CHAPTER 21: OPTION VALUATION

CHAPTER 21: OPTION VALUATION

PROBLEM SETS

1. The value of a put option also increases with the volatility of the stock. We see this

from the put–call parity theorem as follows:

Given a value for S and a risk-free interest rate, then, if C increases because of an

2. A $1 increase in a call option’s exercise price would lead to a decrease in the

5. A call option with a high exercise price has a lower hedge ratio. This call option is

less in the money. Both d1 and N(d1) are lower when X is higher.

6. a. Put A must be written on the stock with the lower price. Otherwise, given the

lower volatility of Stock A, Put A would sell for less than Put B.

c. Call B must have the lower time to expiration. Despite the higher price of

21-1

CHAPTER 21: OPTION VALUATION

7.

Exercise

Price

Hedge

Ratio

120

0/30 = 0.000

As the option becomes more in the money, the hedge ratio increases to a

maximum of 1.0.

8.

S d1N(d1)

45 -0.2768 0.3910

The hedge ratio is:

0 0

0 30 3

130 80 5

u d

P P

HuS dS

––

= = =-

– –

b.

Riskless

Portfolio ST = 80 ST = 130

c. The portfolio cost is: 3S + 5P = 300 + 5P

10. a. The hedge ratio for the call is:

0 0

20 0 2

130 80 5

u d

C C

HuS dS

––

= = =

– –

21-2

CHAPTER 21: OPTION VALUATION

Riskless

Portfolio S = 80 S = 130

b. Does P = C + PV(X) – S?

11. d1 = 0.2192 N(d1) = 0.5868

This value is derived from our Black-Scholes spreadsheet, but note that we could

have derived the value from put-call parity:

13. a. C falls to $5.1443

14. According to the Black-Scholes model, the call option should be priced at:

Since the option actually sells for more than $8, implied volatility is greater than 0.30.

15. A straddle is a call and a put. The Black-Scholes value would be:

21-3

CHAPTER 21: OPTION VALUATION

C + P = S0 × N(d1) Xe–rT × N(d 2) + Xe–rT × [1 N(d 2)] S0 [1 N(d1)]

= S0 × [2N(d1) 1] + Xe–rT × [1 2N(d 2)]

On the Excel spreadsheet (Spreadsheet 21.1), the valuation formula would be:

16. A. A delta-neutral portfolio is perfectly hedged against small price changes in the

underlying asset. This is true both for price increases and decreases. That is, the

18. The best estimate for the change in price of the option is

19. The number of call options necessary to delta hedge is

51, 750 75,000

0.69 =

options, or 750

options contracts, each covering 100 shares. Since these are call options, the options

should be sold short.

20. The number of calls needed to create a delta-neutral hedge is inversely proportional to

21. A delta-neutral portfolio can be created with any of the following combinations: long

stock and short calls, long stock and long puts, short stock and long calls, and short

21-4

CHAPTER 21: OPTION VALUATION

25. The hedge ratio approaches one. As S increases, the probability of exercise

26. The hedge ratio approaches 0. As X decreases, the probability of exercise

27. A straddle is a call and a put. The hedge ratio of the straddle is the sum of the hedge

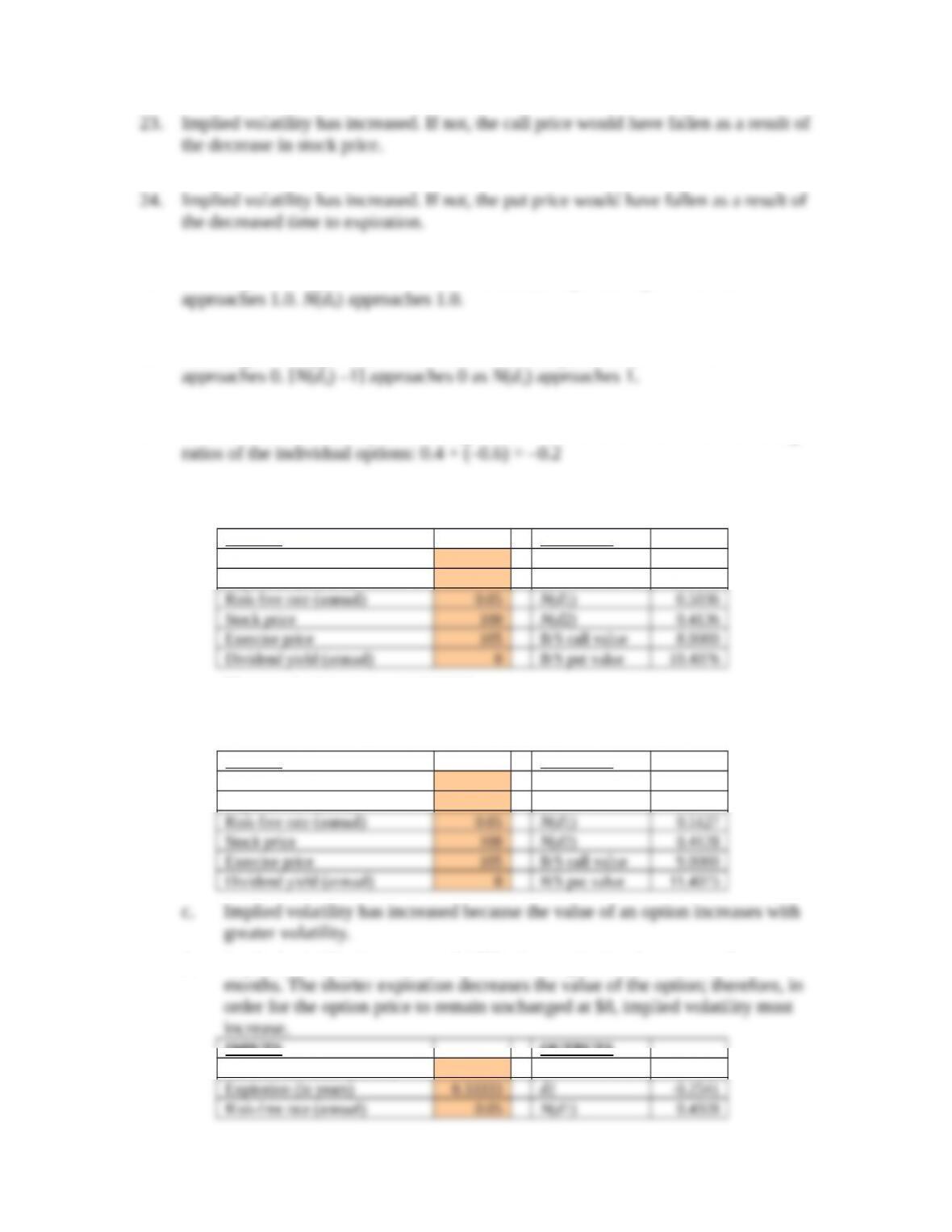

28. a. The spreadsheet appears as follows:

INPUTS OUTPUTS

Standard deviation (annual) 0.3213 d1 0.0089

Expiration (in years) 0.5 d2 -0.2183

The standard deviation is: 0.3213

b. The spreadsheet below shows the standard deviation has increased to: 0.3568

INPUTS OUTPUTS

Standard deviation (annual) 0.3568 d1 0.0318

Expiration (in years) 0.5 d2 -0.2204

d. Implied volatility increases to 0.4087 when expiration decreases to four

INPUTS OUTPUTS

Standard deviation (annual) 0.4087 d1 -0.0182

21-5

CHAPTER 21: OPTION VALUATION

INPUTS OUTPUTS

Standard deviation (annual) 0.2406 d1 0.2320

f. The decrease in stock price decreases the value of the call. In order for the

option price to remain at $8, implied volatility increases.

INPUTS OUTPUTS

Standard deviation (annual) 0.3566 d1 -0.0484

Expiration (in years) 0.5 d2 -0.3006

29. a. The delta of the collar is calculated as follows:

Position Delta

Buy stock 1.0

If the stock price increases by $1, then the value of the collar increases by

If S becomes very large, then the delta of the collar approaches zero. Both N(d1) terms

approach 1. Intuitively, for very large stock prices, the value of the portfolio is simply the

(present value of the) exercise price of the call, and is unaffected by small changes in the

stock price.

As S approaches zero, the delta also approaches zero: both N(d1) terms

21-6

CHAPTER 21: OPTION VALUATION

30. Put XDelta

CHAPTER 21: OPTION VALUATION

This payoff is identical to that of the protective put portfolio. Thus, the stock

plus bills strategy replicates both the cost and payoff of the protective put.

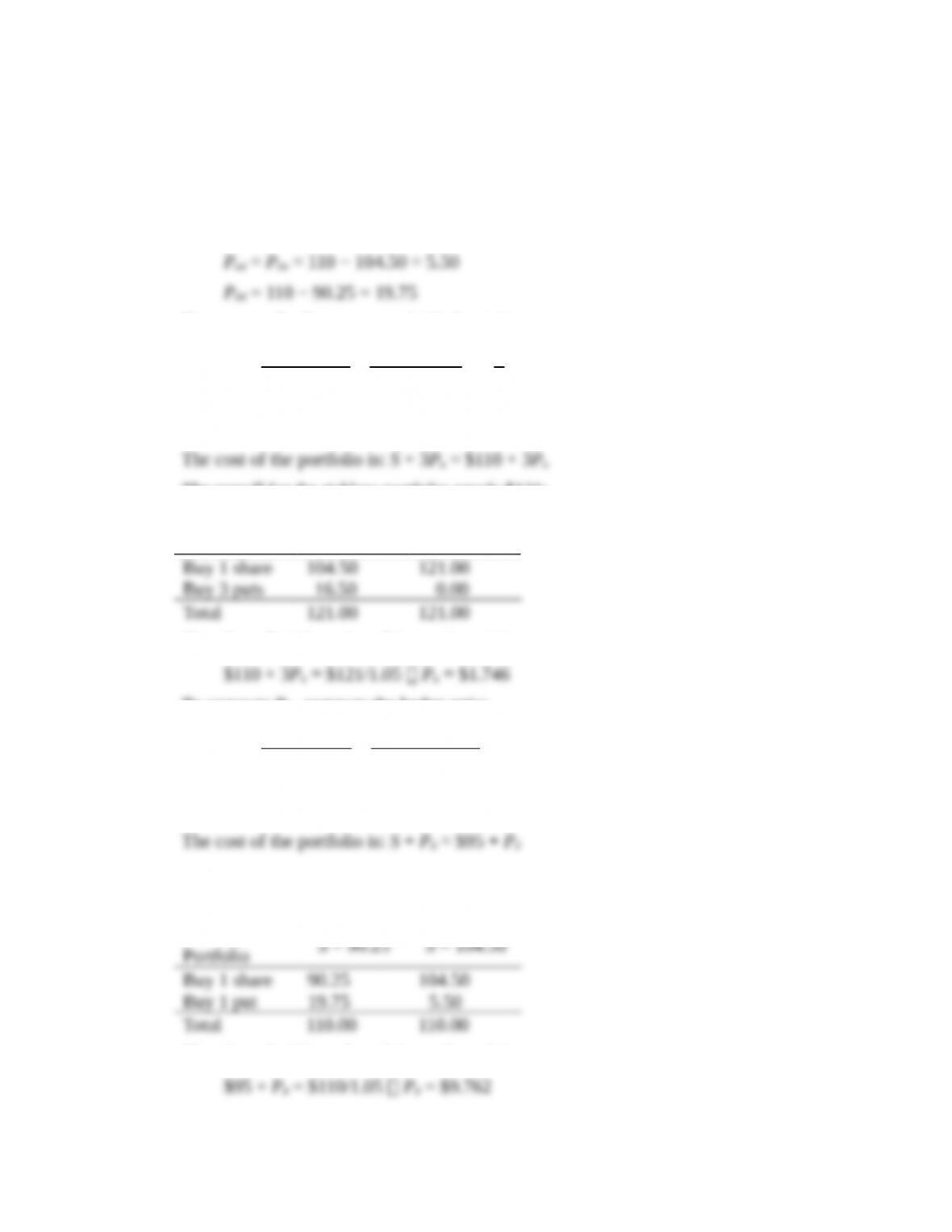

33. The put values in the second period are:

Puu = 0

To compute Pu, first compute the hedge ratio:

0 0

0 5.50 1

121 104.50 3

uu ud

P P

HuuS udS

––

= = =-

– –

Form a riskless portfolio by buying one share of stock and buying three puts.

The cost of the portfolio is: S + 3Pu = $110 + 3Pu

The payoff for the riskless portfolio equals $121:

Riskless

Portfolio S = 104.50 S = 121

Therefore, find the value of the put by solving:

To compute Pd , compute the hedge ratio:

0 0

5.50 19.75 1.0

104.50 90.25

du dd

P P

HduS ddS

––

= = =-

– –

Form a riskless portfolio by buying one share and buying one put.

The payoff for the riskless portfolio equals $110:

Riskless

Therefore, find the value of the put by solving:

21-8

CHAPTER 21: OPTION VALUATION

To compute P, compute the hedge ratio:

0 0

1.746 9.762 0.5344

110 95

u d

P P

HuS dS

––

= = =-

– –

Form a riskless portfolio by buying 0.5344 of a share and buying one put.

The cost of the portfolio is: 0.5344S + P = $53.44 + P

The payoff for the riskless portfolio equals $60.53:

Therefore, find the value of the put by solving:

Finally, we verify this result using put-call parity. Recall from Example 21.1 that:

Put-call parity requires that:

Except for minor rounding error, put-call parity is satisfied.

34. If r = 0, then one should never exercise a put early. There is no “time value cost” to

waiting to exercise, but there is a “volatility benefit” from waiting. To show this

more rigorously, consider the following portfolio: lend $X and short one share of

35. a. XerT

b. X

21-9

CHAPTER 21: OPTION VALUATION

e. It is optimal to exercise immediately a put on a stock whose price has fallen to

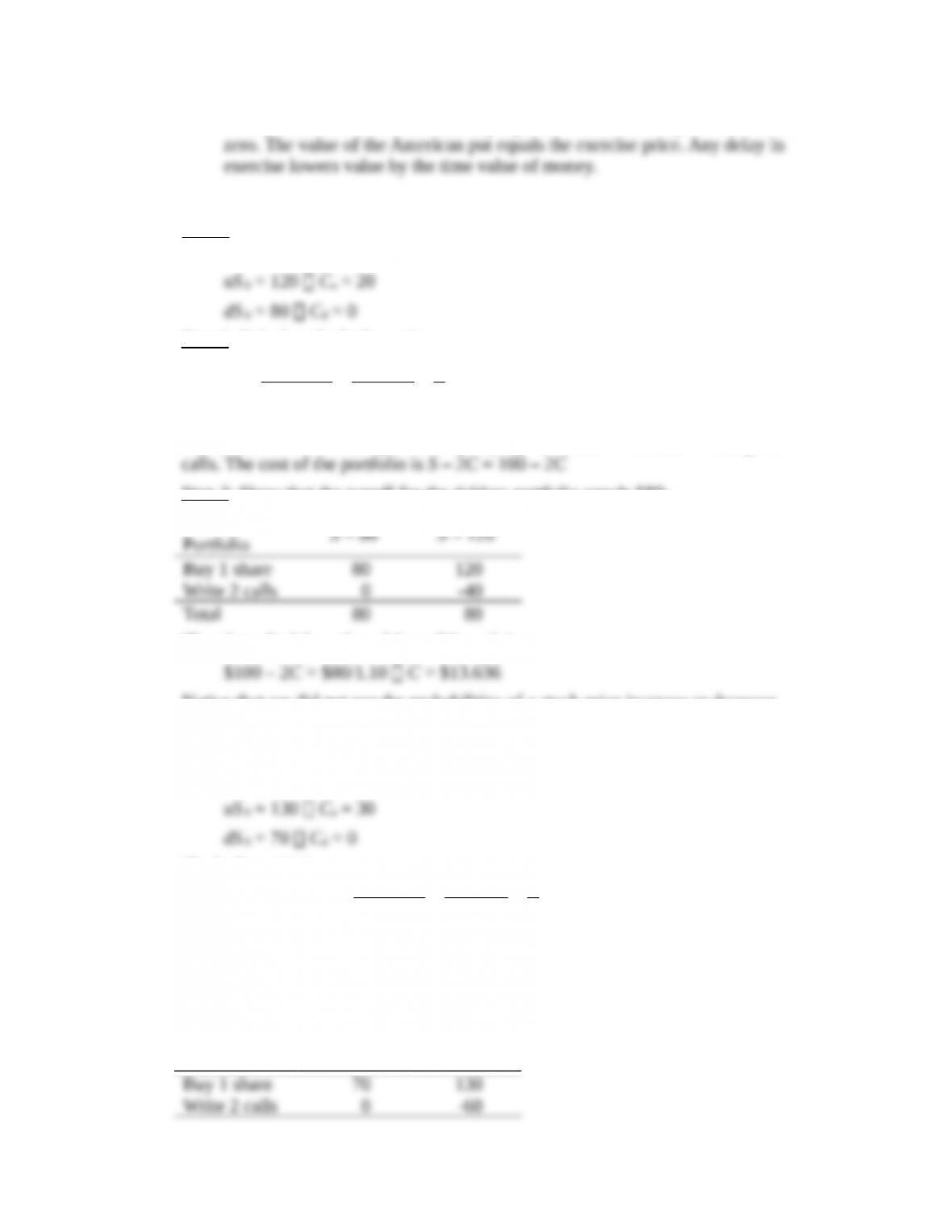

36. Step 1: Calculate the option values at expiration. The two possible stock prices and

the corresponding call values are:

Step 2: Calculate the hedge ratio.

0 0

20 0 1

120 80 2

u d

C C

HuS dS

––

= = =

– –

Therefore, form a riskless portfolio by buying one share of stock and writing two

Step 3: Show that the payoff for the riskless portfolio equals $80:

Riskless

Therefore, find the value of the call by solving

Notice that we did not use the probabilities of a stock price increase or decrease.

These are not needed to value the call option.

37. The two possible stock prices and the corresponding call values are:

The hedge ratio is

0 0

30 0 1

130 70 2

u d

C C

HuS dS

––

= = =

– –

Form a riskless portfolio by buying one share of stock and writing two calls. The

cost of the portfolio is: S – 2C = 100 – 2C

The payoff for the riskless portfolio equals $70:

Riskless

Portfolio S = 70 S = 130

21-10

CHAPTER 21: OPTION VALUATION

Therefore, find the value of the call by solving

Here, the value of the call is greater than the value in the lower-volatility scenario.

21-11