S

T

145 150

Payof

Write call Write put

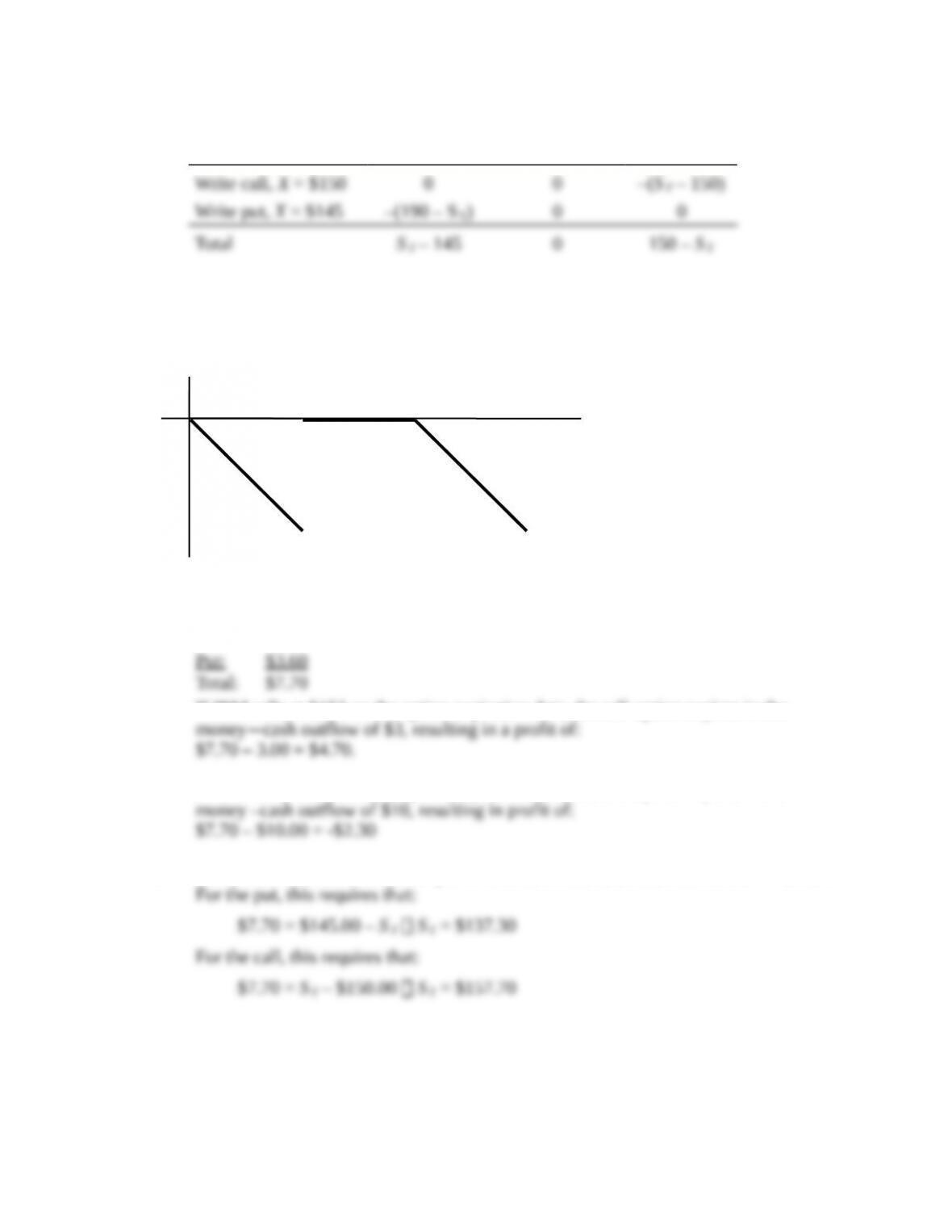

20. a.

Position S T < 145 145 S T 150 S T > 150

b. Proceeds from writing options:

Call: $4.10

If IBM sells at $153 on the option expiration date, the call option expires in the

If IBM sells at $160 on the option expiration date, the call option expires in the

c. You break even when either the put or the call results in a cash outflow of -$1.24.

d. The investor is betting that IBM stock price will have low volatility. This position is

similar to a straddle.

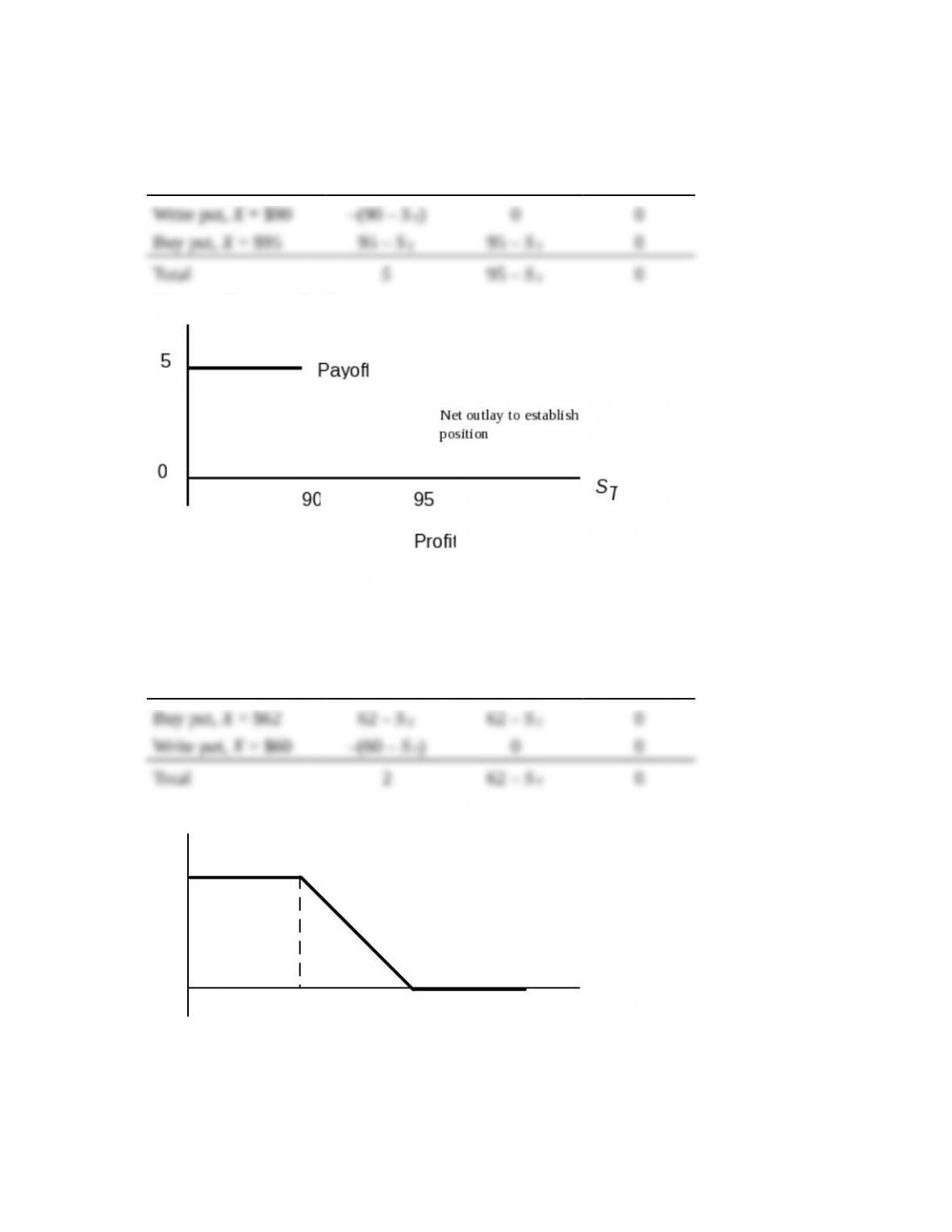

21. The put with the higher exercise price must cost more. Therefore, the net outlay to establish

the portfolio is positive.

Position S T < 90 90 S T 95 S T > 95

The payoff and profit diagram is:

22. Buy the X = 62 put (which should cost more but does not) and write the X = 60 put. Since

the options have the same price, your net outlay is zero. Your proceeds at expiration may be

positive, but cannot be negative.

Position S T < 60 60 S T 62 S T > 62

0 ST

2

60 62

Payoff = Profit (because net investment = 0)

23. Put-call parity states that:

0( ) (Dividends)P C S PV X PV= – + +

Solving for the price of the call option:

0( ) (Dividends)C S PV X PV P= – – +

$100 $2

$100 $7

(1.05) (1.05)

$9.86

C= – – +

=

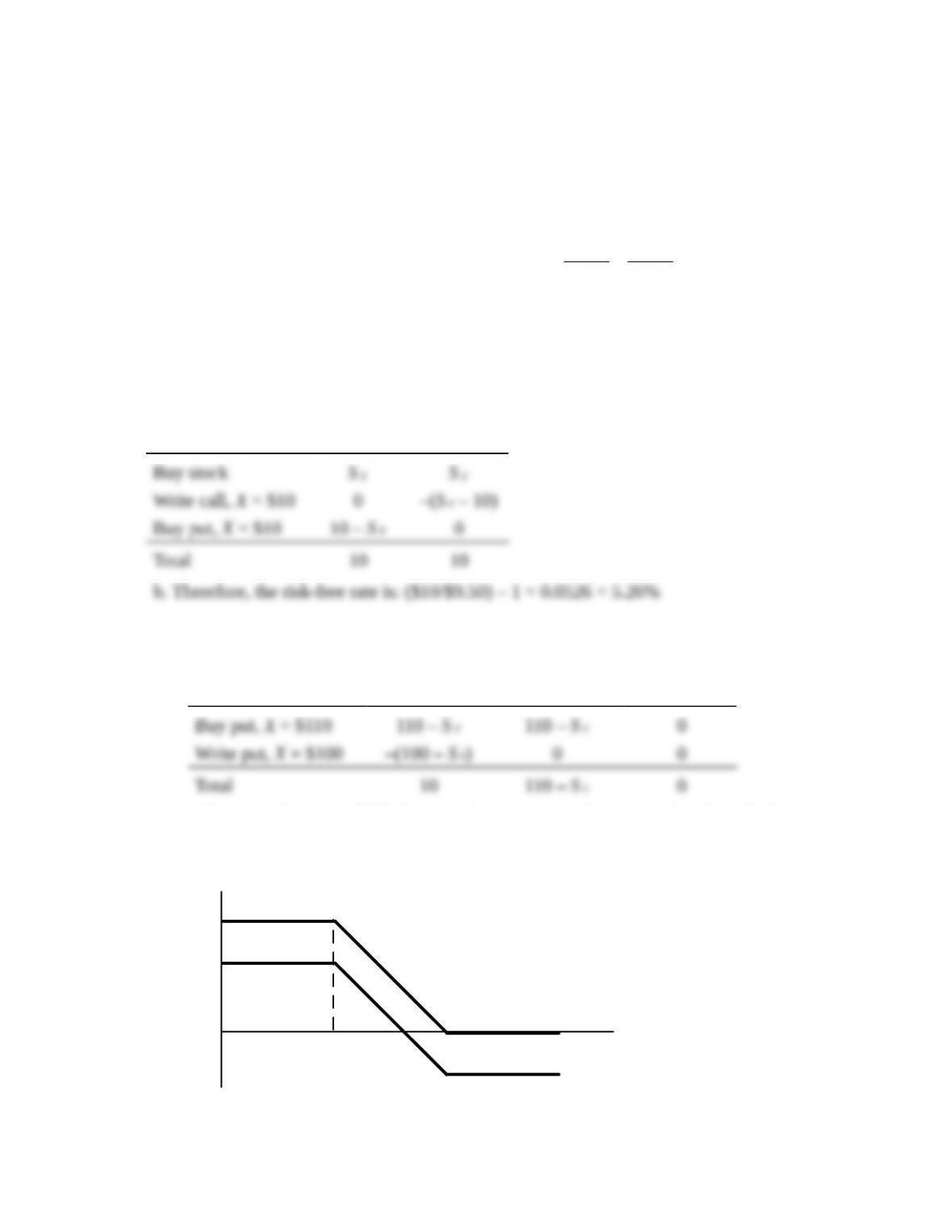

24. a. The following payoff table shows that the portfolio is riskless with time-T value equal to

$10:

Position S T ≤ 10 S T > 10

Buy stock S T S T

Write call, X = $10 0 –(S T – 10)

Buy put, X = $10 10 – S T 0

Total 10 10

b. Therefore, the risk-free rate is: ($10/$9.50) – 1 = 0.0526 = 5.26%

25. a., b.

Position S T < 100 100 S T 110 S T > 110

The net outlay to establish this position is positive. The put you buy has a higher

exercise price than the put you write, and therefore must cost more than the put that

you write. Therefore, net profits will be less than the payoff at time T.

0 S

T

110

100

10

Payoff

Profit

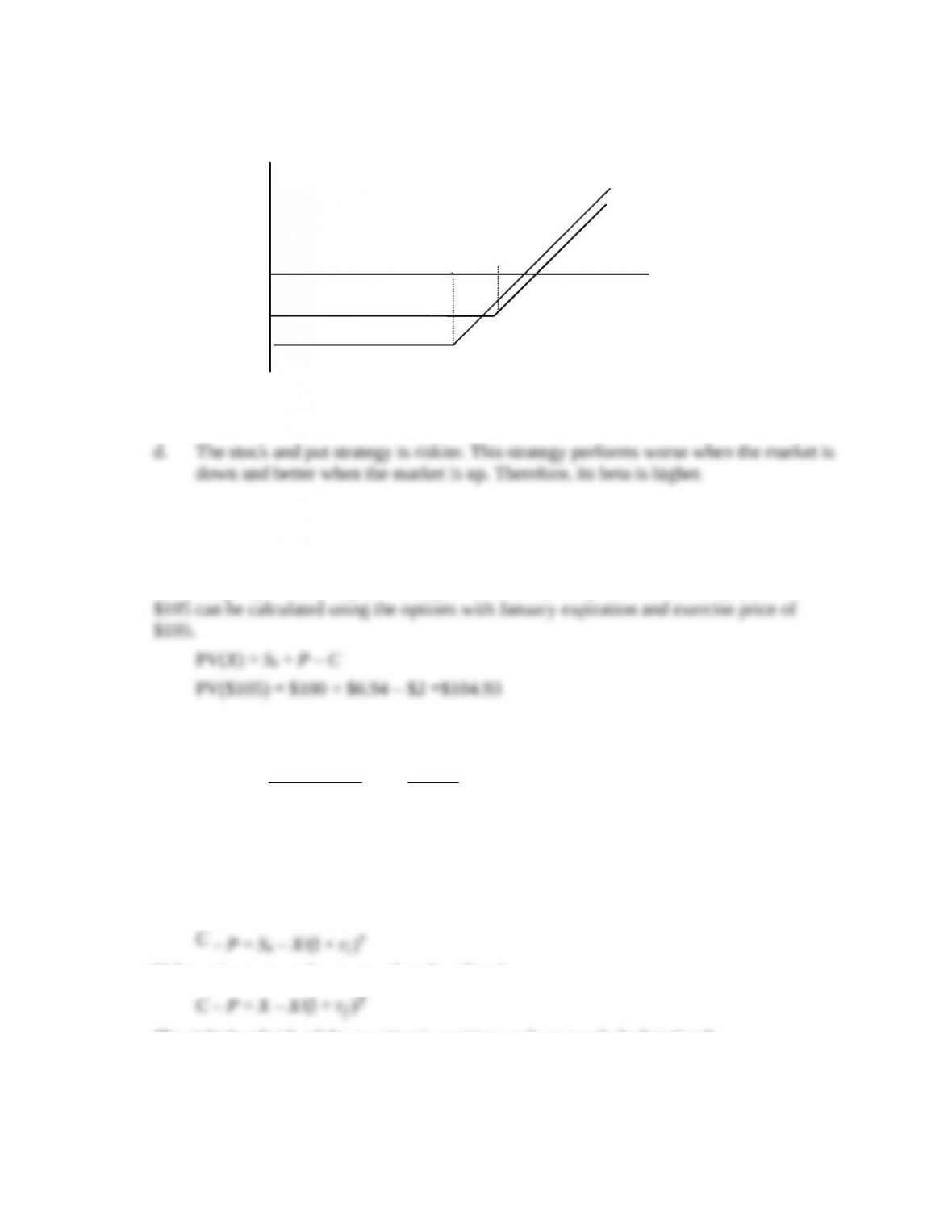

c. The value of this portfolio generally decreases with the stock price. Therefore, its beta

is negative.

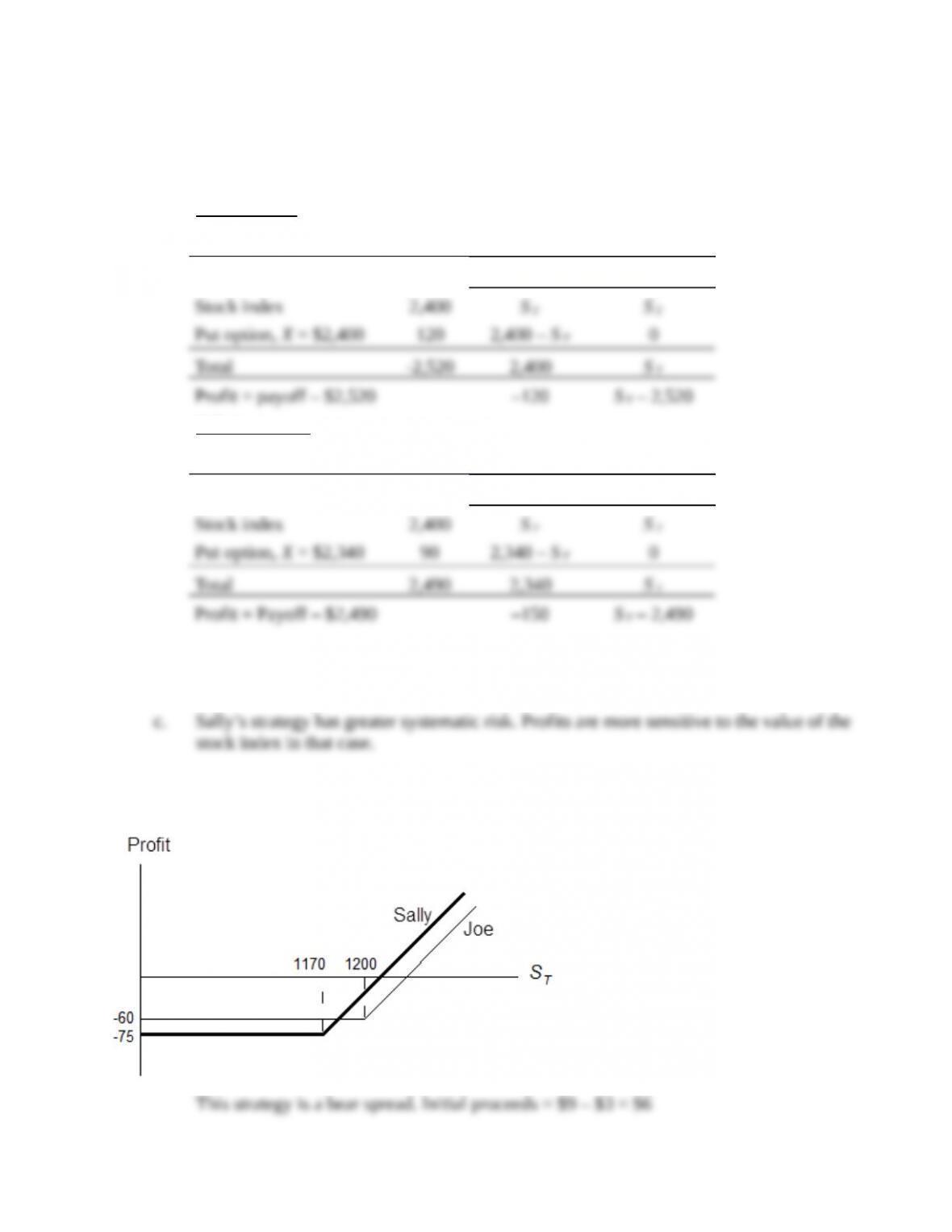

26. a. Joe’s strategy

Position Cost Payoff

S T 2,400 S T > 2,400

Sally’s strategy

Position Cost Payoff

S T 2,340 S T > 2,340

b. Sally does better when the stock price is high, but worse when the stock price is low.

27. a., b. (See graph)

The payoff is either negative or zero:

Position S T < 50 50 S T 60 S T > 60

c. Breakeven occurs when the payoff offsets the initial proceeds of $6, which occurs at

0

S

T

50 60

6

-10

– 4

Profit

Payoff

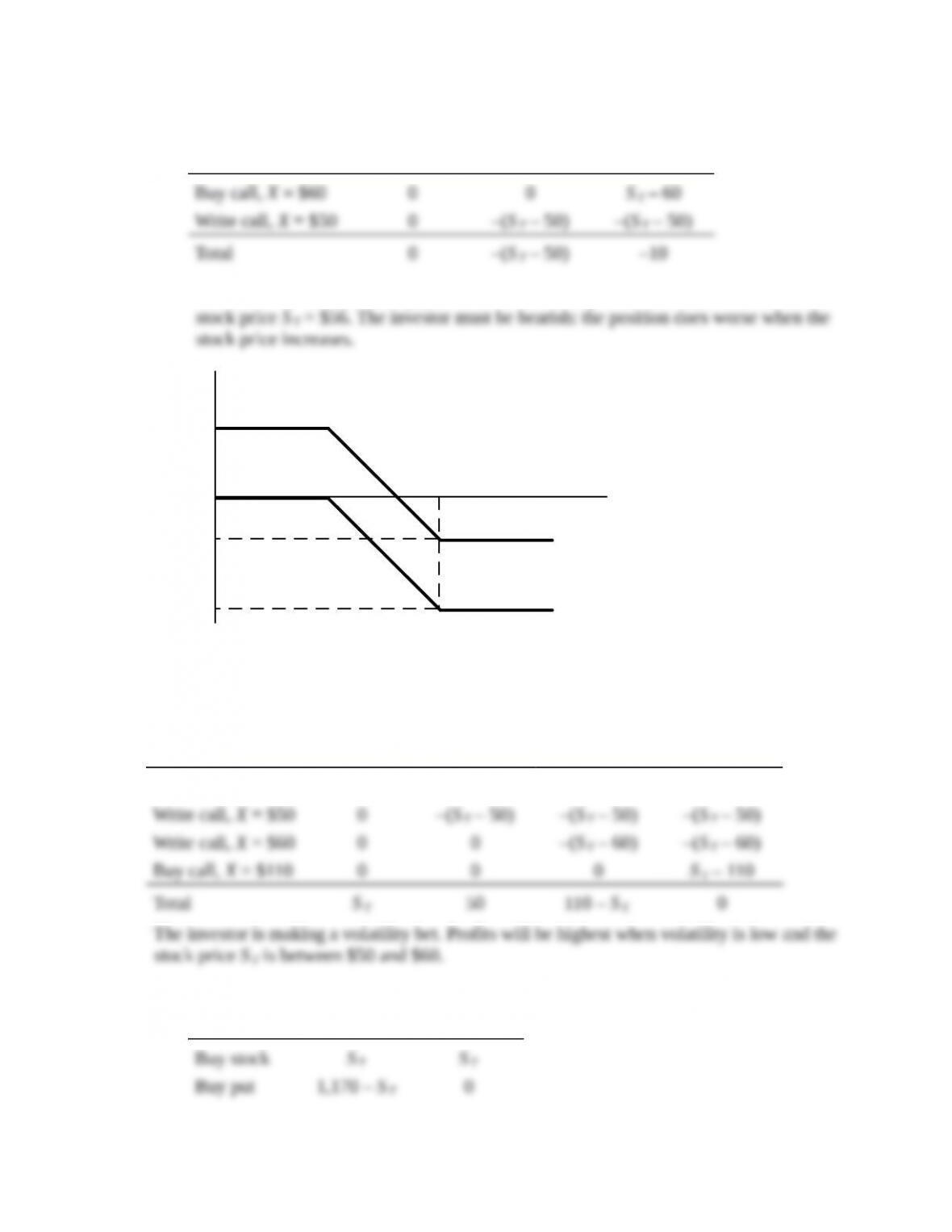

28. Buy a share of stock, write a call with X = $50, write a call with X = $60, and buy a call

with X = $110.

Position S T < 50 50 S T 60 60 < S T 110 S T > 110

Buy stock S T S T S T S T

29. a.

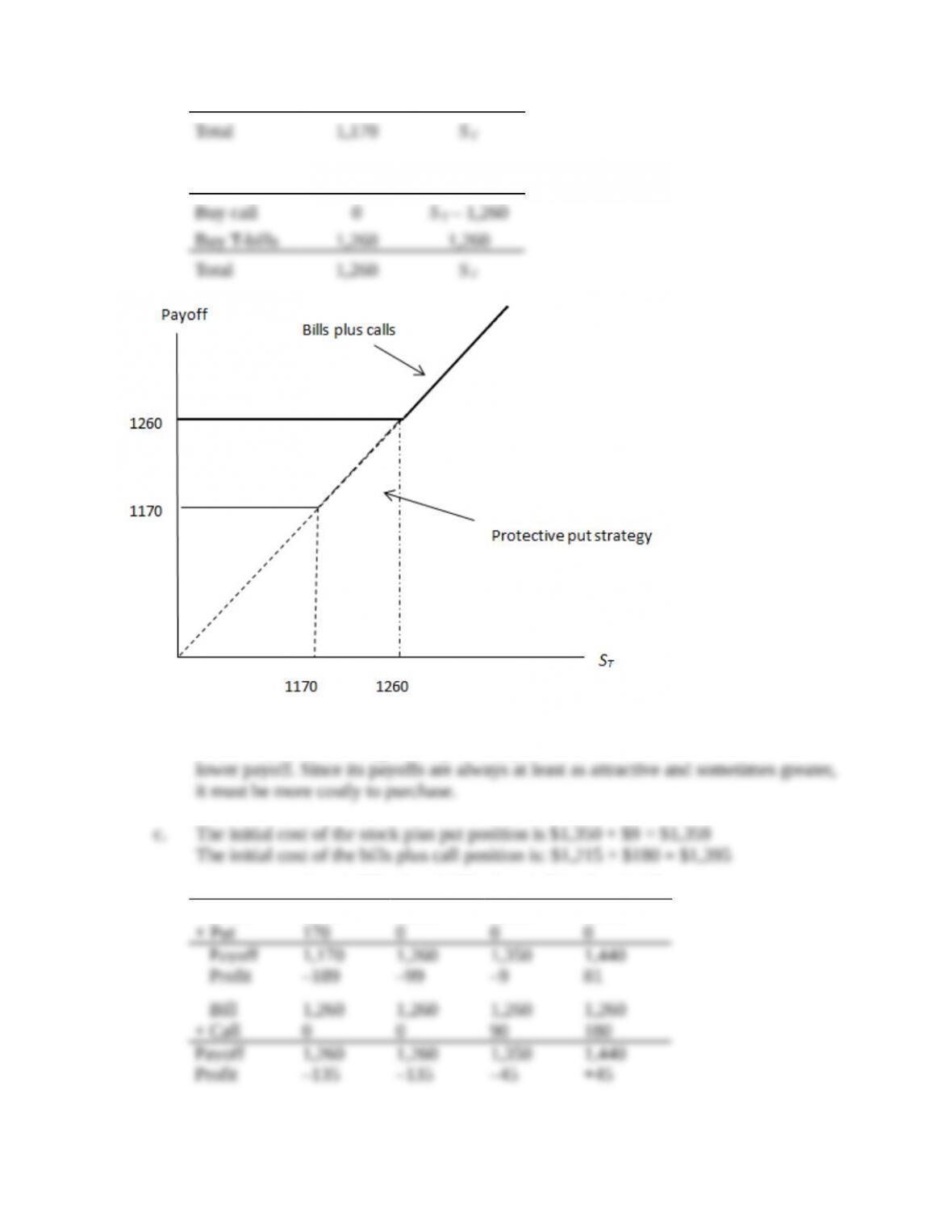

Position S T ≤ 1,179 S T > 1,170

Position S T ≤ 1,260 S T > 1,260

b. The bills plus call strategy has a greater payoff for some values of S T and never a

S T = 1,000 S T = 1,260 S T = 1,350 S T = 1,440

Stock

1,000

1,260

1,350

1,440

Profit

Bills plus calls

Protective put

-135

-189

1170

1260

S

T

e. Parity is not violated because these options have different exercise prices. Parity

applies only to puts and calls with the same exercise price and expiration date.

30. According to put-call parity (assuming no dividends), the present value of a payment of

12

( ) :

105 1.008

104.93

.8%

n

f

f

f

f

Effective Annual Yield EAY

FaceValue

EAY PV

r

æ ö æ ö

= = = ®

ç ÷ ç ÷

ç ÷ è ø

è ø

=

31. From put-call parity:

If the options are at the money, then S0 = X and

The right-hand side of the equation is positive, and we conclude that C > P.

CFA PROBLEMS

1. a. Donie should choose the long strangle strategy. A long strangle option strategy

consists of buying a put and a call with the same expiration date and the same

underlying asset, but different exercise prices. In a strangle strategy, the call has an

exercise price above the stock price and the put has an exercise price below the stock

b. i. The maximum possible loss per share is $9, which is the total cost of the two

ii. The maximum possible gain is unlimited if the stock price moves outside the

breakeven range of prices.

2. i. Equity index-linked note: Unlike traditional debt securities that pay a scheduled rate

of coupon interest on a periodic basis and the par amount of principal at maturity, the

ii. Commodity-linked bear bond: Unlike traditional debt securities that pay a scheduled

rate of coupon interest on a periodic basis and the par amount of principal at maturity,

3. i. Conversion value of a convertible bond is the value of the security if it is converted

immediately. That is:

Conversion value = Market price of the common stock × Conversion ratio

ii. Market conversion price is the price that an investor effectively pays for the common

stock if the convertible bond is purchased:

Market conversion price = Market price of the convertible bond/Conversion ratio

4. a. i. The current market conversion price is computed as follows:

Market conversion price = Market price of the convertible bond/Conversion ratio =

ii. The expected one-year return for the Ytel convertible bond is

Expected return = [(End of year price + Coupon)/Current price] – 1

iii. The expected one-year return for the Ytel common equity is:

Expected return = [(End of year price + Dividend)/Current price] – 1

b. The two components of a convertible bond’s value are

1. The straight bond value, which is the convertible bond’s value as a bond.

2. The option value, which is the value from a potential conversion to equity.

(i.) In response to the increase in Ytel’s common equity price, the straight bond value

should stay the same and the option value should increase.

(ii.) In response to the increase in interest rates, the straight bond value should

decrease and the option value should increase.

b. (i) The most the put writer can lose occurs when the stock price drops completely to