LEGEND:

Enter data

Value calculated

See comment

b. The spreadsheet demonstrates that the futures prices now decrease with

increased income yield:

Spot Futures Parity and Time Spreads

Spot price 2,000

Income yield (%) 4.0 Futures prices versus maturity

Interest rate (%) 3.0

LEGEND:

Enter data

Value calculated

See comment

22-4

CHAPTER 22: FUTURES MARKETS

18. a. The current yield for Treasury bonds (coupon divided by price) plays the role of

the dividend yield.

b. When the yield curve is upward sloping, the current yield exceeds the short

19. a.

Cash Flows

Action Now T1T2

Long futures with maturity T1 0 P1 – F( T1)0

b. Since the T2 cash flow is riskless and the net investment was zero, then any

profits represent an arbitrage opportunity.

c. The zero-profit no-arbitrage restriction implies that

CFA PROBLEMS

1. a. The strategy that would take advantage of the arbitrage opportunity is a “reverse

F0 ≥ S0 (1+ C)

If the futures price is less than the spot price plus the cost of carrying the goods to

the futures delivery date, then an arbitrage opportunity exists. A trader would be

b.

Cash Flows

Action Now One year from now

22-5

CHAPTER 22: FUTURES MARKETS

22-6

CHAPTER 22: FUTURES MARKETS

Buy the commodity futures expiring in 1 year $0.00 $0.00

2. a. The call option is distinguished by its asymmetric payoff. If the Swiss franc

rises in value, then the company can buy francs for a given number of dollars

to service its debt and thereby put a cap on the dollar cost of its financing. If

the franc falls, the company will benefit from the change in the exchange rate.

b. The call option gives the company the ability to benefit from depreciation in the

franc but at a cost equal to the option premium. Unless the firm has some special

3. The important distinction between a futures contract and an options contract is that the

futures contract is an obligation. When an investor purchases or sells a futures contract,

the investor has an obligation to either accept or deliver, respectively, the underlying

Futures and options modify a portfolio’s risk in different ways. Buying or selling a

futures contract affects a portfolio’s upside risk and downside risk by a similar

4. a. The investor should sell the forward contract to protect the value of the bond

against rising interest rates during the holding period. Because the investor

22-7

CHAPTER 22: FUTURES MARKETS

b. The value of the forward contract on expiration date is equal to the spot price of

the underlying asset on expiration date minus the forward price of the contract:

The contract has a negative value. This is the value to the holder of a long position

in the forward contract. In this example, the investor should be short the forward

c. The value of the combined portfolio at the end of the six-month holding period is:

The change in the value of the combined portfolio during this six-month

The value of the combined portfolio is the sum of the market value of the

bond and the value of the short position in the forward contract. At the start

of the six-month holding period, the bond is worth $1,000 and the forward

The fact that the combined value of the long position in the bond and the short

position in the forward contract at the forward contract’s maturity date is equal

to the forward price on the forward contract at its initiation date is not a

These results support VanHusen’s statement that selling a forward contract on the

underlying bond protects the portfolio during a period of rising interest rates. The

5. a. Accurate. Futures contracts are marked to the market daily. Holding a short

position on a bond futures contract during a period of rising interest rates

22-8

CHAPTER 22: FUTURES MARKETS

b. Inaccurate. According to the cost-of-carry model, the futures contract price is

adjusted upward by the cost of carry for the underlying asset. Bonds (and other

financial instruments), however, do not have any significant storage costs.

22-9