CHAPTER 20: OPTIONS MARKETS: INTRODUCTION

CHAPTER 20: OPTIONS MARKETS: INTRODUCTION

PROBLEM SETS

1. Options provide numerous opportunities to modify the risk profile of a portfolio.

The simplest example of an option strategy that increases risk is investing in an ‘all

options’ portfolio of at the money options (as illustrated in the text). The leverage

provided by options makes this strategy very risky, and potentially very profitable.

2. Buying a put option on an existing portfolio provides portfolio insurance, which is

protection against a decline in the value of the portfolio. In the event of a decline in

value, the minimum value of the put-plus-stock strategy is the exercise price of the

3. An investor who writes a call on an existing portfolio takes a covered call position.

If, at expiration, the value of the portfolio exceeds the exercise price of the call, the

writer of the covered call can expect the call to be exercised, so that the writer of

4. An option is out of the money when exercise of the option would be unprofitable. A

call option is out of the money when the market price of the underlying stock is less

than the exercise price of the option. If the stock price is substantially less than the

exercise price, then the likelihood that the option will be exercised is low, and

20-1

CHAPTER 20: OPTIONS MARKETS: INTRODUCTION

A call is in the money when the market price of the stock is greater than the exercise price

of the option. If stock price is substantially greater than exercise price, then the price of

the option approaches the order of magnitude of the price of the stock. Also, since such

5.

Cost Payoff Profit

a.

Call option, X = $145.00

$5.18

$5.00

-$0.18

b. Put option, X = $145.00 0.48 0.00 -0.48

6. In terms of dollar returns, based on a $10,000 investment:

Price of Stock 6 Months from Now

Stock Price

$ 80

$ 100

$ 110

$ 120

All stocks (100 shares)

8,000

10,000

11,000

12,000

Price of Stock 6 Months from Now

Stock Price

$80

$100

$110

$120

All stocks (100 shares)

-20%

0%

10%

20%

20-2

CHAPTER 20: OPTIONS MARKETS: INTRODUCTION

All options

All stocks

Bills plus options

ST

100

–100

0

– 6.4

Rate of return (%)

100

110

7. a. From put-call parity:

0.25

100

10 100 $7.65

(1 ) 1.10

T

f

X

P C S r

= – + = – + =

+

b. Purchase a straddle, i.e., both a put and a call on the stock. The total cost of the

8. a. From put-call parity:

0.25

50

4 50 $5.18

(1 ) 1.10

T

f

X

C P S r

= + – = + – =

+

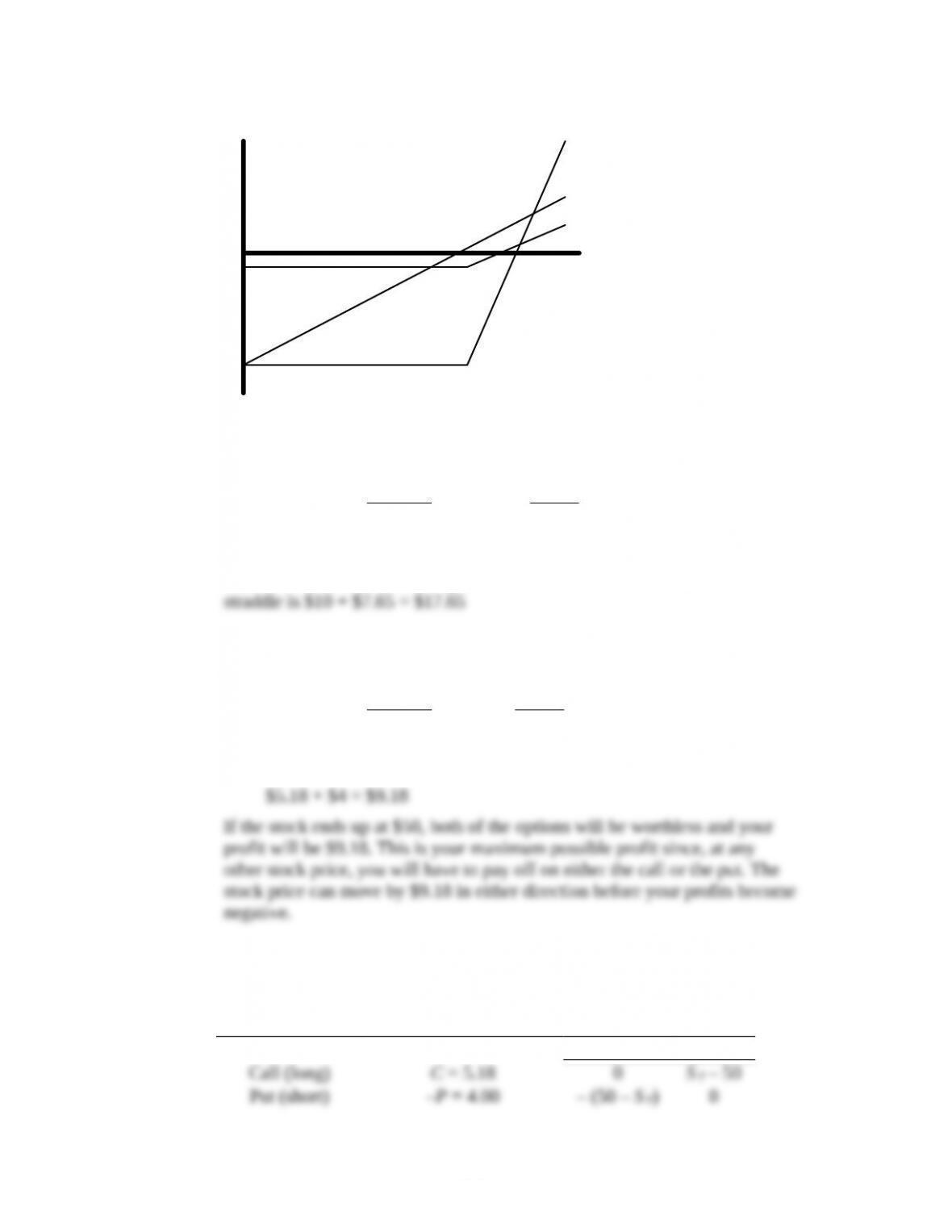

b. Sell a straddle, i.e., sell a call and a put, to realize premium income of

c. Buy the call, sell (write) the put, lend $50/(1.10)1/4

The payoff is as follows:

Position Immediate CF CF in 3 months

S T ≤ X S T > X

20-3

CHAPTER 20: OPTIONS MARKETS: INTRODUCTION

82.48

10.1

50

Total

C – P +

00.50

10.1

50

4/1

S T S T

By the put-call parity theorem, the initial outlay equals the stock price:

S0 = $50

In either scenario, you end up with the same payoff as you would if you

bought the stock itself.

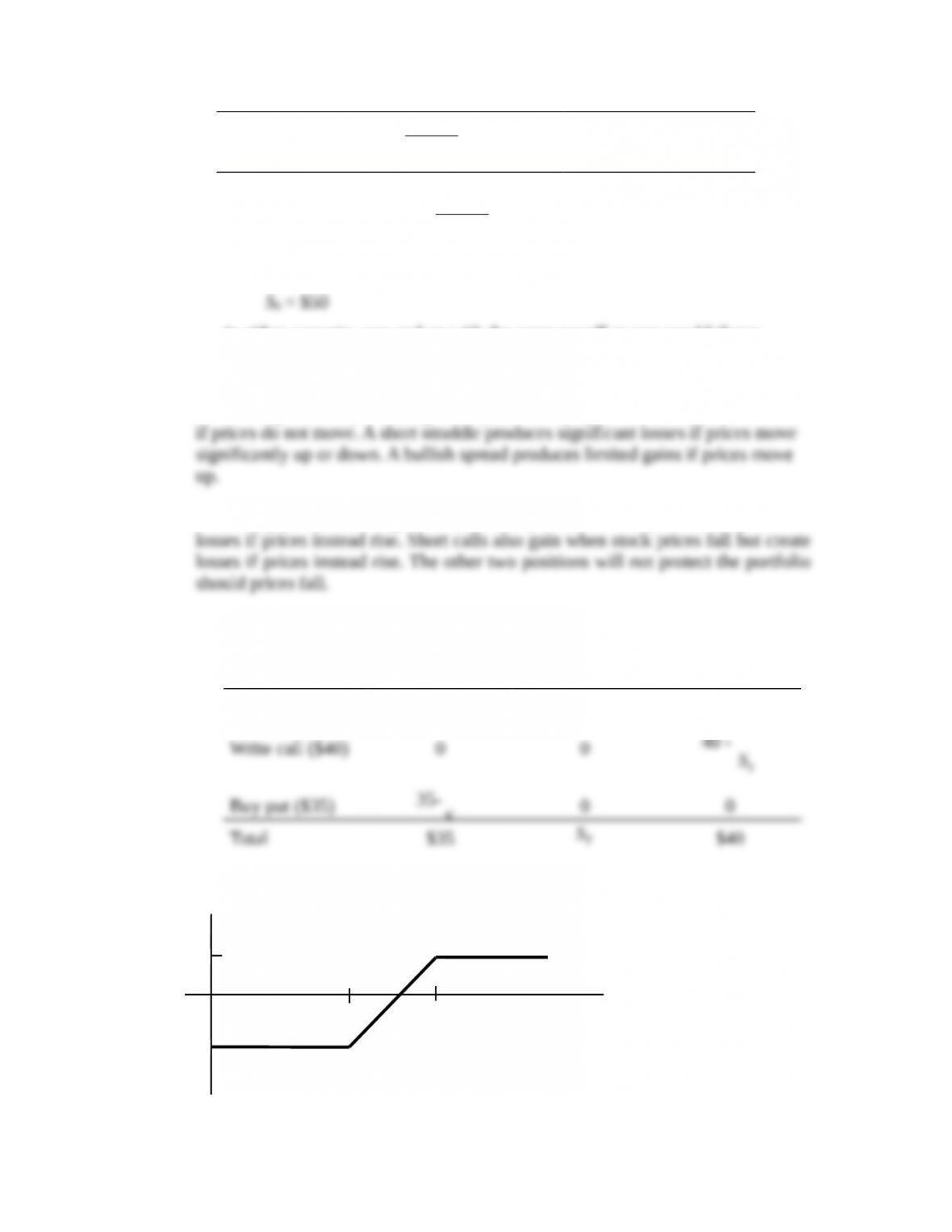

9. a. i. A long straddle produces gains if prices move up or down and limited losses

b. i. Long put positions gain when stock prices fall and produce very limited

10. Note that the price of the put equals the revenue from writing the call, net initial

cash outlays = $38.00

Position

T

S

< 35

35

T

S

40

40 <

T

S

Buy stock

T

S

T

S

T

S

T

S

T

S

35-

$35

Profit

$2

-$3

$40

20-4

CHAPTER 20: OPTIONS MARKETS: INTRODUCTION

11. Answers may vary. For $5,000 initial outlay, buy 5,000 puts, write 5,000 calls:

Position

T

S

= $30

T

S

= $40

T

S

=$50

Stock portfolio $150,000 $200,000 $250,000

Compare this to just holding the portfolio:

Position

T

S

= $30

T

S

= $40

T

S

=$50

12. a.

CHAPTER 20: OPTIONS MARKETS: INTRODUCTION

X

2

– X

1

S

T

X

1

X

2

Payoff

X

3

b.

Position S T < X1X1 S T X2

X2X2XX2

X2 < S T

X

1

S

T

X

1

X

2

Payoff

14.

Position S T < X1X1 S T X2

XX2

X2 < S T

20-6

CHAPTER 20: OPTIONS MARKETS: INTRODUCTION

Payoff

0

S

T

X

1

X

2

Payoff

–(X

2

–

X

1

)

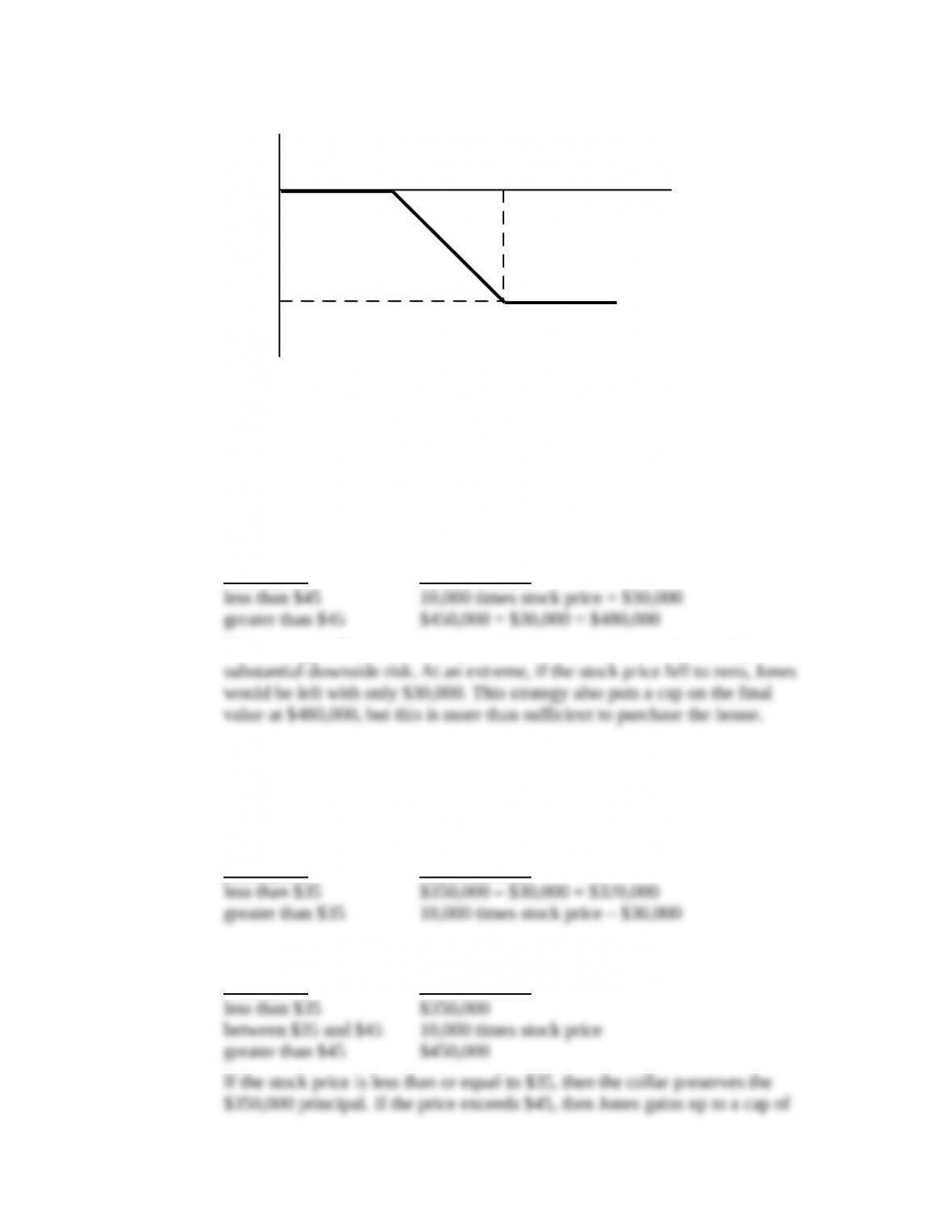

15. a. By writing covered call options, Jones receives premium income of $30,000.

If, in January, the price of the stock is less than or equal to $45, then Jones

will have his stock plus the premium income. But the most he can have at that

time is ($450,000 + $30,000) because the stock will be called away from him

if the stock price exceeds $45. (We are ignoring here any interest earned over

this short period of time on the premium income received from writing the

option.) The payoff structure is

Stock price Portfolio value

This strategy offers some extra premium income but leaves Jones subject to

b. By buying put options with a $35 strike price, Jones will be paying $30,000 in

premiums in order to ensure a minimum level for the final value of his

position. That minimum value is ($35 × 10,000) – $30,000 = $320,000.

This strategy allows for upside gain, but exposes Jones to the possibility of a

moderate loss equal to the cost of the puts. The payoff structure is:

Stock price Portfolio value

c. The net cost of the collar is zero. The value of the portfolio will be as follows:

Stock price Portfolio value

20-7

CHAPTER 20: OPTIONS MARKETS: INTRODUCTION

The best strategy in this case would be (c) since it satisfies the two

Our ranking would be: (1) strategy c; (2) strategy b; (3) strategy a.

16. Using Excel, with Profit Diagram on next page.

Stock Prices

Beginning Market

Price 116.5 Price Profit

Ending Market Price 130 Ending Straddle

Buying Options: 50 42.80

Call Options Strike Price Payoff Profit Return % 60 32.80

110 -17.20

Put Options Strike Price Payoff Profit Return % 120 -27.20

170 2.80

Straddle Price Payoff Profit Return % 180 12.80

Selling Options: Ending Bullish

Call Options Strike Price Payoff Profit Return % Stock

Price Spread

90 -3.2

Put Options Strike Price Payoff Profit Return % 100 -3.2

150 6.8

20-8

CHAPTER 20: OPTIONS MARKETS: INTRODUCTION

Money Spread Price Payoff Profit 160 6.8

Bullish Spread 170 6.8

210 6.8

Profit diagram for problem 16:

Straddle Bullish Spread

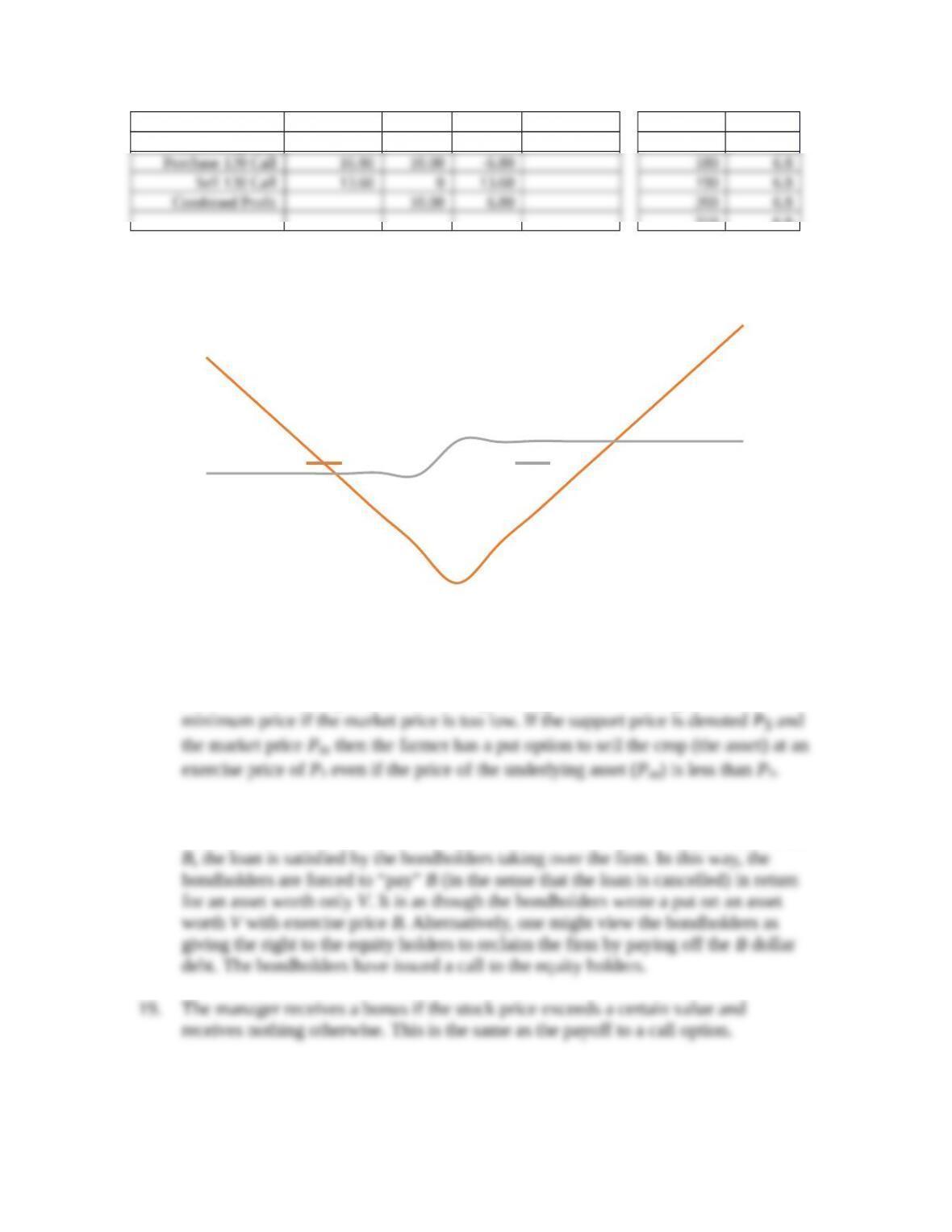

17. The farmer has the option to sell the crop to the government for a guaranteed

18. The bondholders have, in effect, made a loan that requires repayment of B dollars,

where B is the face value of bonds. If, however, the value of the firm (V) is less than

20-9