CHAPTER 18: EQUITY VALUATION MODELS

CHAPTER 18: EQUITY VALUATION MODELS

PROBLEM SETS

1. Theoretically, dividend discount models can be used to value the stock of rapidly

growing companies that do not currently pay dividends; in this scenario, we

would be valuing expected dividends in the relatively more distant future.

However, as a practical matter, such estimates of payments to be made in the

2. It is most important to use multistage dividend discount models when valuing

companies with temporarily high growth rates. These companies tend to be

3. The intrinsic value of a share of stock is the individual investor’s assessment of

the true worth of the stock. The market capitalization rate is the market

4. First estimate the amount of each of the next two dividends and the terminal

5. The required return is 9%.

$1.22 (1.05) 0.05 .09,or 9%

$32.03

k´

= + =

6. The Gordon DDM uses the dividend for period (t+1) which would be 1.05.

18-1

CHAPTER 18: EQUITY VALUATION MODELS

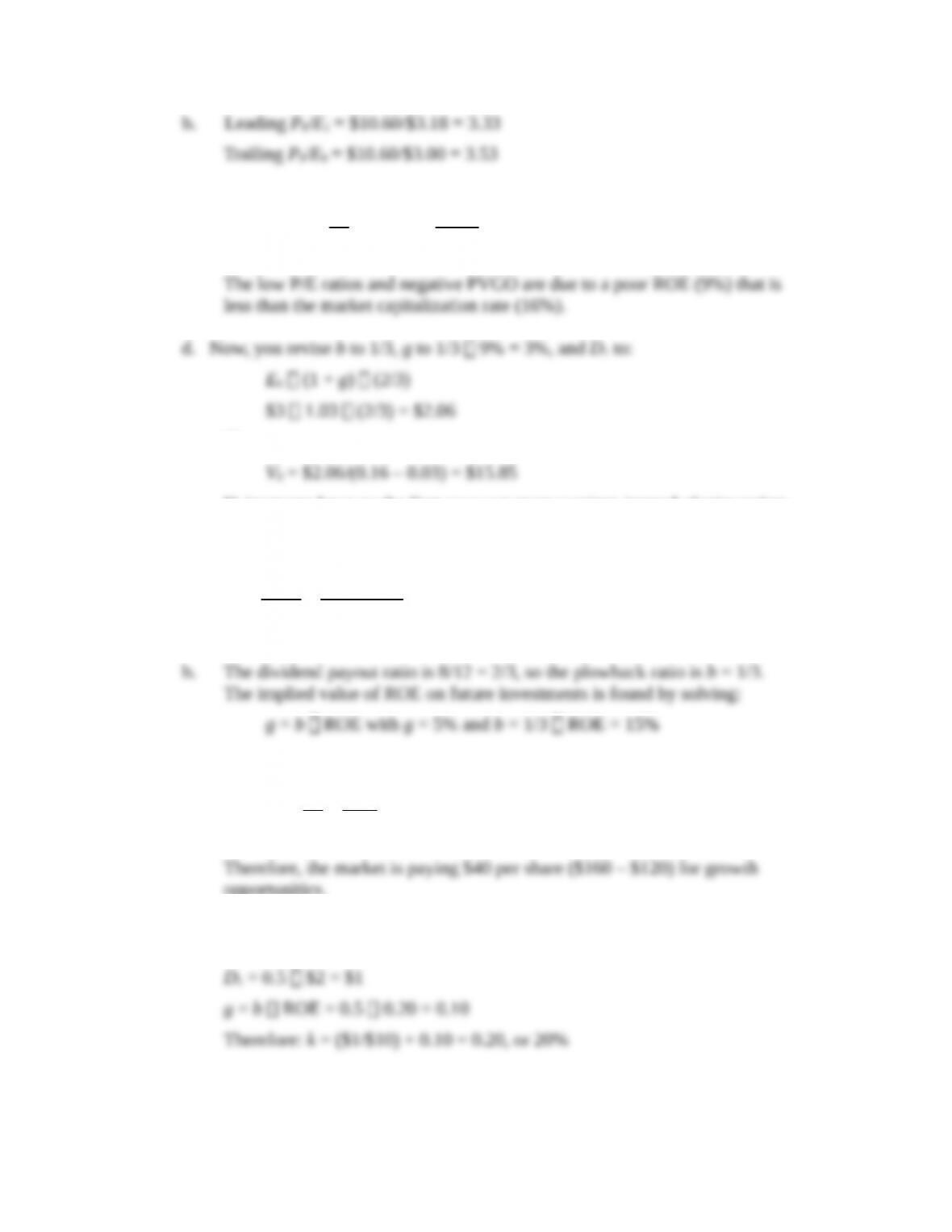

c.

1

0

$3.18

$10.60 $9.275

0.16

E

PVGO P k

= – = – =-

The low P/E ratios and negative PVGO are due to a poor ROE (9%) that is

less than the market capitalization rate (16%).

d. Now, you revise b to 1/3, g to 1/3 9% = 3%, and D1 to:

E0 (1 + g) (2/3)

$3 1.03 (2/3) = $2.06

Thus:

V0 increases because the firm pays out more earnings instead of reinvesting

a poor ROE. This information is not yet known to the rest of the market.

11. a.

1

0

$8 $160

0.10 0.05

D

Pk g

= = =

– –

b. The dividend payout ratio is 8/12 = 2/3, so the plowback ratio is b = 1/3.

The implied value of ROE on future investments is found by solving:

g = b ROE with g = 5% and b = 1/3 ROE = 15%

c. Assuming ROE = k, price is equal to:

1

0

$12 $120

0.10

E

Pk

= = =

Therefore, the market is paying $40 per share ($160 – $120) for growth

opportunities.

12. a. k = D1/P0 + g

b. Since k = ROE, the NPV of future investment opportunities is zero:

18-3

CHAPTER 18: EQUITY VALUATION MODELS

1

0

$10 $10 0

E

PVGO P k

= – = – =

c. Since k = ROE, the stock price would be unaffected by cutting the dividend

and investing the additional earnings.

13. a. k = rf + β [E(rM ) – rf ] = 8% + 1.2(15% – 8%) = 16.4%

0

0

(1 ) $4 1.12 $101.82

0.164 0.12

D g

Vk g

+´

= = =

– –

b. P1 = V1 = V0(1 + g) = $101.82 1.12 = $114.04

1 1 0

0

$4.48 $114.04 $100

( ) 0.1852,or 18.52%

$100

D P P

E r P

–

++ –

= = =

14.

Time: 0 1 5 6

E t

$10.000

$12.000

$24.883

$27.123

The year-6 earnings estimate is based on growth rate of 0.15 × (1-0.40) = 0.09.

a.

6

5

$10.85 $180.82

0.15 0.09

D

Vk g

= = = Þ

– –

5

05 5

$180.82 $89.90

(1 ) 1.15

V

Vk

= = =

+

b. The price should rise by 15% per year until year 6: because there is no

c. The price should rise by 15% per year until year 6: because there is no

dividend, the entire return must be in capital gains. Therefore the price in

two years should be $118.89.

d.

18-4

Time: 0 1 5 6

E t

$10.000

$12.000

$24.883

$27.869

CHAPTER 18: EQUITY VALUATION MODELS

The year-6 earnings estimate is based on growth rate of 0.15 × (1-0.20) = 0.12.

6

5

$5.57 $185.79

0.15 0.12

D

Vk g

= = = Þ

– –

5

05 5

$185.79 $92.37

(1 ) 1.15

V

Vk

= = =

+

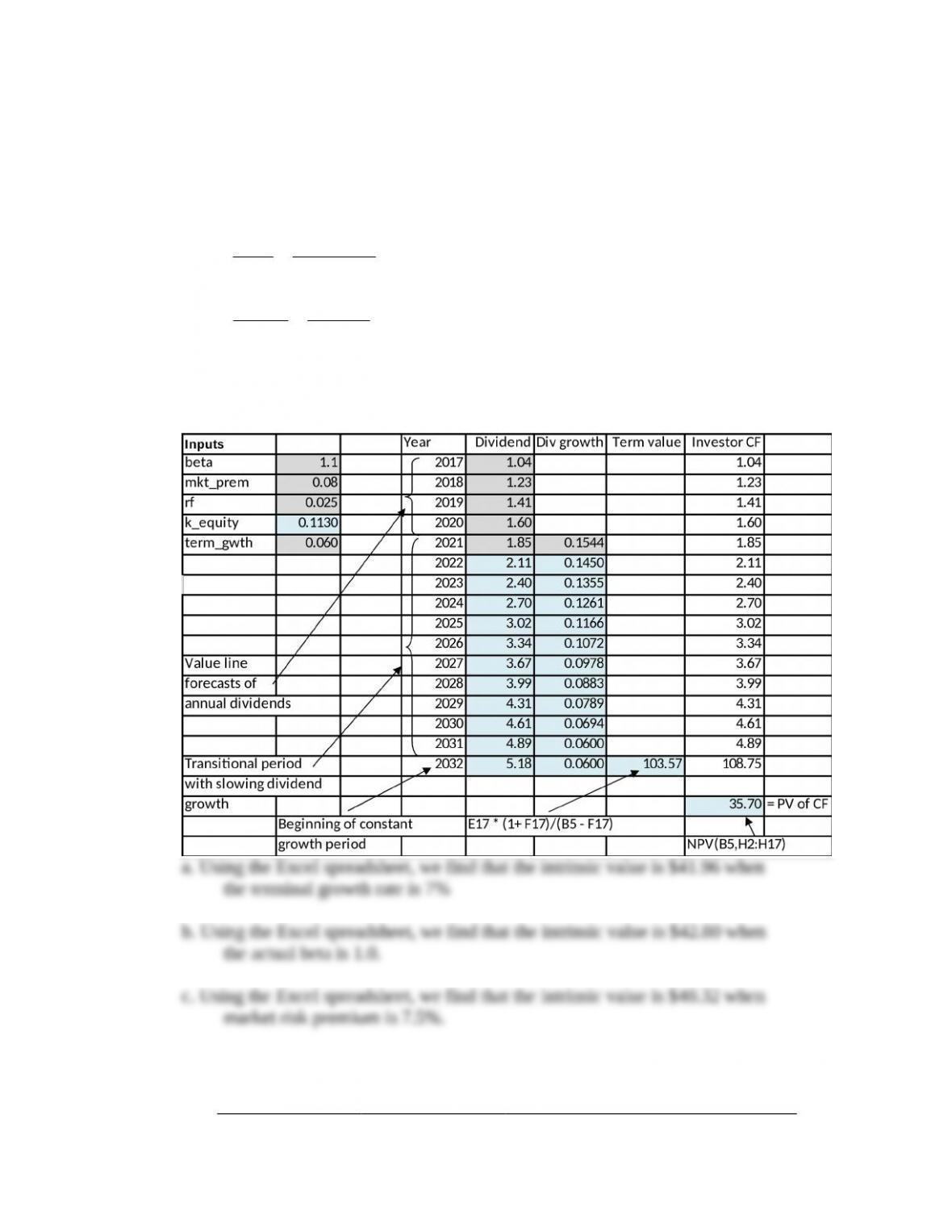

15. The base case solution is shown in the Excel spreadsheet below:

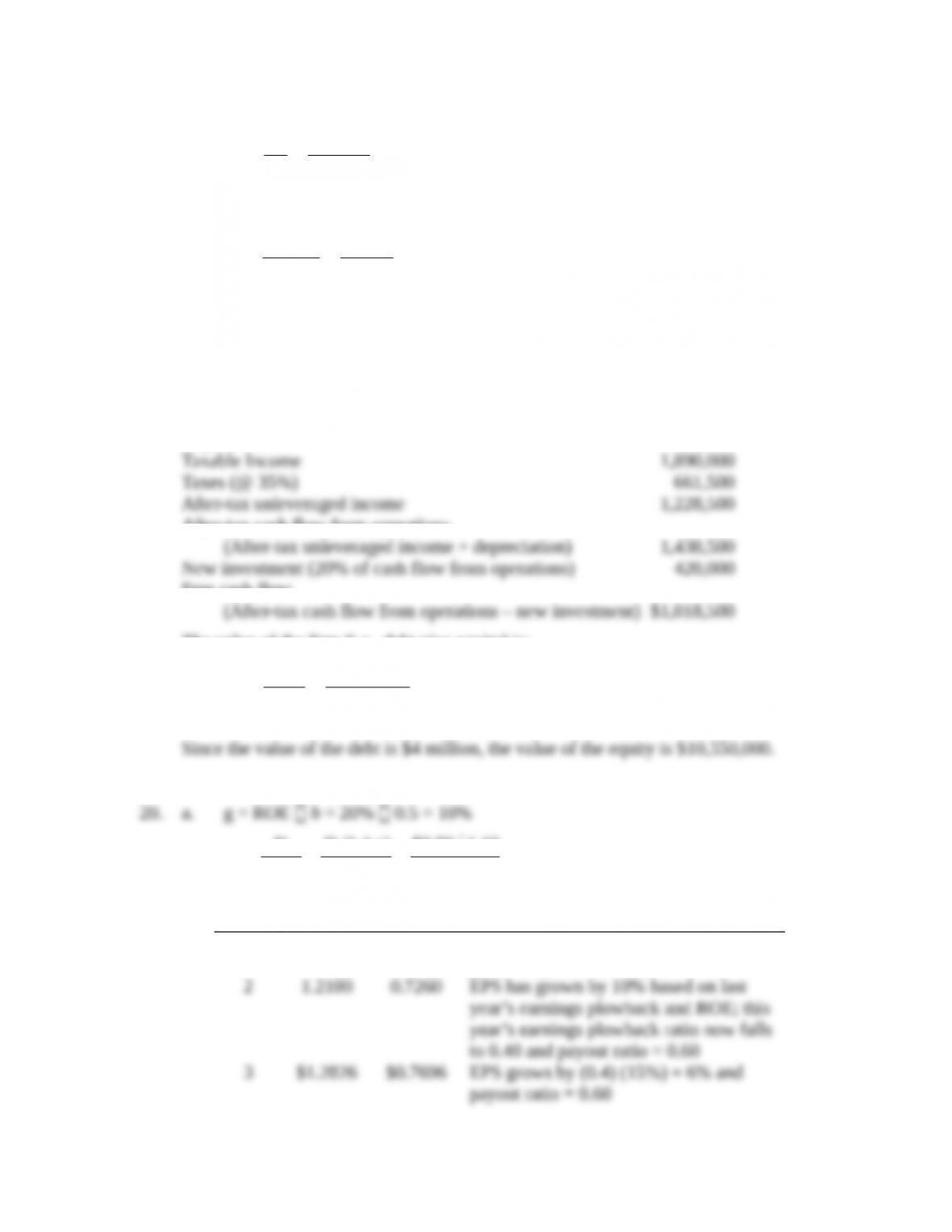

16. The solutions derived from Spreadsheet 18.2 are as follows:

Intrinsic Value:

FCFF

Intrinsic Value:

FCFE

Intrinsic Value

per Share: FCFF

Intrinsic Value

per Share: FCFE

18-5

CHAPTER 18: EQUITY VALUATION MODELS

a. 367,080 261,289 24.42 28.10

17.

Time: 0 1 2 3

D t

$1.0000

$1.2500

$1.5625

$1.953

g25.0% 25.0% 25.0% 5.0%

a. The dividend to be paid at the end of year 3 is the first installment of a

dividend stream that will increase indefinitely at the constant growth rate of

The expected price 2 years from now is:

The PV of expected dividends in years 1 and 2 is

13.2$

20.1

5625.1$

20.1

25.1$

2

Thus the current price should be: $9.04 + $2.13 = $11.17

b. Expected dividend yield = D1/P0 = $1.25/$11.17 = 0.112, or 11.2%

c. The expected price one year from now is the PV at that time of P2 and D2:

The implied capital gain is

The sum of the implied capital gains yield and the expected dividend yield

is equal to the market capitalization rate. This is consistent with the DDM.

18.

Time: 0 1 4 5

E t

$5.000

$6.000

$10.368

$10.368

D t$0.000 $0.000 $0.000 $10.368

Dividends = 0 for the next four years, so b = 1.0 (100% plowback ratio).

18-6

CHAPTER 18: EQUITY VALUATION MODELS

At time 2:

3

2

$0.7696 $8.551

0.15 0.06

D

Pk g

= = =

– –

At time 0:

02

$0.55 $0.726 $8.551 $7.493

1.15 (1.15)

V+

= + =

(Because the market is unaware of the changed competitive situation, it

believes the stock price should grow at 10% per year, in other words, no new

information is publicly available.)

($12.10 $11) $0.55 0.150,or 15.0%

$11

– + =

d. P1 = P0(1 + g) = $12.10 and P2 = $8.551 after the market becomes aware of the

changed competitive situation.

($8.551 $12.10) $0.726 0.233,or 23.3%

$12.10

– + =- –

e. P2 = $8.551 and P3 = $8.551 1.06 = $9.064 (The new growth rate is 6%.)

($9.064 $8.551) $0.7696 0.150,or 15.0%

$8.551

– + =

Moral: In normal periods when there is no special information, the stock

return = k = 15%. When special information arrives, all the abnormal return

accrues in that period, as one would expect in an efficient market.

18-8